Archives

978-1259722660 Appendix Appendix Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Appendix Appendix Part 2

Exercise A–4 Requirement 1 June 30 Fair value of interest rate swap $11,394 Fair value of note payable $220,000 Fixed rate 10% Floating rate 6% Fixed receipts $5,000 ([10% x ¼] x $200,000) Floating payments (3 ,000) ([6% x ¼] […]

978-1259722660 Appendix Appendix Part 3

Problem A–1 (continued) Requirement 5 Swap Note Jan. 1, 2018 100,000 Dec. 31, 2018 1,759 1,759 Balance 1,759 98,241 Dec. 31, 2019 2,694 2,694 Balance 935 100,935 Dec. 31, 2020 935 935 100 ,000 Balance 0 0 Problem A–1 (continued) […]

978-1259722660 Appendix Appendix Part 4

Problem A-3 (continued) Requirement 6 Income Statement ( ) 2018 (8,000) Interest expense 2019 (8,842) Interest expense (158) Interest expense 3,852 Holding gain—interest rate swap (1 ,852) Holding loss—hedged note (7 ,000) Net effect—same as floating interest payment […]

978-1259722660 Chapter 1 Lecture Note Part 1

CHAPTER 1 ENVIRONMENT AND THEORETICAL STRUCTURE OF FINANCIAL ACCOUNTING Overview The primary function of financial accounting is to provide useful financial information to users external to the business enterprise. The focus of financial accounting is on the information needs of […]

978-1259722660 Chapter 1 Lecture Note Part 2

3. Group/Research Activity The debate over principles-based versus rules-based accounting standards provides an excellent opportunity for class discussion, in-class debate, or for a writing assignment. One suggestion is to form groups of 4 or 5 students to research the issue. […]

978-1259722660 Chapter 1 Solution Manual Part 1

Question 1–1 Financial accounting is concerned with providing relevant financial information about various kinds of organizations to different types of external users. The primary Question 1–2 Resources are efficiently allocated if they are given to enterprises that will use them […]

978-1259722660 Chapter 1 Solution Manual Part 2

Exercise 1–2 Requirement 1 Year 2 Year 3 Revenues $350,000 $450,000 Expenses: Rent ($80,000 2) (40,000) (40,000) Requirement 2 Amount owed at the end of year one $ 5,000 Advertising costs incurred in year two 25 ,000 30,000 Amount […]

978-1259722660 Chapter 1 Solution Manual Part 3

Communication Case 1–7 Suggested Grading Concepts and Grading Scheme: Content (70%) _______ 30 Briefly outlines the standard setting process. ______ Role of FASB, SEC. ______ The process. Writing (30%) _______ 6 Terminology and tone appropriate to the audience of a […]

978-1259722660 Chapter 10 Lecture Note Part 1

CHAPTER 10 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: ACQUISITION Overview This chapter and the one that follows address the measurement and reporting issues involving property, plant, and equipment and intangible assets, the tangible and intangible long-lived assets that are […]

978-1259722660 Chapter 10 Lecture Note Part 2

Suggestions for Class Activities 1. Guest Speaker The assigning of fair value to assets acquired in an acquisition is an interesting topic for students. The accounting issues are interesting, as are the valuation issues. Through your contacts at local CPA […]

978-1259722660 Chapter 10 Solution Manual Part 1

Question 10–1 The difference between tangible and intangible long-lived, revenue-producing Question 10–2 The cost of property, plant, and equipment and intangible assets includes the purchase price (less any discounts received from the seller); transportation costs paid by the buyer to […]

978-1259722660 Chapter 10 Solution Manual Part 2

Brief Exercise 10–4 Cost of silver mine: Acquisition, exploration, and development $5,600,000 *Present value of $1, n = 5, i = 6% (from Table 2) Brief Exercise 10–5 After one year, the liability will increase to $455,456. ($429,675† + ($429,675 […]

978-1259722660 Chapter 10 Solution Manual Part 3

Exercise 10–5 Patent ($200,000 + 10,000)…………………………………………. 210,000 ……………………………………………………………………..Cash ……………………………………………………………………….935,000 *The ongoing expense each month of operating as a franchise would be expensed as incurred. Exercise 10–6 Calculation of goodwill: Consideration exchanged $17,000,000 Less fair value of net assets: Assets $23,000,000 […]

978-1259722660 Chapter 10 Solution Manual Part 4

Exercise 10–18 Requirement 1 Fair value of old land + Cash given = Fair value of new land Requirement 2 Land—new ($72,000 + 14,000)…………………………………… 86,000 ……………………………………………………………………..Cash …………………………………………………………………………14,000 ……………………………………………..Land—old (book value) …………………………………………………………………………30,000 ……………………………………………………………….Gain ($72,000 – 30,000) …………………………………………………………………………42,000 Requirement 3 Land—new ($30,000 […]

978-1259722660 Chapter 10 Solution Manual Part 5

Exercise 10–22 Average accumulated expenditures: Interest capitalized: $3,000,000 – 1 ,500,000 (construction loan) x 10% = $150,000 $1,500,000 x 7%* = 105 ,000 $255 ,000 = interest capitalized * Weighted-average rate of all other debt: $2,000,000 x 9% = $180,000 […]

978-1259722660 Chapter 10 Solution Manual Part 6

Exercise 10–32 Requirement 1 2018: ………………………………………………………………………..Cash ……………………………………………………………………………..2,200,000 2019: Research and development expense……………………………. 800,000 Software development costs ……………………………………… 400,000 ………………………………………………………………………..Cash ……………………………………………………………………………..1,200,000 Requirement 2 (1) Percentage-of-revenue method: $1,000,000 = 20% × $400,000 = $80,000 $5,000,000 (2) Straight-line method: 1/4 or 25% × […]

978-1259722660 Chapter 10 Solution Manual Part 7

Problem 10–8 Case A. Requirement 1 Book value less fair value = loss on exchange Fair value of old tractor + cash given = Initial value of new tractor $9,000 + 20,000 = $29,000 Journal entry (not required): New tractor […]

978-1259722660 Chapter 10 Solution Manual Part 8

Judgment Case 10–1 Requirement 1 All costs necessary to bring the land to its condition for use should be capitalized as the cost of the land. This should include the following costs: Purchase price. Title insurance. Requirement 2 Assets acquired […]

978-1259722660 Chapter 10 Solution Manual Part 9

Judgment Case 10–9 Requirement 1 The costs of research equipment used exclusively for Trouver would be reported as research and development expenses in the period incurred. The costs of research equipment used on both Trouver and future research Requirement 2 […]

978-1259722660 Chapter 11 Lecture Note Part 1

CHAPTER 11 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: UTILIZATION AND DISPOSITION Overview This chapter completes our discussion of accounting for property, plant, and equipment and intangible assets. We address the allocation of the cost of these assets to the […]

978-1259722660 Chapter 11 Solution Manual Part 1

Question 11–1 The terms depreciation, depletion, and amortization all refer to the process of allocating the cost of property, plant, and equipment and finite-life intangible assets Question 11–2 The term depreciation often is confused with a decline in value or […]

978-1259722660 Chapter 11 Solution Manual Part 10

Problem 11–13 (concluded) 2019 Depreciation of equipment: Original cost $140,000 Less: 2018 depreciation (19 ,500) 2019 Depreciation of structures: Original cost $68,000 Less: 2018 depreciation (10 ,200) Remaining depreciable cost $57,800 Revised estimate of tons remaining (1,000,000 – 120,000) […]

978-1259722660 Chapter 11 Solution Manual Part 11

Ethics Case 11–10 Requirement 1 2018 expense using CEO’s approach: $42,000,000 Cost Depreciation to date (2016–2017) 33,600,000 Book value ÷ 3 Estimated remaining life (2018–2020) $11,200,000 New annual depreciation 2018 income would include only depreciation expense of $11,200,000. 2018 expense […]

978-1259722660 Chapter 11 Solution Manual Part 2

Brief Exercise 11–3 a. Straight-line: b. Sum-of-the-years’ digits: Sum-of-the-digits is ([4 (4 + 1)] ÷ 2) = 10 2018 $28,000 × 4/10 × 9/12 = $8,400 2019 $28,000 × 4/10 × 3/12 = $2,800 + $28,000 × 3/10 × 9/12 […]

978-1259722660 Chapter 11 Solution Manual Part 3

Exercise 11–2 1. Straight-line: 2. Sum-of-the-years’ digits: Sum-of-the-digits is ([10 (10 + 1)] ÷ 2) = 55 2018 $110,000 × 10/55 = $20,000 2019 $110,000 × 9/55 = $18,000 3. Double-declining balance: Straight-line rate is 10% (1 ÷ 10 years) […]

978-1259722660 Chapter 11 Solution Manual Part 4

Exercise 11–11 Requirement 1 To update depreciation in 2018; 2 months of service to date of disposal. Depreciation expense …………………………………………….. 2,000 ……………………………………….Accumulated depreciation …………………………………………………………………………..2,000 Requirement 2 To record the sale of the truck. Cash …………………………………………………………………….. 58,000 Loss on sale of […]

978-1259722660 Chapter 11 Solution Manual Part 5

Exercise 11–20 Adjustment of amortization expense to reflect change in useful life. ($ in millions) ……………………………………………………………………Patent ………………………………………………………………………..2.5 Calculation of annual amortization after the estimate change: $ in millions) $9 Cost $1 Previous annual amortization ($9 ÷ 9 years) × 4 […]

978-1259722660 Chapter 11 Solution Manual Part 6

Exercise 11–30 Requirement 1 Determination of implied fair value of goodwill: Fair value of Centerpoint, Inc. $220 million Measurement of impairment loss: Book value of goodwill $50 million Implied fair value of goodwill 20 million Impairment loss $30 million Requirement […]

978-1259722660 Chapter 11 Solution Manual Part 7

Problem 11–1 Requirement 1 Determine useful life: Determine age of assets: $40,000 accumulated depreciation = 4 years old $10,000 annual depreciation Double-declining balance in 4th year of life: Year 1 (2015) $200,000 × 10% = $20,000 Year 2 (2016) 180,000 […]

978-1259722660 Chapter 11 Solution Manual Part 8

Problem 11–7 Requirement 1 Cost of mineral mine: Depletion: $2,200,000 – 100,000 Depletion per ton = = $5.25 per ton 400,000 tons 2018 depletion = $5.25 × 50,000 tons = $262,500 2019 depletion: Revised depletion rate = ($2,200,000 – 262,500) […]

978-1259722660 Chapter 11 Solution Manual Part 9

Problem 11–10 (concluded) b. This is a change in accounting principle that is accounted for as a change in estimate. SYD 2014 depreciation $ 60,000 ($330,000 × 10/55) 2015 depreciation 54,000 ($330,000 × 9/55) 2016 depreciation 48,000 ($330,000 × 8/55) […]

978-1259722660 Chapter 12 Lecture Note Part 1

CHAPTER 12 INVESTMENTS Overview In this chapter we cover various approaches used to account for investments that companies make in the debt and equity securities of other companies. An investing company has the option to account for these investments at […]

978-1259722660 Chapter 12 Solution Manual Part 1

Question 12–1 Question 12–2 Increases and decreases in the market value between the time a debt security is acquired and the day it matures to a prearranged maturity value are ignored for a security classified as “held-to-maturity.” These changes aren’t […]

978-1259722660 Chapter 12 Solution Manual Part 10

Problem 12–5 (continued) 2) Recording the sale transaction: Cash (proceeds)…………………………………………………….. 425,000 November 1 Investment in M&D Corporation bonds ………………… 1,400,000 Cash……………………………………………………………….. 1,400,000 Investment in Distribution Transformers bonds (cost) 400,000 Fair-value adjustment (account balance)…………………. 25,000 Problem 12–5 (continued) December 31 Adjusting […]

978-1259722660 Chapter 12 Solution Manual Part 11

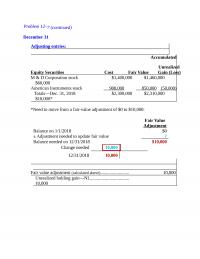

Problem 12–7 (continued) December 31 Adjusting entries: Accumulated Unrealized Equity Securities Cost Fair Value Gain (Loss) $10,000* *Need to move from a fair-value adjustment of $0 to $10,000: Fair-Value Adjustment 1/1/2018 0 Change needed 10,000 12/31/2018 10,000 Fair value adjustment […]

978-1259722660 Chapter 12 Solution Manual Part 12

Problem 12–9 2018 ($ in millions) October 18 October 31 Cash…………………………………………………………………………………. 1.5 Interest revenue………………………………………………………………. 1.5 November 1 Investment in Holistic Entertainment bonds (HTM)……………….. 18 Cash……………………………………………………………………………… 18 November 1 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment […]

978-1259722660 Chapter 12 Solution Manual Part 13

Problem 12–11 Note: the answer to P12-11 is the same as the answer to Requirement 2 of P12-10. Purchase ($ in millions) Net income No entry Dividends Cash (10 million shares x $2)……………………………………………………. 20 Dividend revenue……………………………………………………………. 20 Adjusting entry Need […]

978-1259722660 Chapter 12 Solution Manual Part 14

Problem 12–16 (continued) Need to move from a fair-value adjustment from $0 to ($9,420): Fair-Value Adjustment 1/1/2018 0 December 31, 2018 Cash ($150,000 x 6%) ÷ 2……………………………….. 4,500 Discount on bond investment (difference)…………. 390 Interest revenue [{$150,000 – ($10,658 – […]

978-1259722660 Chapter 12 Solution Manual Part 15

International Case 12–4 Requirement 1 P. 140 of the 10K includes the following note: “Interests in other companies Interests in other companies are measured at fair value. Investments in equity investments that do not have a quoted market price in […]

978-1259722660 Chapter 12 Solution Manual Part 2

Brief Exercise 12–2 Because S&L Financial is purchasing the bonds for purposes of earning profits on short-term differences in price, those bonds would be classified as trading securities. For trading securities, gains and losses from changes in fair values are […]

978-1259722660 Chapter 12 Solution Manual Part 3

Brief Exercise 12–19 LED does not intend to sell the investment, and it does not believe it is more likely than not that it will have to sell the investment before fair value recovers, so Fair value adjustment…………………………………… 100,000 Reclassification […]

978-1259722660 Chapter 12 Solution Manual Part 4

Exercise 12–7 (continued) 2019 January 5 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment of $50,000 to $45,000: Fair-Value Adjustment Change needed 5,000 1/5/2019 45,000 Unrealized holding loss—NI ($395,000 – $400,000)…………… 5,000 Fair value adjustment………………………………………………. 5,000 […]

978-1259722660 Chapter 12 Solution Manual Part 5

Exercise 12–12 (continued) a. June 30, 2019: Recognition of interest revenue b. July 1, 2019: Any entries necessary upon sale of the Jackson bonds 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment of $200,000 to ($100,000): […]

978-1259722660 Chapter 12 Solution Manual Part 6

Exercise 12–17 (continued) Requirement 2 Need to move from a fair-value adjustment from ($145,000) to ($70,000): Fair-Value Adjustment 1/1/2018 145,000 Fair Value Adjustment Balance on 1/1/2018 ($145,000) ± Adjustment needed to update fair value ? Balance needed on 12/31/2018 ($1,275,000 […]

978-1259722660 Chapter 12 Solution Manual Part 7

Exercise 12–24 Requirement 1 Purchase ($ in millions) Net income Investment in VB shares (25% x $32 million) ………………………. 8 Investment revenue…………………………………………………. 8 Dividends Cash (25% x $24 million)………………………………………………… 6 Investment in VB shares………………………………………….. 6 Amortization of differential Investment revenue […]

978-1259722660 Chapter 12 Solution Manual Part 8

Exercise 12–29 Requirement 1 Requirement 2 Cash (death benefit)………………………………………………… 250,000 Cash surrender value of life insurance (account balance) 16,000 Gain on life insurance settlement (to balance)………… 234,000 Insurance expense (difference)………………………………… 22,900 Cash surrender value of life insurance ($4,600 – 2,500).. […]

978-1259722660 Chapter 12 Solution Manual Part 9

Problem 12–2 Requirement 1 ($ in millions) Requirement 2 Cash (4% x $80 million)…………………………………… 3.20 Discount on bond investment (difference)…………. .10 Interest revenue (5% x $66)……………………………… 3.30 Requirement 3 Cash (4% x $80 million)…………………………………… 3.20 Discount on bond investment (difference)…………. […]

978-1259722660 Chapter 13 Lecture Note Part 1

CHAPTER 13 CURRENT LIABILITIES AND CONTINGENCIES Overview Chapter 13 is the first of five chapters devoted to liabilities. In Part A of this chapter, we discuss liabilities that are classified appropriately as current. In Part B, we turn our attention […]

978-1259722660 Chapter 13 Lecture Note Part 2

5. Ethical Dilemma Consider the following ethical dilemma: ETHICAL DILEMMA You are chief financial officer of Camp Industries. Camp is the defendant in a $44 million class-action suit. The company’s legal counsel informally advises you that chances are remote that […]

978-1259722660 Chapter 13 Solution Manual Part 1

A liability involves the past, the present, and the future. It is a present responsibility, to sacrifice assets in the future, caused by a transaction or other event 1. are probable, future sacrifices of economic benefits 2. that arise from […]

978-1259722660 Chapter 13 Solution Manual Part 10

TARGET CASE Requirement 1 a. The four components of current liabilities are: ($ in millions) 1/30/2016 1/31/2015 Current Liabilities: Accounts payable $ 7,418 $ 7,759 b. Current assets are sufficient to cover current liabilities in both the fiscal years ended […]

978-1259722660 Chapter 13 Solution Manual Part 2

Brief Exercise 13–6 December 12 January 16 Cash…………………………………………………………….. 216,000 Deferred sales revenue……………………………………. 24,000 Sales revenue…………………………………………….. 240,000 Brief Exercise 13–7 In 2018 Lizzie would recognize $11,500 of revenue ($4,000 + 3,000 + 2,500 + 2,000). In 2019 Lizzie would recognize the […]

978-1259722660 Chapter 13 Solution Manual Part 3

Exercise 13–7 Requirement 1 Deposits Collected Containers Returned Liability—refundable deposits …………………… 790,000 Cash…………………………………………………….. 790,000 Deposits Forfeited Liability—refundable deposits …………………… 35,000 Revenue—sale of containers…………………… 35,000 Cost of goods sold…………………………………….. 35,000 Inventory of containers ………………………….. 35,000 Requirement 2 Balance on January 1 […]

978-1259722660 Chapter 13 Solution Manual Part 4

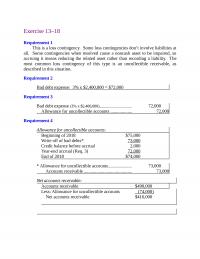

Exercise 13–18 Requirement 1 This is a loss contingency. Some loss contingencies don’t involve liabilities at all. Some contingencies when resolved cause a noncash asset to be impaired, so Requirement 2 Bad debt expense: 3% x $2,400,000 = $72,000 Requirement […]

978-1259722660 Chapter 13 Solution Manual Part 5

Problem 13–1 Requirement 1 Blanton Plastics L & T Bank Notes receivable………………………………………………. 14,000,000 Cash …………………………………………………………… 14,000,000 Requirement 2 Adjusting entries (December 31, 2018) Blanton Plastics Interest expense ($14,000,000 x 12% x 3/12)…………….. 420,000 Interest payable…………………………………………….. 420,000 L & T Bank […]

978-1259722660 Chapter 13 Solution Manual Part 6

Problem 13–7 Requirement 1 Item (a): Because the loss is probable and can be reasonably estimated, HW would be required to accrue a liability under both U.S. GAAP and Item (b): Under IFRS, present values would be used, so the […]

978-1259722660 Chapter 13 Solution Manual Part 7

Problem 13–13 Salaries and wages expense (total amount earned)……….. 2,000,000 Withholding taxes payable (federal income tax)………. 400,000 Withholding taxes payable (local income tax)…………. 53,000 Payroll tax expense (total)……………………………………. 273,000 Social security taxes payable (employer’s matching amount) 124,000 Medicare taxes payable […]

978-1259722660 Chapter 13 Solution Manual Part 8

Communication Case 13–7 Assumptions students make will determine the correct answer to some classifications. Depending on the assumptions made, different views can be convincingly defended. The process of developing and synthesizing the arguments will likely be more beneficial than any […]

978-1259722660 Chapter 13 Solution Manual Part 9

IFRS Case 13–15 Under IFRS, the $70 million environmental contingency would be accrued and included in Fizer’s liabilities. The associated loss would be reported in the income statement. Accounting for contingencies is covered under IAS No. 37, “Provisions, Contingent Liabilities, […]

978-1259722660 Chapter 14 Lecture Note Part 1

CHAPTER 14 BONDS AND LONG-TERM NOTES Overview This chapter continues the presentation of liabilities. While the discussion focuses on the accounting treatment of long-term liabilities, the borrowers’ side of the same transactions is presented as well. Long-term notes and bonds […]

978-1259722660 Chapter 14 Lecture Note Part 2

Suggestions for Class Activities 1. Real World Scenario An article in Barron’s, titled “Wall Street’s Latest Illusion,” reported that “Goldman Sachs, Morgan Stanley and other firms are booking profits from the falling value of their own debt.” The article asserts […]

978-1259722660 Chapter 14 Solution Manual Part 1

QUESTIONS FOR REVIEW OF KEY TOPICS Question 14–1 Periodic interest is calculated as the effective interest rate times the amount of the debt outstanding during the period. This same principle applies to the flip side of the Question 14–2 Long-term […]

978-1259722660 Chapter 14 Solution Manual Part 10

Problem 14–11 Requirement 1 *Present value of an ordinary annuity of $1: n = 5, i = 10% (Table 4) ** Present value of $1: n = 5, i = 10% (Table 2) Equipment (fair value)……………………………………………. 115,883 Discount on notes […]

978-1259722660 Chapter 14 Solution Manual Part 11

Problem 14–19 Requirement 1 Convertible Bonds—2005 issue Cash (97.5% x $200 million)……………………………………………….. 195 Bonds with Warrants—2009 issue Cash (102% x $50 million)………………………………………………….. 51 Discount on bonds payable (difference)………………………………. 3 Bonds payable (face amount)………………………………………….. 50 Equity—stock warrants (given)……………………………………… 4 Requirement 2 […]

978-1259722660 Chapter 14 Solution Manual Part 12

Problem 14–23 (continued) Requirement 4 If the fair value on December 31 is $342,000, Appling needs to compare that amount with the amortized initial measurement on that date. That amount was increased when Appling recorded interest on December 31: Interest […]

978-1259722660 Chapter 14 Solution Manual Part 13

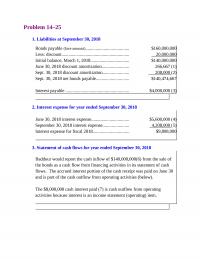

Problem 14–25 1. Liabilities at September 30, 2018 Bonds payable (face amount)……………………………….. $160,000,000 Less: discount………………………………………………….. 20 ,000,000 2. Interest expense for year ended September 30, 2018 June 30, 2018 interest expense…………………………… $5,600,000 (4) September 30, 2018 interest expense………………….. 4 ,208,000 […]

978-1259722660 Chapter 14 Solution Manual Part 14

Case 14–3 (continued) Arguments Supporting View 1: 1. Those who favor accounting for convertible debt as entirely a liability until it is either converted or repaid argue that a convertible bond offers the holder two mutually exclusive choices. The holder […]

978-1259722660 Chapter 14 Solution Manual Part 15

Case 14–9 (continued) AGF has experienced favorable leverage, as demonstrated by calculating and comparing the return on assets and the return on shareholders’ equity for 2016: The debt to equity ratio is not used to shareholders’ advantage. The return on […]

978-1259722660 Chapter 14 Solution Manual Part 2

Brief Exercise 14–1 face annual fraction of the cash amount rate annual period interest Brief Exercise 14–2 Interest $ 2,000,000 ¥ x 23.11477* =$46,229,540 Principal $80,000,000 x 0.30656** = 24,524,800 Present value (price) of the bonds $70,754,340 ¥ [5 ÷ […]

978-1259722660 Chapter 14 Solution Manual Part 3

Exercise 14–3 1. Price of the bonds at January 1, 2018 2. January 1, 2018 Cash (price determined above)……………………………….. 70,823,680 Discount on bonds payable (difference)………………… 9,176,320 Bonds payable (face amount)……………………………. 80,000,000 3. June 30, 2018 Interest expense (6% x $70,823,680)………………………….. […]

978-1259722660 Chapter 14 Solution Manual Part 4

Exercise 14–11 1. February 1, 2018 2. July 31, 2018 Interest expense (5% x $731,364)…………………… 36,568 Discount on bonds payable (difference)…… 568 Cash (4.5% x $800,000)………………………….. 36,000 3. December 31, 2018 Interest expense (5/6 x 5% x [$731,364 + 568]). […]

978-1259722660 Chapter 14 Solution Manual Part 5

Exercise 14–19 1. January 1, 2018 Cash ……………………………………………………………………….. 8,000,000 2. Amortization schedule $8,000,000 ÷ 2.67301 = $2,992,881 amount (from Table 4) of loan n = 3, i = 6% Cash Effective Decrease in Outstanding Dec.31 Payment Interest Balance Balance 6% […]

978-1259722660 Chapter 14 Solution Manual Part 6

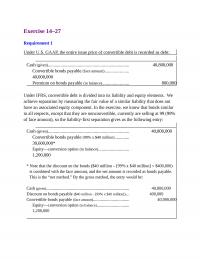

Exercise 14–27 Requirement 1 Under U.S. GAAP, the entire issue price of convertible debt is recorded as debt: Under IFRS, convertible debt is divided into its liability and equity elements. We achieve separation by measuring the fair value of a […]

978-1259722660 Chapter 14 Solution Manual Part 7

Exercise 14–30 (concluded Rapid will report the loss from the change in the fair value of the bonds in net income if the entire change is due to the change in general interest rates. But any change in the fair […]

978-1259722660 Chapter 14 Solution Manual Part 8

Problem 14–3 (continued) Requirement 3 (effective interest) (straight-line) Interest expense ($4,500 + 404)…………………………………. 4,904 Discount on bonds payable ($3,232 ÷ 8)…………….. 404 Cash (4.5% x $100,000)…………………………………….. 4,500 Requirement 4 By the straight-line method, a company determines interest indirectly by allocating […]

978-1259722660 Chapter 14 Solution Manual Part 9

Problem 14–6 (concluded) February 28, 2021 (Western) Interest expense ($1,800,000 + 40,000 – 1,200,000). 640,000 Interest payable (from adjusting entry)……………….. 1,200,000 February 28, 2021 (Stillworth) Cash ($30,000 x 12% x 6/12)……………………………… 1,800 Discount on bond investment ($20 x 2 months)…… […]

978-1259722660 Chapter 15 Lecture Note Part 1

CHAPTER 15 LEASES Overview In the previous chapter, we saw how companies account for their long-term debt. The focus of that discussion was bonds and notes. In this chapter, we continue our discussion of debt, but we now turn our […]

978-1259722660 Chapter 15 Lecture Note Part 2

PowerPoint Slides Two PowerPoint presentations of the chapter are available in the Connect Library: 1. With “Concept Checks” useful for classroom presentation, permitting the instructor to intersperse in the presentation short exercises students can be asked to solve individually or […]

978-1259722660 Chapter 15 Solution Manual Part 1

QUESTIONS FOR REVIEW OF KEY TOPICS Question 15-1 Regardless of the legal form of the agreement, a lease is accounted for as either a rental agreement or a purchase/sale accompanied by debt financing depending on the Question 15-2 Periodic interest […]

978-1259722660 Chapter 15 Solution Manual Part 10

Problem 15-4 Requirement 1 Finance lease to lessee; Sales-type lease to lessor. Since the present value of lease payments (same for both the lessor and the Calculation of the Present Value of Lease Payments Present value of periodic lease payments […]

978-1259722660 Chapter 15 Solution Manual Part 11

Problem 15-9 Situation 1 2 3 4 A. The lessor’s: 1. Lease payments1$40,000 $40,000 $40,000 $33,000 B. The lessee’s: 4. Lease payments440,000 40,000 40,000 33,000 5. Right-of-use asset534,437 34,437 34,437 29,319 6. Lease payable634,437 34,437 34,437 29,319 1 ($10,000 x […]

978-1259722660 Chapter 15 Solution Manual Part 12

Problem 15–13 Requirement 1 January 1, 2018 Present Value of Lease Payments for Lessee Present value of periodic lease payments Plus: Present value of the excess lessee-guaranteed residual value ($40,000 x .82270*) 32 ,908 Present value of lease payments $742 […]

978-1259722660 Chapter 15 Solution Manual Part 13

Problem 15-17 (connued) Requirement 2 Branson Construction (Lessee) Interest expense (10% x [$936,492* – 100,000])………………… 83,649 ** present value of an annuity due of $1: n=20, i=10% Amortization expense ($936,492 ÷ 20 years)…………………….. 46,825 …………………………………………………..Right-of-use asset …………………………………………………………………………46,825 *** This debit […]

978-1259722660 Chapter 15 Solution Manual Part 14

Problem 15-18 (connued) Requirement 10 December 31, 2021 Yard Art Landscaping (Lessee) Maintenance expense (2021 fee)……………………………………… 1,000 ………………….Prepaid maintenance expense (paid in 2020) …………………………………………………………………………..1,000 Branch Motors (Lessor) Cash (lease payment)…………………………………………………. 11,000 …..Maintenance fee payable [or prepaid maintenance*] …………………………………………………………………………..1,000 ……………Lease receivable […]

978-1259722660 Chapter 15 Solution Manual Part 15

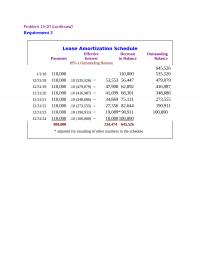

Problem 15-20 (connued) Requirement 3 Lease Amortization Schedule Effective Decrease Outstanding Payments Interest in Balance Balance 10% x Outstanding Balance 645,526 1/1/18 110,000 110,000 535,526 12/31/18 110,000 .10 (535,526) = 53,553 56,447 479,079 12/31/19 110,000 .10 (479,079) = 47,908 62,092 […]

978-1259722660 Chapter 15 Solution Manual Part 16

Problem 15-22 Requirement 1 Lessor’s Calculation of Lease payments Amount to be recovered (fair value) $365,760 Less: Present value of the residual value ($25,000 x .68301*) (17 ,075) * present value of $1: n=4, i=10% ** present value of an […]

978-1259722660 Chapter 15 Solution Manual Part 17

Problem 15-23 (connued) (a) by Western Soya Co. (the lessee) Since at least one (two in this case) classification criterion is met, this is a finance lease to the lessee. Western Soya records the present value of lease payments as […]

978-1259722660 Chapter 15 Solution Manual Part 18

Problem 15–26 Requirement 1 $5,000 .86384*** = $4,319 * Present value of $1: n = 1, i = 5%. ** Present value of $1: n = 2, i = 5%. *** Present value of $1: n = 3, i […]

978-1259722660 Chapter 15 Solution Manual Part 19

Problem 15-29 (concluded) Calculations: September 30, 2018* Lease receivable (present value calculated above)…………. 6,000,000 December 31, 2018** Cash (lease payment)……………………………………………….. 391,548 Lease receivable (difference)………………………………… 223,294 Interest revenue (3% x [$6,000,000 – 391,548])………… 168,254 Equipment (lessor’s cost)……………………………………… 6,000,000 Cash (lease payment)……………………………………………….. […]

978-1259722660 Chapter 15 Solution Manual Part 2

Brief Exercise 15-1 The present value of the lease payments is greater than “substantially all” of the Brief Exercise 15-2 The lease is a finance lease to Athens because the present value of the lease payments is greater than “substantially […]

978-1259722660 Chapter 15 Solution Manual Part 20

Communication Case 15-2 First, this case has no single right answer. The process of developing the proposed solutions will likely be more beneficial than the solutions themselves. Students should benefit from participating in the process, interacting first with other group […]

978-1259722660 Chapter 15 Solution Manual Part 3

Exercise 15-1 Situation 1 Since none of the criteria is met, this is an operating lease to the lessee: Lessee’s Application of Classification Criteria 1 Does the agreement specify that ownership of the asset transfers 2 Does the agreement contain […]

978-1259722660 Chapter 15 Solution Manual Part 4

Exercise 15-5 1. Calculation of the present value of lease payments (“selling price”) 2. Receivable at December 31, 2018 Receivable Initial balance, June 30, 2018…………. $3,000,000 June 30, 2018 reduction………………… (562,907)* Dec. 31, 2018 reduction………………… (441 ,052)** December 31, 2018 […]

978-1259722660 Chapter 15 Solution Manual Part 5

Exercise 15–11 Present Value of Lease Payments: contract present payments value * Present value of an annuity due of $1: n = 20, i = 2% [i = 2% (8% ÷ 4) because the contract calls for quarterly payments] Requirement […]

978-1259722660 Chapter 15 Solution Manual Part 6

Exercise 15-16 Present Value of Lease Payments: lease present payments value * present value of an annuity due of $1: n=8, i=2% [i = 2% (8% ÷ 4) because the lease calls for quarterly payments] January 1, 2018 Right-of-use asset […]

978-1259722660 Chapter 15 Solution Manual Part 7

Exercise 15-23 The lease term will be 6 years. The lease term is the contractual lease term modified by any renewal or termination options for which exercise of the options is “reasonably certain.” Requirement 1 January 1, 2018 […]

978-1259722660 Chapter 15 Solution Manual Part 8

Exercise 15-29 Requirement 1 Note: Because exercise of the option appears at the beginning of the lease to be reasonably certain, payment of the option price ($45,000) is expected to occur when the option becomes exercisable (at the end of […]

978-1259722660 Chapter 15 Solution Manual Part 9

Exercise 15-36 Requirement 1 The specific citation that specifies when a lessee remeasures the lease payments is FASB ASC 842–10–35–4: “Leases–Overall–Subsequent Measurement–Lease Payments.” Requirement 2 A lessee shall remeasure the lease payments if any of the following occur: a. The […]

978-1259722660 Chapter 16 Lecture Note Part 1

CHAPTER 16 ACCOUNTING FOR INCOME TAXES Overview In this chapter we explore financial accounting and reporting for the effects of income taxes. The discussion defines and illustrates temporary differences, which are the basis for recognizing deferred tax assets and deferred […]

978-1259722660 Chapter 16 Lecture Note Part 2

Suggestions for Class Activities 1. Target Analysis Have students, individually or in groups, go to Target’s most recent annual report at Target’s website. Ask them to: 1. Determine the temporary difference that for Target creates the largest deferred assets and […]

978-1259722660 Chapter 16 Solution Manual Part 1

_____________________________________________________________________________ Question 16–1 Income tax expense is comprised of both the current and the deferred tax consequences of events and transactions already recognized. Specifically, the $12.3 Question 16–2 Temporary differences between the reported amount of an asset or liability in […]

978-1259722660 Chapter 16 Solution Manual Part 10

Analysis Case 16–1 Requirement 1 Temporary differences originate in one or more years and reverse in one or more future years. Differing depreciation methods are a common example of a Requirement 2 Intraperiod tax allocation allocates the total income tax […]

978-1259722660 Chapter 16 Solution Manual Part 11

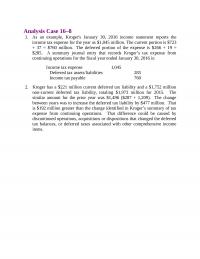

Analysis Case 16–8 1. As an example, Kroger’s January 30, 2016 income statement reports the income tax expense for the year as $1,045 million. The current portion is $723 Income tax expense 1,045 Deferred tax assets/liabilities 285 Income tax payable […]

978-1259722660 Chapter 16 Solution Manual Part 2

Brief Exercise 16–9 Current year Future taxable amount Pretax accounting income $ 900,000 Permanent difference: Taxable income (tax return) $ 760,000 Enacted tax rate 40% 40% Tax payable currently $ 304 ,000 Deferred tax liability $ 48,000 Journal entry Income […]

978-1259722660 Chapter 16 Solution Manual Part 3

Exercise 16–7 1. Liability—loss contingency 2. Liability—deferred subscription revenue 3. Prepaid rent 4. Accrued bond interest payable 5. Prepaid insurance 6. Unrealized loss on investments (shareholders’ equity account) 7. Warranty liability 8. Liability—deferred rent revenue 9. Accumulated depreciation; and thus […]

978-1259722660 Chapter 16 Solution Manual Part 4

Exercise 16–15 Requirement 1 ($ in millions) Current Future Year Deductible Amounts Total 2018 2019 2020 2021 2022 Pretax accounting income 14 Temporary difference: Deferred Tax Asset Deferred Tax Asset: 0 Ending balance (balance currently needed) $ 1.7 1.7 […]

978-1259722660 Chapter 16 Solution Manual Part 5

Exercise 16–22 Requirement 1 ($ in thousands) Current Future Prior Years Year Deductible 2016 2017 2018 Amounts [total] Net operating loss (160) Deferred Tax Asset Deferred Tax Asset: 0 Ending balance (balance currently needed) $ 8 8Less: beginning balance […]

978-1259722660 Chapter 16 Solution Manual Part 6

Exercise 16–30 Income Statement For the fiscal year ended March 31, 2018 ($ in millions) Revenues $ 830 Cost of goods sold (350 ) The FASB Accounting Standards Codification represents the single source of authoritative U.S. generally accepted accounting principles. […]

978-1259722660 Chapter 16 Solution Manual Part 7

Problem 16–4 2018 2019 2020 2021 Pretax accounting income $60,000 $80,000 $70,000 $70,000 Cumulative Temporary 2018 2019 2020 2021 Difference Straight-line 30,000 30,000 30,000 30,000 Tax depreciation (39 ,600) (52 ,800) (18 ,000) (9 ,600) Temporary differences: (9,600) (22,800) 12,000 […]

978-1259722660 Chapter 16 Solution Manual Part 8

Problem 16–8 (continued) Journal entry at the end of 2018 Income tax expense (to balance) 52 * Temporary difference for subscriptions: 2017 2018 2019 Earned in current yr. (reported on income statement) $25 $33 Collected in prior yr., recognized in […]

978-1259722660 Chapter 16 Solution Manual Part 9

Problem 16–11 Requirement 1 Deferred tax assets are recognized for all deductible temporary differences and operating loss carryforwards. Deferred tax assets are then reduced by a valuation allowance if it is “more likely than not” that some portion or all […]

978-1259722660 Chapter 17 Lecture Note Part 1

CHAPTER 17 PENSIONS AND OTHER POSTRETIREMENT BENEFITS Overview Employee compensation comes in many forms. Salaries and wages, of course, provide direct and current payment for services provided. However, it’s commonplace for compensation also to include benefits payable after retirement. We […]

978-1259722660 Chapter 17 Lecture Note Part 2

PowerPoint Slides Two PowerPoint presentations of the chapter are available in the Connect Library: 1. With “Concept Checks” useful for classroom presentation, permitting the instructor to intersperse in the presentation short exercises students can be asked to solve individually or […]

978-1259722660 Chapter 17 Lecture Note Part 3

Assignment Chart Learning Est. time Questions Objective(s) Topic (min.) 17–1 1 Motivation to offer a pension plan 5 17–2 1 Qualified pension plans 5 17–3 1 What type of pension plan? 5 17–4 2 What is the vested benefit obligation? […]

978-1259722660 Chapter 17 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 17 Solution Manual Part 10

Problem 17–15 ( )s indicate credits; debits otherwise ($ in 000s) PBO Plan Assets Prior Service Cost –AOCI Net Loss –AOCI Pension Expense Cash Net Pension (Liability) / Asset Balance, Jan. 1, 2018 (4100) 4530 840 477 430 Service cost2(332) […]

978-1259722660 Chapter 17 Solution Manual Part 11

Problem 17–17 (concluded) Requirement 2 GLOBAL COMMUNICATIONS Statement of Comprehensive Income Year ended December 31, 2018 Net income $300.0 Other comprehensive income: Net unrealized holding gain on investments ($30, net of $12 tax) $ 18.0 Loss on pensions—PBO estimate ($23, […]

978-1259722660 Chapter 17 Solution Manual Part 12

Case 17–1 (continued) Requirement 2 The value of your plan assets as of the anticipated retirement date is $1,872,981: A B C D E End of Years to Future Value Year: Retirement Salary Contribution at Retirement 2018 39 100,000 8,000 […]

978-1259722660 Chapter 17 Solution Manual Part 13

Real World Case 17–7 Requirement 1 FedEx sponsors both defined benefit and defined contribution pension plans as well as a postretirement healthcare plan. These are described in disclosure note 13 (in part) for the years ended May 31, 2015 and […]

978-1259722660 Chapter 17 Solution Manual Part 2

Brief Exercise 17–1 ($ in millions) Beginning of the year PBO $80 Service cost 10 Brief Exercise 17–2 ($ in millions) Beginning of the year PBO $80 Service cost ? Interest cost 4 (5% x $80) Loss (gain) on […]

978-1259722660 Chapter 17 Solution Manual Part 3

Exercise 17–4 Requirement 1 ($ in millions) Pension expense (total)…………………………………………… 14 Requirement 2 ($ in millions) Pension expense (total)…………………………………………… 10 Plan assets (expected return on assets)………………………….. 4 Amortization of net gain—OCI (current amortization)* ….. 2 PBO ($10 service cost + […]

978-1259722660 Chapter 17 Solution Manual Part 4

Exercise 17–15 PBO Plan Assets Prior Service Cost –AOCI Net Gain –AOCI Pension Expense Cash Net Pension (Liability ) / Asset Balance, Jan. 1, 2018 (800) 600 114 80 (200) Service cost (84) 84 (84) Interest cost, 5% (40) 40 […]

978-1259722660 Chapter 17 Solution Manual Part 5

978-1259722660 Chapter 17 Solution Manual Part 6

Exercise 17–21 Requirement 1 ($ in millions) Service cost $ 60 Interest cost 27 * Since the amendment was at the end of the year, there is no amortization of prior service cost in 2018. Requirement 2 ($ in millions) […]

978-1259722660 Chapter 17 Solution Manual Part 7

Exercise 17–29 Requirement 1 ($ in millions) Service cost $34 Requirement 2 ($ in millions) Postretirement benefit expense (calculated above)…………………… 47 Amortization of prior service cost—OCI (amortization)*……. 1 APBO ($34 service cost + $12 interest cost)…………………………… 46 The amortization amount […]

978-1259722660 Chapter 17 Solution Manual Part 8

Problem 17–6 1. Projected Benefit Obligation ($ in 000s) Balance, January 1, 2018 $ 0 Service cost 150 2. Plan Assets Balance, January 1, 2018 $ 0 Actual return on plan assets (10% x $0) 0 Contributions, 2018 160 Benefits […]

978-1259722660 Chapter 17 Solution Manual Part 9

Problem 17–10 (concluded) Requirement 3 ($ in millions) PBO balance, January 1 $480 Service cost 75 Plan assets balance, January 1 $300 Actual return on plan assets 20 Contributions 2018 60 Benefits paid (36 ) Plan assets balance, December 31 $344 Because […]

978-1259722660 Chapter 18 Lecture Note Part 1

CHAPTER 18 SHAREHOLDERS’ EQUITY Overview We turn our attention in this chapter from liabilities, which represent the creditors’ interests in the assets of a corporation, to the shareholders’ residual interest in those assets. The discussions distinguish between the two basic […]

978-1259722660 Chapter 18 Lecture Note Part 2

5. Professional Skills Development Activities The following are suggested assignments from the end-of-chapter material that will help your students develop their communication, research, analysis, and judgment skills. Communication Skills. Analysis Case 18–2, Exercise 18–23, and Problem 18–6 are suitable for […]

978-1259722660 Chapter 18 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 18 Solution Manual Part 10

Case 18–4 (concluded) Requirement 4 One component of Other comprehensive income for Cisco is “unrealized gains on investments.” For reporting purposes, some investments in securities are reported at their fair values. The holding gains and losses from writing “available-for-sale” 15. […]

978-1259722660 Chapter 18 Solution Manual Part 11

Research Case 18–9 The results students report will vary depending on the companies chosen. It Typical items that affect retained earnings are dividends (cash, property, or stock) and net income or loss. Treasury stock or retired stock transactions also affect […]

978-1259722660 Chapter 18 Solution Manual Part 2

Brief Exercise 18–5 Horton’s total paid-in capital will decline by $17 million, the price paid to buy back the shares. Journal entry (not required): ($ in millions) Common stock (2 million shares x $1 par)……………………………. 2 * Paid-in capital—excess of […]

978-1259722660 Chapter 18 Solution Manual Part 3

Exercise 18–2 Requirement 1 The specific citation that describes the guidelines for presenting accumulated other comprehensive income on the statement of shareholders’ equity is FASB ASC Requirement 2 45-14 The total of other comprehensive income for a period shall be […]

978-1259722660 Chapter 18 Solution Manual Part 4

Exercise 18–12 1. January 23, 2018 ($ in millions) 2. September 3, 2018 Cash (1 million shares x $21)……………………………………………… 21 Treasury stock (1 million shares x $20)…………………………….. 20 Paid-in capital—share repurchase (remainder)………………… 1 3. November 4, 2018 Cash (1 million […]

978-1259722660 Chapter 18 Solution Manual Part 5

Exercise 18–22 The FASB Accounting Standards Codification represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. Disclosure for the pertinent rights and privileges of the various securities […]

978-1259722660 Chapter 18 Solution Manual Part 6

Problem 18–3 Requirement 1 February 15, 2018 (a) Retired Common stock (300,000 shares x $1 par)…………………….. 300,000 (b) Accounted for as treasury stock Treasury stock (300,000 shares x $8)………………………….. 2,400,000 Cash (300,000 shares x $8)……………………………………. 2,400,000 February 17, 2019 (a) […]

978-1259722660 Chapter 18 Solution Manual Part 7

Problem 18–6 Requirement 1 2018 ($ in millions) Cash……………………………………………………………………………. 480 Preferred stock (1 million shares x $10 par per share)…………… 10 Paid-in capital—excess of par, preferred……………………… 470 Cash……………………………………………………………………………. 70 2019 ($ in millions) Common stock (3 million shares x $1 […]

978-1259722660 Chapter 18 Solution Manual Part 8

Problem 18–11 A stock dividend is the distribution of additional shares of stock to current shareholders of the corporation. The investor receives no assets, only additional shares. Because each shareholder receives the same percentage increase in To record the investment […]

978-1259722660 Chapter 18 Solution Manual Part 9

Real World Case 18–1 Requirement 1 Assuming the shares are issued at the midpoint of the price range indicated, Requirement 2 $ in millions Cash (determined above)…………………………………………………..398.750 Common stock (27.5 million shares x $.01 par)…………………. .275 Paid-in capital—excess of par […]

978-1259722660 Chapter 19 Lecture Note Part 1

CHAPTER 19 SHARE-BASED COMPENSATION AND EARNINGS PER SHARE Overview We’ve discussed a variety of employee compensation plans in prior chapters, including pension and other postretirement benefits in Chapter 17. In this chapter we look at some common forms of compensation […]

978-1259722660 Chapter 19 Lecture Note Part 2

Suggestions for Class Activities 1. Research Activity Microsoft reported the following in a recent annual report: Employee Stock Purchase Plan. We have an employee stock purchase plan for all eligible employees. Compensation expense for the employee stock purchase plan is […]

978-1259722660 Chapter 19 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 19 Solution Manual Part 10

Real World Case 19–7 Requirement 1 The note indicates that Best Buy does not include potentially dilutive shares of common stock when calculating EPS for the twelve months ended March 3, 2012. Requirement 2 Best Buy’s diluted earnings per share […]

978-1259722660 Chapter 19 Solution Manual Part 11

Case 19–12 (concluded) Requirement 2 Sometimes, the effect of potential common shares would be to increase, rather than decrease, EPS. These we refer to as “antidilutive” securities. Such securities are ignored when calculating both basic and diluted EPS. For example, […]

978-1259722660 Chapter 19 Solution Manual Part 2

Question 19–20 The accounting treatment of SARs depends on whether the award is considered an equity instrument or a liability. If the employer can choose to settle in shares rather than cash, the award is considered to be equity. If […]

978-1259722660 Chapter 19 Solution Manual Part 3

Exercise 19–2 Requirement 1 Requirement 2 no entry Requirement 3 ($ in millions) Compensation expense ($30 million ÷ 3 years)… 10 Paid-in capital—restricted stock…………….. 10 Requirement 4 Compensation expense ($30 million ÷ 3 years)… 10 Paid-in capital—restricted stock…………….. 10 Requirement […]

978-1259722660 Chapter 19 Solution Manual Part 4

1. EPS in 2018 (amounts in thousands, except per share amount) net Earnings income Per Share $400 $400 —————————————————————————— –––– = 2. EPS in 2019 (amounts in thousands, except per share amount) net Earnings income Per Share $400 $400 —————————————————————————— […]

978-1259722660 Chapter 19 Solution Manual Part 5

Requirement 1 three-year vesting period, reducing earnings by $30 million each year. 2017 Compensation expense………………………………………………………….. 30 Paid-in capital—restricted stock………………………………………….. 30 2018 Compensation expense………………………………………………………….. 30 Paid-in capital—restricted stock………………………………………….. 30 Requirement 2 The total compensation for the award is $90 million ($5 […]

978-1259722660 Chapter 19 Solution Manual Part 6

Requirement 1 We treat each individual vesting date as a separate award and allocate the compensation cost for each of the four groups (tranches) evenly over its individual vesting (service) period: Vesting Amount Fair Value Date Vesting per Option The […]

978-1259722660 Chapter 19 Solution Manual Part 7

Problem 19–7 Requirement 1 No entry until the end of the reporting period, but compensation must be estimated at the grant date: options fair estimated expected value total to vest per option compensation Requirement 2 December 31, 2018, 2019, 2020, […]

978-1259722660 Chapter 19 Solution Manual Part 8

(amounts in millions, except per share amounts) Basic EPS net preferred income dividends shares at Jan. 1 The incremental effect of the conversion of the preferred stock is: preferred dividends +120* ————————————— = $3.75 +32 conversion of preferred stock The […]

978-1259722660 Chapter 19 Solution Manual Part 9

Problem 19–19 (continued) Requirement 2 (amounts in millions, except per share amount) 2019 Basic EPS net income shares at Jan. 1 2019 Diluted EPS net income $160 $160 —————————————————————————— = —— = $.50 300 + (30 – 20*) + (15 […]

978-1259722660 Chapter 2 Lecture Note

CHAPTER 2 REVIEW OF THE ACCOUNTING PROCESS Overview Chapter 1 explained that the primary means of conveying financial information to investors, creditors, and other external users is through financial statements and related notes. The purpose of this chapter is to […]

978-1259722660 Chapter 2 Solution Manual Part 1

Question 2–1 External events involve an exchange transaction between the company and a separate economic entity. For every external transaction, the company is receiving Question 2–2 According to the accounting equation, there is equality between the total economic resources of […]

978-1259722660 Chapter 2 Solution Manual Part 10

Problem 2–10 (continued) McGUIRE CORPORATION Income Statement For the Year Ended December 31, 2018 Sales revenue …………………………………………… $342,000 Rent………………………………………………………. 12,000 Depreciation…………………………………………… 3,000 Miscellaneous ……………………………………….. 10,000 Total operating expenses ……………. 110,000 Operating income …………………………………….. 32,000 Other expense: Interest …………………………………………………. 3,600 Net […]

978-1259722660 Chapter 2 Solution Manual Part 11

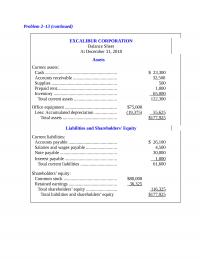

Problem 2–13 (continued) EXCALIBUR CORPORATION Balance Sheet At December 31, 2018 Assets Current assets: Cash ……………………………………………………… $ 23,300 Accounts receivable ……………………………….. 32,500 Liabilities and Shareholders’ Equity Current liabilities: Accounts payable …………………………………… $ 26,100 Salaries and wages payable ……………………… 4,500 Note […]

978-1259722660 Chapter 2 Solution Manual Part 2

Brief Exercise 2–12 Sales revenue………………………………………………………… 850,000 ……………………………………………………Income summary ……………………………………………………………………….850,000 Solutions Manual, Vol.1, Chapter 2 Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Income summary…………………………………………………… 815,000 ………………………………………………….Cost of goods […]

978-1259722660 Chapter 2 Solution Manual Part 3

Exercise 2–8 1. Prepaid insurance ($12,000 x 30/36)………………………… 10,000 Insurance expense………………………………………….. 10,000 2. Depreciation expense…………………………………………. 15,000 Accumulated depreciation ……………………………… 15,000 Solutions Manual, Vol.1, Chapter 2 Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior […]

978-1259722660 Chapter 2 Solution Manual Part 4

Exercise 2–15 Requirement 1 Supplies 11/30 Balance 1,500 Expense 2,000 Requirement 2 Prepaid insurance 11/30 Balance 6,000 Expense ? 12/31 Balance 4,500 Insurance expense for December = $6,000 – 4,500 = $1,500 December 31, 2018 Insurance expense………………………………………………….. 1,500 ……………………………………………………Prepaid insurance […]

978-1259722660 Chapter 2 Solution Manual Part 5

Exercise 2–21 Requirement 1 June 30 – adjusting entry Salaries and wages expense ($10,000 x 3/5)………………….. 6,000 July 1 – reversing entry Salaries and wages payable…………………………………….. 6,000 ……………………………………..Salaries and wages expense …………………………………………………………………………..6,000 July 2 – payment of salaries Salaries and […]

978-1259722660 Chapter 2 Solution Manual Part 6

Problem 2–2 (continued) Requirements 1 and 3 BALANCE SHEET ACCOUNTS Cash Accounts receivable _____________________________ _____________________________ 1/1 Bal. 5,000 1/1 Bal. 1/31 Bal. Inventory Equipment _____________________________ _____________________________ 1/1 Bal. 5,000 1/1 Bal. 1/10 9,500 2,000 1/1 1/2 5,500 2,800 1/8 1/13 […]

978-1259722660 Chapter 2 Solution Manual Part 7

Problem 2–4 (continued) PASTINA COMPANY Statement of Shareholders’ Equity For the Year Ended December 31, 2018 Total Common Retained Shareholders’ Stock Earnings Equity Balance at January 1, 2018 $60,000 $28,500 $ 88,500 Issue of common stock – 0 – – […]

978-1259722660 Chapter 2 Solution Manual Part 8

Problem 2–6 (continued) INCOME STATEMENT ACCOUNTS Service revenue Miscellaneous expenses _____________________________________________________________________________ _____________________________________________________________________________ 0 1/1 Bal. 0 Salaries expense _____________________________________________________________________________ 1/1 Bal. 0 d. 41,000 _______ 12/31 Bal. 41,000 Requirement 4 Account Title Debits Credits Cash 45,800 Accounts receivable 17,700 Equipment […]

978-1259722660 Chapter 2 Solution Manual Part 9

Requirement 2 Income overstated (understated) Adjustments to revenues: Adjustments to expenses: Overstatement of insurance expense (1,500) Understatement of depreciation expense 6,000 Understatement of interest expense 600 Understatement of supplies expense 1 ,100 Overstatement of net income $3 ,600 Understatement of […]

978-1259722660 Chapter 20 Lecture Note Part 1

CHAPTER 20 ACCOUNTING CHANGES AND ERROR CORRECTIONS Overview Chapter 4 provided a brief overview of accounting changes and error correction. Later, we discussed changes encountered in connection with specific assets and liabilities as we dealt with those topics in subsequent […]

978-1259722660 Chapter 20 Lecture Note Part 2

3. Professional Skills Development Activities The following are suggested assignments from the end-of-chapter material that will help your students develop their communication, research, analysis, and judgment skills. Communication Skills. Ethics Case 20–3, Research Case 20–7, and Problem 20–10 are suitable […]

978-1259722660 Chapter 20 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 20 Solution Manual Part 10

Problem 20-16 Fair value adjustment calculation: Investment balance, December 31, 2018, as reported $250,000 Error adjustment 40,000 Corrected balance, 12/31/2018 $290,000 Fair value, 12/31/2018 (274,000) Fair value credit adjustment needed, 12/31/2018 $ 16,000 c. Loss–lawsuit……………………………………………………………. 130,000 Liability—lawsuit…………………………………………………. 130,000 d. Cost […]

978-1259722660 Chapter 20 Solution Manual Part 11

Analysis Case 20-4 For changes not involving LIFO or changes from the LIFO method to another, the event is accounted for as a normal change in accounting principle. In general, we report voluntary changes in accounting principles retrospectively. This means […]

978-1259722660 Chapter 20 Solution Manual Part 12

Judgment Case 20-10 Situation I 2.The change in estimate should be reflected in the current period and in future periods. Unlike a change in accounting principle, the change in accounting estimate should not be applied retrospectively. 3.This change in accounting […]

978-1259722660 Chapter 20 Solution Manual Part 2

Brief Exercise 20-1 To record the change: ($ in millions) Retained earnings ……………………………………………………………………………. 8.2 Inventory ($32 million – 23.8 million)………………………………. 8.2 B & B applies the average cost method retrospectively; that is, to all prior Then, the cumulative effects of […]

978-1259722660 Chapter 20 Solution Manual Part 3

Brief Exercise 20-12 (concluded) Error b 1. To include the $3 million in year 2018 purchases and increase retained earnings to what it would have been if 2017 cost of goods sold had not included the $3 million purchases. Analysis: […]

978-1259722660 Chapter 20 Solution Manual Part 4

Exercise 20-6 The FASB Accounting Standards Codification® represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. Reporting most changes in accounting principle: 2. Disclosure requirements for a […]

978-1259722660 Chapter 20 Solution Manual Part 5

Exercise 20-15 Requirement 1 A deferred tax liability is established using the currently enacted tax rate for the year(s) a temporary difference is expected to reverse. In this case that rate was ($ in millions) Income tax expense (to balance)………………………………………… […]

978-1259722660 Chapter 20 Solution Manual Part 6

Exercise 20-21 Requirement 1 The error caused both 2016 net income and 2017 net income to be overstated, so retained earnings is overstated by a total of $85,000. Also, the note payable would be understated by the same amount. Remember, […]

978-1259722660 Chapter 20 Solution Manual Part 7

Problem 20-4 Requirement 1 To record the change: Retained earnings (net effect) ………………………………………….. 12,000 Note: For financial reporting purposes, but not for tax, the company is retrospectively decreasing accounting income, but not taxable income. This creates a temporary difference between […]

978-1259722660 Chapter 20 Solution Manual Part 8

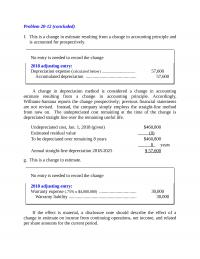

Problem 20-8 (concluded) A change in depreciation method is considered a change in accounting estimate resulting from a change in accounting principle. Accordingly, the Hoffman Group reports the change prospectively; previous financial statements are not revised. Instead, the company simply […]

978-1259722660 Chapter 20 Solution Manual Part 9

Problem 20-12 (concluded) f. This is a change in estimate resulting from a change in accounting principle and is accounted for prospectively. No entry is needed to record the change 2018 adjusting entry: A change in depreciation method is considered […]

978-1259722660 Chapter 21 Lecture Note Part 1

CHAPTER 21 THE STATEMENT OF CASH FLOWS REVISITED Overview The objective of financial reporting is to provide investors and creditors with useful information, primarily in the form of financial statements. The balance sheet and the income statement—the focus of your […]

978-1259722660 Chapter 21 Lecture Note Part 2

3. Spreadsheet Activity Have students create a functional spreadsheet in Excel or some other spreadsheet program capable of being used to help prepare a statement of cash flows. Suggest that the spreadsheet: 1. Accommodate debit and credit “explanations” for changes […]

978-1259722660 Chapter 21 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 21 Solution Manual Part 10

Problem 21–14 (continued) Spreadsheet for the Statement of Cash Flows (continued) Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Statement of Cash Flows Operating activities: Net income (1)50 Adjustments for noncash effects: Depreciation expense (2)22 Bad debt expense (3) 8 […]

978-1259722660 Chapter 21 Solution Manual Part 11

METAGROBOLIZE INDUSTRIES Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 375 (15)205 580 Accounts receivable 450 (7)150 600 6 ,880 Liabilities: Accounts payable 450 (9)300 750 Accrued expenses 225 […]

978-1259722660 Chapter 21 Solution Manual Part 12

Problem 21–19 (continued) INCOME STATEMENT ACCOUNTS Sales Dividend Revenue ________________________ ________________________________ Cost of Goods Sold Salaries Expense ________________________ ________________________________ 120 25 __________ (3) 120 (4) 25 Depreciation Expense Bad Debt Expense ________________________ ________________________________ 5 1 __________ (5) 5(1) 1 Interest […]

978-1259722660 Chapter 21 Solution Manual Part 13

Problem 21–21 (continued) INCOME STATEMENT ACCOUNTS Sales Investment Revenue ________________________ ________________________________ Gain on Sale of Treasury Bills Cost of Goods Sold ________________________ ________________________________ 2 180 __________ 2(3) (4) 180 Salaries Expense Depreciation Expense ________________________ ________________________________ 73 12 __________ (5) 73 […]

978-1259722660 Chapter 21 Solution Manual Part 14

Analysis Case 21–5 Requirement 1 (a) Cash _________________________________________________________________ Beginning balance ? Beginning cash + Net increase in cash = Ending cash Beginning cash + 183 = 360 Beginning cash = 360 – 183 Beginning cash = 177 (b) Accounts Receivable […]

978-1259722660 Chapter 21 Solution Manual Part 15

Research Case 21–9 Requirement 1 The specific citation that specifies the classification of notes payable to suppliers is Requirement 2 Specifically, paragraph 45–17a states that cash outflows for operating activities include payments to acquire materials for manufacture or goods for […]

978-1259722660 Chapter 21 Solution Manual Part 2

($ in millions) Interest expense (10% x 1/2 x $380) 19 Agee would report the cash inflow of $380 million from the sale of the bonds as a cash inflow from financing activities in its statement of cash flows. The […]

978-1259722660 Chapter 21 Solution Manual Part 3

Cost of Accounts Cash paid to Situation goods sold Inventory payable suppliers increase increase (decrease) (decrease) 2 200 6 0 206 2. Summary Entry Cost of goods sold 200 Inventory 6 Cash (paid to suppliers of goods) 206 3 200 […]

978-1259722660 Chapter 21 Solution Manual Part 4

Exercise 21–15 Wilson would report the $3,000,000* investment in the commercial food The $391,548 ($195,774* + 195,774**) cash lease payments are divided into the interest portion and the principal portion. The interest portion, $84,127, is reported as cash outflows from […]

978-1259722660 Chapter 21 Solution Manual Part 5

Direct Method Cash Flows from Operating Activities: Cash received from customers $672 Cash paid to suppliers (234) The depreciation expense, patent amortization expense, and loss on sale of land are not cash flows. Indirect Method Cash Flows from Operating Activities: […]

978-1259722660 Chapter 21 Solution Manual Part 6

$ in millions Pension expense (given) 82 Plan assets (expected return) 90 Exercise 21–28 PBO ($112 service cost + $51 interest cost) 163 Amortization of net loss—OCI (given) 1 Amortization of prior service cost—OCI (given) 8 Plan assets 9 Gain—OCI […]

978-1259722660 Chapter 21 Solution Manual Part 7

WRIGHT COMPANY Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 30 (15)12 42 Accounts receivable 75 (1) 2 73 Liabilities: Accounts payable 35 (2) 7 28 Salaries payable 5 […]

978-1259722660 Chapter 21 Solution Manual Part 8

METAGROBOLIZE INDUSTRIES Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 375 (14)205 580 Liabilities: Accounts payable 450 (4)300 750 Accrued expenses 225 (9)75 300 Lease liability—land 0 (2)20 X(2)150 […]

978-1259722660 Chapter 21 Solution Manual Part 9

ARDUOUS COMPANY Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 81 (21)28 109 Accounts receivable 194 (1) 4 190 Investment rev. receivable 4 (2) 2 6 1 ,211 Liabilities: […]

978-1259722660 Chapter 3 Lecture Note Part 1

CHAPTER 3 THE BALANCE SHEET AND FINANCIAL DISCLOSURES Overview Chapter 1 stressed the importance of the financial statements in helping investors and creditors predict future cash flows. The balance sheet, along with accompanying disclosures, provides relevant information useful in helping […]

978-1259722660 Chapter 3 Lecture Note Part 2

5. Ethical Dilemma The chapter contains the following ethical dilemma: ETHICAL DILEMMA The Raintree Cosmetic Company has several loans outstanding with a local bank. The debt agreements all contain a covenant stipulating that Raintree must maintain a current ratio of […]

978-1259722660 Chapter 3 Solution Manual Part 1

Question 3–1 The purpose of the balance sheet, also known as the statement of financial position, is to present the financial position of the company on a particular date. Unlike the income statement, Question 3–2 The balance sheet does not […]

978-1259722660 Chapter 3 Solution Manual Part 2

Exercise 3–1 1. Total current assets 2. Short-term investments $90,000 – 5,000 – 20,000 – 60,000 = $5,000 3. Retained earnings Current assets + Long-term assets = Current liabilities + Long-term liabilities + Paid-in capital + Retained earnings (RE) $90,000 […]

978-1259722660 Chapter 3 Solution Manual Part 3

Exercise 3–12 1. (B) in a separate disclosure note. 2. (A) in the summary of significant policies note. 3. (C) on the face of the balance sheet. 4. (B) in a separate disclosure note. 5. (B) in a separate disclosure […]

978-1259722660 Chapter 3 Solution Manual Part 4

Exercise 3–19 1. Debt to equity ratio = Total liabilities ÷ Shareholders’ equity = 1.4 Shareholders’ equity × 1.4 = Total liabilities $2,500,000 × 1.4 = $3,500,000 = Total liabilities Total liabilities + Equity = Total assets $3,500,000 + 2,500,000 […]

978-1259722660 Chapter 3 Solution Manual Part 5

Problem 3–4 WEISMULLER PUBLISHING COMPANY Balance Sheet At December 31, 2018 Assets Current assets: Cash and cash equivalents (1) ………………………………………….. $ 95,000 Short-term investments …………………………………………………… 110,000 Property, plant, and equipment: Machinery and equipment ………………………………………………. $320,000 Less: Accumulated depreciation ………………………………………. (110 […]

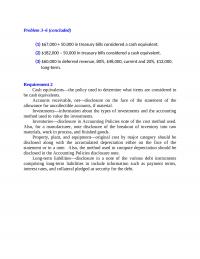

978-1259722660 Chapter 3 Solution Manual Part 6

Problem 3–6 (concluded) (1) $67,000 + 50,000 in treasury bills considered a cash equivalent. Requirement 2 Cash equivalents—the policy used to determine what items are considered to be cash equivalents. Accounts receivable, net—disclosure on the face of the statement of […]

978-1259722660 Chapter 3 Solution Manual Part 7

Communication Case 3–1 IBM manufactures and sells personal and mainframe computers. The computers included as current assets in the balance sheet for the company represent the cost of inventory available for sale. In addition, IBM uses computers in its operations. […]

978-1259722660 Chapter 3 Solution Manual Part 8

Real World Case 3–10 Requirement 3 a. Note 21 reports the following subsequent event: On February 5, 2014, the Company entered into agreements with Green Mountain Coffee Roasters, Inc. (“GMCR”), providing for the development and introduction of the Company’s global […]

978-1259722660 Chapter 4 Lecture Note Part 1

CHAPTER 4 THE INCOME STATEMENT, COMPREHENSIVE INCOME, AND THE STATEMENT OF CASH FLOWS Overview This chapter has a threefold purpose: (1) To consider important issues dealing with the content, presentation, and disclosure of net income and other components of comprehensive […]

978-1259722660 Chapter 4 Lecture Note Part 2

PowerPoint Slides Three PowerPoint presentations of the chapter are available in the Connect Library: 1. With “Concept Checks” useful for classroom presentation, permitting the instructor to intersperse in the presentation short exercises students can be asked to solve individually or […]

978-1259722660 Chapter 4 Solution Manual Part 1

Question 4–1 The income statement is a change statement that reports transactions— Question 4–2 Income from continuing operations includes the revenue, expense, gain, and loss transactions that will probably continue in future periods. It is important to segregate the income […]

978-1259722660 Chapter 4 Solution Manual Part 10

Requirement 5 The current ratios of the two firms are comparable and within the range of the Current ratio = Current assets Current liabilities Metropolitan = $1,203.0 = 0.94 $1,280.2 Republic = $1,478.7 =0.83 $1,787.1 Acid-test ratio = Quick assets […]

978-1259722660 Chapter 4 Solution Manual Part 11

Judgment Case 4–6 Financial Statement Presentation Situation Treatment (a–g) (CO, BC, or RE) 1. a. CO 2. b. RE 3. e. CO 4. f. CO 5. a. CO 6. d. BC 7. c. RE Judgment Case 4–7 1. The loss […]

978-1259722660 Chapter 4 Solution Manual Part 12

Case 4–15 (concluded) 1. The company could have chosen to present the information in the two statements in a single, continuous statement of comprehensive income. 2. The company reported the following other comprehensive income items: a. Foreign currency translation adjustments. […]

978-1259722660 Chapter 4 Solution Manual Part 2

Brief Exercise 4–3 PACIFIC SCIENTIFIC CORPORATION Income Statement For the Year Ended December 31, 2018 ($ in millions) Operating expenses: Selling………………………………………………………. $126 General and administrative………………………….. 105 Total operating expenses …………………………. 231 Operating income ………………………………………… 635 Other income (expense): Gain on […]

978-1259722660 Chapter 4 Solution Manual Part 3

Brief Exercise 4–15 Receivables turnover ratio = Net sales Average accounts receivable (net) Receivables turnover ratio = $600,000 [$100,000 + 120,000] ÷ 2 Inventory turnover ratio = $400,000* [$80,000 + 60,000] ÷ 2 =5.45 times =5.71 times Inventory turnover ratio […]

978-1259722660 Chapter 4 Solution Manual Part 4

Exercise 4–5 AXEL CORPORATION Income Statement For the Year Ended December 31, 2018 Sales revenue ………………………………………………. $ 592,000 Operating expenses: Selling …………………………………………………….. $67,000 Administrative …………………………………………. 87,000 Restructuring costs ……………………………………. 55 ,000 Total operating expenses …………………………. 209 ,000 Operating income ………………………………………… […]

978-1259722660 Chapter 4 Solution Manual Part 5

Exercise 4–16 (concluded) Requirement 2 WAINWRIGHT CORPORATION Statement of Cash Flows For the Month Ended March 31, 2018 Cash flows from operating activities: Collections from customers $ 55,000 Cash flows from investing activities: Purchase of equipment (10 ,000) Net cash […]

978-1259722660 Chapter 4 Solution Manual Part 6

Exercise 4–23 The FASB Accounting Standards Codification® represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. The calculation of the weighted average number of shares for basic […]

978-1259722660 Chapter 4 Solution Manual Part 7

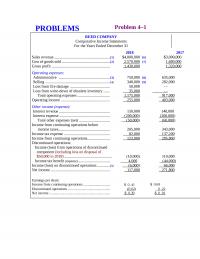

Problem 4–1 REED COMPANY Comparative Income Statements For the Years Ended December 31 2018 2017 Sales revenue …………………………………………………[1] $4,000,000 [6] $3,000,000 Operating expenses: Administrative …………………………………………….[3] 750,000 [8] 635,000 Selling ………………………………………………………..[4] 340,000 [9] 282,000 Loss from fire damage ………………………………….. 50,000 – […]

978-1259722660 Chapter 4 Solution Manual Part 8

Problem 4–8 DUKE COMPANY Statement of Comprehensive Income For the Year Ended December 31, 2018 Sales revenue ………………………………………………………… $15,000,000 Operating expenses: General and administrative …………………………………… $1,000,000 Selling ………………………………………………………………. 500,000 Restructuring costs ………………………………………………. 300,000 Loss from write-down of obsolete inventory …………… […]

978-1259722660 Chapter 4 Solution Manual Part 9

Requirement 2 The return on assets indicates a company’s overall J&J’s profitability is significantly higher than that of Pfizer. Rate of return on assets = Net income Total assets profitability, ignoring specific sources of financing. In this regard, J&J = […]

978-1259722660 Chapter 5 Lecture Note Part 1

CHAPTER 5 REVENUE RECOGNITION Overview In Chapter 4, we discussed net income and its presentation in the income statement. In Chapter 5, we focus on revenue recognition, which determines when and how much revenue appears in the income statement. In […]

978-1259722660 Chapter 5 Lecture Note Part 2

Supplement: GAAP in Effect Prior to ASU No. 2014-09 I. Summary of GAAP Changes A. ASU No. 2014-09 replaced over 200 specific items of revenue recognition guidance. Illustration 5–S1 summarizes some important changes in GAAP that occurred. II. The Realization […]

978-1259722660 Chapter 5 Solution Manual Part 1

Chapter 5 Revenue Recognition and Profitability Analysis QUESTIONS FOR REVIEW OF KEY TOPICS Question 5–1 The five key steps in applying the core revenue recognition principle are: 1. Identify the contract with a customer. 5. Recognize revenue when (or as) […]

978-1259722660 Chapter 5 Solution Manual Part 10

Problem 5-1 (concluded) Requirement 2 a. Number of performance obligations in the contract: 1. The access to the gym for 50 visits is one performance obligation. The option to is not a performance obligation in the contract. (Note: It could […]

978-1259722660 Chapter 5 Solution Manual Part 11

Problem 5–6 Requirement 1 Cash 80,000 Deferred revenue 80,000 $80,000 is recognized as deferred revenue. Requirement 2 Deferred revenue ($80,000 ÷ 10) Bonus receivable ($40,000 ÷ 10) 8,000 4,000 Service revenue 12,000 Super Rise earns revenue of $12,000 associated in […]

978-1259722660 Chapter 5 Solution Manual Part 12

Requirement 5 2018 2019 2020 Costs incurred during the year $2,400,000 $3,800,000 $3,900,000 2018 2019 2020 Contract price $10 ,000,000 $10 ,000,000 $10,000,000 Actual costs to date 2,400,000 6,200,000 10,100,000 Estimated costs to complete 5 ,600,000 4 ,100,000 – 0 […]

978-1259722660 Chapter 5 Solution Manual Part 13

Problem 5–15 Requirement 1 2018 cost recovery % : $180,000 2019 cost recovery %: $280,000 = 70% (gross profit % = 30%) $400,000 2018 gross profit: Cash collection from 2018 sales = $120,000 x 40% = $48,000 2019 gross profit: […]

978-1259722660 Chapter 5 Solution Manual Part 14

Problem 5–19 Requirement 1 a. January 30, 2018 Cash ……………………………………………………………………. 200,000 1,200,000 b. September 1, 2018 Deferred franchise fee revenue………………………………… 1,200,000 Franchise fee revenue ………………………………………… 1,200,000 c. September 30, 2018 Accounts receivable ($40,000 x 3%) …………………………… 1,200 Service revenue …………………………………………………. […]

978-1259722660 Chapter 5 Solution Manual Part 15

Communication Case 5–7 The critical question that student groups should address is how to account for The preferred solution should include the idea that the sale of an ice cream cone to a person who has a card involves two […]

978-1259722660 Chapter 5 Solution Manual Part 16

Target Case Requirement 1 Target reports Sales revenue of $73,785 million for the 2015 fiscal year, which ended January 30, 2016. Requirement 2 Recording revenue at the point of sale indicates that Target records revenue at the Requirement 3 Target […]

978-1259722660 Chapter 5 Solution Manual Part 2

Question 5–21 Sometimes a company arranges for another company to sell its product under consignment. The “consignor” physically transfers the goods to the other company commission and approved expenses) to the consignor. Because the consignor retains the risks and rewards […]

978-1259722660 Chapter 5 Solution Manual Part 3

Brief Exercise 5-11 Number of performance obligations in the contract: 1. The separate goods and services that Precision Equipment has agreed to provide each other. The contractor’s role is to integrate and customize them to create one automated assembly line. […]

978-1259722660 Chapter 5 Solution Manual Part 4

Brief Exercise 5–40 Orange has separate sales prices for the two parts of LearnIt-Plus, so the that revenue will be deferred and recognized over the life of the one-year period in which the Office Hours are delivered. If LearnIt were […]

978-1259722660 Chapter 5 Solution Manual Part 5

Exercise 5-8 Requirement 1 Number of performance obligations in the contract: 2. Delivery of keyboards is one performance obligation. The special discount being distinct, as it could be sold or provided separately, and it is separately identifiable, as it is […]

978-1259722660 Chapter 5 Solution Manual Part 6