Chapter 8 – Cost Estimation

8-31

8-42 (continued – 3)

3.

The Gilmore company is likely to have a number of sustainability

issues in its business. As a company that renovates older homes, it

must frequently deal with hazardous materials such as asbestos used

in siding and other construction materials decades ago. Current

construction codes require renovations of older homes to treat the

hazardous materials with special, sometimes expensive procedures.

The removal and proper disposal of the materials must be carefully

and effectively done in compliance with local, state, and federal

The role of cost estimation is important when a construction company

such as the Gilmore company must accurately budget costs for

renovations in making bids and in dealing with the occasional

unexpected problems. Careful cost estimates can help Gilmore to

more effectively prepare bids and proposals for new work, and to

increase profitability along the way.

8-32

8-43 Cost Estimation; Machine Replacement; Ethics (25 min)

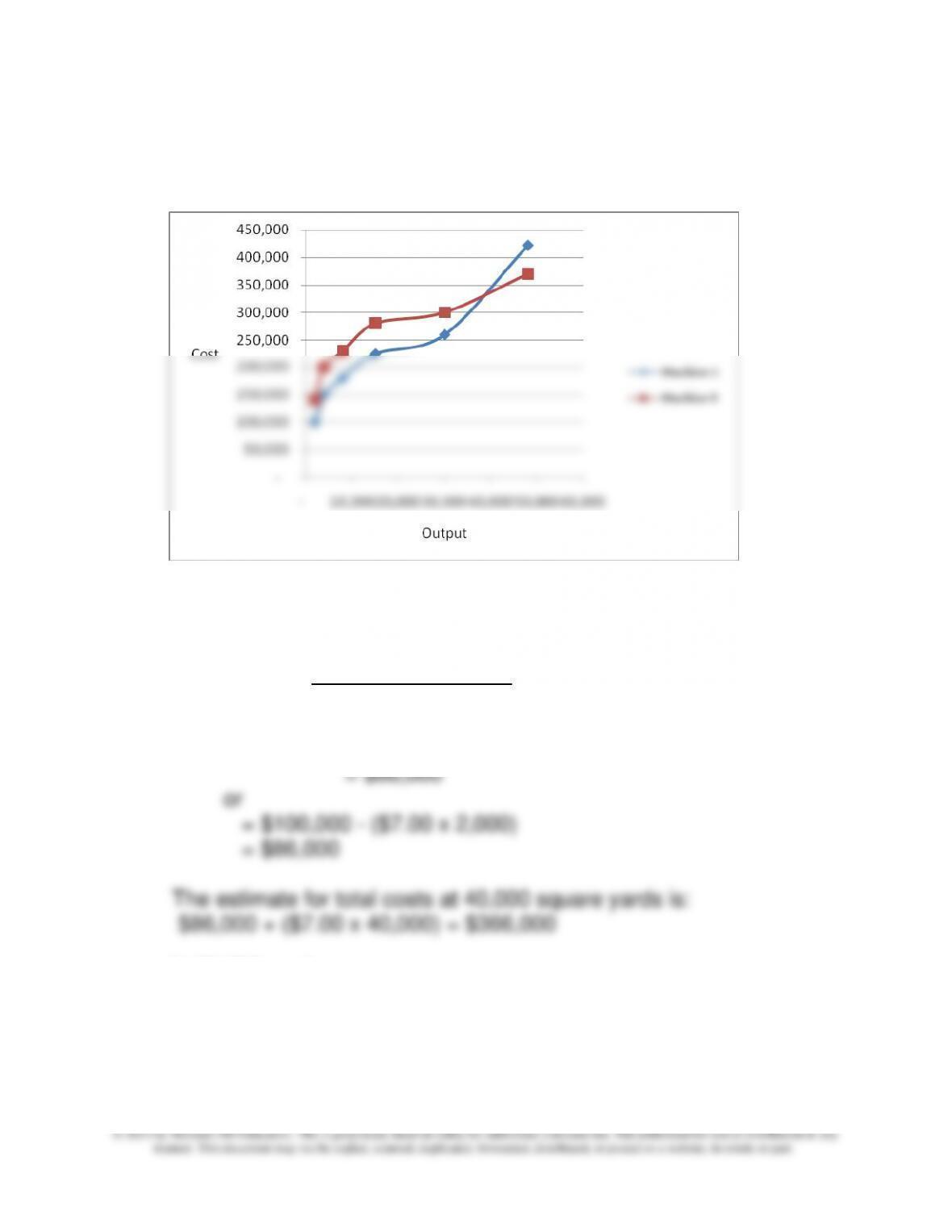

1. A graph of the data shows no significant outliers nor nonlinear

relationships. See below

Using the High-Low method:

Machine A:

slope = $422,000 – $100,000 = $7.00

48,000 – 2,000

constant = $422,000 – ($7.00 x 48,000)

At 25,000 yards:

$86,000 + ($7.00 x 25,000) = $261,000

8-33

8-43 (continued -1)

Machine B:

slope = $370,000 – $140,000 = $5.00

48,000 – 2,000

constant = $370,000 – ($5.00 x 48,000) = $130,000

The calculations show that the costs are lower at both the 40,000

and the 25,000 level for Machine B, which suggest that Machine B is

preferred to Machine A for production levels above at least 25,000.

The answer is wrong. Note by inspection of the chart in the text and

inspection of the graph above, that Machine A is preferred to Machine

B up to approximately 40,000 units. The error in the analysis is the

error in using the High-Low method for cost estimation in this

8-34

8-43 (continued -2)

2. The ethical issue presented in this case should be addressed using

the approach described in chapter 1. Here it seems important to

consider the nature and extent of the effect of the defect on

customers and also GlasTech. Since the glass is used in office

the calculations should not be modified.

3. In addition to the costs of the machine, GlasTech should be aware

of any import duties or restrictions for the purchase of the machines

from Germany or Canada. How will these restrictions and duties, if

country might open up new markets for GlasTech.

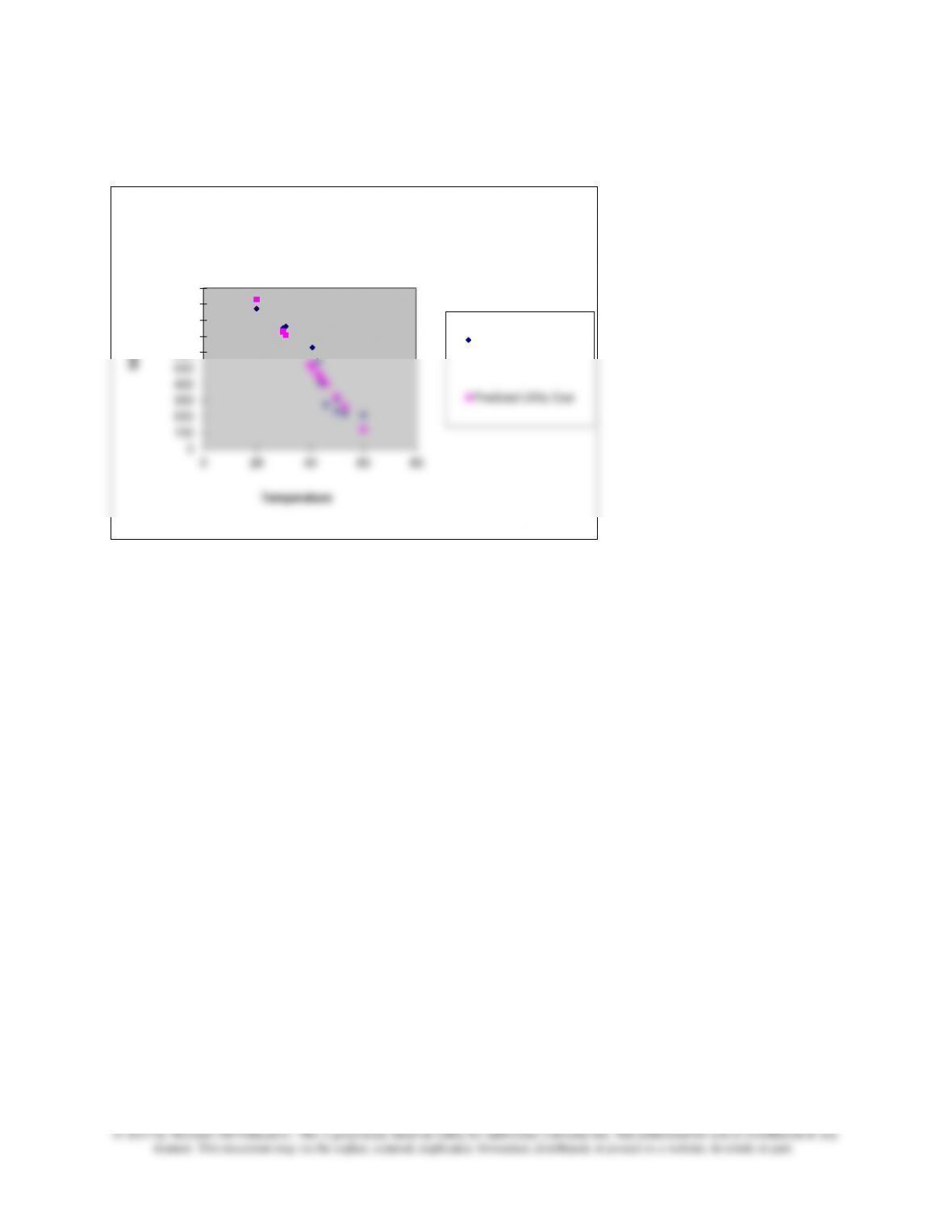

8-44 Cost Estimation; High-Low Method (25 min)

Estimated cost of electricity equals $210 (from information about

August)

At 20 degrees F:

$870 = intercept + (-$16.50 x 20)

intercept = $1,200

A cost estimate for January is not available since the average

temperature of 10 degrees is outside the relevant range of the data

used to develop the high-low estimate. The cost estimate for

February is: $1,200 – $16.50 x 40 = $540

Note to instructor: the problem can also be solved using regression

analysis, as shown below. Note that the predicted cost, $525, differs

from the High-Low method, but not significantly.

Regression Statistics

Multiple R 0.94586791

R Square 0.8946661

Adjusted R Square 0.88413271

Standard Error 80.2291185

Observations 12

ANOVA

df SS MS F

Regression 1 546709.8021 546709.8 84.9362

Residual 10 64367.1146 6436.711

Total 11 611076.9167

Coefficients Standard Error t Stat P-value

Intercept 1330.88094 95.4055084 13.94973 7.01E-08

Temperature -20.1487624 2.186260788 -9.21608 3.34E-06

Cost equation: Utility cost = $1,331 – $20.1488 * Temperature

Estimated cost for February with the predicted temperature at 40 degree:

$1,331 – $20.1488 * 40 = $525

8-36

8-44 (continued –1)

The cost/temperature relationship is shown in the Excel chart below:

0

100

200

300

400

500

600

700

800

900

1000

020 40 60 80

Utility Cost

Temperature

Temperature Line Fit Plot

Utility Cost

Predicted Utility Cost

Chapter 8 – Cost Estimation

8-37

8-45 Regression Analysis; Evaluating Regression Equations (20 min)

1. The Pilot Shop should adopt regression 2 to forecast total shipping

department costs for the following reasons:

a. R-squared, the coefficient of determination (the proportion of the

variance explained by the independent variable), is higher for

regression 2 is OK (3.46).

2. Since the number of orders to be shipped next week is given, the

appropriate estimation model is regression 2, and the total estimated

shipping cost is $2,994.90.

3. An important limitation of the regression we have chosen is that we

have not been able to assess the potential for nonlinearity in the

relationships among the variables. The presence of nonlinear

relationships can be assessed by examining the Durbin-Watson

statistic and/or by examining the graphs of the data. One of

be corrected for obtaining the regression results.

An additional limitation is that we are unable to assess the potential

for nonconstant error variance since we do not have a graph of the

data. Maynard should prepare a graph of the data and assess the

potential for nonlinearity.

8-38

8-45 (continued –1)

The global nature of the Pilot Shop’s operations adds another

limitation to the analysis. The purchasing and shipping costs will vary

with international business conditions and also with fluctuations in

Chapter 8 – Cost Estimation

8-46 Regression Analysis (20 min)

1.

The total projected attendance is 20,422, as determined below.

Independent Variables Results Example Totals

Regression intercept 1,224 1,224

Attendance at prior concert

Coefficient 3445 1 3,445

t-value 4.11

Spending on advertising

Coefficient 0.113 35,000 3,955

t-value 1.88

Performer’s CD sales

Coefficient 0.00044 10,000,000 4,400

t-value 1.22

Television appearances

Coefficient 898 0

t-value 2.4

Other Public performances

Coefficient 1,233 6 7,398

t-value 3.7

R-squared 0.88

Standard error of the estimate 2,447

Total Projected Attendance 20,422

2. The overall reliability of the regression, as measured by R-squared is

very good, at 88% and the standard error of the estimate, at 2,447 is

reasonably small, considering the level of predicted attendance, 20,422.

On the other hand, two of the five independent variables have

(near a holiday weekend, early or late in the season, the prior appearance

was on a rainy day, etc), and other variables related to the performer’s

popularity, such recent appearances in the print media, release of a new

8-40

8-47 Correlation Analysis (20 min)

1.

The correlation analysis shows that only one of the correlations is

significant at the .05 level – order size and runtime, and the relationship is

negative, or inverse. That is, the larger the order size, the smaller the

runtime per unit. Based on an actual company, this result is due to the fact

that the machine operators slowed the machine time at the start of each

order to ensure that the order was running properly before getting the

machine up to the normal runtime speed. The effect of this practice is that

Another informative aspect of the correlation analysis is to show the

positive (.459) and marginally significant (p< 0.10) relationship between

complexity and setup time per unit. This means that greater complexity

tends to increase setup time, an intuitive result.

2. The information above is particularly useful to PolyChem as it begin to

focus on smaller customers in order to find profitable alternatives to the

low-cost competition it now faces. The key point is that selling in smaller

Chapter 8 – Cost Estimation

8-41

8-48 Regression Analysis (20min)

1. Assuming that all purchases of autos for resale (cost of goods

sold) represent variable costs

Price = $30,000,000/1,500 = $20,000

Variable cost per unit =

= [$862,500 + (.9 x $2,300,000) + $24,750,000] / 1,500

= $ 18,455

2.

a. The relevant range is the band or range of activity within which

specified cost relationships (behavioral assumptions) remain valid

and fixed costs remain fixed.

b. The R-squared value is a measure of the goodness of fit between

the independent and dependent variable, the extent to which the

independent variable accounts for the variability in the dependent

include factors that are peculiar to the start-up of a dealership.

d. The standard error of the estimate is the measure of precision of

the regression. The standard error of the estimate helps to determine

8-42

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

the range of the accuracy of the estimate with a given degree of

confidence.

8-48 (continued -1)

3. Using the regression equation that Jack Snyder developed, the

approximate range of sales that could occur during the year is

calculated below.

Range of sales = Sales +/- (Standard error x 2)

= $28,500,000 +/- ($4,500,000 x 2)

relatively poor regression. The mediocre R-Squared of 60% is a

further indication of the weakness of the model, and therefore of the

lack of precision of the predictions from the model.

4. A key issue for USMI is the risk of expanding its dealership

network. Regression analysis allows financial managers to make

predictions about the effect of the proposed expansion on sales and

profits. While Jack Snyder’s model is not particularly reliable or

Chapter 8 – Cost Estimation

8-43

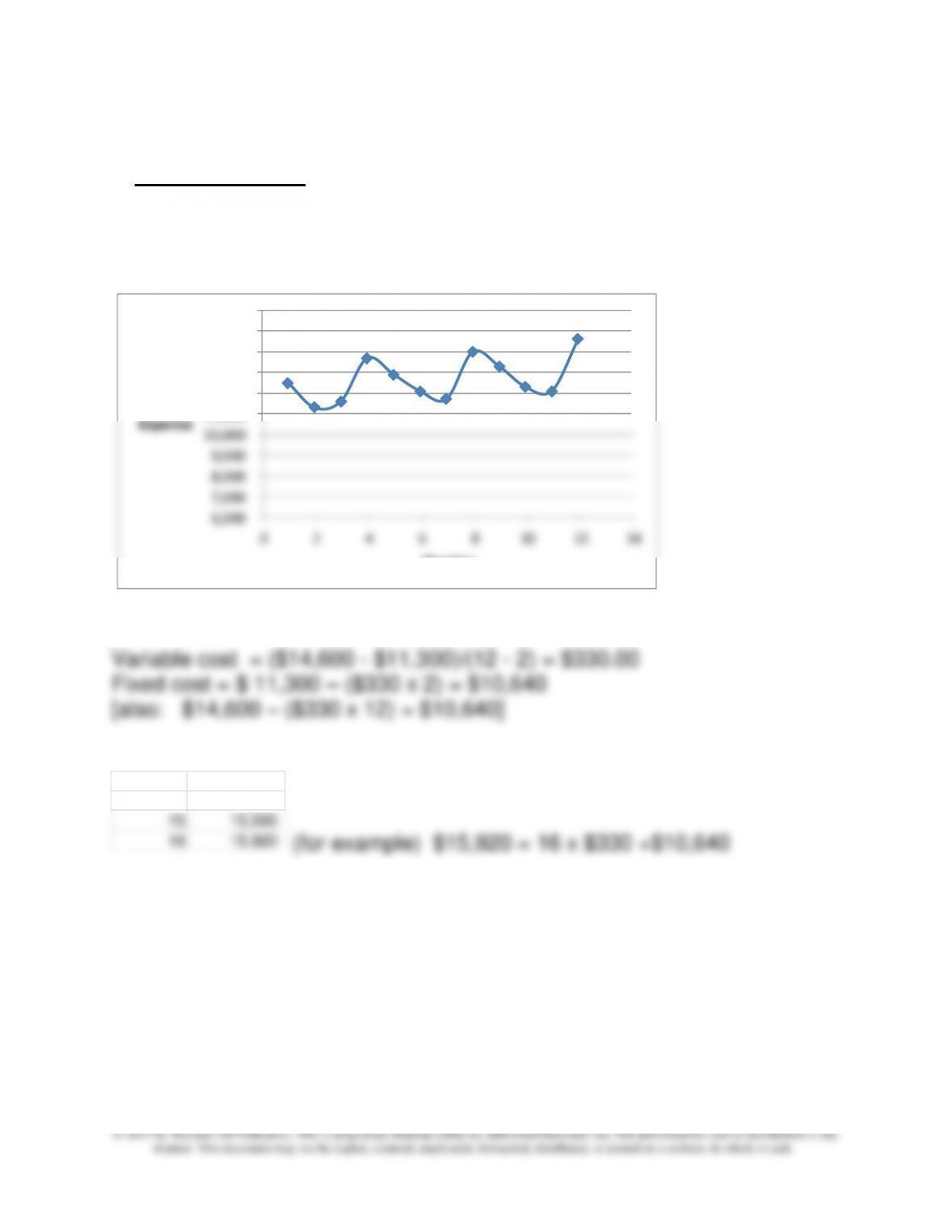

8-49 Cost Estimation; High-Low Method, Regression Analysis (30min)

1. High-Low Method

An examination of the exhibit below indicates that representative high

and low points are the last and second data points, respectively, so

these points are used to develop the high-low estimate.

Quarterly Predictions are:

Because these predictions do not take into account all the seasonal

variation in the data, it is useful to consider the results for a regression

analysis, as shown below.

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

0 2 4 6 8 10 12 14

Return

Expense

Quarter

13 14,930$

14 15,260

15 15,590

16 15,920

8-44

8-49 (continued –1)

Regression

The regression equation from the spreadsheet (see below) is:

Regression One

Regression Statistics

Multiple R 0.439734422

R Square 0.193366362

Adjusted R Square 0.112702998

Standard Error 974.8928577

Observations 12

ANOVA

df SS MS F Significance F

Regression 1 2278339.161 2278339 2.397202 0.152593037

Residual 10 9504160.839 950416.1

Total 11 11782500

Coefficients

Standard Error

t Stat P-value Lower 95%

Intercept 11854.54545 600.005077 19.75741 2.42E-09 10517.65083

Quarter 126.2237762 81.52463628 1.54829 0.152593 -55.4244333

Return Expense = $11,855 + [$126.2238 x (quarter number)]

Predicted Expense for the next four quarters using regression analysis:

Quarter Regression Prediction

13 $11,855 + (13 x $126.2238) = $ 13,495.98

14 $11,855 + (14 x $126.2238) = $ 13,622.13

Chapter 8 – Cost Estimation

8-49 (continued –2)

At this point because of the relatively low R-squared, and the relatively low

t-value for the independent variable (note that the F value is not significant),

we consider a revision of the regression model. Since there is noticeable

seasonality in the data (higher for periods 1,4,8 and 12, the last quarters of

squared, improved SE, and a significant t-value for the dummy variable.

Regression Two

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.873681599

R Square 0.763319537

Adjusted R Square 0.710723879

Standard Error 556.6454641

Observations 12

ANOVA

df SS MS F Significance F

Regression 2 8993812.445 4496906 14.51298 0.00152662

Residual 9 2788687.555 309854.2

Total 11 11782500

Coefficients

Standard Error

t Stat P-value Lower 95%

Intercept 11252.65118 366.1756041 30.7302 2E-10 10424.30442

Quarter 137.3356705 46.61018705 2.946473 0.016314 31.89610196

Season 1589.000876 341.3221703 4.655428 0.001193 816.8764841

This regression has the equation: Expense = $11,252.65118 + ($1,589.00876 x dummy

The regression predictions for the revised regression are as follows:

Quarterly Predictions

13 14,627$

14 13,175$

15 13,313$

16 15,039$

Because the second regression has better statistical measures, the

management accountant should rely on these predictions.