Archives

978-0078025532 Appendix C Lecture Note

Appendix I Base Case Analysis of Park Hill Acres Without Superstore WACC 15% Sales Growth Rate 4% Cost of Good Sold 75.30% Salary Costs 11.90% Employee Benefits 25% Other Employee Costs 0.55% Base Rent 97,900 % Rent 0.00% Advertising 0.90% […]

978-0078025532 Appendix C Lecture Note Part 2

Appendix VII Base Case Analysis of Webster Street Store With 30% Loss to Albertson Superstore WACC 15% Sales Growth Rate 4% Cost of Good Sold 75.90% Salary Costs 12.10% Employee Benefits 25% Other Employee Costs 0.60% Base Rent $79,400 % […]

978-0078025532 Chapter 1 Lecture Note

Chapter 1 – Cost Management and Strategy 1-1 Chapter 1 Cost Management and Strategy Teaching Notes for Cases 1-1. Critical Success Factors The critical success factors for Kirsten’s business, including the proposed new publishing business are related to the needs […]

978-0078025532 Chapter 1 Solution Manual Part 1

Chapter 1 – Cost Management and Strategy 1-1 CHAPTER 1: COST MANAGEMENT AND STRATEGY QUESTIONS 1-1 Firms Using Cost Management. Here are some examples; there are many possible answers. 1. Wal-Mart: to keep costs low by streamlining restocking and sales […]

978-0078025532 Chapter 1 Solution Manual Part 2

Chapter 1 – Cost Management and Strategy 1-16 1-27 (continued –1) 4. Business intelligence (BI) is becoming a critical management tool for many companies, so a variety of industries and companies could be chosen. Some examples provided in Chapter 8 […]

978-0078025532 Chapter 1 Solution Manual Part 3

Chapter 1 – Cost Management and Strategy 1-31 The category, technology and data, is also likely to be different for a manufacturer. While data management is critical for a health insurance and health services company like UHG that has many […]

978-0078025532 Chapter 10 Case

Case 10-2: Letsgo Travel Trailers Data Input Area Exhibit 1: Actual and Projected Sales in Number of Trailers 1992 1993 1994 1995 1996 1997 Actual sales 13,765 14,880 15,991 17,809 19,634 23,322 1998 1999 2000 2001 2002 Projected sales 28,000 […]

978-0078025532 Chapter 10 Lecture Note

Chapter 10 – Strategy and the Master Budget 10-1 Chapter 10 Strategy and the Master Budget Teaching Notes for Cases 10-1: Emerson Electric Company Background • Emerson is an $8 billion company. • Its successful strategy is efficient, quality, and […]

978-0078025532 Chapter 10 Lecture Note Part 2

Chapter 10 – Strategy and the Master Budget 10–16 **An external risk factor not mentioned in case: economic–threats to funding sources. Note this is included in COSO framework and may be mentioned in student solutions. Internal Risk Factors (see Table […]

978-0078025532 Chapter 10 Lecture Note Part 3

10–31 Exhibit 3 Use of Resource Drivers (time or usage) by Activities A1 A2 A3 A4 A5 A6 A7 A8 A9 A10 A11 A12 A13 Total Manager 1.00% 14.00% 70.00% 15.00% 100.00% Advisors 15.00% 15.00% 10.00% 8.00% 5.00% 10.00% 5.00% […]

978-0078025532 Chapter 10 Lecture Note Part 4

10–44 Reading 10-3: “How Challenging Should Profit Budget Targets Be? This article argues for using “highly achievable” budget targets, and explains six key advantages for doing so, including the favorable effect on a manager’s commitment and confidence. The article also […]

978-0078025532 Chapter 10 Solution Manual Part 2

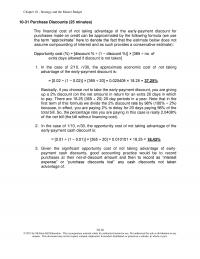

Chapter 10 – Strategy and the Master Budget 10–31 Purchase Discounts (25 minutes) The financial cost of not taking advantage of the early-payment discount for purchases made on credit can be approximated by the following formula (we use the term […]

978-0078025532 Chapter 10 Solution Manual Part 3

Chapter 10 – Strategy and the Master Budget 10–31 10-40 Activity–Based Budgeting (ABB) (20-30 Minutes) 1. Budgeted Cost- Activity Activity Driver Rate Total Cost Storage 400,000 $0.4925 $ 197,000 Requisition Handling 30,000 $12.50 $ 375,000 Pick Packing 800,000 $ 1.50 […]

978-0078025532 Chapter 10 Solution Manual Part 4

Chapter 10 – Strategy and the Master Budget 10–46 10–47 (Continued-5) 7. Budgeted selling and administrative expenses: Spring Manufacturing Company Selling and Administrative Expense Budget 2013 Selling Expenses: Advertising $60,000 Sales salaries 200,000 Travel and entertainment 60,000 Depreciation 5,000 $325,000 […]

978-0078025532 Chapter 10 Solution Manual Part 5

Chapter 10 – Strategy and the Master Budget 10–61 Alternatively, the end-of-December Accounts Payable Balance = Purchases made in December = answer to Part 5 above. 10-51 Retailer Budget (50 minutes) 1. Budgeted merchandise purchases D. Tomlinson Retail Budgeted Merchandise […]

978-0078025532 Chapter 10 Solution Manual Part 6

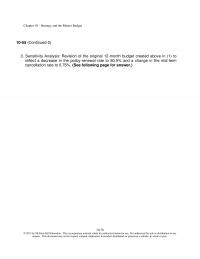

Chapter 10 – Strategy and the Master Budget 10–76 10–55 (Continued-2) 3. Sensitivity Analysis: Revision of the original 12-month budget created above in (1) to reflect a decrease in the policy-renewal rate to 80.0% and a change in the mid-term […]

978-0078025532 Chapter 10 Solution Manual Part 7

Chapter 10 – Strategy and the Master Budget 10–89 Cell references: $73,125 = cell G32 (=G23); $4,687.50 = cell G42 (=SUM(G37:G41)); $56,250.00 = cell G43. Revised Level of Monthly Processing Costs (other than materials): Month Labor Electricity 1 $3,465.00 $1,175.63 […]

978-0078025532 Chapter 11 Lecture Note

Chapter 11 – Decision Making with a Strategic Emphasis 11-1 Chapter 11 Decision Making with a Strategic Emphasis Teaching Notes for Cases Case 11-1: Product-Promotion Strategies; Use of Probabilities Question 1: Exquisite Foods Incorporated (EFI) wishes to select the most […]

978-0078025532 Chapter 11 Lecture Note Part 2

Chapter 11 – Decision Making with a Strategic Emphasis 11–16 Some students may consider the implementation of a shared-services arrangement without the investment in a systems upgrade. The cost incurred would be only the $45,000 in consultant fees. However, it […]

978-0078025532 Chapter 11 Lecture Note Part 3

Chapter 11 – Decision Making with a Strategic Emphasis 11–26 • Channels – Pop’s, Inc. needs to research specific target markets and develop products to meet those specific consumer’s needs. Pop’s, Inc. could do this by providing private labeled soda […]

978-0078025532 Chapter 11 Solution Manual

Chapter 11 – Decision Making with a Strategic Emphasis 11-1 CHAPTER 11: DECISION MAKING WITH A STRATEGIC EMPHASIS QUESTIONS 11-1 Relevant costs are costs to be incurred at some future time and differ for each option available to the decision […]

978-0078025532 Chapter 11 Solution Manual Part 2

Chapter 11 – Decision Making with a Strategic Emphasis 11–16 11–26 Sell or Process Further; Product Mix (30-40 min) 1. The key is to identify the relevant costs and revenues associated with any GR37 diverted for production of SilPol (silver […]

978-0078025532 Chapter 11 Solution Manual Part 3

Chapter 11 – Decision Making with a Strategic Emphasis 11–31 11–30 (continued-2) More generally, the minimum selling price per unit = incremental costs (variable + fixed + opportunity): Out-of-pocket costs: Variable out-of-pocket costs per meal $2.00 Fixed out-of-pocket costs per […]

978-0078025532 Chapter 11 Solution Manual Part 4

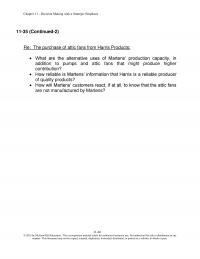

Chapter 11 – Decision Making with a Strategic Emphasis 11–46 11-35 (Continued-2) Re: The purchase of attic fans from Harris Products: • What are the alternative uses of Martens’ production capacity, in addition to pumps and attic fans that might […]

978-0078025532 Chapter 11 Solution Manual Part 5

Chapter 11 – Decision Making with a Strategic Emphasis 11–61 future service demand? (Would negative media coverage reduce demand?) • Does the existing cleaning compound create a hazardous work environment for employees (the problem is silent on this issue)? • […]

978-0078025532 Chapter 11 Solution Manual Part 6

Chapter 11 – Decision Making with a Strategic Emphasis 11–76 No Frills Standard Super Model Model Model CM per unit $13.00 $23.00 $27.00 Relative machine hours/unit 1.00 2.00 2.00 CM per relative hour $13.00 $11.50 $13.50 across the three products, […]

978-0078025532 Chapter 11 Solution Manual Part 7

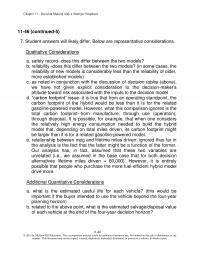

Chapter 11 – Decision Making with a Strategic Emphasis 11–88 11–46 (continued-5) 7. Student answers will likely differ. Below are representative considerations. Qualitative Considerations a. safety record—does this differ between the two models? b. reliability—does this differ between the two […]

978-0078025532 Chapter 12 Lecture Note

Chapter 12 – Strategy and the Analysis of Capital Investments 12-1 Chapter 12 Strategy and the Analysis of Capital Investments Teaching Notes for Cases 12-1: Floating Investments (Source: Paul Rouse and Leigh Houghton, “Instructional Case: Floating Investments,” Journal of Accounting […]

978-0078025532 Chapter 12 Lecture Note Part 2

Chapter 12 – Strategy and the Analysis of Capital Investments 12–16 Option 1 – do nothing to both stores: Added value is $5.60 million. This number is the sum of the NPV of $3.492 million from Appendix VIII from the […]

978-0078025532 Chapter 12 Lecture Note Part 3

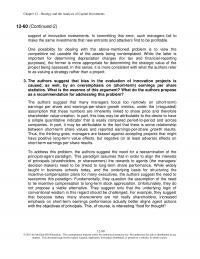

Chapter 12 – Strategy and the Analysis of Capital Investments 12–31 © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, […]

978-0078025532 Chapter 12 Lecture Note Part 4

Chapter 12 – Strategy and the Analysis of Capital Investments 12–39 Reading 12–6: Using Monte Carlo Simulation for a Capital Budgeting Project Although many types of analyses are useful in determining the scope and possible success of a project, Monte […]

978-0078025532 Chapter 12 Solution Manual Part 2

Chapter 12 – Strategy and the Analysis of Capital Investments 12–16 12–30 Future and Present Values Using Excel (30 minutes) A. To calculate future values, use the following Excel function: FV(rate,nper,pmt, pv,type) 1. Between January 1, 1701 and December 31, […]

978-0078025532 Chapter 12 Solution Manual Part 3

Chapter 12 – Strategy and the Analysis of Capital Investments 12–31 12–39 (Continued) 5. NPV Calculations under different assumptions regarding the discount rate (required rate of return) and annual after-tax net cash inflows. Assume a ten-year life and an initial […]

978-0078025532 Chapter 12 Solution Manual Part 4

Chapter 12 – Strategy and the Analysis of Capital Investments 12–46 12-46 (Continued) Step 2: Complete the following “Goal Seek” dialog box: Step 3: Results 4. Many firms raise the discount rate in evaluating a particular capital investment in view […]

978-0078025532 Chapter 12 Solution Manual Part 5

Chapter 12 – Strategy and the Analysis of Capital Investments 12–61 12–50 (Continued-2) PV of Cash Inflows, at t = 0: High: (=NPV(0.15,70,70,70)) ÷ (1 + 0.15) = $138.9789 million Medium: (=NPV(0.15,50,50,50)) ÷ (1 + 0.15) = $99.2707 million Low: […]

978-0078025532 Chapter 12 Solution Manual Part 6

Chapter 12 – Strategy and the Analysis of Capital Investments 12–76 12–54 (Continued-4) 1See part (1), Problem 12-53, reproduced as follows: Years 1 and 2: Depreciation expense per year (SL basis): ($120,000 – $20,000) 10 years = $10,000 Income […]

978-0078025532 Chapter 12 Solution Manual Part 7

Chapter 12 – Strategy and the Analysis of Capital Investments 12–91 12–58 MACRS Depreciation and Capital-Budgeting Analysis; Sensitivity Analysis; Spreadsheet Application (60 minutes) 1. The estimated after-tax NPV of this proposed investment is ($66,917), as follows: Net investment outlay, time […]

978-0078025532 Chapter 12 Solution Manual Part 8

Chapter 12 – Strategy and the Analysis of Capital Investments 12–99 12–60 (Continued-2) support of innovation investments. In committing this error, such managers fail to make the same investments that new entrants and attackers find to be profitable. One possibility […]

978-0078025532 Chapter 13 Lecture Note

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13-1 Chapter 13 Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing Teaching Notes for Cases […]

978-0078025532 Chapter 13 Solution Manual

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13-1 CHAPTER 13: Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing QUESTIONS 13-1 Target costing […]

978-0078025532 Chapter 13 Solution Manual Part 2

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13–16 13-35 Pricing (25 min) The price, contribution, and profit information is as follows. 1. $214.190 = ($7,385,875 × 1.45) ÷ 50,000 […]

978-0078025532 Chapter 13 Solution Manual Part 3

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13–31 © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in […]

978-0078025532 Chapter 13 Solution Manual Part 4

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing 13–39 13–48 Life-Cycle Costing; Ethics (25 min) 1. Waters’ analysis based on the prepared report fails to consider the very significant amount […]

978-0078025532 Chapter 14 Case

Porter’s Problems Co. Basic Information For Year Ended December 31, Year 2 Key Assumptions: Sales Information: Sales Numbers Trasposed for Copying Current Assets Cash $30,176 Accounts Receivable $413,250 Raw Materials Inventory $69,884 Finished Good Inventory $66,152 Total Current Assets $579,462 […]

978-0078025532 Chapter 14 Lecture Note

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-1 Chapter 14 Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures Teaching Notes for Case Case 14-1: Pet Groom […]

978-0078025532 Chapter 14 Lecture Note Part 2

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-9 Reading 14-5: Larry Grasso, “Are ABC and RCA Accounting Systems Compatible with Lean Management?,” Management Accounting Quarterly, Vol. 7, No. 1 (Fall 2005), […]

978-0078025532 Chapter 14 Solution Manual

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14-1 CHAPTER 14: OPERATIONAL PERFORMANCE MEASUREMENT: SALES, DIRECT-COST VARIANCES, AND THE ROLE OF NONFINANCIAL PERFORMANCE MEASURES QUESTIONS 14-1 A master budget represents forecasted operating […]

978-0078025532 Chapter 14 Solution Manual Part 2

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14–16 1. Right click anywhere in the worksheet area below. 2. Select “worksheet object” and then select “Open.” 3. To return to the Word […]

978-0078025532 Chapter 14 Solution Manual Part 3

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14–31 14-36 Ethical Considerations (20-25 minutes) 1. The IMA Statement of Ethical Professional Practice provides a set of four overarching principles designed to guide […]

978-0078025532 Chapter 14 Solution Manual Part 4

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14–46 14–44 Materials Purchase-Price Variance and Foreign Exchange Rates (20-30 minutes) 1. Actual Results Actual Purchase Standard Price Quantity Price Total Cost Price Variance […]

978-0078025532 Chapter 14 Solution Manual Part 5

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14–61 14-50 (Continued-4) Mr. Guglielmi says Meijer “expects employees to be at 100% performance to the standards, but we do not begin any formal […]

978-0078025532 Chapter 14 Solution Manual Part 6

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial Performance Measures 14–72 14–52 (Continued-1) ▪ Assembly Group 2,200 × 2.0 = 4,400 hours PCB Group 2,200 × 1.0 = 2,200 hours RH Group 2,200 × […]

978-0078025532 Chapter 15 Lecture Note

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-1 Chapter 15 Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management Teaching Notes for Readings Reading 15-1: Kennard T. Wing, “Using Enhanced Cost Models in Variance Analysis for Better […]

978-0078025532 Chapter 15 Lecture Note Part 2

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–10 traditional standard cost system (including the allocation of service department costs to production departments). The cost model used in the pilot implementation is depicted in Figure 1 of […]

978-0078025532 Chapter 15 Solution Manual

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15-1 CHAPTER 15: OPERATIONAL PERFORMANCE MEASUREMENT: INDIRECT-COST VARIANCES AND RESOURCE-CAPACITY MANAGEMENT QUESTIONS 15-1 The total factory overhead can be the same as the standard amount allowed for the current […]

978-0078025532 Chapter 15 Solution Manual Part 2

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–16 15–30 Performance Reporting: the Use of Standard Cost Variance Information (30 minutes) Among recommended improvements to the cost-variance report currently used by Zobel Manufacturing Company to evaluate subunit […]

978-0078025532 Chapter 15 Solution Manual Part 3

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–31 15–37 Factory Overhead Analysis–Two, Three, and Four Variances; Spreadsheet Application (50-60 Minutes) 1. Total Factory Overhead Application Rate: Fixed factory overhead application rate: Total machine hours at practical […]

978-0078025532 Chapter 15 Solution Manual Part 4

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–46 15–43 Income Statement Effects of Alternative Denominator Activity Levels; Spreadsheet Application (60 minutes) (1) Production Volume Variance: Budgeted Standard Standard Fixed OVH Production Fixed Fixed OVH Allowed Applied […]

978-0078025532 Chapter 15 Solution Manual Part 5

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–61 15–48 Proration of Variances (60 minutes) Proration of Direct Materials Variances Proration of DM Proration of DM Net Change Total $DM Standard Price Variance, PV Total after Usage […]

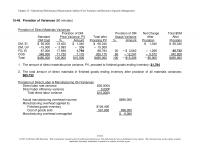

978-0078025532 Chapter 15 Solution Manual Part 6

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management 15–74 15–52 (Continued-2) efficiency of the customer order-handling process. (Note: this cost might increase a bit to cover the cost of the TQM initiative.) Note, however, that the cost […]

978-0078025532 Chapter 16 Lecture Note

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16–1 Chapter 16 Operational Performance Measurement: Further Analysis of Productivity and Sales Teaching Notes for Cases Case 16-1 Dallas Consulting Group* This case serves as a review of […]

978-0078025532 Chapter 16 Solution Manual

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16-1 CHAPTER 16: OPERATIONAL PERFORMANCE MEASUREMENT: FURTHER ANALYSIS OF PRODUCTIVITY AND SALES QUESTIONS 16-1 Productivity is the ratio of output to input. It is a measure of the […]

978-0078025532 Chapter 16 Solution Manual Part 2

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16–16 16-36 Productivity and the Economy (20 min) This question is intended for class discussion. Answers are likely to vary. Here are some points that could be brought […]

978-0078025532 Chapter 16 Solution Manual Part 3

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16–31 16–46 Direct Labor Variances, Productivity Measures, and Standard Costs (30 min) 1. Assembly Department Direct Labor Variances 2012: Total actual direct labor hours: 25 x 20,000 = […]

978-0078025532 Chapter 16 Solution Manual Part 4

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16–46 16–52 Sales Volume, Sales Quantity, and Sales Mix Variances (20 min) Sales Mix Budget Actual Flavor Quantity Mix Quantity Mix Vanilla 250,000 .3125 180,000 .18750 Chocolate 300,000 […]

978-0078025532 Chapter 16 Solution Manual Part 5

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales 16–55 The calculations for the volume and selling price variances are shown below. The volume variances for each product: Half Inch: $13,200 (F) = [(.3 x 6,500) – […]

978-0078025532 Chapter 17 Lecture Note

Chapter 17 – The Management and Control of Quality 17-1 Chapter 17 The Management and Control of Quality Teaching Notes for Cases Case 17-1: Precision Systems, Inc. This case illustrates that quality cost information can play an important role in […]

978-0078025532 Chapter 17 Lecture Note Part 2

Chapter 17 – The Management and Control of Quality 17–16 The rational is that in 10 to 30 years the petroleum product will break down naturally and will no longer be a hazard. If you did establish a contingent liability […]

978-0078025532 Chapter 17 Lecture Note Part 3

Chapter 17 – The Management and Control of Quality 17–29 Reading 17-6: Jan P. Brosnahan, “Unleash the Power of Lean Accounting,” Journal of Accountancy (July 2008), pp. 60-66. (Available at: http://www.journalofaccountancy.com/Issues/2008/Jul/UnleashthePowerofLeanAccounting.htm) The author of this article is divisional controller at […]

978-0078025532 Chapter 17 Solution Manual Part 2

Chapter 17 – The Management and Control of Quality 17–16 17–28 (Continued-2) Diminishing Returns Conceptualization: Trading Off Costs and Benefits for Spending on Quality Basically, the above representation assumes that after a point, increases in quality spending do not generate […]

978-0078025532 Chapter 17 Solution Manual Part 3

Chapter 17 – The Management and Control of Quality 17–31 17–37(Continued-1) The instructor might want to use some of the following example disclosures from First Energy Corporation (https://www.firstenergycorp.com/environmental.html) for illustrative purposes: Environmental Characteristics Associated with Various Sources of Power Generation […]

978-0078025532 Chapter 17 Solution Manual Part 4

Chapter 17 – The Management and Control of Quality 17–46 17–46 Value-Stream Income Statement (20-30 Minutes) The value stream income statement is shown below. Note that the temporary $28 million effect on income due to the decrease in inventory is […]

978-0078025532 Chapter 17 Solution Manual Part 5

Chapter 17 – The Management and Control of Quality 17–61 17–53 Cost-of-Quality (COQ) Reporting; Spreadsheet Application (45–60 Minutes) 1. LEE ENTERPRISES COST-OF-QUALITY REPORT FOR YEARS 2013 and 2014 © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized […]

978-0078025532 Chapter 17 Solution Manual Part 6

Chapter 17 – The Management and Control of Quality 17–74 some public information available on its efforts to address global warming. 17–58 (Continued-2) 4. As indicated in the referenced HBR piece (October 2007, pp. 30, 34), companies that have sub-par […]

978-0078025532 Chapter 18 Lecture Note

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-1 Chapter 18 Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard Teaching Notes for Cases 18-1 Industrial Chemical Company; Decentralization; Cost SBUs; International […]

978-0078025532 Chapter 18 Lecture Note Part 2

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–11 • Competence: The competence standard binds IMA members to “provide decision support information and recommendations that are accurate.” Will Mary violate the competence standard if […]

978-0078025532 Chapter 18 Solution Manual

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18-1 CHAPTER 18: STRATEGIC PERFORMANCE MEASUREMENT: COST CENTERS, PROFIT CENTERS, AND THE BALANCED SCORECARD QUESTIONS 18-1 Performance evaluation can be thought of as the process by […]

978-0078025532 Chapter 18 Solution Manual Part 2

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–16 18–28 Allocation of Marketing and Administrative Costs; Profit SBUs (20 min) 1. The 2012 and 2013 allocations using revenue as a base: (All numbers in […]

978-0078025532 Chapter 18 Solution Manual Part 3

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–31 Reference: Pierce, L. and J. Snyder. (2008). “Ethical Spillovers in Firms: Evidence from Vehicle Emissions Testing.” Management Science 54 (11): pp 1891-1903. 18–39 Allocation of […]

978-0078025532 Chapter 18 Solution Manual Part 4

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–46 18-45 Balanced Scorecard (15 min) Solution for problem 2-43, The Tartan Corporation. An example of a balanced scorecard for Tartan Corp follows: Financial Internal Customer […]

978-0078025532 Chapter 18 Solution Manual Part 5

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–61 Moreover, these income statements fail to include the amount invested in each of the divisions and geographical areas. Managers should be held accountable for the […]

978-0078025532 Chapter 18 Solution Manual Part 6

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard 18–76 18-59 (continued –1) 3. The scorecard perspectives appear to be correctly aligned with the mission statement which has goals for improvement in terms of patient […]

978-0078025532 Chapter 18 Solution Manual Part 7

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may […]

978-0078025532 Chapter 19 Lecture Note

Chapter 19 – Strategic Performance Measurement: Investment Centers 19-1 Chapter 19 Strategic Performance Measurement: Investment Centers Teaching Notes for Cases Case 19-1: Investment Centers 1. The prior performance measurement system was called “performance income,” and is best described as a […]

978-0078025532 Chapter 19 Lecture Note Part 2

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–16 © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025532 Chapter 19 Solution Manual

Chapter 19 – Strategic Performance Measurement: Investment Centers 19-1 CHAPTER 19: STRATEGIC PERFORMANCE MEASUREMENT: INVESTMENT CENTERS QUESTIONS 19-1 Investment centers are commonly used when there are a number of business units to be compared, and/or when top management intends to […]

978-0078025532 Chapter 19 Solution Manual Part 2

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–16 19–29 Return on Investment (ROI) for Innovative Companies (30-45 minutes, including reading time) The objective of this assignment is to engage the class in a discussion of the limitation of return […]

978-0078025532 Chapter 19 Solution Manual Part 3

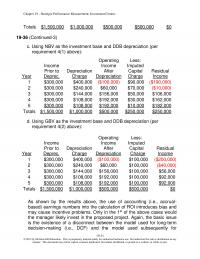

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–31 Totals $1,500,000 $1,000,000 $500,000 $500,000 $0 19–36 (Continued-3) c. Using NBV as the investment base and DDB depreciation (per requirement 4(1) above): Year Income Prior to Deprec. Depreciation Charge Operating Income […]

978-0078025532 Chapter 19 Solution Manual Part 4

Chapter 19 – Strategic Performance Measurement: Investment Centers © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025532 Chapter 19 Solution Manual Part 5

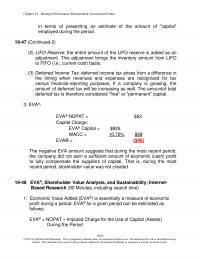

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–61 in terms of presenting an estimate of the amount of “capital” employed during the period. 19–47 (Continued-2) (2) LIFO Reserve: the entire amount of the LIFO reserve is added as an […]

978-0078025532 Chapter 19 Solution Manual Part 6

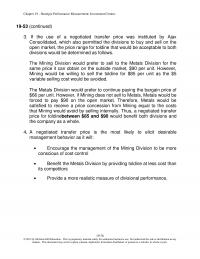

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–76 19–53 (continued) 3. If the use of a negotiated transfer price was instituted by Ajax Consolidated, which also permitted the divisions to buy and sell on the open market, the price […]

978-0078025532 Chapter 19 Solution Manual Part 7

Chapter 19 – Strategic Performance Measurement: Investment Centers 19–84 19–57 Transfer Pricing; Strategy (45–50 minutes) 1. At first glance, the overall strategy seems to be one of cost leadership, due to the competitive conditions in the global market and the […]

978-0078025532 Chapter 2 Lecture Note

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-1 Chapter 2 Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map Teaching Notes for Cases 2-1. Atlantic City Casino: Value Chain […]

978-0078025532 Chapter 2 Lecture Note Part 2

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-9 © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This […]

978-0078025532 Chapter 2 Solution Manual Part 1

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-1 CHAPTER 2: IMPLEMENTING STRATEGY: THE VALUE CHAIN, THE BALANCED SCORECARD, AND THE STRATEGY MAP QUESTIONS 2-1 The two types of competitive strategy (per Michael […]

978-0078025532 Chapter 2 Solution Manual Part 2

Chapter 2: Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-16 2-34 (continued -1) Each class will have different results, and these differences can be used for a discussion of the value to the consumer of […]

978-0078025532 Chapter 2 Solution Manual Part 3

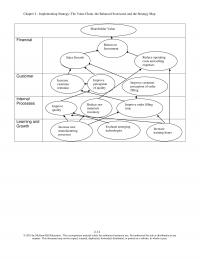

Chapter 2 – Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-31 Financial Customer Internal Processes Learning and Growth Improve order filling time Improve perception of quality Increase new manufacturing processes Improve quality Evaluate emerging technologies […]

978-0078025532 Chapter 2 Solution Manual Part 4

Chapter 2: Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-46 2-51 (continued –2) 3. Most students will be familiar with the Deepwater Horizon oil spill and its consequences. The purpose of the question is to […]

978-0078025532 Chapter 2 Solution Manual Part 5

Chapter 2: Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map 2-56 2-57 (continued -2) Weighting Financial 40% Customer 30% Processes 15% People 15% The bank’s approach and the weighting’s used could provide a useful basis for […]

978-0078025532 Chapter 20 Lecture Note

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-1 Chapter 20 Management Compensation, Business Analysis, and Business Valuation Teaching Notes for Cases 20-1. Midwest Petro-Chemical Company: Evaluation of a Firm; Strategy Adapted from teaching note provided by the […]

978-0078025532 Chapter 20 Lecture Note Part 2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–16 benefit. Cumulative Goodwill Amortization. Goodwill arises when the acquisition of another firm is recorded as a purchase and there is an excess of cost over the fair value of […]

978-0078025532 Chapter 20 Lecture Note Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–31 experience and commitment of its employees (an environment fostered by this long relationship) as one of its sustaining competitive advantages (Salter and Dayley 2000). If John Deere used (or […]

978-0078025532 Chapter 20 Solution Manual

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20-1 CHAPTER 20: MANAGEMENT COMPENSATION, BUSINESS ANALYSIS, AND BUSINESS VALUATION QUESTIONS 20-1 The key objective of the firm is to develop management compensation plans that support the firm’s strategic objectives: […]

978-0078025532 Chapter 20 Solution Manual Part 2

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–16 20-28 Compensation and Trust (15 min) This question is intended primarily for class discussion or for a short written project. The answers are likely to vary. I would have […]

978-0078025532 Chapter 20 Solution Manual Part 3

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–31 20–39 (continued -1) 2. [Operating Income – (.06 x Invested Assets)] x .10 = Bonus Amount The total bonuses for each division and in total are determined as follows: […]

978-0078025532 Chapter 20 Solution Manual Part 4

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation 20–43 20-45 (continued -1) Liquidity looks OK overall, except for the recent buildup in inventory. The current ratio has fallen below the bank restriction years ago, but has been safely […]

978-0078025532 Chapter 3 Lecture Note

Chapter 3 – Basic Cost Management Concepts 3-1 Chapter 3 Basic Cost Management Concepts Teaching Notes for Cases 3-1. Strategy; Critical Success Factors, Cost Objects, and Performance Measures Increasingly, students in accounting and business courses are expected to actively engage […]

978-0078025532 Chapter 3 Solution Manual Part 1

Chapter 3 – Basic Cost Management Concepts 3-1 CHAPTER 3: BASIC COST MANAGEMENT CONCEPTS QUESTIONS 3-1 Cost assignment refers to the general case of assigning costs to cost pools or cost objects. When there is a direct and traceable link […]

978-0078025532 Chapter 3 Solution Manual Part 2

Chapter 3 – Basic Cost Management Concepts 3-16 3-42 (continued –1) 3. The growth of the company globally means that the company will be more exposed to the effects of foreign currency fluctuations. For example, a falling dollar relative to […]

978-0078025532 Chapter 3 Solution Manual Part 3

Chapter 3 – Basic Cost Management Concepts 3-26 3-51 Classification of Costs (15 Min) Parts 1 and 2 Fixed(F) or Product (P) Variable (V) Period (PD) 1.Technicians F P 2.Parts V P 3.Purchase of oil and tires V P 4.Supplies […]

978-0078025532 Chapter 4 Lecture Note

Chapter 4 – Job Costing 4-1 Chapter 4 Job Costing Teaching Notes For Cases 4-1. Constructo Inc. (Under or Overapplied Overhead) This case has the learning objectives of: (1) explaining when it is appropriate for a company to use a […]

978-0078025532 Chapter 4 Solution Manual Part 1

Chapter 4 – Job Costing 4-1 CHAPTER 4: JOB COSTING QUESTIONS 4-1 The strategic role of costing is to provide accurate cost information that is need for product pricing, profitability analysis of products and customers, evaluation of managers, and refinement […]

978-0078025532 Chapter 4 Solution Manual Part 2

Chapter 4 – Job Costing 4-16 4-37 Application of Overhead (15 min) 1. Budgeted total overhead $360,125 Budgeted direct labor hours 33,500 Overhead rate $10.75 =$360,125/33,500 Job Direct Materials Gallons of Paint Direct Labor Hours Direct Labor Cost Applied Overhead […]

978-0078025532 Chapter 4 Solution Manual Part 3

Chapter 4 – Job Costing 4-31 h. Selling& Administrative Expense 2,400 Accumulated Depreciation 2,400 4-46 (Continued –1) i. Advertising Expense 5,500 Cash 5,500 j. Factory Overhead 13,500 Cash 13,500 k. Selling & Administrative Expense 13,250 Cash 13,250 l. Applied Overhead […]

978-0078025532 Chapter 4 Solution Manual Part 4

Chapter 4 – Job Costing 4-42 4-49 (continued –5) 2. Go to the Insert tab on the ribbon, and select the PivotTable button. You can choose Pivot Table or Pivot Chart; choose Pivot Table. 3. Once you have selected PivotTable […]

978-0078025532 Chapter 5 Lecture Note

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-1 Chapter 5 Activity-Based Costing and Customer Profitability Analysis Teaching Notes for Cases 5-1 Blue Ridge Manufacturing (Activity-Based Costing for Marketing Channels) Case Description: Blue Ridge Manufacturing produces and sells towels […]

978-0078025532 Chapter 5 Lecture Note Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-16 In practice, TOC accounting is similar to variable costing, and like variable costing, “Emphasis is placed on short-run differential or incremental costs rather than on long-run full costs” (Usry & […]

978-0078025532 Chapter 5 Lecture Note Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-29 Comparison Incrrease Total Total Batch Batch Total Total Batch Batch Total Total Batch Batch (Drop) in Cost Cost Total Gross Cost Cost Total Gross Cost Cost Total Gross Gross Product […]

978-0078025532 Chapter 5 Solution Manual Part 2

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-16 5-35 Customer Profitability Analysis (25 minutes) 1. Jerry Inc. Kate Co. Customer Unit Level Costs: Sales return(40×$5;175×$5) $200 $875 Customer Batch Level Costs: Order processing (5×$300; 30×$300) $1,500 $9,000 Sales […]

978-0078025532 Chapter 5 Solution Manual Part 3

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-31 5-42 (continued-1) Calculation for general administration allocated to branches: Total direct labor dollar: $382,413 + $317,086 + $317,188 = $1,016,687 Allocation of general administration based on direct labor dollar: Proportion […]

978-0078025532 Chapter 5 Solution Manual Part 4

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis 5-42 5-47 (continued –1) 2. The additional business with AS would leave very little unused capacity(less than 3%) as shown below: Total Calls Answered Avg. No. of Minutes/ Call Total Time […]

978-0078025532 Chapter 6 Solution Manual

Chapter 6 – Process Costing 6-1 CHAPTER 6: PROCESS COSTING QUESTIONS 6-1 A company that should use a process costing system typically has homogenous products, which pass through a series of similar processes or departments. These firms usually engage in […]

978-0078025532 Chapter 6 Solution Manual Part 2

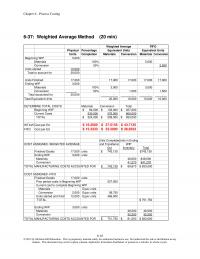

Chapter 6 – Process Costing 6-16 6-37: Weighted Average Method (20 min) Physical Percentage Units Completion Materials Conversion Materials Conversion Beginning WIP 5,000 Materials 100% 5,000 Conversion 50% 2,500 Units started 15,000 Total to account for 20,000 Units FinIshed 17,000 […]

978-0078025532 Chapter 6 Solution Manual Part 3

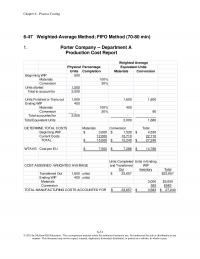

Chapter 6 – Process Costing 6-31 6-47 Weighted-Average Method; FIFO Method (70-80 min) 1. Porter Company — Department A Production Cost Report Physical Percentage Units Completion Materials Conversion Beginning WIP 500 Materials 100% Conversion 30% Units started 1,500 Total to […]

978-0078025532 Chapter 6 Solution Manual Part 4

Chapter 6 – Process Costing 6-40 Problem 6-50 (continued –2) Ted is apparently correct about the under-costing of ending working process. The activity-based method, which separates the batch-related costs from the other conversion costs, shows $104,329 ending work in process, […]

978-0078025532 Chapter 7 Lecture Note

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-1 Chapter 7 Cost Allocation: Departments, Joint Products, and By-Products Teaching Notes for Cases 7-1. Revenue Allocation; Utility Industry; Strategy This case concerns the process used in the state of […]

978-0078025532 Chapter 7 Solution Manual

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-1 CHAPTER 7: COST ALLOCATION: DEPARTMENTS, JOINT PRODUCTS, AND BY-PRODUCTS QUESTIONS 7-1 The four objectives in the strategic role of cost allocation are to achieve effective cost management through methods […]

978-0078025532 Chapter 7 Solution Manual Part 2

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-16 7-28 (continued -1) Premium Dept. Advertising Dept Sales Dept Allocation of Actuarial Dept $80,000 x .8 = $64,000 $80,000 x .1 = $8,000 $80,000 x .1 = $8,000 Allocation […]

978-0078025532 Chapter 7 Solution Manual Part 3

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-31 7-35 (continued –3) Sourcing Operations Asssembly Finishing Total DEPARTMENTAL ALLOCATION BASES Information Systems Hours 25,000 45,000 70,000 140,000 percent 17.8571% 32.1429% 50.00% 100% Facilities; square feet (000) 10,000 50,000 […]

978-0078025532 Chapter 7 Solution Manual Part 4

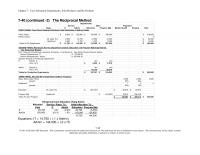

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-46 7-40 (continued -2) The Reciprocal Method Base IT Admin Education Program Mgt Mental Health Housing Total FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs Direct […]

978-0078025532 Chapter 7 Solution Manual Part 5

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products 7-58 7-45 (continued –2) Net Realizable Value Method M10 M15 M18 Total Units Sold 150,000 125,000 125,000 400,000 Price (after addt’l processing) 20$ 10$ 15$ Separable Processing cost 550,000$ 125,000$ […]

978-0078025532 Chapter 8 Lecture Note

Chapter 8 – Cost Estimation 8-1 Chapter 8 Cost Estimation Teaching Notes for Cases 8-1. High-Low Method and Regression Analysis 1, 2. The spreadsheet below shows the analysis of the Brenham Hospital data using both regression and high-low methods. Before […]

978-0078025532 Chapter 8 Lecture Note Part 2

Chapter 8 – Cost Estimation 8-11 Case 8-5 Predicting the Effect of Poverty on High School Graduation Rate High School graduation rates are a key measure of economic development and potential for economic growth. The data below show the graduation […]

978-0078025532 Chapter 8 Solution Manual

Chapter 8 – Cost Estimation 8-1 CHAPTER 8: COST ESTIMATION QUESTIONS 8-1 Cost estimation is the process of developing a well-defined relationship between a cost object and its cost driver for the purpose of predicting the cost. The cost predictions […]

978-0078025532 Chapter 8 Solution Manual Part 2

8-16 8-35 Cost Estimation: High-Low method (15 min) 1. Model to fit: Maintenance Expense = a + (b x M) (where M = machine hours) The highest and lowest points are months 6 and 10, respectively. Note that the point […]

978-0078025532 Chapter 8 Solution Manual Part 3

Chapter 8 – Cost Estimation 8-31 8-42 (continued – 3) 3. The Gilmore company is likely to have a number of sustainability issues in its business. As a company that renovates older homes, it must frequently deal with hazardous materials […]

978-0078025532 Chapter 8 Solution Manual Part 4

8-46 8-49 (continued -3) 2. If Lexon is involved in global production of its products, then expenses incurred from returns must be analyzed by production facility, as these costs are likely to differ among production facilities due to different equipment […]

978-0078025532 Chapter 8 Solution Manual Part 5

8-56 8-54 (continued –1) 2. The limitations of this regression are somewhat unique since the independent variables (except for average pay) and the dependent variable are rankings (ordinal numbers rather than real numbers). Thus, the issue of nonlinearity arises, but […]

978-0078025532 Chapter 9 Lecture Note

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9–1 Chapter 9 Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis Teaching Notes for Cases Case 9-1: CVP Analysis; Strategy This problem can perhaps be visualized most easily by first constructing a table […]

978-0078025532 Chapter 9 Lecture Note Part 2

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9–12 Case 9-5: Sensitivity Analysis: Regression Analysis 1. The regression analysis to identify the stores that seem to be operating at below their potential, based on relationships for all the stores […]

978-0078025532 Chapter 9 Solution Manual

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-1 CHAPTER 9: SHORT-TERM PROFIT PLANNING: COST-VOLUME-PROFIT (CVP) ANALYSIS QUESTIONS 9-1 The underlying relationship depicted in a cost-volume-profit (CVP) analysis is that costs, revenues, and operating profits (Y) all change in […]

978-0078025532 Chapter 9 Solution Manual Part 2

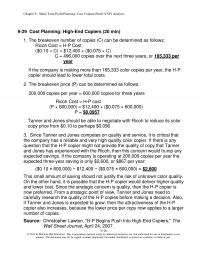

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-16 9-29 Cost Planning: High-End Copiers (20 min) 1. The breakeven number of copies (C) can be determined as follows: Ricoh Cost = H-P Cost ($0.10 × C) = $12,400 + […]

978-0078025532 Chapter 9 Solution Manual Part 3

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-31 9-38 Profit Planning: Multiple Products (50-60 min) 1. Break-even in units: weighted-average contribution margin approach a. Overall breakeven point = F ÷ weighted-average contribution margin/unit Weighted-average unit contribution per unit […]

978-0078025532 Chapter 9 Solution Manual Part 4

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-46 9-43 CVP Analysis; Commissions; Ethics (50 min) 1. Breakeven dollars (dollars in thousands), Y: Y = total fixed costs ÷ contribution margin ratio Y = ($6,120 + $1,890) ÷ (1 […]

978-0078025532 Chapter 9 Solution Manual Part 5

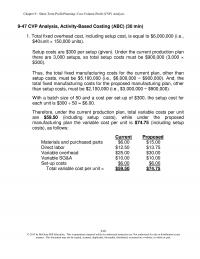

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-61 9-47 CVP Analysis, Activity-Based Costing (ABC) (30 min) 1. Total fixed overhead cost, including setup cost, is equal to $6,000,000 (i.e., $40/unit × 150,000 units). Setup costs are $300 per […]

978-0078025532 Chapter 9 Solution Manual Part 6

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis 9-74 9-49 (continued-4) 5. Calculation and interpretation of degree of operating leverage (DOL) under each decision alternative at Q = 400,000 units and at Q = 600,000 units. DOL, at any […]

AC 223

1) horton company uses a job costing system, and factory overhead is applied on the basis of machine hours. at the beginning of the year, management estimated that the company would incur $1,050,000 of factory overhead costs and use 70,000 […]

AC 232

1) in the current year, becker sofa company expected to sell 12,000 leather sofas. fixed costs for the year were expected to be $8,400,000; unit sales price was budgeted at $4,600; and unit variable costs were expected to be $2,200. […]

AC 249 Quiz 3

1) budgets can serve as the standard against which actual performance is measured. when compensation is based on this comparison, the organization is said to use: a.fixed performance contracts b.rolling financial forecasts c.continuous-improvement budgets d.variable compensation contracts e.a linear compensation […]

AC 392 Midterm

1) the ideal criterion for choosing an allocation base for overhead is: a.ease of calculation b.a cause-and-effect relationship c.ease of use d.its preciseness e.its applicability 2) consider the following for guardian manufacturing company: what are the cost of goods manufactured […]

AC 427 Midterm 1

1) a firm has decided to use the balanced scorecard. which of the following is not an advantage the company will gain by using the balanced scorecard? a.it links the firm’s csfs to its strategy b.it helps the firm monitor […]

AC 718

1) the following data pertains to lam co.’s manufacturing operations: additional information for the month of april: overhead is applied at $12 per direct labor hour. for the month of april, conversion cost incurred was: a.$75,000 b.$66,000 c.$70,000 d.$39,000 2) […]

AC 756 Midterm 2

1) moss manufacturing has just completed a major change in its quality control (qc) process. previously, products had been reviewed by qc inspectors at the end of each major process, and the company’s ten qc inspectors were charged as direct […]

AC 892 Quiz 3

1) the following information was taken from the accounting records of elliott manufacturing corp. unfortunately, some of the data were destroyed by a computer malfunction. cost of goods manufactured is calculated to be: a.$32,000 b.$30,000 c.$33,000 d.$38,000 e.$27,000 2) ardel […]

Acc 106 Test

1) sales forecasting by its nature is: a.precise b.deterministic in nature c.objective d.somewhat subjective e.mechanical 2) quick telephone response (qtr) was started several years ago to provide an outsource telephone service for the growing number of small, specialty catalog mail-order […]

Acc 165 Quiz 2

1) larsen company adds materials at the beginning of the process in department 2 . data concerning the materials used in may production are as follows: using the weighted-average method, the equivalent units for materials are: a.44,000 b.41,000 c.36,000 d.33,000 […]

Acc 192 Final

1) a manager of a large retail firm is interested in knowing what the company’s product costs are. which of the following would be considered a product cost for the manager’s company? a.direct materials b.direct labor c.factory overhead d.transportation costs […]

Acc 209 Quiz 2

1) committed or ‘sunk” costs are generally: a.not fixed b.small in amount c.the result of prior bad decisions d.those that have been incurred in the past e.recoverable in trade 2) the long term care plus company has two service departments […]

Acc 266 Test 1

1) a plan that states the units or costs of merchandise to be purchased by a retailer or wholesaler during the budget period is called a: a.production budget b.merchandise purchases budget c.accounts payable budget d.cash payments budget e.cost of goods […]

Acc 401 Quiz 1

1) based on analyzing the relationship of total factory overhead (y) to direct labor hours (x). the following relationship was found: y = $1,000 + $2x the equation was probably found through the use of which of the following mathematical […]

ACC 606 Test 2

1) based on analyzing the relationship of total factory overhead (y) to direct labor hours (x). the following relationship was found: y = $1,000 + $2x the relationship is: a.parabolic b.curvilinear c.linear d.probabilistic 2) which of the following is not […]

Acc 654 Midterm 2

1) the total cost of direct materials, direct labor, and factory overhead transferred from the work-in-process inventory account to the finished goods inventory account during an accounting period is: a.normal cost of goods sold b.adjusted cost of goods sold c.total […]

ACC 662 Quiz 2

1) many companies in the consumer products and electronics industries such as walmart and texas instruments compete using a strategy of: a.professionalism b.growth c.cost leadership d.abc costing e.target costing 2) financial budgets include the: a.pro forma balance sheet b.projected income […]

ACC 670 Test

1) which of the following is not a step in the cost estimation process? a.determine the cost drivers b.determine the outliers c.select and employ the estimation method d.graph the data 2) assume only the specified parameters change in a sensitivity […]

Accounting 167 Test 2

1) factory overhead costs for a given period were 2 times as much as the direct material costs. prime costs totaled $8,000. conversion costs totaled $11,350. what are the direct labor costs for the period? a.$4,650 b.$3,560 c.$4,200 d.$3,860 2) […]

Accounting 282 Test

1) national inc. manufactures two models of cmd that can be used as cell phones, mpx, and digital camcorders. national uses a volume-based costing system to apply factory overhead based on direct labor dollars. the unit prime costs of each […]

Accounting 332 Quiz

1) which of the following would not be considered a cost pool? a.inventory manager b.revenue c.engineering department d.direct materials cost 2) which of the following statements concerning value chain analysis is false? a.the goal of value chain analysis is to […]

Accounting 606 Test 2

1) which of the following is not one of the main issues regarding data collection which can significantly affect precision and reliability when using regression or any other cost estimation method? a.data accuracy b.time period choice c.nonlinearity d.relevant range 2) […]

Accounting 741

1) during the current year, outlytech corp. expected to sell 24,000 telephone switches. fixed costs for the year were expected to be $12,144,000, the unit sales price was budgeted at $3,200, and unit variable costs were budgeted at $1,440. outlytech’s […]

Accounting 792 Quiz

1) manders manufacturing corporation uses the following model to determine its product mix for metal (m) and scrap metal (s): the point where m = 2 and s = 3 would: a.minimize total cost b.minimize total variable cost c.lie in […]

Accounting 823 Test 1

1) cost management has moved from a traditional role of product costing and operational control to a broader strategic focus, which places an emphasis on: a.competitive pricing b.domestic marketing c.short-term thinking d.strategic thinking e.independent judgment 2) sheen co. manufacturers laser […]

Accounting 870 Midterm 1

1) tierney construction, inc. recently lost a portion of its financial records in an office theft. the following accounting information remained in the office files: direct labor cost incurred during the period amounted to 2.5 times the factory overhead. the […]

ACCT 112 Midterm 1

1) abnormal spoilage is considered what kind of cost? a.period cost b.product cost c.opportunity cost d.sunk cost 2) the balanced scorecard can be made more effective by developing it at a detail level so that employees: a.can see how it […]

Acct 148

1) the contribution margin per machine hour is calculated as: a.full cost per unit number of machine-hours per unit b.number of machine-hours per unit full-cost per unit c.selling price per unit less variable manufacturing cost per unit d.selling price per […]

Acct 548 Quiz 1

1) pearson electric company uses the high-low method to analyze mixed costs. the following information relates to the production data for the first six months of the year. what is the estimated total cost at an operating level of 1,180 […]

ACCT 574 Midterm 1

1) which of the following statements about budgeting is not true? a.budgeting is designed to be an aid to planning and control b.budgets create standards for performance evaluation c.budgets help coordinate the activities of the entire organization d.budgeting forces managers […]

Acct 578 Midterm 1

1) management accountants are frequently asked to analyze various decision situations including the following: i. the cost of a special device that is necessary if a special order is accepted. ii. the cost proposed annually for the plant service for […]

Acct 593

1) cost estimation includes all of the following steps except: a.defining the cost object for which the related costs are to be estimated b.determining the cost drivers c.graphing the data d.selecting and employing the appropriate estimation method e.calculating the multiple […]

Acct 619 Quiz 2

1) the journal entry to record the application of factory overhead to work in process would include a credit to: a.work-in-process b.cost of goods sold c.factory overhead d.materials inventory e.finished goods inventory 2) which of the following is not a […]

ACCT 672 Homework

1) which of the following items is not useful for addressing risk and uncertainty in cvp analysis? a.regression analysis b.sensitivity analysis c.what-if analysis d.monte carlo simulation (mcs) analysis e.decision trees and decision tables 2) sales forecasts are the first step […]

ACCT 691 Midterm 2

1) which of the following statements regarding cvp analysis is true? a.because of cost-structure issues, it cannot be used in a service setting b.it is a short-term profit-planning tool c.it is impossible to apply when there are multiple products sold […]

ACCT 719

1) national inc. manufactures two models of cmd that can be used as cell phones, mpx, and digital camcorders. national uses a volume-based costing system to apply factory overhead based on direct labor dollars. the unit prime costs of each […]

ACCT 777 Test

1) zapvideo inc. produces two basic types of video games, clash and slash. pertinent data follow: there is insufficient labor capacity in the plant to meet the combined demand for both clash and slash. both products are produced through the […]

Acct 821 Midterm 1

1) the coefficient of determination is a number between: a.0 and 1 b.-1 and 1 c.-2 and 2 d.the coefficient of determination can be any number 2) which of the following is not a way for a management accountant to […]

Acct 853 Midterm 2

1) the additional cost incurred as the cost driver increases by one unit is: a.average cost b.controllable cost c.variable cost d.unit cost 2) neary co. produces three products x, y, and z from a joint process. each product may be […]

Acct 860

1) blake company has $15,000 cash at the beginning of june and anticipates $50,000 in cash receipts and $34,500 in cash disbursements. the company requires a minimum cash balance of $20,000. any excess cash over the minimum desired balance is […]

Acct 871 Test

1) east bay fisheries inc. processes king salmon for various distributors. two departments are involved processing and packaging. data relating to tons of king salmon processed in the processing department during june 2013 are provided below: total equivalent units for […]

ACCT 894 Midterm 2

1) wings co. budgeted $555,600 manufacturing direct wages, 2,315 direct labor hours, and had the following manufacturing overhead: the total overhead of job #971 under the abc costing is: a.$95 b.$380 c.$1,520 d.$2,300 e.$9,200 2) randall company manufactures products to […]

ACT 203 Test 1

1) armer company is accumulating data to use in preparing its annual profit plan for the coming year. the cost behavior pattern of the maintenance costs must be determined. the accounting staff has suggested the use of linear regression to […]

ACT 248 Test 2

1) maple mount fishery is a canning company in astoria. the company uses a normal costing system in which factory overhead is applied on the basis of direct labor costs. budgeted factory overhead for the year was $680,400, and management […]

ACT 275

1) matrix inc. calculates cost for an equivalent unit of production using both the weighted-average and the fifo methods. total equivalent units for materials under the weighted-average method are calculated to be: a.126,000 equivalent units b.114,000 equivalent units c.90,000 equivalent […]

ACT 318

1) staley co. manufactures computer monitors. the following is a summary of its basic cost and revenue data: assume that staley co. is currently selling 600 computer monitors per month and monthly fixed costs are $80,000. staley co.’s margin of […]

ACT 319 Quiz 1

1) the following table was taken from firm x’s production cost report: what is the number of weighted-average equivalent units? a.40,000 b.50,000 c.48,000 d.38,000 2) the following costs were for bikeway inc., a bicycle manufacturer: at an output level of […]

ACT 346 Homework

1) the mathematical tool used to determine the optimum short-term product (or service) mix is: a.linear regression (i.e., ordinary least-squares) analysis b.linear programming c.linear ratio analysis d.pareto optimality analysis e.nonlinear cost-benefit analysis 2) based on analyzing the relationship of total […]

ACT 443 Quiz 3

1) orange computer co. is quickly becoming a major player in the personal computer market. the company currently has multiple companies producing products that go into an orange computer. this practice of having an outside firm provide a function for […]

ACT 559 Quiz 1

1) customer profitability analysis: a.always shows that the company with the highest total sales generates the highest net customer profit b.always shows that the company with the lowest total sales generates the lowest net customer profit c.produces the same results […]

ACT 561 Quiz

1) a manager uses regression to express sales as a function of advertising expenditures (x1), and per capita income (x2) in your sales area. the following multiple linear regression equation is developed: y = 10 + .51×1 + .45×2 the […]

ACT 664 Quiz 3

1) which of the following would likely be the most appropriate cost driver to allocate machine set-up costs to products? a.machine hours b.direct labor hours c.number of production runs d.number of products e.number of purchase orders 2) framing house, inc. […]

ACT 841 Test

1) assume the following information pertaining to moonbeam company: costs incurred during the period are as follows: cost of goods sold is calculated to be: a.$890,000 b.$896,000 c.$883,000 d.$877,000 e.$870,000 Answer: c cogm = $85,000 + $896,000 – $104,000 = […]

ACT 853 Midterm 1

1) nafta and wto refer to a.organizations with expertise in business process improvement b.laws and organizations which regulate international trade c.laws and regulations regarding sustainability d.organizations and trade groups that work for global economic development e.none of the above 2) […]

ACT 875 Quiz

1) if a firm has 1,200 completed and transferred out units, 200 equivalent units of beginning work in process and 500 ending work-in-process equivalent units, what is the total of equivalent units of production using the weighted-average method? a.1,500 units […]

MET MG 134 Quiz

1) neary co. produces three products x, y, and z from a joint process. each product may be sold at the split-off point or processed further. additional processing requires no special facilities, and production costs of further processing are entirely […]

MET MG 151 Quiz

1) which of the following should be considered a structural cost driver? a.scale b.experience c.complexity d.technology e.all of the above 2) moss point manufacturing recently completed and sold an order of 50 units that had the following costs: * applied […]

MET MG 226 Midterm 1

1) in the situation where a firm produces multiple products and the firm has a single resource constraint (e.g., machine hours), the most profitable use of available capacity (machine hours) requires that we assess: a.total demand for each product b.the […]

MET MG 338 Quiz

1) in performing activity analysis during the design of an activity-based costing system (abc), the management accountant studies: a.the cost drivers and managers in the plant b.the advice of operation-level managers c.the resources, activities and cost drivers in the operation […]

MET MG 409 Quiz 1

1) the following information pertains to mackenzie corp: if the sales price per unit were to decrease by 5% and variable expenses were to increase by $2.00 per unit, which of the following is true? a.the new selling price is […]

MET MG 417 Final

1) maple mount fishery is a canning company in astoria. the company uses a normal costing system in which factory overhead is applied on the basis of direct labor costs. budgeted factory overhead for the year was $680,400, and management […]

MET MG 508

1) in a make-or-buy decision: a.only variable costs are relevant b.fixed costs that can be avoided in the future are relevant c.fixed costs that will continue regardless of the decision are relevant d.only opportunity costs are relevant e.opportunity costs are […]

MET MG 576 Final

1) harrington corporation produces three products, a, b, and c. pertinent information on these products is as follows: the objective function for a linear program to maximize contribution margin from the three products is: a.max z = $3a + $3b […]

MET MG 608

1) effective execution of the cost leadership strategy requires all of the following except: a.incentives based on meeting strict quantitative goals b.frequent, detailed control reports c.tight cost control d.structured organization and policies e.strong coordination among functions: research, product development, manufacturing, […]

MET MG 894

1) which of the following is not an ethical issue managers encounter with cost allocation? a.products that are produced for both a competitive market and a public agency b.governmental agency provides a free service to the public c.governmental agency reimburses […]

SMG AC 106 Final

1) process costing is not intended to help determine a.departmental cost flows b.product costs c.profitability of products d.profitability of product mix 2) crown co. can produce two types of lamps, the enlightner and foglighter. the data on the two lamp […]

SMG AC 230 Quiz 3

1) successful activity-based costing (abc) implementation depends upon the firm: a.having support of consultants with needed expertise b.having a thorough activity analysis c.starting with a relatively simple system d.having well-trained managers e.having adequate computer resources 2) marin products produces three […]

SMG AC 370

1) a time ticket: a.shows the time an employee worked on each job, the pay rate, and the total cost chargeable to each job b.shows the time that a department’s employees worked on all jobs, the pay rate of each […]

SMG AC 492

1) the best way to allocate scare resources to attain a specific objective, such as the maximization of operating income, is: a.relevant costing b.responsibility accounting c.simple regression (ols) analysis d.operations management e.linear programming 2) neary co. produces three products x, […]

SMG AC 505

1) structural cost drivers are to executional cost drivers as: a.long-term is to short-term b.fixed is to variable c.total is to partial d.direct is to indirect 2) sutherland company listed the following data for 2013: if overhead is applied based […]

SMG AC 603 Quiz 3

1) national inc. manufactures two models of cmd that can be used as cell phones, mpx, and digital camcorders. national uses a volume-based costing system to apply factory overhead based on direct labor dollars. the unit prime costs of each […]

SMG AC 655 Homework

1) the mathematical technique that underlies the reciprocal cost allocation method is: a.regression analysis b.simultaneous equations c.analysis of variances d.complex algebraic functions e.multiple correlation 2) marin products produces three products dbb-1, dbb-2, and dbb-3 from a joint process. each product […]

SMG AC 858

1) the practice of maintaining budgets for the same number of future periods, revising those budgets as each period is completed and adding a new budget each period, is called: a.master budgeting b.cyclical budgeting c.zero-based budgeting (zbb) d.rolling budgets (or, […]