Chapter 11 – Decision Making with a Strategic Emphasis

11–76

Product Rankings =

(2) (3) (1)

11-44 (Continued-1)

fact that the labor rate is $20.00 per hour (given).

4. If machine hours represent the scarce resource, then the allocation of

machine hours to products should be based on the contribution margin

per machine hour. As seen from the calculations below, the product

profitability rankings differ from those determined in Part 3 above.

(Note that in the present case we do not know the actual machine

hours per unit, but we do know the relative machine hours per unit

5. If there are only two products (and one or more constraints), we could

solve the product-mix problem using the graphical approach presented

No Frills Standard Super

Model Model Model

CM per unit $13.00 $23.00 $27.00

÷ DLHs/unit of output* 0.50 1.00 1.50

CM per DLH $26.00 $23.00 $18.00

Chapter 11 – Decision Making with a Strategic Emphasis

11–77

with the feasible region and to choose the product mix (corner point)

that maximizes short-term profit. Another alternative is to us a set of

iso-profit lines (combination of the two products that results in a given

level of profit). Extend the iso-profit line up to the right until it just

11-44 (Continued-2)

touches a point in the feasible set (region): this point (mix of the two

products) defines the optimum product mix.

6. In the case where there are more than two products (and one or more

constraints), the graphical approach is not practical. In this case, the

7. The primary role of the management accountant in terms of short-term

profit planning is to generate accurate estimates of the contribution

margins for each product (or service). Whether a simple or a complex

decision context, the general solution to the product-mix problem is to

11–78

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

11–45 Profitability Analysis; Linear programming (50-60 min)

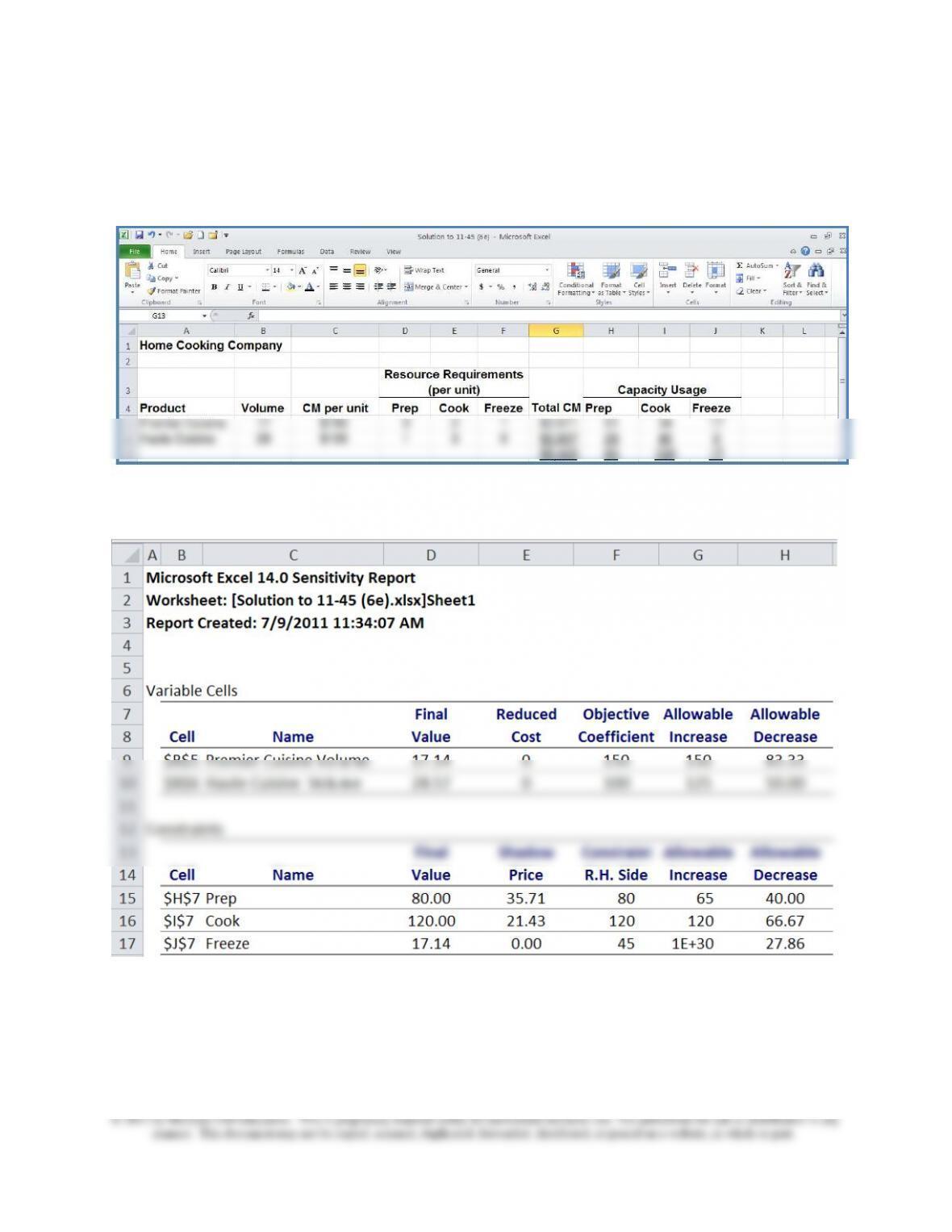

1. Solve for all three constraints: the solution is 17 units of Premier

Cuisine and 29 units of Haute Cuisine, as shown in Exhibit 11-45C,

cells B5 and B6. Total contribution margin for this mix is $5,429. The

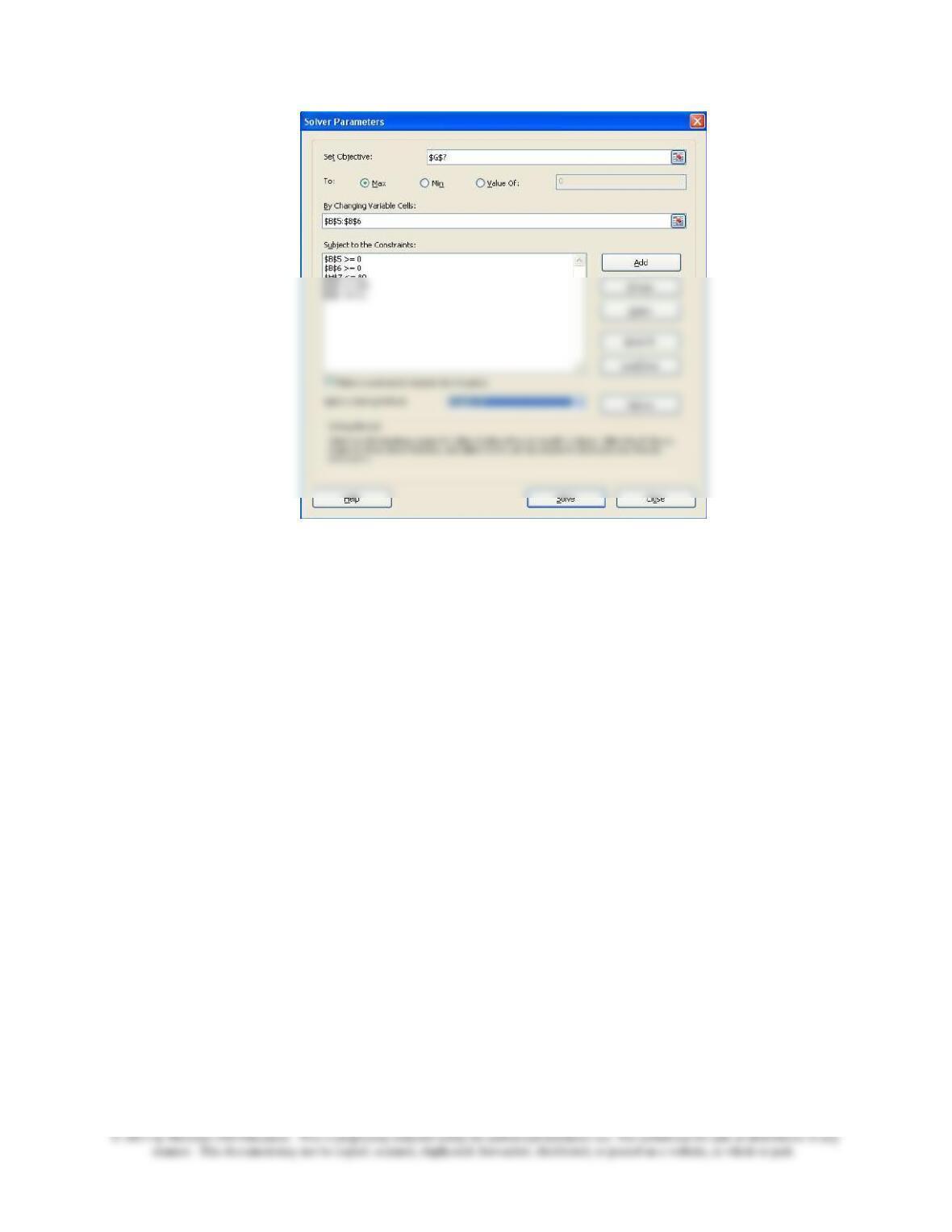

Solver set up for this solution is shown in Exhibit 11–45A. The

Exhibit 11-45A: Solver Set Up

Exhibit 11-45B: Completed Dialog Box (“Solver Parameters”)

Chapter 11 – Decision Making with a Strategic Emphasis

11–79

Chapter 11 – Decision Making with a Strategic Emphasis

11–80

11-45 (Continued-1)

Exhibit 11-45C: Solver Solution (Optimum Product Mix)

2. Sensitivity Report

Notes—Sensitivity Report:

Chapter 11 – Decision Making with a Strategic Emphasis

11–81

1. Reduced costs: these pertain to the two decision variables (Premier

and Haute). If all such variables are in the optimum solution (as in the

present case), then these values will all be zero. Technically, the

11-45 (Continued-2)

“reduced cost” for a variable not in the optimum solution represents

the amount by which the per-unit contribution margin would have to

change in order for the variable to enter the optimal solution.

2. For each decision variable, the “Allowable Increase” and “Allowable

Decrease” provide a range over the objective function coefficients

(here, per-unit contribution margins) over which the optimum solution

willing to pay for one additional unit (here, hour) of each constraint.

You will note that under the optimum solution the entire amount of

Freeze hours is not used up. Thus, by definition the “shadow price”

for this constraint must be zero.

4. Finally, for each constraint there is an “Allowable Increase” and an

“Allowable Decrease.” This information shows the range, around the

value of each constraint, over which the indicated “shadow prices”

hold.

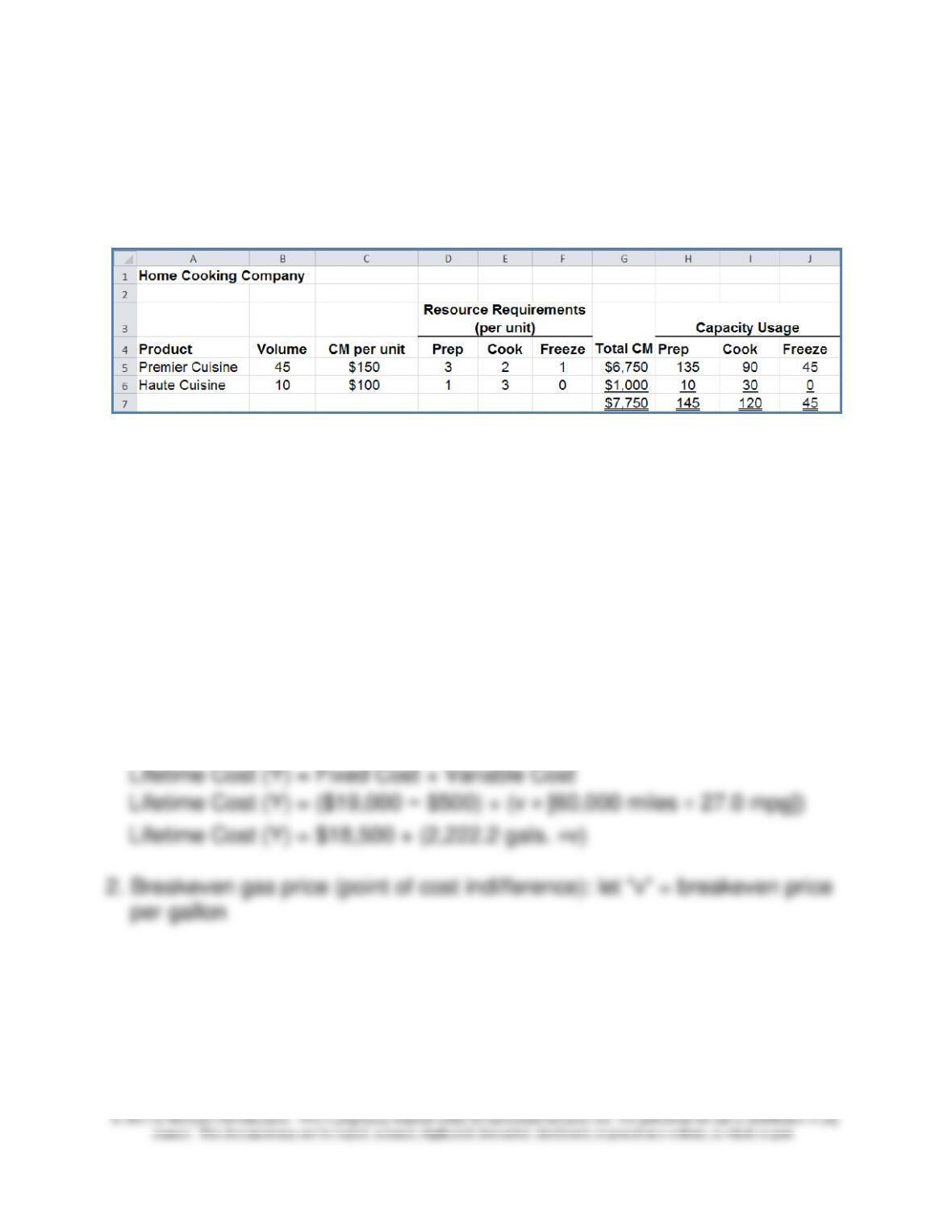

3. Optimal Solution after removing preparation time constraint: the optimal

Chapter 11 – Decision Making with a Strategic Emphasis

11–82

11-45 (Continued-3)

Exhibit 11-45D

11–46 (Also Problem 9-50): CVP Analysis; Sustainability; Uncertainty;

Decision Tables (60-75 min)

1. Lifetime cost functions: let Y = lifetime cost, and v = cost per gallon of

gas

Regular model:

Lifetime Cost (Y) = Fixed Cost + Variable Cost

Lifetime Cost (Y) = $17,000 + (v × [60,000 miles ÷ 23.0 mpg])

Lifetime Cost (Y) = $17,000 + (2,608.7 gals. × v)

Hybrid model:

Lifetime Cost (Y) = Fixed Cost + Variable Cost

Lifetime Cost (Y) = ($19,000 − $500) + (v × [60,000 miles ÷ 27.0 mpg])

Lifetime Cost (Y) = $18,500 + (2,222.2 gals. ×v)

2. Breakeven gas price (point of cost indifference): let “v” = breakeven price

per gallon

Chapter 11 – Decision Making with a Strategic Emphasis

11–83

Lifetime Cost—Gas Model = Lifetime Cost—Hybrid Model

$17,000 + (2,608.7 gals. × v) = $18,500 + (2,222.2 gals. × v)

v = [$18,500 – $17,000] ÷ [2,608.7 gals. − 2,222.2 gals.]

= $1,500 ÷ 386.5 gals. = $3.88 per gallon

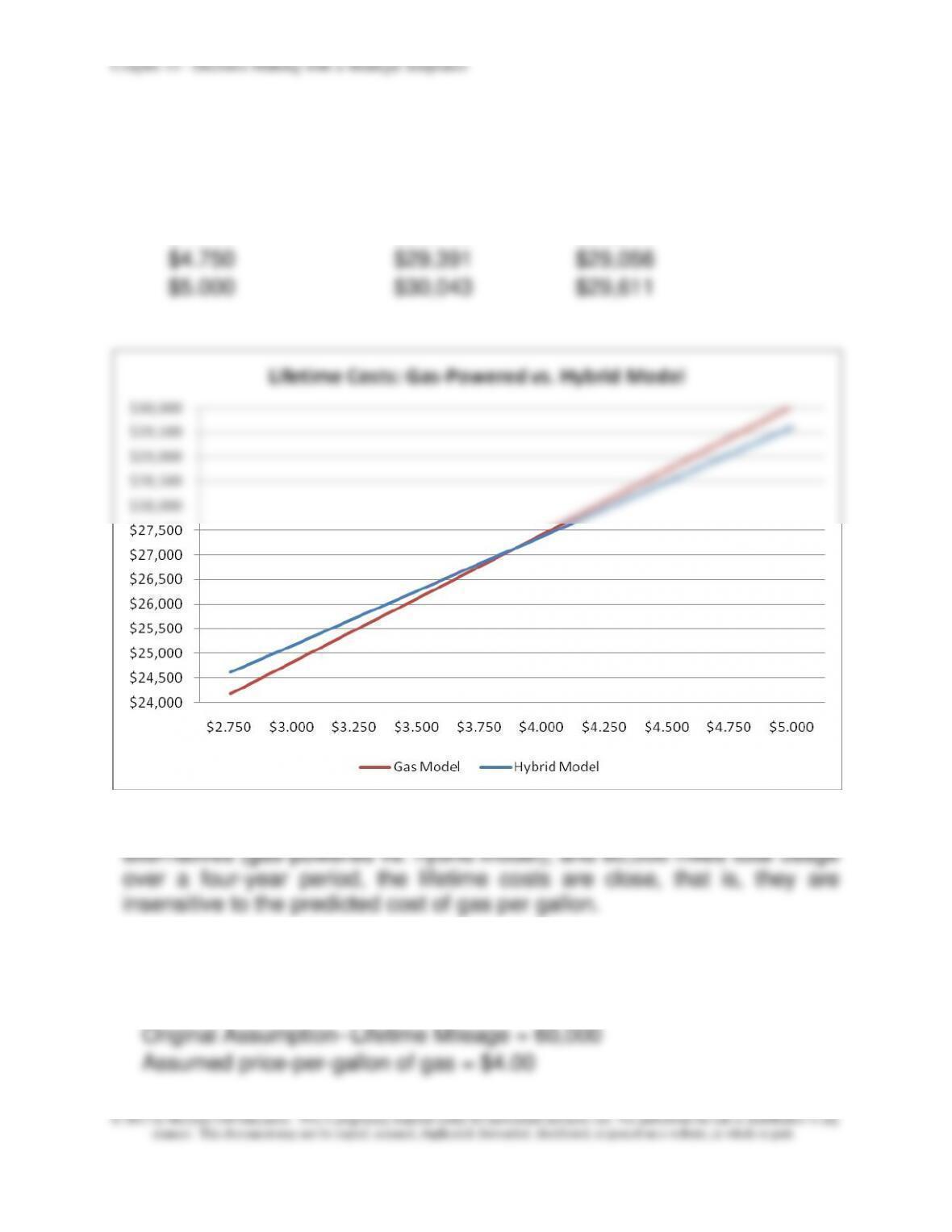

3. Graph of Lifetime Cost Function—Regular and Hybrid Models

X (price

Lifetime Cost

per gal.)

Gas Model

Hybrid

$2.750

$24,174

$24,611

$3.000

$24,826

$25,167

$3.250

$25,478

$25,722

$3.500

$26,130

$26,278

$3.750

$26,783

$26,833

11–84

11–46 (Continued-1)

$4.000

$27,435

$27,389

$4.250

$28,087

$27,944

$4.500

$28,739

$28,500

$4.750

$29,391

$29,056

$5.000

$30,043

$29,611

Based on the above analysis and graph, we see that for these two

4. Pseudo degree of operating leverage (DOL) measure

Alternative Lifetime Mileage Assumption = 62,000

Original Assumption—Lifetime Mileage = 60,000

Assumed price-per-gallon of gas = $4.00

Chapter 11 – Decision Making with a Strategic Emphasis

11–46 (Continued-2)

Lifetime Cost

Lifetime Cost

%

Option

@ 62,000

miles

@ 60,000

miles

Change

Cost

% Change

Mileage

Pseudo

DOL

Gas Powered

Car

$27,783

$27,435

1.2678%

3.333%

0.380

Hybrid Model

$27,685

$27,389

1.0818%

3.333%

0.325

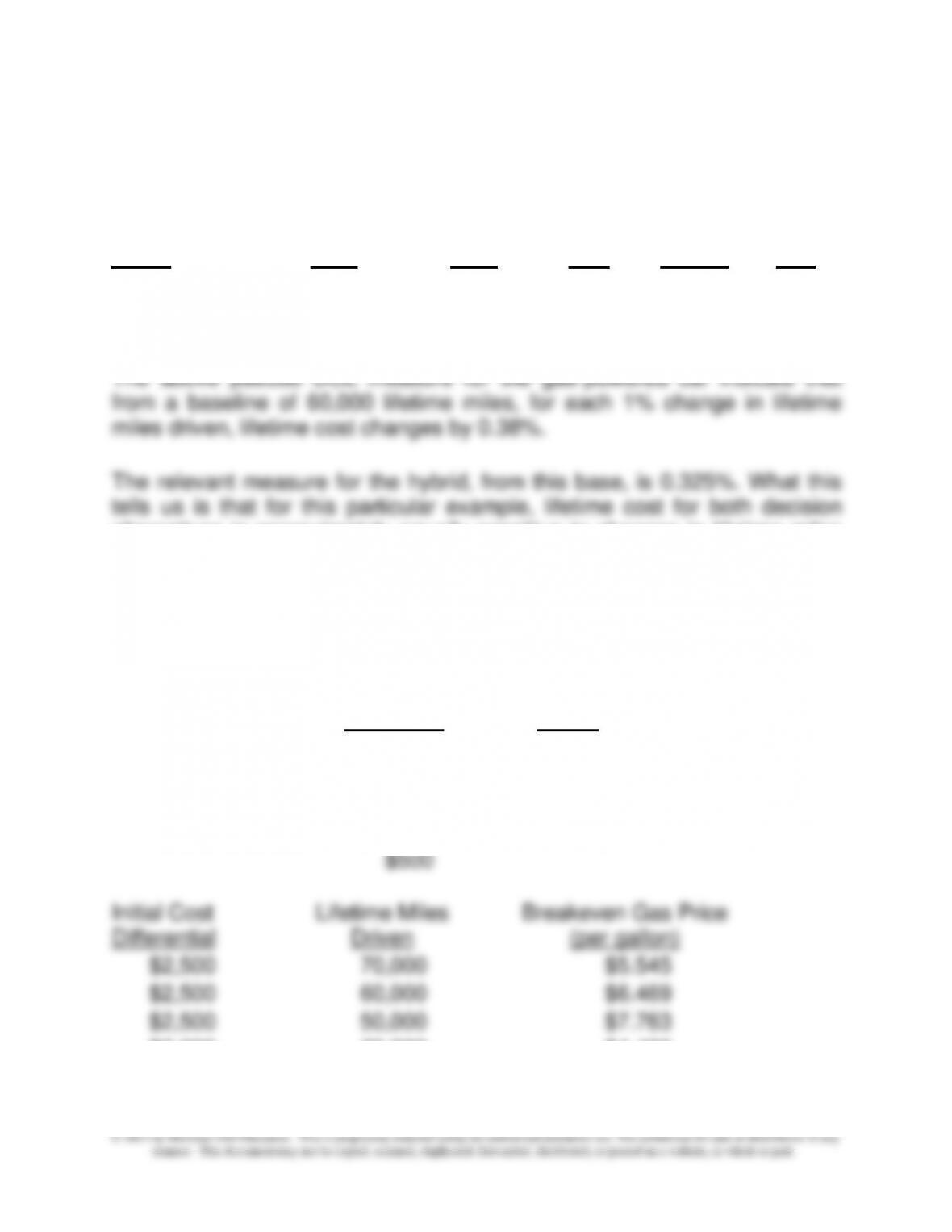

The above pseudo DOL measure for the gas-powered car indicate that

from a baseline of 60,000 lifetime miles, for each 1% change in lifetime

miles driven, lifetime cost changes by 0.38%.

The relevant measure for the hybrid, from this base, is 0.325%. What this

tells us is that for this particular example, lifetime cost for both decision

alternatives is approximately equally sensitive to changes in lifetime miles

driven.

5. Decision Table—Break-even gas price as a function of different

combinations of initial cost differential (Hybrid cost [net of rebate] −

Cost of gasoline-powered model) and lifetime miles driven

Initial Cost

Difference

Lifetime Miles

Driven

$2,500

70,000

$2,000

60,000

$1,500

50,000

$1,000

$500

Chapter 11 – Decision Making with a Strategic Emphasis

11–86

11–46 (continued-3)

Breakeven

Initial Cost Lifetime Miles Gas Price

Differential Driven (per gallon)

$1,500

70,000

$3.327

$1,500

60,000

$3.881

$1,500

50,000

$4.658

$1,000

70,000

$2.218

$1,000

60,000

$2.588

$1,000

50,000

$3.105

$500

70,000

$1.109

$500

60,000

$1.294

$500

50,000

$1.553

indifferent between the hybrid model and the gasoline-powered model.

Notice from the above table that the higher the initial cost differential for the

hybrid versus the gasoline-powered model, the greater the breakeven point

in terms of cost per gallon of fuel. You also notice that the breakeven gas

price is inversely related to lifetime miles driven. While both conclusions

seem intuitively appealing, the advantage of the decision table is the

structured way in which it allows you to deal quantitatively with uncertainty

surrounding the financial consequence of your decision choice.

6. Expected value calculations:

10

E(ax) = ∑(Lifetime costi × pi)

i=1

$2,000

50,000

$6.210

Chapter 11 – Decision Making with a Strategic Emphasis

11–87

9-46 (continued-4)

Action (Decision)

i

Event

p

Hybrid

Gas Model

1

$2.75

0.01

$246

$242

2

$3.00

0.05

$1,258

$1,241

3

$3.25

0.05

$1,286

$1,274

4

$3.50

0.05

$1,314

$1,307

5

$3.75

0.15

$4,025

$4,017

6

$3.88

0.15

$4,069

$4,069

7

$4.00

0.15

$4,108

$4,115

8

$4.25

0.20

$5,589

$5,617

9

$4.50

0.10

$2,850

$2,874

10

$4.75

0.09

$2,615

$2,645

Expected Lifetime cost =

$27,360

$27,401

Lifetime cost = initial cost outlay (F) + variable (gas) cost over four-year

period

Example: for the hybrid model, if the probability of gas selling at

$2.75/gallon is 0.01, then the appropriate amount is cost

component for calculating expected lifetime cost is:

then the expected lifetime cost of both actions (given the assumed

probability distribution) is approximately equal.

Finally, note that basing the decision solely on expected value (in the

present case, cost) ignores the risk preferences (utility function) of the

decision-maker. The decision table presented above in part 5 can

facilitate this discussion.