Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-1

CHAPTER 9:

SHORT-TERM PROFIT PLANNING:

COST-VOLUME-PROFIT (CVP) ANALYSIS

QUESTIONS

9-1 The underlying relationship depicted in a cost-volume-profit (CVP) analysis is that

costs, revenues, and operating profits (Y) all change in a predictable way as the

volume of activity (X) changes.

9-2 The contribution margin ratio (CMR) is: (selling price per unit − variable cost per unit)

÷ (selling price per unit) = p ÷ (p – v)

The contribution margin ratio (CMR) represents the net contribution per sales dollar.

The CMR tells us the change in operating profit associated with a given change in

high CMR is associated with higher risk but also higher upside potential.

9-3 The basic assumption of the CVP model is that the behavior of revenues and total

costs is assumed to be linear over the relevant range of activity. Managers must be

deterministic, not stochastic), and a single cost driver: volume.

9-4 Sensitivity analysis is used to deal with uncertainties in profit planning, in two major

respects:

9-5 Sensitivity analysis deals with the risk that sales may fall short of expectations or that

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-2

9-6 The issue of taxes does not affect the calculation of the breakeven point because the

the basis of profits earned.

9-7 Margin of safety (MOS) = sales − breakeven sales, where “sales” can be either

budgeted or actual sales

9-8 The concept of operating leverage refers to the extent to which fixed (rather than

variable) costs characterize an organization’s cost structure. The higher the

9-9 The degree of operating leverage (DOL) is a measure, at any volume (X), of the

sensitivity of operating profit to a change is sales volume. It is measured as the ratio

9-10 In order to use the CVP model to find the breakeven point for multiple products, one

must assume that the sales of the products will continue at the present sales mix.

(Each product will continue to comprise the same proportion of total sales.) The

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-3

BRIEF EXERCISES

9-11 Unit contribution margin = selling price per unit − variable cost per unit

9-12 Total Contribution Margin = (selling price per unit − variable cost per unit) × #units sold

= ($100 − $80) × 500,000

9-13 Breakeven Point—Units:

Q × p = F + (v × Q)

Q × $20 = $175,000 + ($10 × Q)

9-14 Breakeven Point—Dollars:

p × Q = F + (v × Q)

9-15 Breakeven in Dollars: Y = [(v/p) × Y] + F

Y = [($500,000/$750,000) × Y] + $75,000

OR, breakeven in sales dollars = F ÷ cm ratio

= $75,000 ÷ 33.33% = $225,000

9-16 Unit Sales Q = (F + πB) ÷ (p – v)

Q = ($400,000 + $200,000) ÷ ($1 − $0.50)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-4

9-17 With a contribution margin (p – v) of $8 per battery, operating profits will increase by

9-18 Q = F + πA/(1− t)

(p – v)

Q = $200 + [$400/(1− 0.2)]

9-19 Margin of Safety (MOS), in units = Planned Sales – Breakeven Sales

= 100,000 − 80,000

= 20,000 units

MOS, in $ = Planned Sales ($) − Breakeven Sales ($)

9-20 Degree of Operating Leverage (DOL) = Contribution Margin ÷ operating income

= [($40 − $20) × 400,000] ÷ $2,500,000

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-5

EXERCISES

9-21 Profit Planning (20-25 min)

1.πB= Sales − variable costs − fixed cost

= (30,000 × $67) − (30,000 × $34) − $480,500

= $509,500

2. BE units: $67Q = $34Q + $480,500

(Operating profit falls by $35,000 = ($33 × 5,000) − $200,000, from

$509,500 to $474,500 as a result of the plan to increase sales with

increased advertising.)

4. BE units: $67Q = $34Q + $680,500

(the slight difference between the indicated operating profit,

$26, and zero is due to rounding up the breakeven point to the

nearest whole number, 20,622 units)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-6

Slight difference in the above answers is due to

rounding on sales volume, Q. The primary point,

however, is that a given percentage change in fixed

cost leads to an equivalent percentage change in the

breakeven point. (This can be confirmed precisely if the

above breakeven volumes were not rounded.)

9-21 (Continued)

Percentage increase in fixed cost (F):

New level of fixed cost $680,500

Original level of fixed cost $480,500

Percentage increase 41.62%

Percentage increase in breakeven point:

New breakeven point (rounded up) 20,622

Original breakeven point

14,561

Percentage increase 41.63%

5. $509,500 = $67Q − $34Q − $680,500

(To justify the advertising plan, sales would have to rise to at least 36,061

units, somewhat above the projected level of 35,000 units.)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-7

9-22 Margin of Safety (MOS) (20 min)

1. First, calculate the breakeven point, using the contribution margin ratio

(CMR), as follows:

CMR = $227,500 ÷ $650,000 = 0.35

Breakeven in dollars = $105,000 ÷ 0.35 = $300,000

Therefore:

2. The MOS and related MOS ratio (or, percentage) are rough measures of

operating risk. They indicate the amount by which sales could fall before

losses are incurred.

3. If sales fall to $500,000, the breakeven point will remain the same, but the

MOS will change:

MOS, in $ = $500,000 – $300,000 = $200,000

Operating profit:

Contribution margin = $500,000 × 0.35 = $175,000

Less fixed costs 105,000

Why this works:

Operating profit = MOS × CMR

= (Expected Sales − Breakeven) × CMR

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-8

9-22 (Continued)

(Note: by definition, breakeven in sales dollars × CMR = fixed costs; i.e., at the

breakeven point there is just enough contribution margin generated to cover

total fixed costs)

9-23 The Role of Income Taxes (20 min)

1. Pre-tax income = $70,000 ÷ (1 − 0.35) = $107,692.31

2. Contribution margin − fixed cost = before tax profit

3. total sales – total variable cost = total contribution margin

total sales – (variable cost ratio × sales) = $347,692.31

4. Contribution margin ratio (CMR) = $347,692.31 ÷ $1,390,769.31 = 0.25

Breakeven point = fixed costs ÷ CMR

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-9

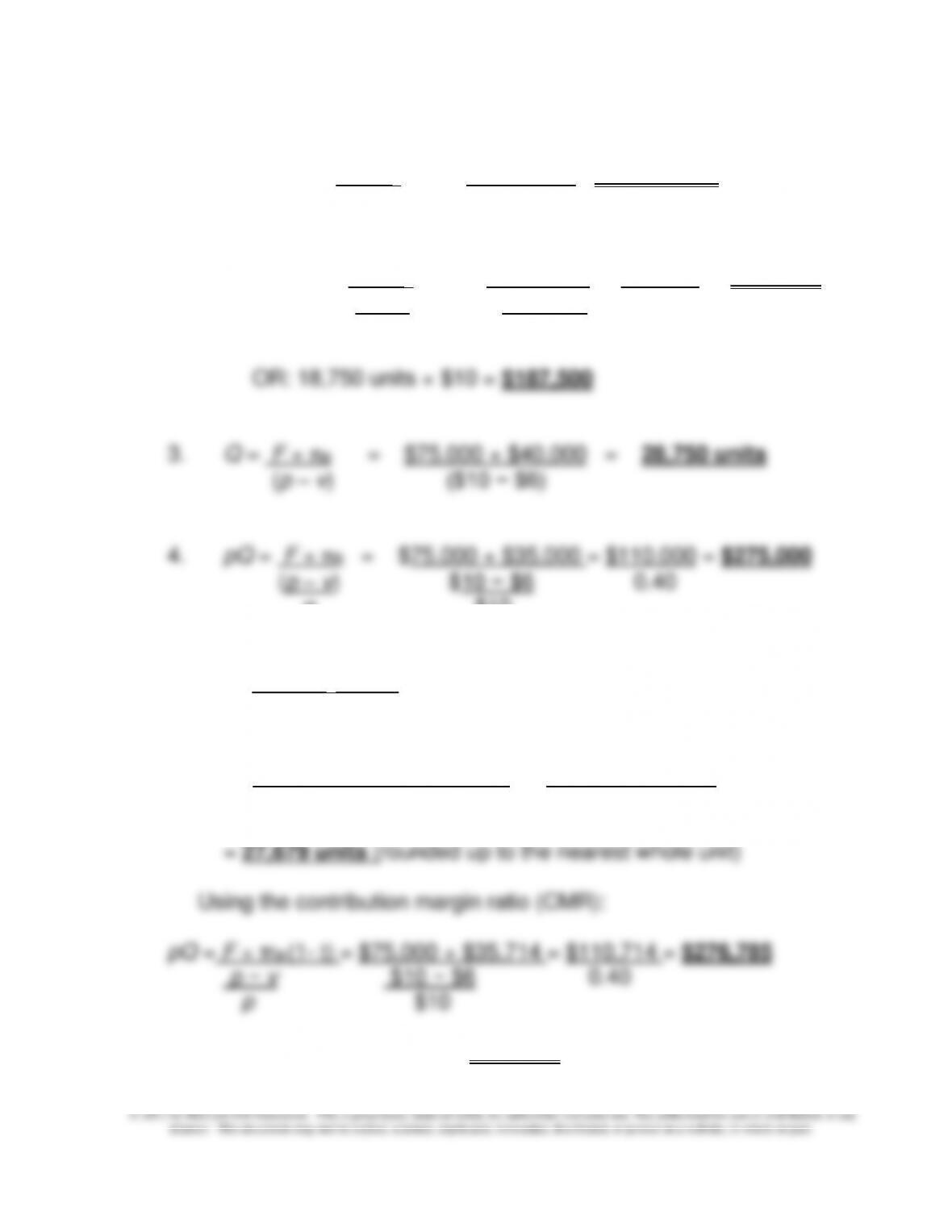

9-24 CVP Analysis with Taxes (20-25 min)

1. BE units = F + πB = $75,000 + 0 = 18,750 units

(p – v) $10 − $6

2. BE dollars = F + πB = $75,000 + 0 = $75,000 = $187,500

(p – v) $10 − $6 0.40

p $10

p $10

5. Q = F + πA/(1 − t)

(p – v)

Q = $75,000 + $25,000/(1 − 0.3) = $75,000 + $35,714

$10 − $6 $4

OR: 27,679 units × $10/unit = $276,790 (difference due to rounding)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-10

9-25 Cost Planning; Machine Replacement (30 min)

1.

Machine A Machine B

$2Q = $0.65Q + $135,000 $2Q = $0.3Q + $204,000

Q = 100,000 Q = 120,000

2. cost of using Machine A = cost of using Machine B

When 197,143 switches are needed, the Vista Company is indifferent as

to which machine to use.

An alternative way to determine the indifference point is:

Fixed cost of Machine A − Fixed Cost of Machine B

Unit variable cost of A − Unit variable cost of B

$204,000 − $135,000

$0.65 − $0.30

machine B.

3.

cost when purchasing from outside supplier:

$2 × 200,000 = $400,000

cost when using machine A:

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-11

9-25 (continued-1)

4. Recommendation to management:

Considerations regarding outsourcing (rather than making internally):

what is the reliability of the existing supplier? Likely price increases in the

future from this supplier? What is the reliability of the external supplier

(delivery time, etc.)? As we’ve seen with supply disruptions in Japan

subsequent to the 2011 tsunami/earthquake in Japan, it may make

Considerations regarding insourcing (rather than purchasing

externally from the current supplier): is sufficient capital (to purchase and

install machinery) available? Are there any training-related costs to be

borne? The decision to insource increases the operating leverage of the

company, which in turn increases the business (or operating) risk of the

company. Therefore, what is the long-term upside potential for increases

in sales—if large, then perhaps a move to a greater level of fixed costs

makes sense. What are anticipated year-to-year fluctuations in

sales/demand for the component in question? If these are significant,

then perhaps lower operating leverage is more advantageous. Finally, by

locking the company into a certain technology, does this decrease

flexibility (for future investments in alternative technologies, as an

example)?

The basic point to make to students is that choice of cost structure both

reflects and influences a company’s strategy. This elevates the

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-12

9-26 Degree of Operating Leverage (DOL) (20 min)

1. DOL = contribution margin÷ operating profit

A’s DOL = $50,000 ÷ $35,000 = 1.43

B’s DOL = $70,000 ÷ $30,000 = 2.33

If sales increase, company B will benefit more. Company B has a higher

proportion of fixed costs in relation to variable costs; therefore it has a

higher operating leverage than does Company A. The degree of

2. COMPANY A COMPANY B

Amount % Amount %

Sales $110,000 100 $110,000 100

Less variable costs 55,000 50 33,000 30

Contribution margin $ 55,000 50 $ 77,000 70

Less fixed costs 15,000 40,000

Operating income $ 40,000 $ 37,000

Therefore, if sales volume increased by 10%, operating profit should

increase by 14.3%. This is precisely what happened. The same logic

applies to Company B.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-13

9-26 (Continued)

3. Further interpretation of DOL—in what sense is DOL a measure of risk?

As indicated by the above responses, DOL measures how sensitive

operating profits are to changes in sales volume. If DOL is high, then

even small (%) changes in sales will lead to large (%) changes in

operating income. It is this magnification process that captures what is

called business or operating risk (as compared, for example, to financial

Finally, we note that DOL can be defined as: % change in operating

income/% change in sales (i.e., the percentage change in operating

income for each percentage change in sales volume from point Q).

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-14

9-27 Cost Planning: The Cost of an MBA; Time Value of Money (10 min)

Using the present value factor (4.212) for an annuity for five years at 6% shows

that the present value of $23,742 per year is $100,000 ($100,000 ÷ 4.212); this

means that for the student a current payment (at one point in time in this

simplified example) of $100,000 is equivalent to receiving a benefit of $23,742

Note that the cost of the program includes the foregone pre-MBA salary, and

for students at prestigious programs like School B, the pre-MBA salaries are

relatively high. So the increase in salary post-MBA does not show the degree

of “bump” that is seen in other schools. Also, the calculation above does not

reflect the opportunity that might attract a new MBA to a company, apart from

the pay offer. For example, BusinessWeek provides a listing of its Top-50

Employers, based on surveys of students, college placement personnel, and

the employers themselves. As of September 2008, the Big-4 public accounting

firms, Goldman Sachs, Google, Marriott, Lockheed Martin, IBM and

JPMorgan/Chase lead the list.

Another Business Week survey shows the cost and increase in pay for 20 well–

know U.S. universities. Brigham Young University is shown as the top value

with a high ratio of pay increase to cost.

A Wall Street Journal ranking of the return on investment for top executive

MBA programs, based on tuition costs and projected salary, shows surprising

results, among them that the top five programs are at public Universities; the

highest-ranked program, Texas A&M University, produced a 243% return on

investment.

Source: “The High Price of Admission,” BusinessWeek, October 23, 2006, p.

60. Also: “Fifty Employers with the Right Stuff,” BusinessWeek, September 15,

2008, p. 39; Alina Dizik, “Ranking the Returns on Executive MBAs,” The Wall

Street Journal, December 10, 2008, p D1.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-15

9-28 Cost Planning; Gasoline Prices (20-25 min)

1. Solve for the indifference point in miles (M) where 15 is the mpg, and $2.99

is the guarantee price and $5.00 is the expected price:

Savings for the guarantee = Savings for the discount

preferred.

2. Solve for the indifference point in gasoline price (G) where 15 is the mpg,

and $2.99 is the guaranteed price and 8,500 is the expected annual mileage

(8,500 × 3 years = 25,500 miles for three years):

Total cost without the guarantee = Total cost with guaranteed gas price

exceeds $5.637 (on average) over the next three years.

3. Some important decision factors include:

• Do I need a new car, or should I save the money by fixing up my present

car, including a tune up and new tires which could help improve gas

• If in an urban area or where it is available, should I use car-share

programs?