Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–16

15–30 Performance Reporting: the Use of Standard Cost Variance Information (30

minutes)

Among recommended improvements to the cost-variance report currently used by Zobel

Manufacturing Company to evaluate subunit performance are the following:

(1) The reports should emphasize that the terms “favorable” and “unfavorable” should

not automatically be interpreted, without further consideration, as “good

performance” and “bad performance”. These labels simply reflect the impact of the

calculated amount on the operating profit of the current period. Thus, a “favorable”

the performance indicators, providing excessive “slack” in determining standard

costs for manufacturing operations).

(3) Short-term financial performance (measured, for example, by the type of cost–

variance report used by the ABC Manufacturing Company), while important, is not

inclusive enough to achieve operational control. As such, the performance report

might be made more “balanced” by including one or more non-financial

performance indicators, such as quality indicators, on-time delivery, or

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–17

15–30 (Continued)

(5) Related to (4) above, the current profit-variance report does not admit to shared

responsibility. For example, excessive consumption of direct materials could be

traceable to poor quality materials purchased by the purchasing manager. As such,

at least a portion of some of the other manufacturing cost variances would be

attributable to the purchasing, not the manufacturing, function.

(6) Of significant concern is the need to incorporate flexible budgets into the cost–

variance report. Currently, there is no way to evaluate efficiency (consumption of

particularly since they are likely the responsibility of different individuals in the

organization.

(8) It is not clear from the sample report, but it may be the case that ABC Company

uses a single activity measure (e.g., machine hours) as the basis for applying

overhead costs to products (product-costing purpose) and for developing the

flexible-budget for control purposes. To the extent that the chosen measure (or

measures) does (do) not accurately predict changes in manufacturing support

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–18

15–31 Variable Factory Overhead Variances; Journal Entries (30 minutes)

1. Standard variable overhead rate per direct labor hour (DLH):

= Budgeted Total Variable Overhead ÷ Budgeted Total Direct Labor Hours

= $15,000 ÷ 2,500 hours = $6.00 per direct labor hour (DLH)

Standard direct-labor hours (DLH) per unit:

Variable Overhead Variance Analysis

FB Based on FB Based on

Actual Cost Inputs Output

(AQ × AP) (AQ × SP) (SQ x SP)

2,700 hrs. × $5.7777/hr. 2,700 × $6.00/hr. (4,800 × 0.5) × $6.00/hr.

= $15,600 = $16,200 = $14,400

Spending variance Efficiency variance

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–19

15–31 (Continued)

2. To Record Favorable Variable Overhead Spending Variance:

Dr. Factory Overhead (or, Variable Factory

Overhead) 600

3. The factory had a favorable variable overhead spending variance. This could be a

result of conscientious efforts of workers and the manager of the factory in

conserving uses of variable factory items. Alternatively, it could have been due, at

least in part, to the use of an inappropriate activity measure (direct labor hours) for

assigning variable factory overhead costs.

The $1,800 unfavorable variable overhead efficiency variance is a result of using

more direct labor hours (DLHs) to manufacture the output of the period (2,700 hours

the consumption of variable factory overhead cost.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–20

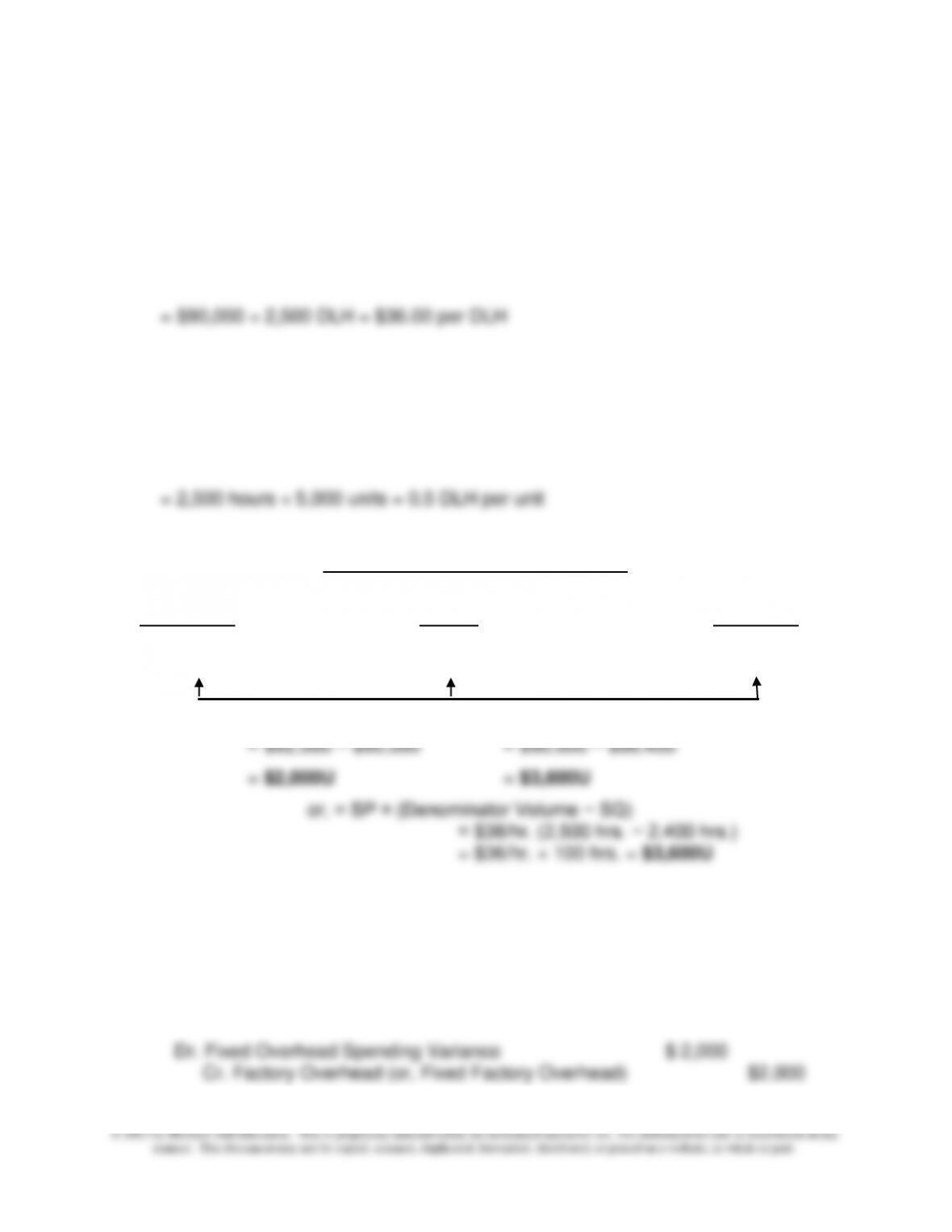

15–32 Fixed Overhead Variances; Journal Entries (30 minutes)

1. Standard fixed factory overhead application rate per direct labor hour (DLH):

= Budgeted Fixed Factory Overhead ÷ Total Direct Labor Hours, Practical

Capacity

Standard direct-labor hours (DLH) per unit:

= Budgeted Total Direct Labor Hours ÷ Practical Capacity Units

Fixed Overhead Variance Analysis

Applied

Actual Cost Budget (SQ × SP)

4,800 units× 0.5 hrs. ×$36/hr.

$92,000 $90,000 = $86,400

Spending variance Production volume variance

2. Fixed factory overhead (FOH) flexible-budget variance

= FOH spending variance = $2,000U

3. To Record Unfavorable Fixed Overhead Spending Variance:

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–21

15–32 (Continued)

To Record Unfavorable Production Volume Variance:

4. The $2,000 unfavorable fixed factory overhead spending variance could be a result

of unexpected fluctuations, overspending, or budgeting errors in one or more fixed

overhead items. However, since the amount is small (2.22% of the budget amount),

it is unlikely that the management needs to spend any time or resources to

investigate this variance.

the text, this variance generally has shared responsibility (with marketing,

purchasing, etc.).

Note that when the denominator activity level is set at practical capacity, then

resulting production volume variances can be interpreted as the cost of unused

capacity. The disclosure of this information over time can help managers make

better decisions regarding capacity-related spending.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–22

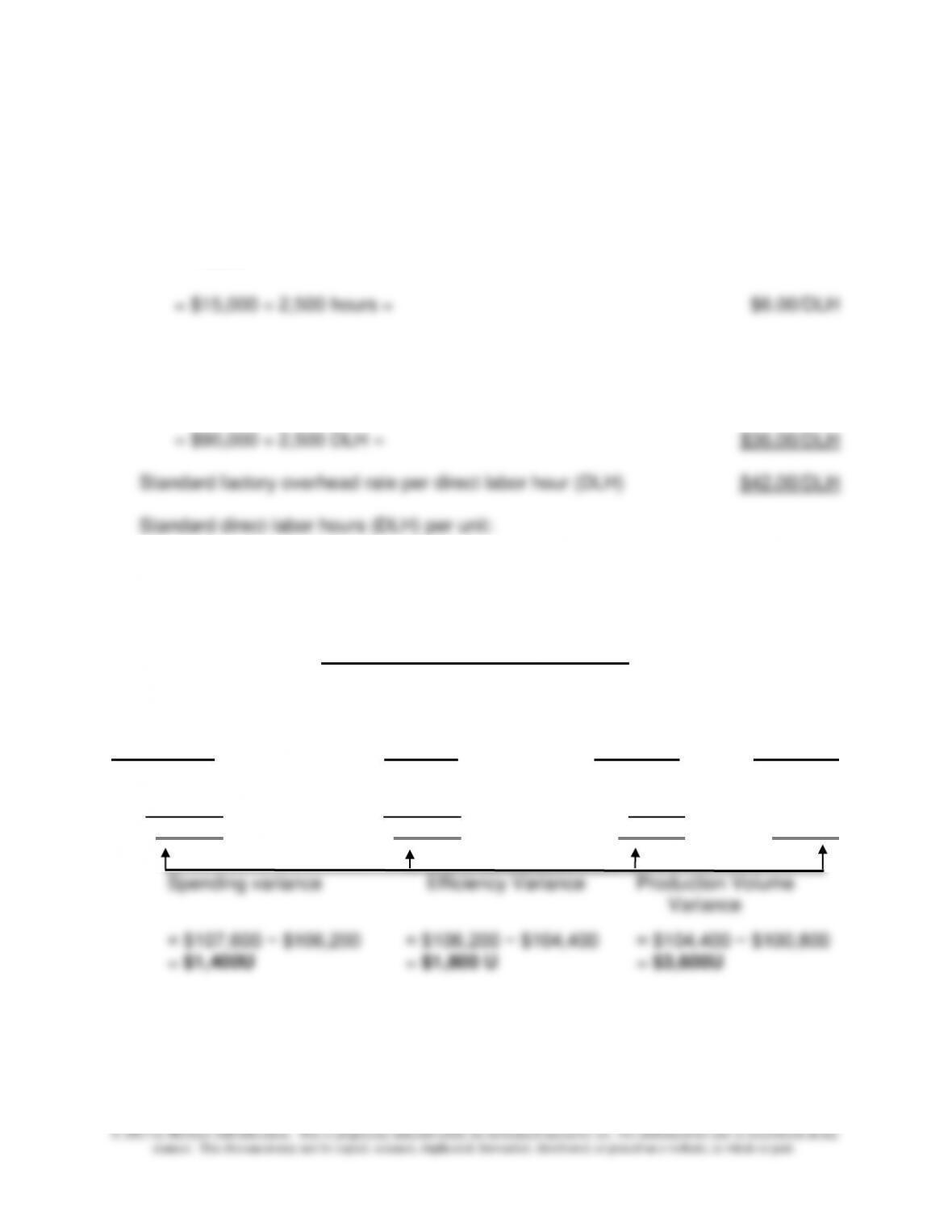

15–33 Three-Variance Factory Overhead Analysis (30-40 minutes)

1. Standard variable factory overhead rate per direct labor hour (DLH):

= Budgeted Total Variable Factory Overhead ÷ Budgeted Total Direct Labor

Hours

Standard fixed factory overhead rate per DLH:

= Budgeted Total Fixed Factory Overhead ÷ Practical Capacity Labor Hours

= Practical Capacity Labor Hours ÷ Practical Capacity, in Units = 0.5 DLH/unit

Three-Variance Overhead Analysis

Flexible Budget Flexible Budget

Based on Inputs Based on Output Applied

Actual Cost AQ × SP (SQ × SP) (SQ × SP)

$ 15,600 2,700 × $6 = $ 16,200 2,400 × $6 = $14,400

+ 92,000 + 90,000 + 90,000 2,400 × $42

$107,600 $106,200 $104,400 = $100,800

15–23

15–33 (Continued)

2.Total overhead spending variance = variable overhead spending variance + fixed

overhead spending variance

= $600F + $2,000U = $1,400U

Total overhead efficiency variance = variable overhead efficiency variance

In sum, the only difference between the three-way and four-way analysis is that in

the former, the spending variances for fixed and for variable overhead (reported in

the latter) are combined into a single overhead spending variance.

Three- and Four-Variance Factory Overhead Analysis: Summary

Overhead Spending Variance:

Variable Overhead Spending Variance $ 600F

Fixed Overhead Spending Variance 2,000U $1,400U

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–24

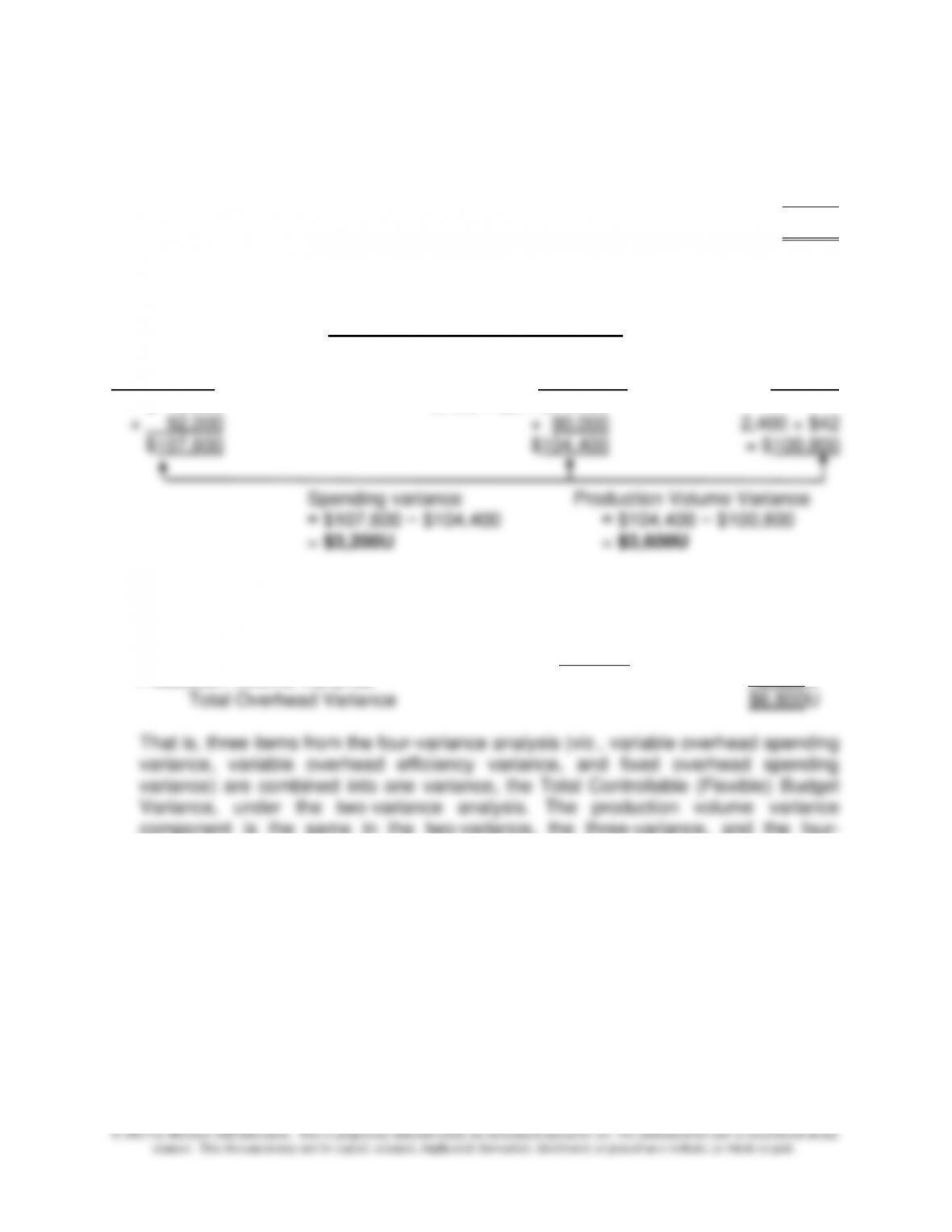

15-34 Two-Variance Analysis of the Total Overhead Variance (30 minutes)

1. Standard variable factory overhead rate per direct labor hour (DLH) $ 6.00

Standard fixed factory overhead rate per DLH 36.00

Standard factory overhead rate per DLH $42.00

Standard DLHs per unit = 0.5 DLH

Two-Variance Overhead Analysis

Flexible Budget Based Overhead

Actual Cost on Output Applied

$ 15,600 2,400 × $6 = $14,400

2. Total Controllable (Flexible) Budget Variance for Overhead:

a) Variable Overhead Spending Variance $ 600F

b) Variable Overhead Efficiency Variance $1,800U

c) Fixed Overhead Spending Variance $2,000U $3,200U

Production Volume Variance 3,600U

component is the same in the two-variance, the three-variance, and the four–

variance breakdown of the total overhead variance.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–25

15–34 (Continued)

3. The two-variance breakdown of the total overhead variance reports two important

factors concerning overhead costs. The flexible-budget (controllable) variance

measures the difference between the actual overhead incurred and the overhead

that should have been incurred based on the actual output of the period. (This latter

The production volume variance, when the fixed overhead application rate is based

on practical capacity, reports the effectiveness of the organization in using available

capacity. Over time, this variance can signal to managers the existence of excess

capacity or the need for capacity expansion. In short, this variance helps managers

control capacity-related resource spending.

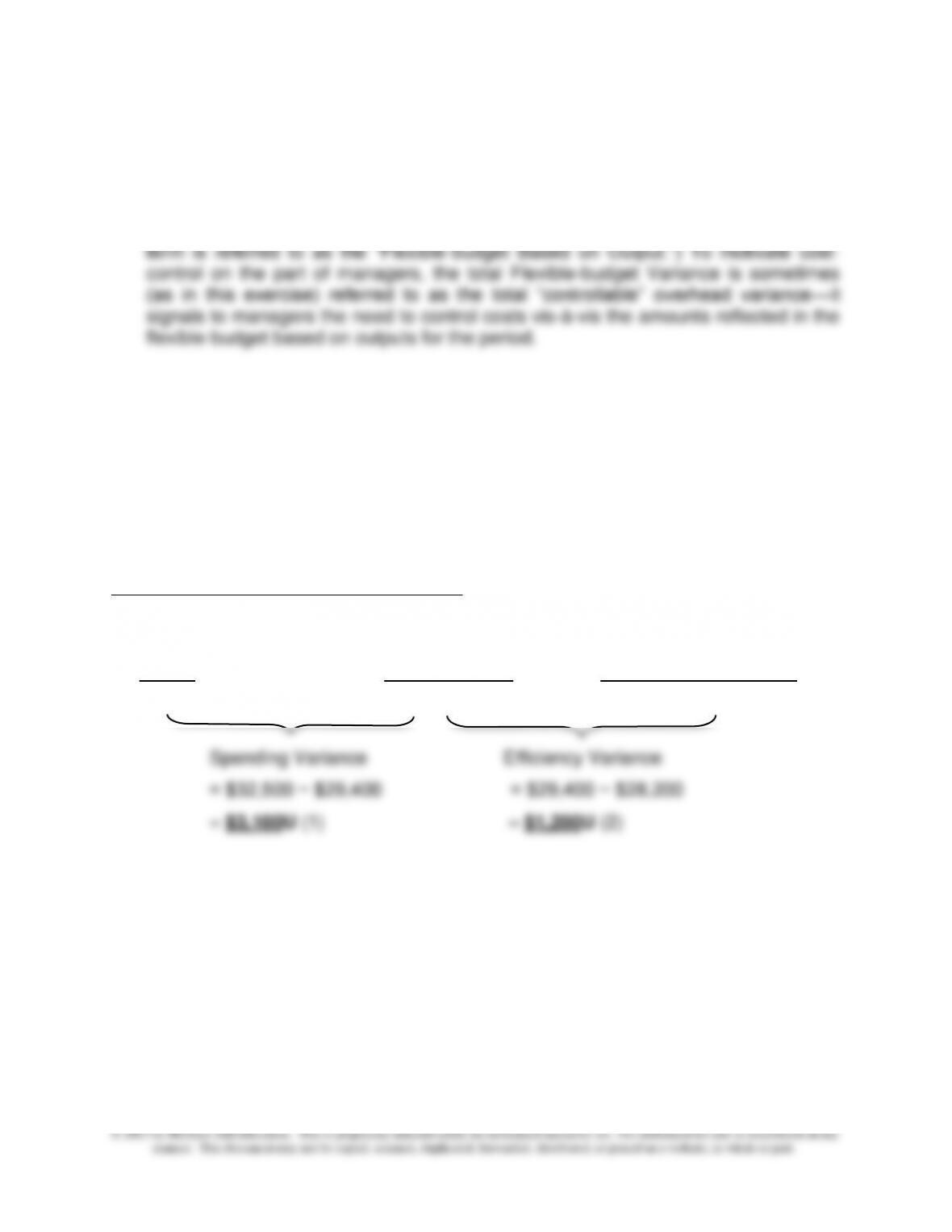

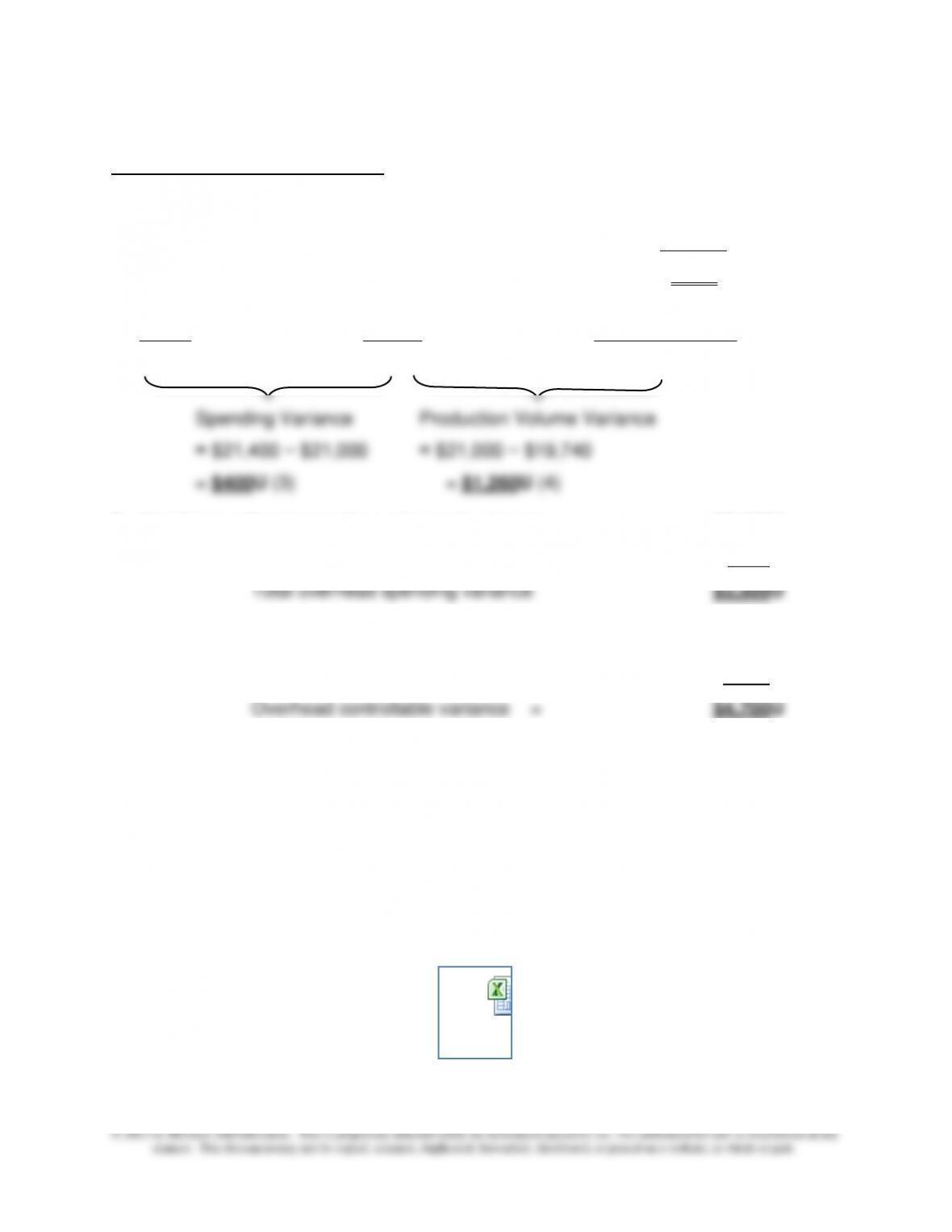

15–35 Factory Overhead Variances; Spreadsheet Application (40-45 minutes)

Standard MH per unit: 10,000 MH 5,000 units = 2 MH per unit

1 & 2: Variable factory overhead variances

Flexible Budget Based Flexible Budget Based

on Inputs (i.e., actual on Output (i.e., standard

Actual machine hours) allowed machine hours)

$32,500 9,800 × $3 = $29,400 (4,700 × 2) × $3 = $28,200

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–26

15–35 (Continued-1)

3 & 4: Fixed overhead variances:

Budgeted fixed overhead (given) $21,000

Denominator volume (machine hours) 10,000

Standard fixed overhead rate per machine hour $2.10

Actual Budget Standard Applied

$21,400 $21,000 (4,700 × 2) × $2.10 = $19,740

5. Variable overhead spending variance (1, above) = $3,100U

Fixed overhead spending variance (3, above) = 400U

6. Total overhead spending variance (5, above) = $3,500U

Variable overhead efficiency variance (2, above) = 1,200U

Note: An Excel spreadsheet solution file for this assignment is embedded below. You

can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then

return you to this Word document.

Ex. 15-3

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–27

15–36 Overhead at Two Activity Levels, and 4-Way versus 2-Way Analysis of the

Total Overhead Variance (60 minutes)

1. Budgeted fixed overhead:

Total standard overhead at 85% level of theoretical capacity

= 21,250 machine hours (MH) × $14.00/MH = $297,500

2. Standard overhead application rates, 2013:

Variable factory overhead rate per machine hour (MH), 2013 = budgeted variable

overhead, 2012 standard direct machine hours allowed for output achieved, 2012

=

$61,250 21,250 MH = $2.8824/MH (rounded to four decimal places)

3. Factory overhead flexible budget for 2013:

Flexible budget for variable factory overhead, based on output in 2013

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–28

15-36 (Continued-1)

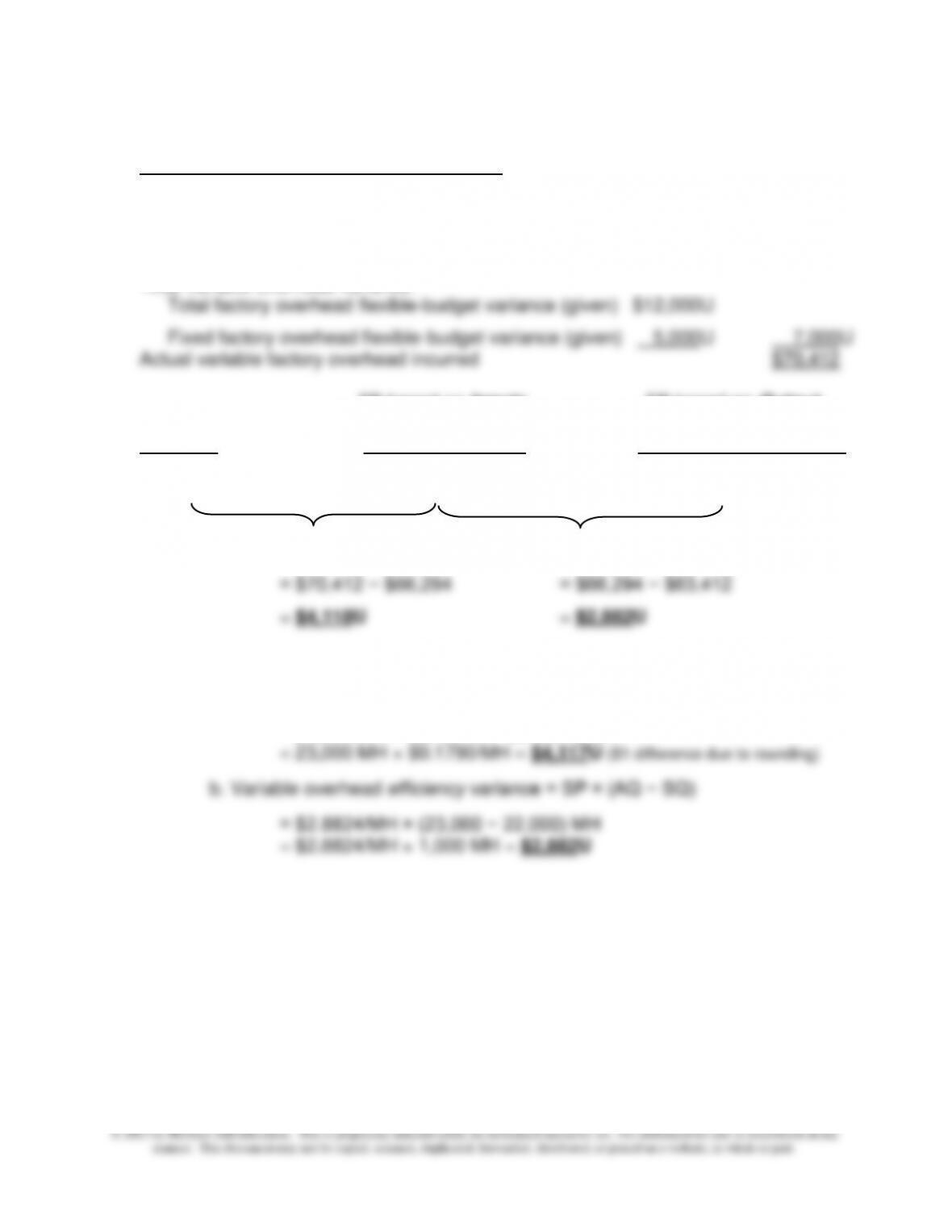

4. Variable Factory Overhead Variances, 2013:

Actual variable factory overhead incurred = Total standard variable factory overhead

for the units manufactured +/– Total variable overhead variance:

Total standard variable factory overhead (see 3 above) = $63,412

Total variable overhead variance:

FB based on Inputs FB based on Output

Actual Cost (i.e., standard VOH cost (i.e., standard VOH cost

Incurred for the MH Worked) for standard MH allowed)

23,000MH × $2.8824/MH 22,000MH × $2.8824/MH

$70,412 = $66,294 = $63,412

a. Spending Variance b. Efficiency Variance

Alternative calculations:

a. Variable overhead spending variance = AQ × (AP − SP)

= 23,000 MH × ($3.06134− $2.8824)/MH

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–29

15-36 (Continued-2)

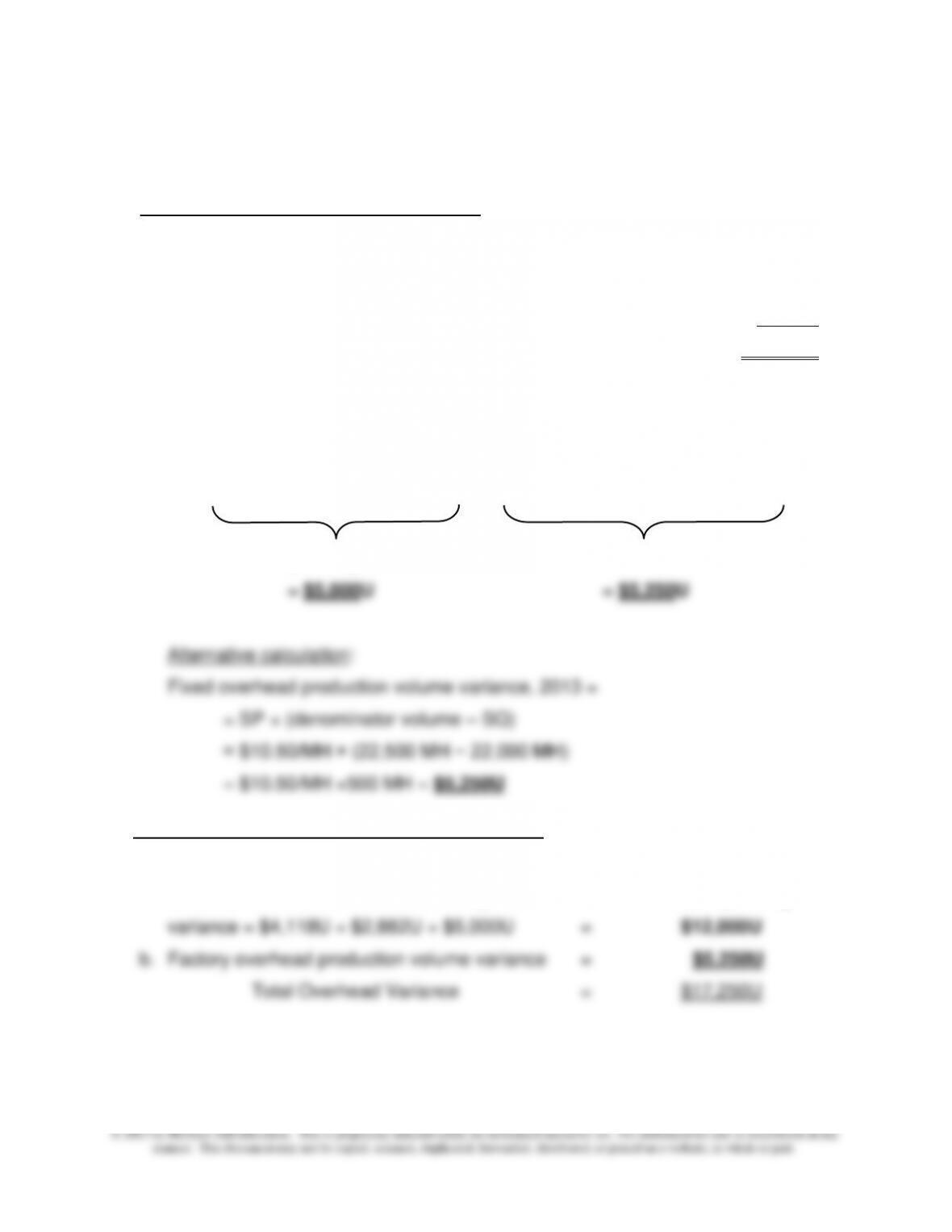

Fixed Factory Overhead Variances, 2013:

Actual fixed factory overhead incurred = budgeted fixed overhead +/– fixed

overhead spending (budget) variance

Budgeted fixed overhead = $236,250

Fixed factory overhead budget variance (given) 5,000 U

Actual fixed factory overhead incurred $241,250

Fixed Overhead Variances:

Actual Budget Applied

$241,250 $236,250 $231,000

Spending Variance Production Volume Variance

5. Two-Way Breakdown of Total Overhead Variance:

a. Factory overhead flexible-budget variance = Variable overhead spending

variance + variable overhead efficiency variance + fixed overhead spending

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–30

15-36 (Continued-3)

Alternatively, we can calculate the total controllable (flexible-budget) variance and

the production volume variance directly, as follows:

a. Total overhead variance = actual overhead − standard overhead applied to

production (based on allowed machine hours for the 11,000 units

produced)

b. Total flexible (control) budget variance = actual overhead – flexible budget (FB)

for total overhead based on output (i.e., based on allowed MH for the 11,000

units produced)

Notes:

1See part 4 above

2See part 2 above ($2.8824/MH variable overhead rate + $10.50/MH fixed

overhead rate)