Chapter 12 – Strategy and the Analysis of Capital Investments

12–76

12–54 (Continued-4)

1See part (1), Problem 12-53, reproduced as follows:

Years 1 and 2:

Depreciation expense per year (SL basis):

($120,000 – $20,000) 10 years = $10,000

Income Tax Rate (t) × 0.40

Tax savings on depreciation, Years 1 and 2 $ 4,000

Years 3, 4, and 5:

Book value before overhaul (end of original useful life) $ 20,000

2Savings from the improved productivity = $10/hr. × 8,000 hours × 20% = $16,000

Less: Income Taxes on the savings (@40.0%) = – 6,400

After-tax savings $9,600

3Years 1 and 2:

Book value at the time of overhaul: $10,000 × 2 + $20,000 = $ 40,000

Overhaul cost + 80,000

Total amount to be depreciated $120,000

Number of years 2

Depreciation expense per year $60,000

4. As a follow-up to (3) above: although the cost difference between

the two alternatives is only $2,852.4, which is less than 0.3% of the

Chapter 12 – Strategy and the Analysis of Capital Investments

12–77

to undertake the overhaul two years early.

12–55 Comparison of Capital-Budgeting Techniques, Sensitivity Analysis

(75minutes)

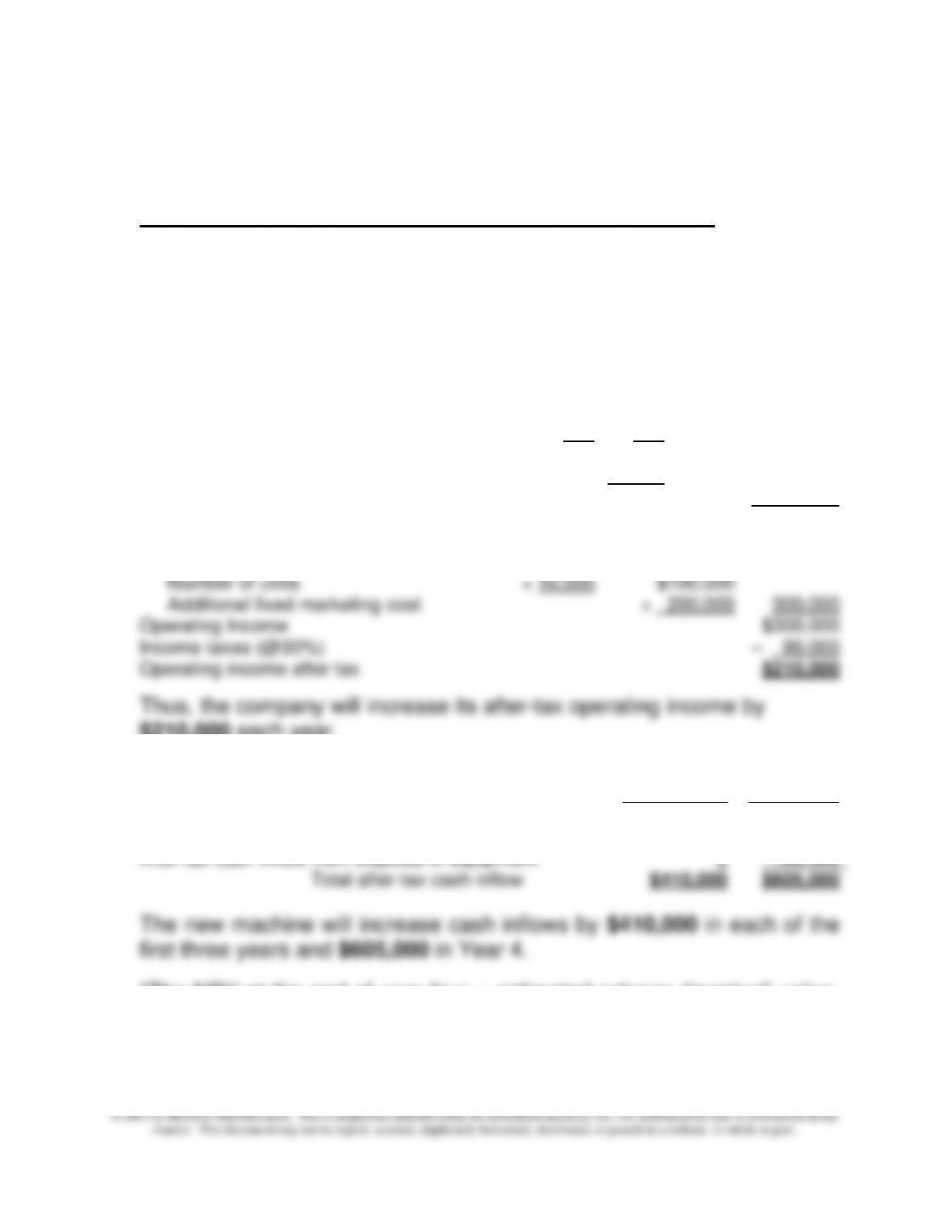

1. Effects of the new equipment on operating income after tax:

Sales $195 × 10,000 = $1,950,000

Cost of goods sold:

Variable manufacturing costs per unit $ 90

Fixed manufacturing costs per unit:

Additional fixed manufacturing overhead:

$250,000 ÷ 10,000 units = $25

Depreciation on new equipment, per unit:

($995,000 – $195,000) ÷ 4 = $200,000/year

$200,000 ÷ 10,000 units per year = + 20 + 45

Total manufacturing cost per unit (@ 10,000 units) $135

Times: Number of units × 10,000

Total cost of goods sold (CGS) 1,350,000

Gross margin $ 600,000

Operating Expenses:

Variable marketing: Cost per unit $ 10

$210,000 each year.

2. Years

1 to 3 Year 4

After-tax operating income (see #1 above) $210,000 $210,000

Add: increased depreciation expense (SL basis) 200,000 200,000

*The NBV at the end of year four = estimated salvage (terminal) value.

Therefore, there is no taxable gain or loss on this transaction.

Chapter 12 – Strategy and the Analysis of Capital Investments

12–78

12–55 (Continued-1)

3. Under the assumption that cash inflows occur evenly throughout the

year, the payback period is as follows:

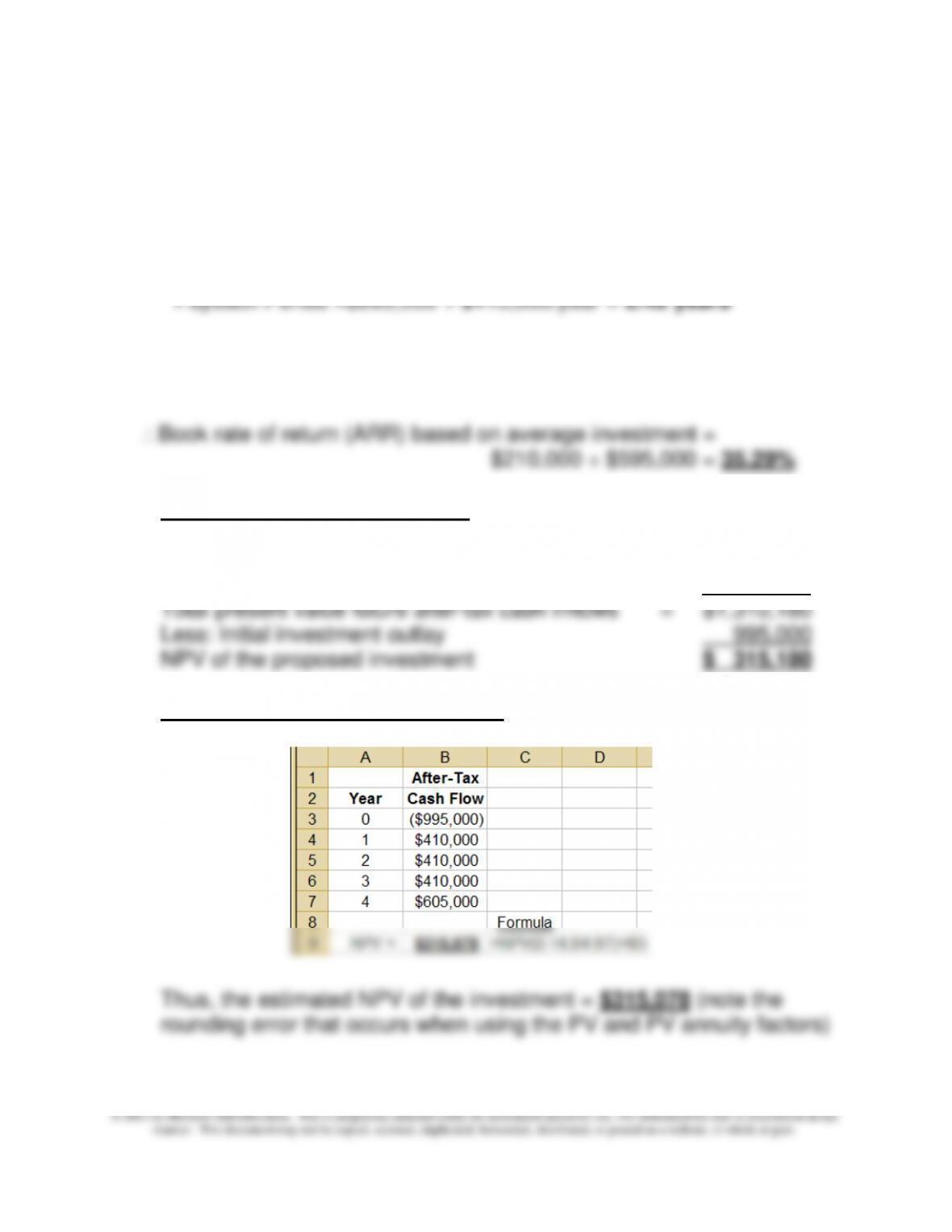

4. Average investment = ($995,000 + $195,000) ÷ 2 = $595,000

Average after-tax operating income = $210,000

5. Using PV and Annuity Tables:

PV of after-tax cash inflows (@14%):

Years 1 through 3: $410,000 × 2.322 = $ 952,020

Year 4 ($410,000 + $195,000): $605,000 × 0.592 = 358,160

Using the NPV Function in Excel:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–55 (Continued-2)

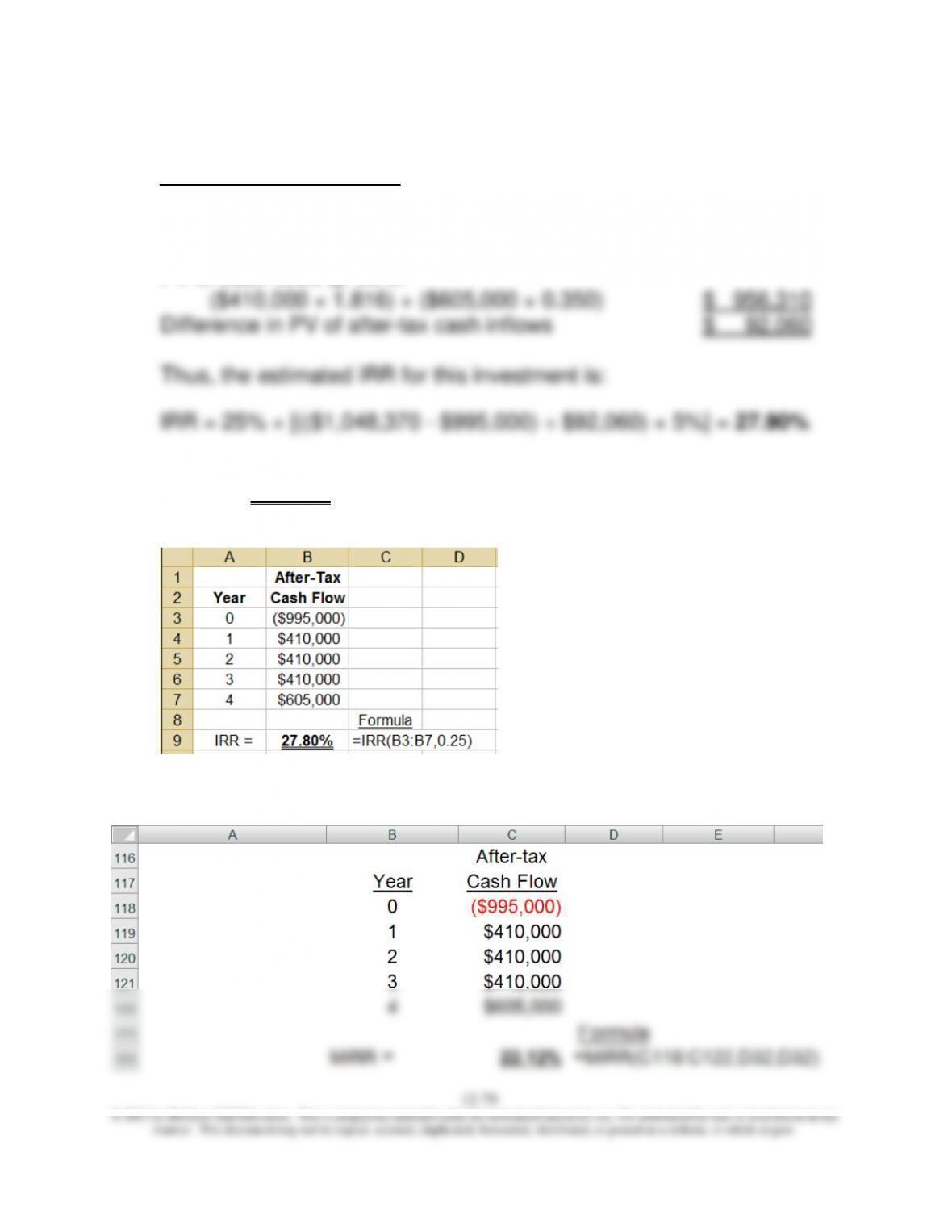

6. Trial-and-Error Approach (initial investment outlay = $995,000):

PV of cash flows @ 25%:

($410,000 × 1.952) + ($605,000 × 0.410) $1,048,370

PV of cash flows @ 30%:

Based on the built-in function in Excel, the estimated IRR of this

project = 27.80%, as follows:

7. The modified internal rate of return (MIRR) = 22.12%, as follows:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–80

12–55 (Continued-3)

8. a. Based on an estimated NPV of $315,078 (part 5, above), the PV of

any after-tax increase in variable costs associated with units produced

by the new machine = $315,078. Thus, the annual after-tax increase

Therefore, the variable cost per unit can increase by a maximum of

$154,466 ÷ 10,000 units = $15.45 per unit. At this increase, the new

equipment would generate a rate of return of exactly 14%—its cost of

capital.

b. The maximum pre-tax decrease in selling price = $154,466 (see (a)

above). On a per-unit basis, for all units sold, the maximum decrease

in unit selling price is therefore equal to $7.72 (rounded), that

9. Strategic considerations—among the additional factors to be considered:

• What is the associated risk of not expanding capacity? (e.g., loss of

• In the absence of increased volume, would Nil Hill be able to match

the anticipated lower prices by competitors?

Chapter 12 – Strategy and the Analysis of Capital Investments

12–81

12–55 (Continued-4)

• Are there any strategic factors associated with this investment?

a) Impact of the new equipment on customer response time?

b) Impact of the new equipment on plant safety?

c) Impact of the new equipment on environmental performance/

f) Are there any more profitable uses of the existing space?

That is, would this space best be used to increase capacity

of the particular product in question?

Chapter 12 – Strategy and the Analysis of Capital Investments

12–82

12–56 Sensitivity Analysis; Equipment-Replacement Decision (45-60

minutes)

1. The maximum amount of annual variable operating expenses, pre-tax,

that would make this an attractive investment from a present-value

PV (@ 12%) of salvage differential, from year 6 = $45,597

Net investment outlay − PV of salvage differential = $414,403

Year PV factor s (@ 12%)

1 0.892857143 (1 ÷ (1+0.12)1)

2 0.797193878 (1 ÷ (1+0.12)2)

3 0.711780248 etc.

4 0.635518078

5 0.567426856

6 0.506631121

Annuity factor = 4.111407324

PV of annuity = annuity amount × annuity factor

Annuity amount = PV of annuity ÷ annuity factor

Chapter 12 – Strategy and the Analysis of Capital Investments

12–83

12–56 (Continued-1)

2. Recalculation, based on an after-tax basis:

Combined (federal and state) income tax rate = 40.00%

After-tax WACC (discount rate) =

10.00%

Net pre-tax investment outlay, time 0 =

$460,000

Tax effect of loss on sale of existing asset =

$4,000

12–56 (Continued-1)

Net-of-tax initial investment outlay, time 0 =

$456,000

Differential salvage value, e-o-y 6 =

$90,000

Tax effect on differential salvage values =

$36,000

Net-of-tax differential salvage value, e-o-y 6 = $54,000

Differential tax shield, depreciation deductions:

Annual tax shield, existing asset =

$3,333

Annual tax shield, replacement asset =

$33,333

$30,000

PV of differential depreciation tax shield (@10%) =

$30,000 × 4.344261 (see below) = $130,658

Annual pre-tax operating expenses, existing asset = $200,000

Annual post-tax operating expenses, existing asset =

$200,000 × (1 − 0.4) = $120,000

Chapter 12 – Strategy and the Analysis of Capital Investments

12–84

12–56 (Continued-2)

Year PV factor (@ 10%)

1

0.90909

2

0.82645

3

0.75131

4

0.68301

5

0.62092

6

0.56447

4.35526

PV of after-tax variable operating costs, replacement asset

=

after-tax net investment outlay − PV of after-tax differential

salvage values − PV of differential tax savings due to

depreciation deductions

= $456,000 − $30,481 − $130,658 = $294,861

PV of annuity = annuity amount × annuity factor

annuity amount = PV of annuity ÷ annuity factor

= $294,861 ÷ 4.355261 = $67,702

Therefore, maximum annual after-tax variable operating expenses new

asset

=

$120,000

−

$67,702

=

$52,298

or, maximum pre-tax variable operating expenses =

$87,163

Chapter 12 – Strategy and the Analysis of Capital Investments

12–85

3. Additional (i.e., strategic) factors that might bear upon this decision:

a) Are any competitors of the Mendoza Company contemplating a similar

investment? Would such investments by competitors pose a strategic

d) Is Mendoza competing on the basis of price? Would the proposed

investment allow the company to establish/maintain its position as a

low-cost competitor?

Chapter 12 – Strategy and the Analysis of Capital Investments

12–86

12–57 Present Value Analysis; Sensitivity Analysis; Spreadsheet Applications (60

Minutes)

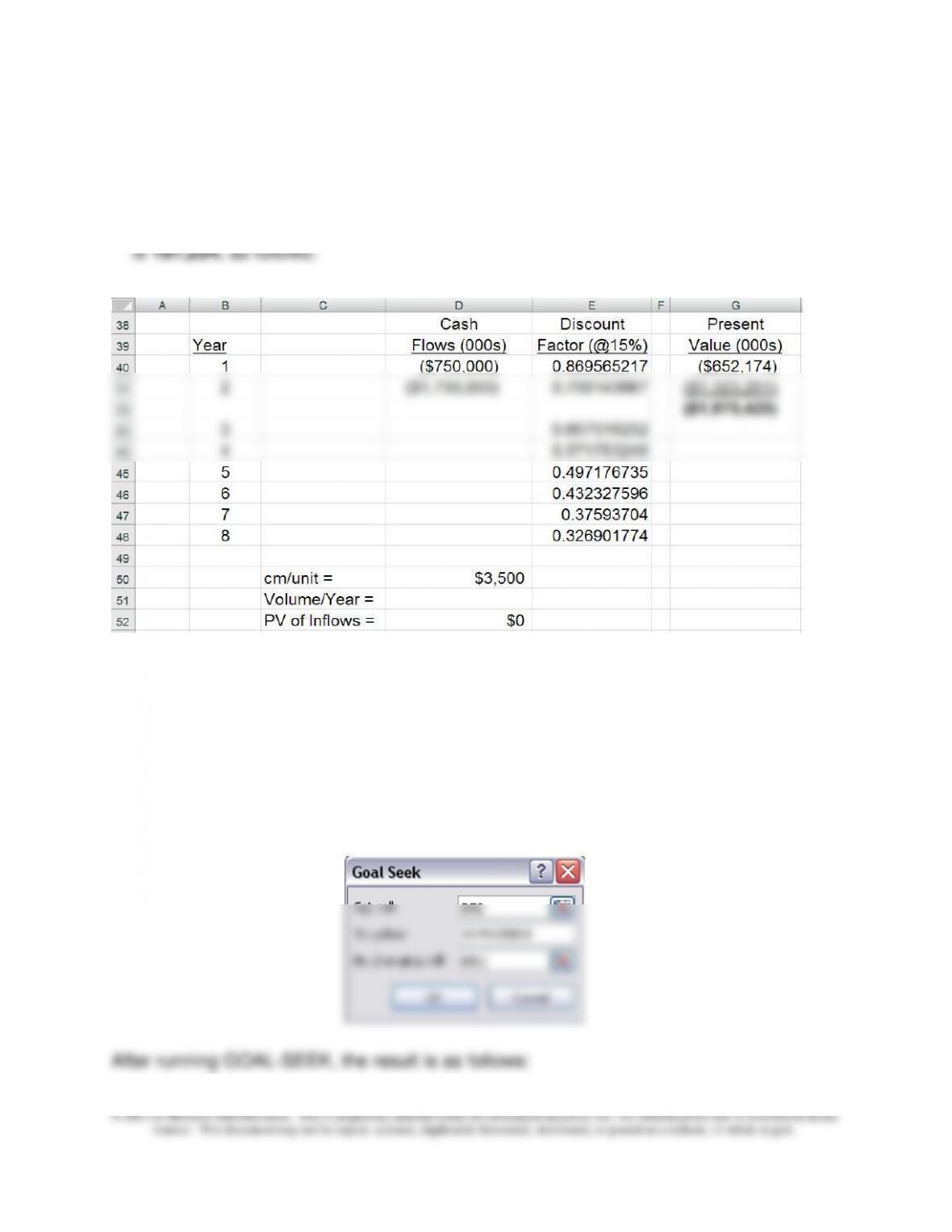

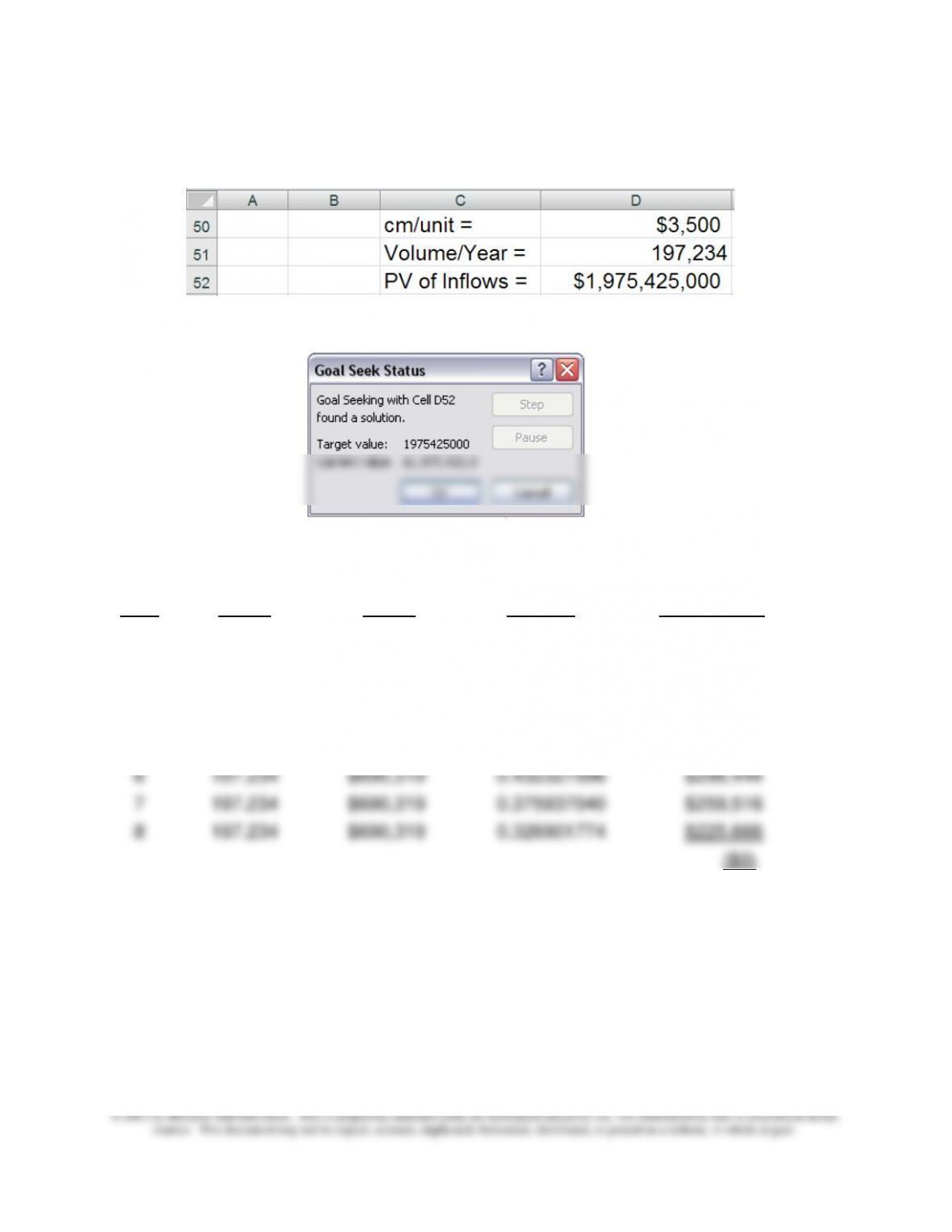

1. The minimum volume of car sales, per year, in the six-year life of the plant that is

needed to make this proposed investment acceptable using NPV as decision criterion

Formula, cell D52:

=(D50*D51*E43)+(D50*D51*E44)+(D50*D51*E45)+(D50*D51*E46)+(D50*D51*E47)

+(D50*D51*E48)

Note: The discount factors in Column D were calculated using the following equation:

PV factori = 1 ÷ (1 + r)i, where r = discount rate (WACC) and i = year (i = 1, 8).

Goal Seek Window:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–87

12–57 (Continued-1)

And the GOAL SEEK window will have changed to:

Check:

Discount

Year

Volume

(000s)

Cash Flows

(000s)

Factor

(@15%)

Present

Value (000s)

1

($750,000)

0.869565217

($652,174)

2

($1,750,000)

0.756143667

($1,323,251)

3

197.234

$690,319

0.657516232

$453,896

4

197.234

$690,319

0.571753246

$394,692

5

197.234

$690,319

0.497176735

$343,211

6

197.234

$690,319

0.432327596

$298,444

7

197.234

$690,319

0.375937040

$259,516

8

197.234

$690,319

0.326901774

$225,666

($0)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–88

12–57 (Conitnued-2)

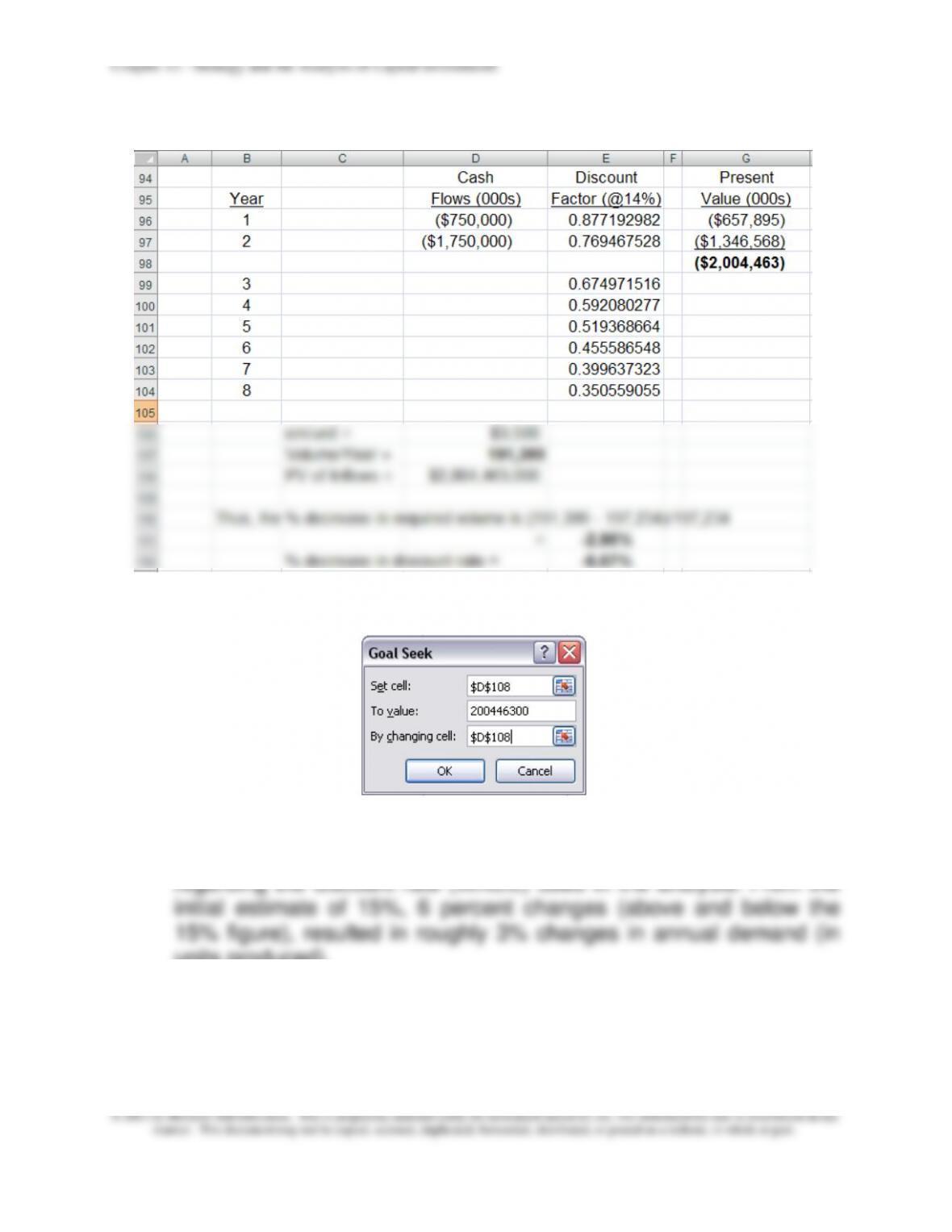

2. Sensitivity analysis:

a. if the company’s pre-tax WACC is 16% (rather than 15%), then the

required annual volume changes to 203,155 units (% change =

3.00%), as follows:

Cash

Discount

Present

Year

Flows (000s)

Factor (@16%)

Value (000s)

1

($750,000)

0.862068966

($646,552)

2

($1,750,000)

0.743162901

($1,300,535)

($1,947,087)

3

0.640657674

4

0.552291098

5

0.476113015

6

0.410442255

7

0.353829530

8

0.305025457

cm/unit sold =

$3,500

Annual volume = 203,155

PV of inflows =

$1,947,087,000

% increase in volume = 3.00%

% increase in discount rate = 6.67%

b. if the company’s pre-tax WACC is 14% (rather than 15%), then the

12–89

12–57 (Continued-3)

The above results were generated using the following GOAL SEEK entries:

2c. Sensitivity issue: based on the limited analysis above, it does not

appear that the results are very sensitive to the assumption

units produced).

3. Selected strategic considerations, including those related to risk

management, that would likely bear on this decision:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–90

12–57 (Continued-4)

a) Given volatility in the demand for fossil fuels, and wide price swings in

the cost of gasoline, are there any embedded options (“real options”) in

this investment project?

b) A rather substantial investment outlay is required. How sensitive is the

product line(s)?

e) Would the company be at competitive risk were it not to invest in the

new technology? That is, is this new-car option available to the

company’s competitors? If these competitors invest in this area, would

the company be at strategic risk?

f) Does the company compete on the basis of product differentiation?

That is, is the new product consistent with the strategy the company is

pursuing? Will, for example, the new facilities allow for reduced