CHAPTER 15

Stockholders’ Equity

SOLUTIONS TO B PROBLEMS

PROBLEM 15-1B

(a)

April 28

Cash (100,000 X $23) ……………………………………….. 2,300,000

July 16

Equipment ………………………………………………………. 76,000

Buildings ………………………………………………………… 240,000

August 8

Treasury Stock (750 X $26) ………………………………. 19,500

Cash ………………………………………………………… 19,500

September 17

PROBLEM 15-1B (Continued)

December 31

Retained Earnings …………………………………………… 467,000

Dividend Payable ………………………………………. 46,000*

December 31

Income Summary …………………………………………….. 96,900

Retained Earnings …………………………………….. 96,900

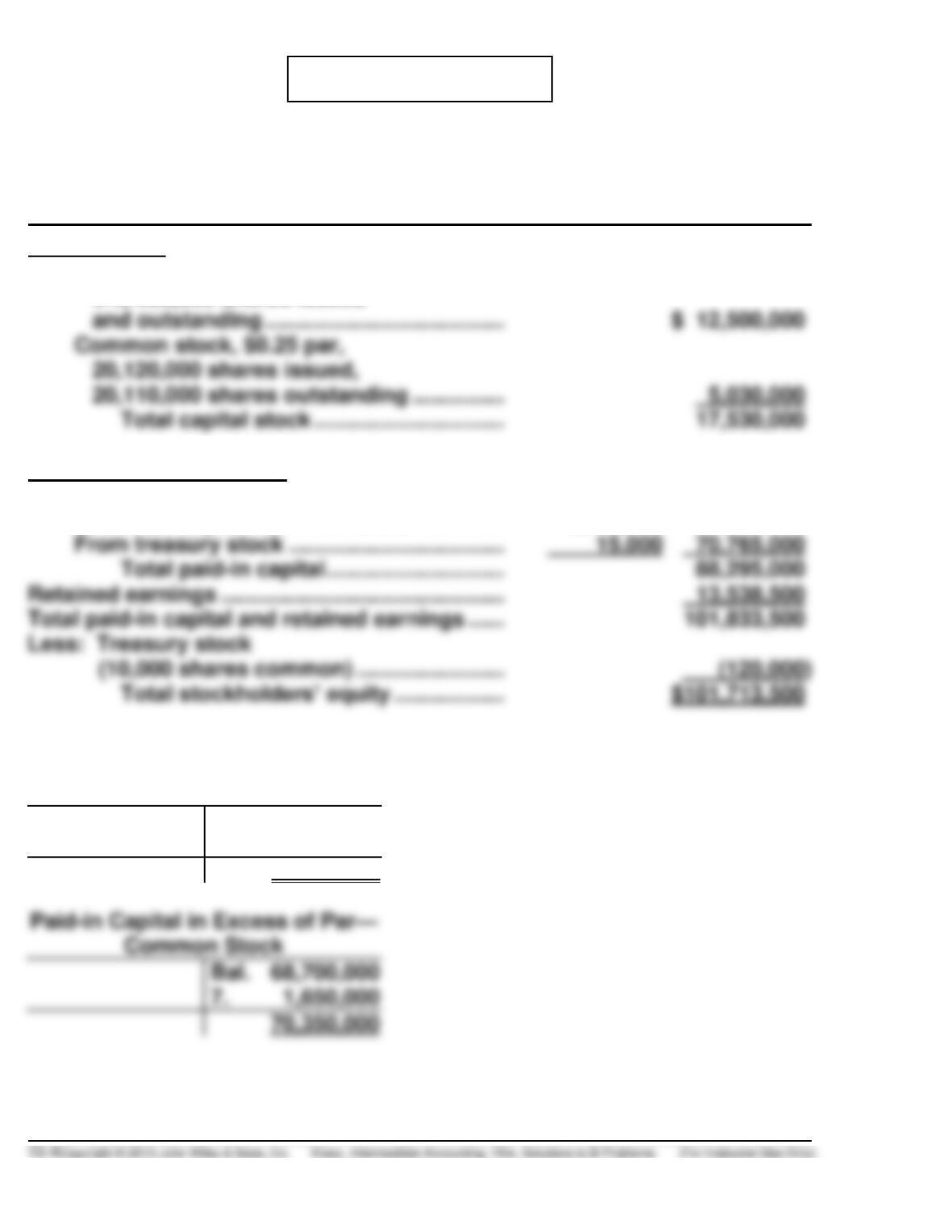

(b) ALLIGATOR CORPORATION

Stockholders’ Equity

December 31, 2014

Capital stock

Preferred stock—par value $100 per share,

6% cumulative and nonparticipating,

100,000 shares authorized,

PROBLEM 15-2B

(a) Feb. 16 Treasury Stock ($15 X 5,000) …………….. 75,000

Cash ……………………………………….. 75,000

Mar. 8 Cash ($16 X 200) ……………………………… 3,200

Paid-in Capital from Treasury

(b) LLP COMPANY

Stockholders’ Equity

June 30, 2014

Common stock, $1 par value, 120,000 shares

issued, 118,000 shares outstanding ……………… $120,000

Paid-in capital in excess of par—

common stock …………………………………………….. 833,000

Paid-in capital from treasury stock …………………… 6,000

Total paid-in capital ………………………………. 959,000

Retained earnings* ………………………………………….. 666,800

1,625,800

PROBLEM 15-3B

MERRIWEATHER COMPANY

Stockholders’ Equity

December 31, 2015

Capital Stock

Preferred stock, $50 par,

6%, 250,000 shares issued

Additional paid-in capital

In excess of par—preferred stock …………. $ 400,000

In excess of par—common stock ………….. 70,350,000

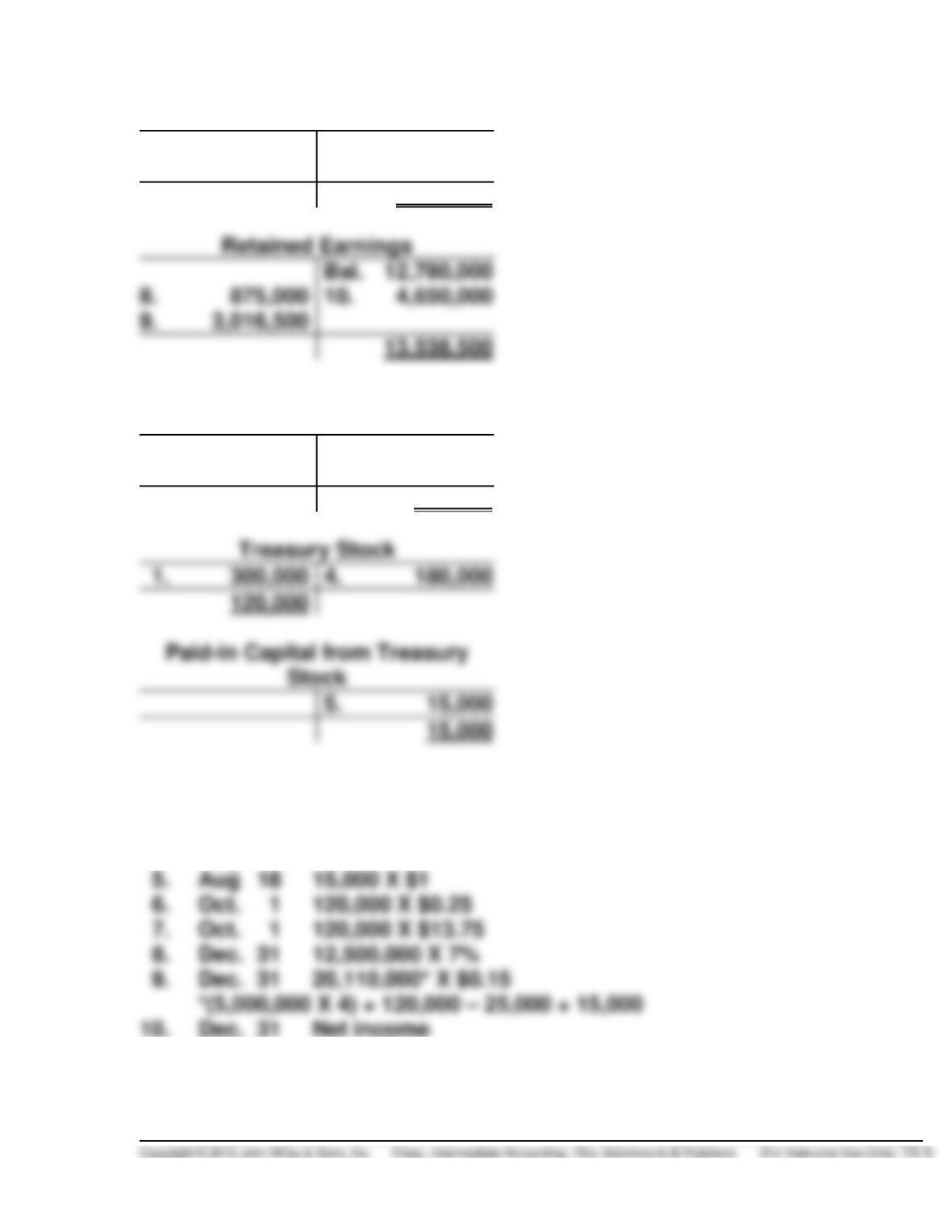

Supporting balances are indicated in the following T-Accounts.

Preferred Stock

Bal. 10,000,000

2. 2,500,000

12,500,000

Bal. 68,700,000

7. 1,650,000

70,350,000

PROBLEM 15-3B (Continued)

Common Stock

Bal. 5,000,000

6. 30,000

5,030,000

Bal. 12,780,000

Paid-in Capital in Excess of Par—

Preferred Stock

Bal. 350,000

3. 50,000

400,000

1. 300,000

4. 180,000

120,000

5. 15,000

1. Apr. 1 25,000 X $12

2. Jun. 18 50,000 X $50

3. Jun. 18 50,000 X $1

4. Aug. 18 15,000 X $12

PROBLEM 15-4B

-1-

Cash ………………………………………………………………………. 100,000

Discount on Bonds Payable …………………………………….. 1,020

-2-

Land (7,500 X $12) …………………………………………………… 90,000

Common Stock ………………………………………………… 7,500

-3-

Cash ………………………………………………………………………. 68,800

Preferred Stock ………………………………………………… 5,000

Paid-in Capital in Excess of Par—Preferred

Stock ($5,367 – $5,000) …………………………………… 367

Common Stock ………………………………………………… 5,000

PROBLEM 15-4B (Continued)

-4-

Equipment……………………………………………………………….. 21,900

Preferred Stock …………………………………………………. 5,000

Paid-in Capital in Excess of Par—Preferred

PROBLEM 15-5B

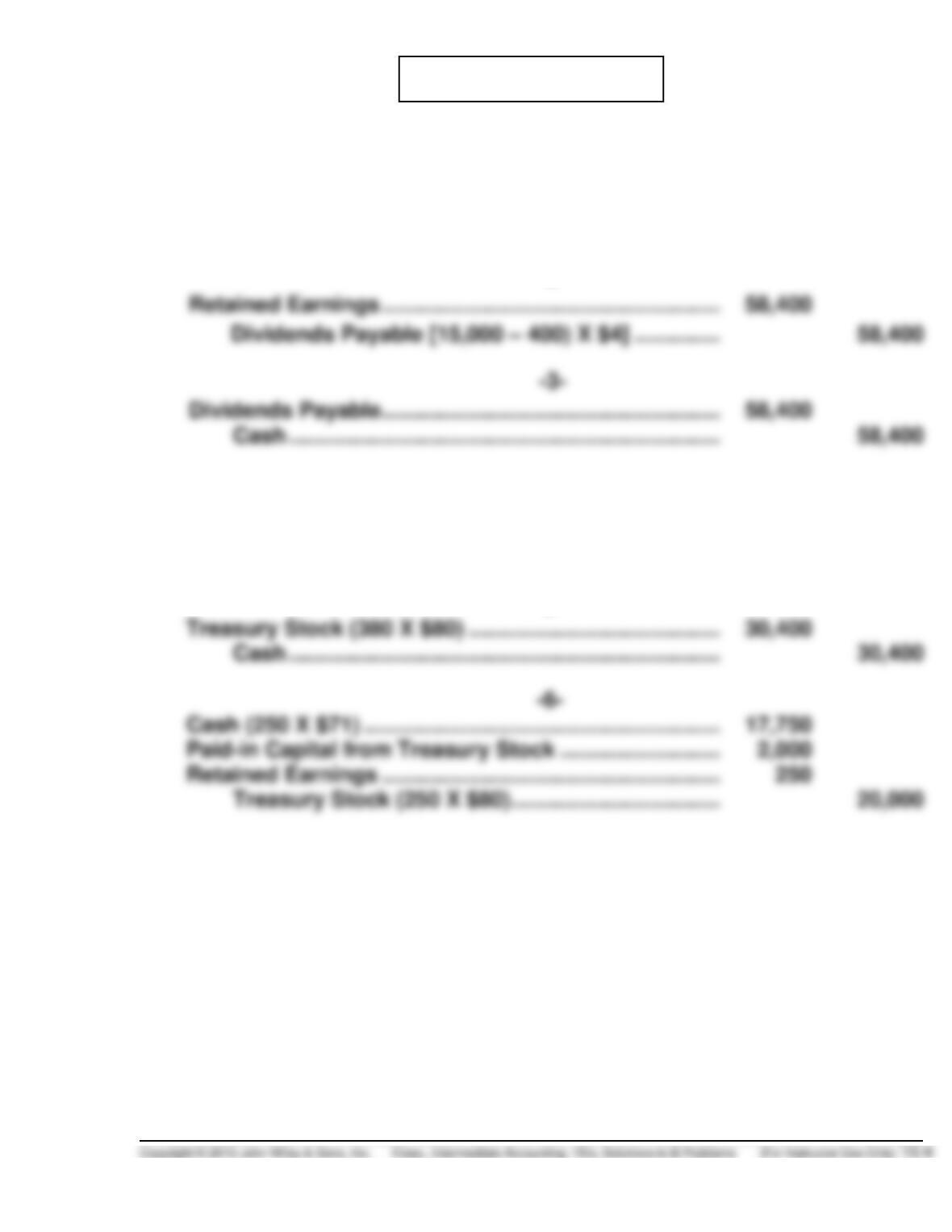

(a) Treasury Stock (600 X $13) …………………………... 7,800

Cash ……………………………………………………. 7,800

(d) Cash (400 X $11) ………………………………………….. 4,400

Paid-in Capital from Treasury Stock ……………… 430

Retained Earnings ……………………………………….. 830

Treasury Stock …………………………………….. 5,660*

PROBLEM 15-6B

(a) -1-

Treasury Stock (400 X $73) ………………………………….. 29,200

Cash ……………………………………………………………. 29,200

-2-

-4-

Cash (400 X $78) …………………………………………………. 21,200

Treasury Stock …………………………………………….. 29,200

Paid-in Capital from Treasury Stock (400 X $5) …. 2,000

-5-

PROBLEM 15-6B (Continued)

(b) RED APPLE COMPANY

Stockholders’ Equity

December 31, 2015

Common stock, $60 par value, authorized

25,000 shares; issued 15,000 shares,

14,870 shares outstanding ……………………….. $900,000

PROBLEM 15-7B

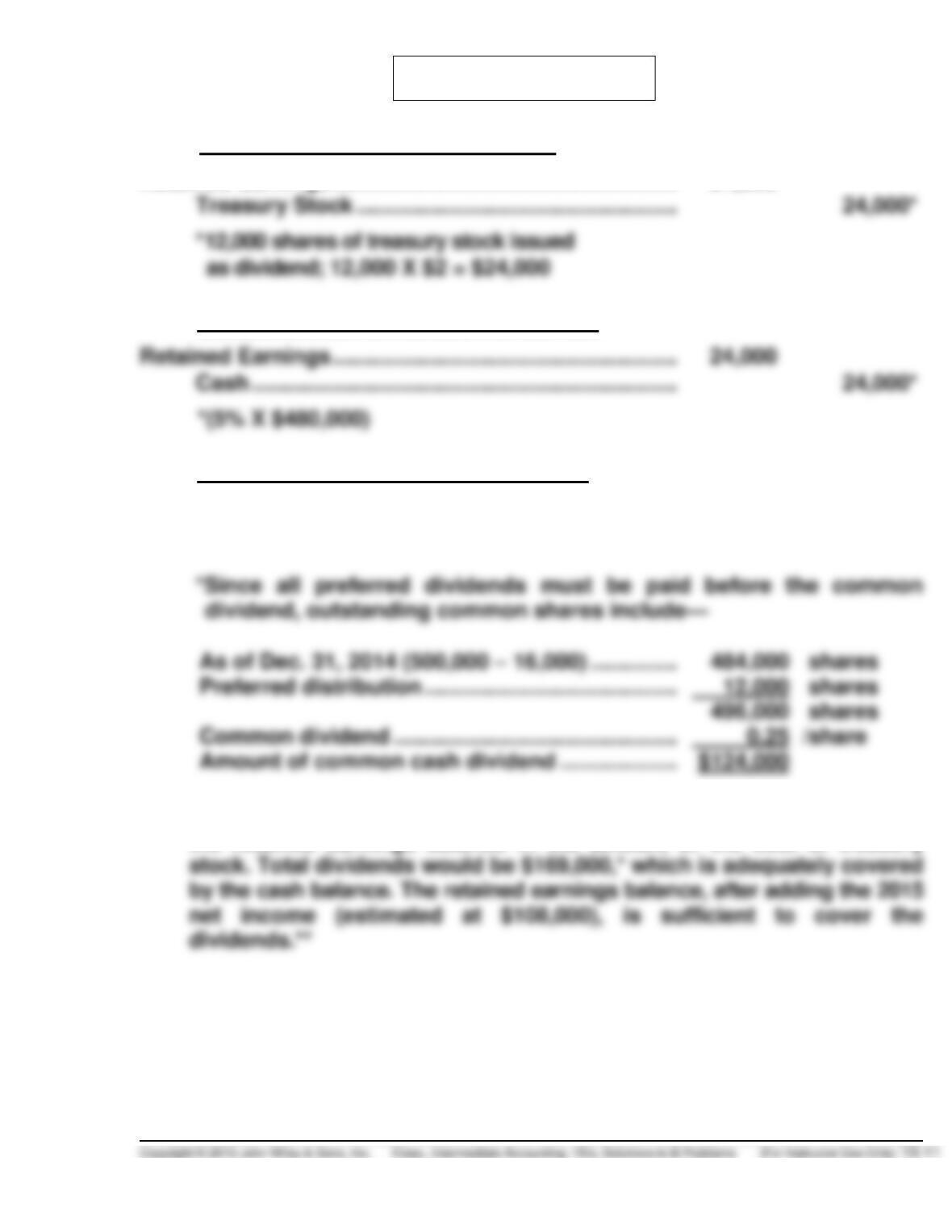

(a)

For preferred dividends in arrears:

Retained Earnings …………………………………………………..

24,000

Treasury Stock ……………………………………………….

For 6% preferred current year dividend:

Retained Earnings ………………………………………………..

24,000

For $0.25 per share common dividend:

Retained Earnings ………………………………………………..

124,000

Cash …………………………..……………………………….

124,000*

(b) The suggested cash dividend could be paid even if state law did restrict

the retained earnings balance in the amount of the cost of treasury

PROBLEM 15-7B (Continued)

*Preferred dividends in arrears (5% X $480,000) …..

$ 24,000

Current preferred dividend (5% X $480,000) ……….

24,000

Total balance available ……………………………………..

PROBLEM 15-8B

Transactions:

(a) Assuming Wellington Co. declares and pays a $0.25 per share cash

dividend.

(1) Total assets—decrease $10,250 (41,000 X $0.25]

(b) Wellington declares and issues a 15% stock dividend when the market

price of the stock is $8.

(1) Total assets—no effect

(c) Wellington declares and issues a 40% stock dividend when the market

price of the stock is $7 per share.

(1) Total assets—no effect

(d) Wellington declares and distributes a property dividend.

(1) Total assets—decrease $31,775 (10,250 X $3.10)—$4,100 gain

less $35,875 dividend