10–31

Exhibit 3

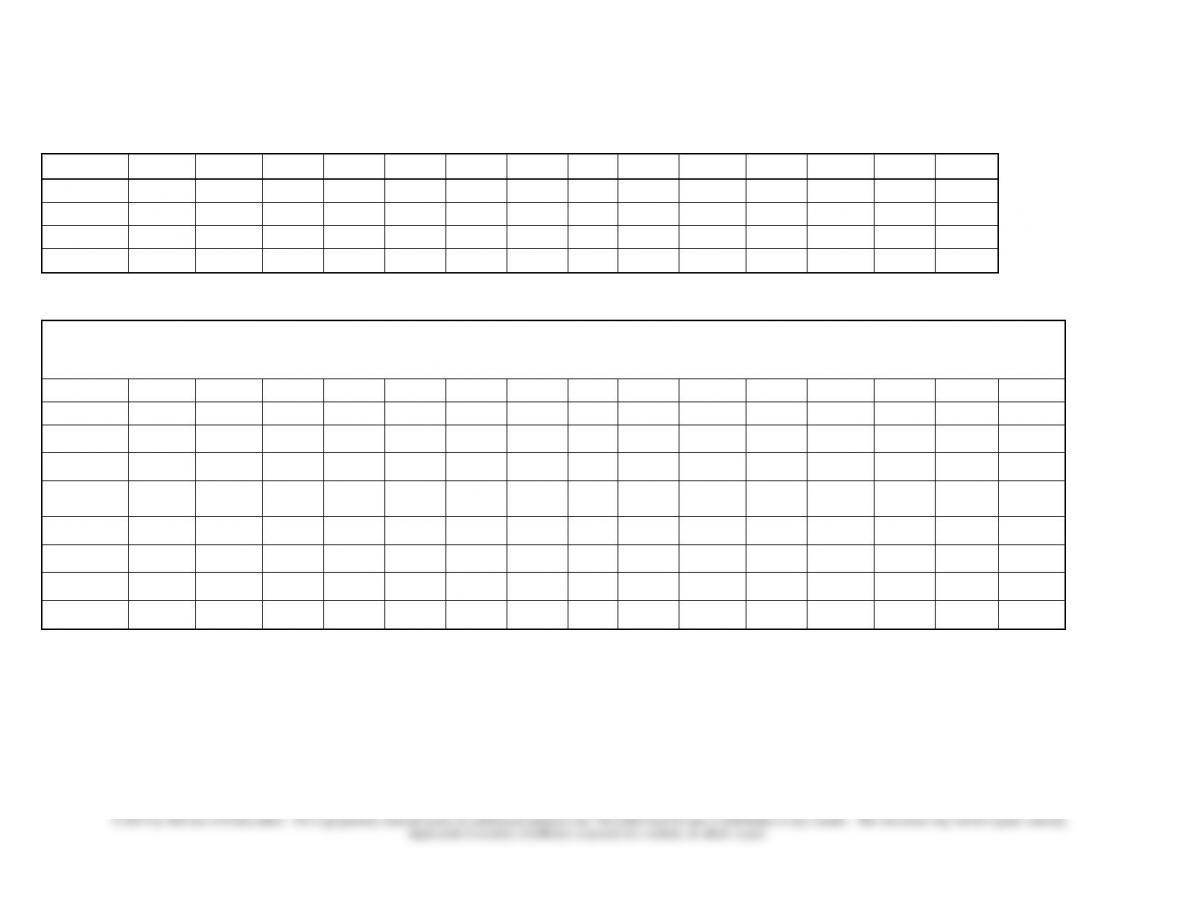

Use of Resource Drivers (time or usage) by Activities

A1

A2

A3

A4

A5

A6

A7

A8

A9

A10

A11

A12

A13

Total

Manager

1.00%

14.00%

70.00%

15.00%

100.00%

Advisors

15.00%

15.00%

10.00%

8.00%

5.00%

10.00%

5.00%

17.00%

15.00%

100.00%

Office Staff

10.00%

10.00%

10.00%

25.00%

15.00%

30.00%

100.00%

Reproduction

55.00%

25.00%

10.00%

10.00%

100.00%

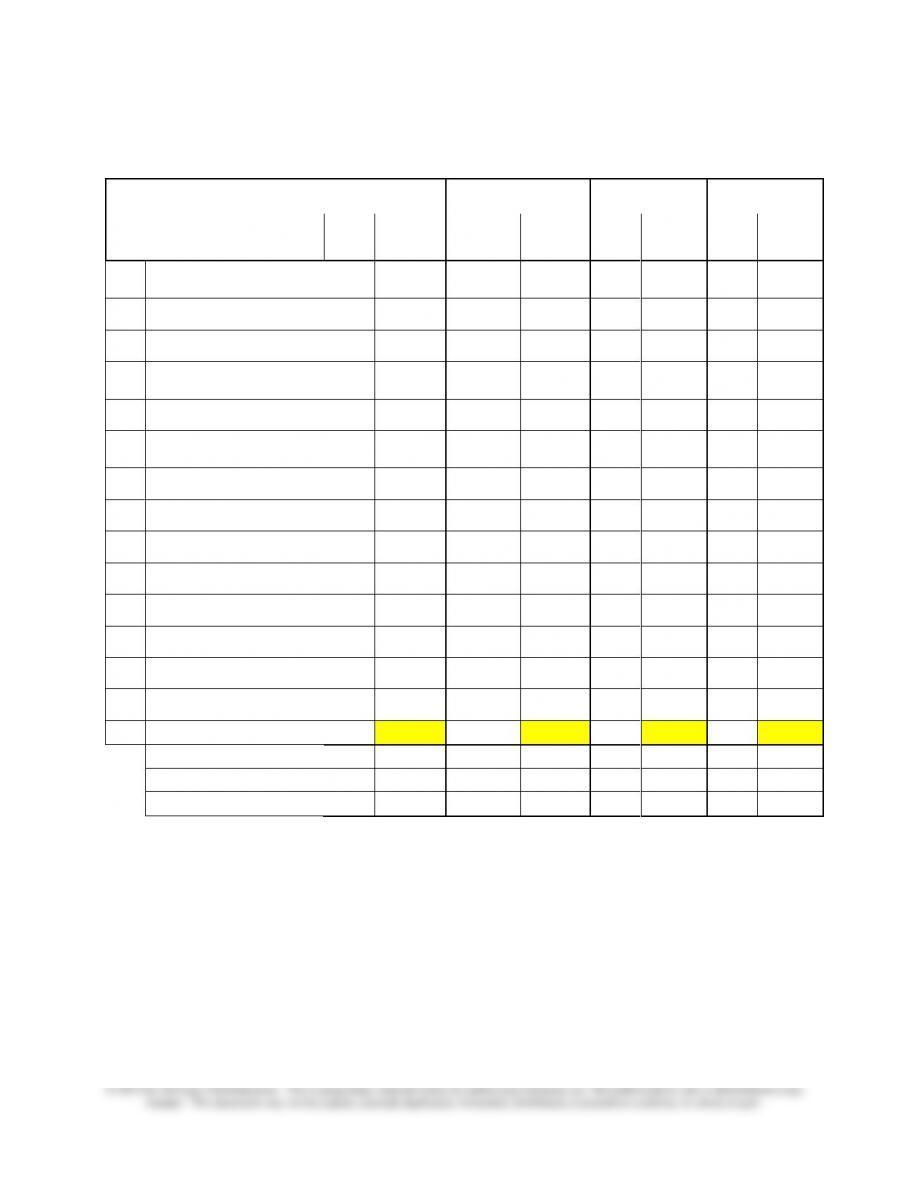

Activity

Costing

Cost Item

Item

Amount

A1

A2

A3

A4

A5

A6

A7

A8

A9

A10

A11

A12

A13

Total

Manager

$ 96,226

$ –

$ –

$ –

$ –

$ –

$ –

$ –

$ 962

$ –

$ 3,472

$ 67,358

$ –

$ 4,434

$ 96,226

Advisors

409,356

61,403

61,403

40,936

32,748

20,468

40,936

–

20,468

69,591

61,403

–

–

–

409,356

Office Staff

106,678

–

10,668

–

–

10,668

10,668

–

–

26,670

16,002

–

32,003

–

106,678

Equipment &

Software

63,840

63,840

63,840

Reproduction

135,000

74,250

–

–

–

33,750

–

–

–

13,500

–

13,500

–

–

135,000

Travel

40,000

40,000

40,000

Hospitality

23,400

23,400

23,400

Total

$874,500

$ 35,653

$ 2,071

$ 0,936

$32,748

$ 4,886

$ 1,603

$ –

$ 1,430

$ 09,760

$ 0,877

$120,858

$ 5,843

$ 7,834

$874,500

10–32

Exhibit 4

Benchmark

COBAA

External

AMC

EDUCATION

Activity Cost Comparisons

$/FTE

$/FTE

$/FTE

$/FTE

Activity

%

6200

%

unknown

%

3400

%

4875

A1

Disseminate graduation

requirements

16%

$

21.88

28%

$ 25.00

25%

$

20.00

20%

$

17.80

A2

Correct graduation checks

8%

11.62

8%

6.40

7%

6.23

A3

Monitor academic progress

5%

6.60

12%

10.50

5%

4.00

2%

1.78

A4

Issue readmission

contracts

4%

5.28

3%

2.23

A5

Enroll freshmen

7%

10.47

12%

9.60

7%

6.23

A6

Review substitution and

waivers

6%

8.32

7%

6.23

A7

Develop advising materials

0

–

1%

1.25

5%

4.45

A8

Update website

2%

3.46

7%

6.00

18%

14.40

15%

13.35

A9

Advise students

13%

17.70

48%

42.00

32%

25.60

29%

25.37

A10

Check prerequisites

10%

14.66

6%

5.34

A11

Recruit students

14%

19.49

A12

Tutor students

11%

15.46

A13

Arrange career fairs

4%

6.10

Miscellaneous other

4%

3.25

Per FTE

100%

$141.05

100%

$88.00

100%

$80.00

100%

$89.00

Student satisfaction

Low

High

High

High

Units at graduation

147

130

136

132

FTF years to graduation

6.8

4.4

5

5

10–33

Exhibit 5

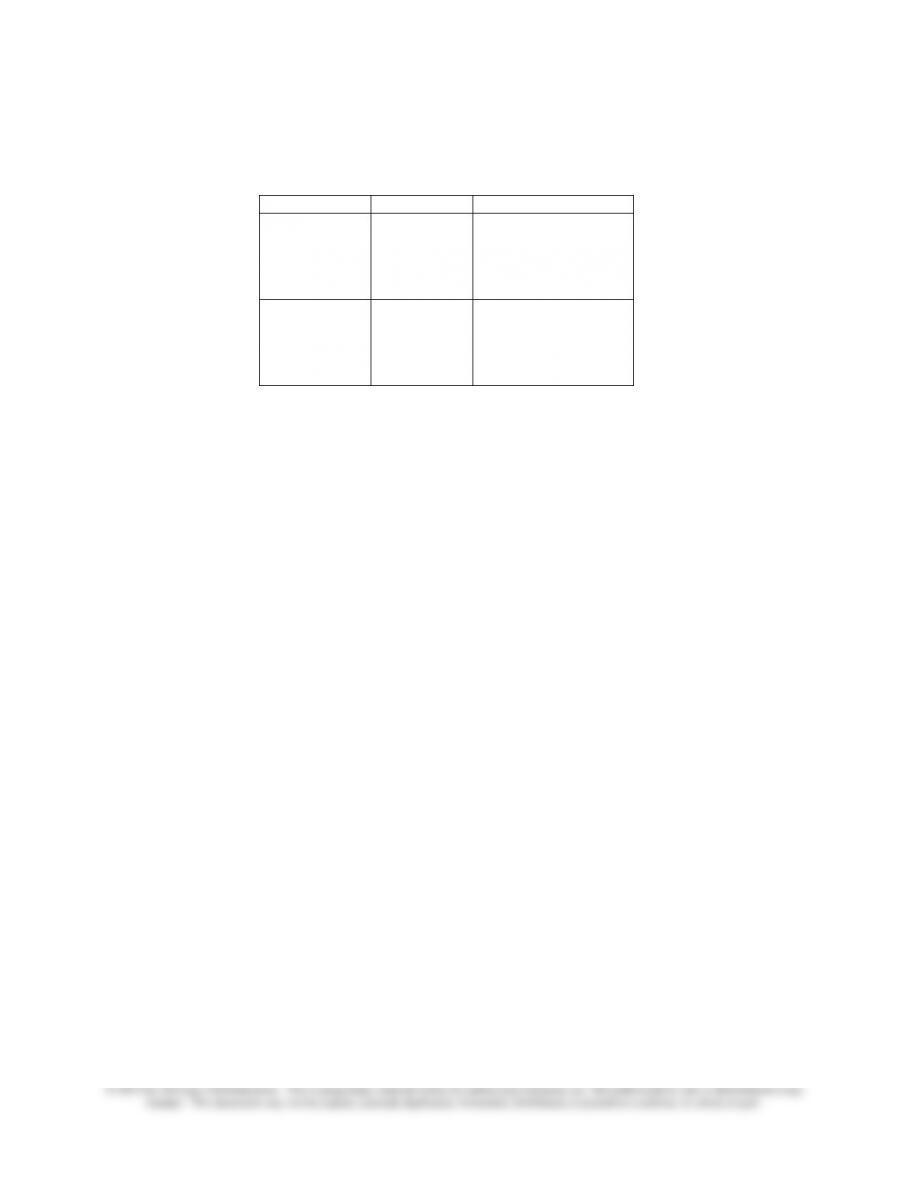

Activity Evaluation Matrix

Performance

Strategic

Non-Strategic

Perform Well

Cell 1

Continue

Cell 2

Drop or Create Niche

Perform Poorly

Cell 3

Improve

Cell 4

Drop

2

10–34

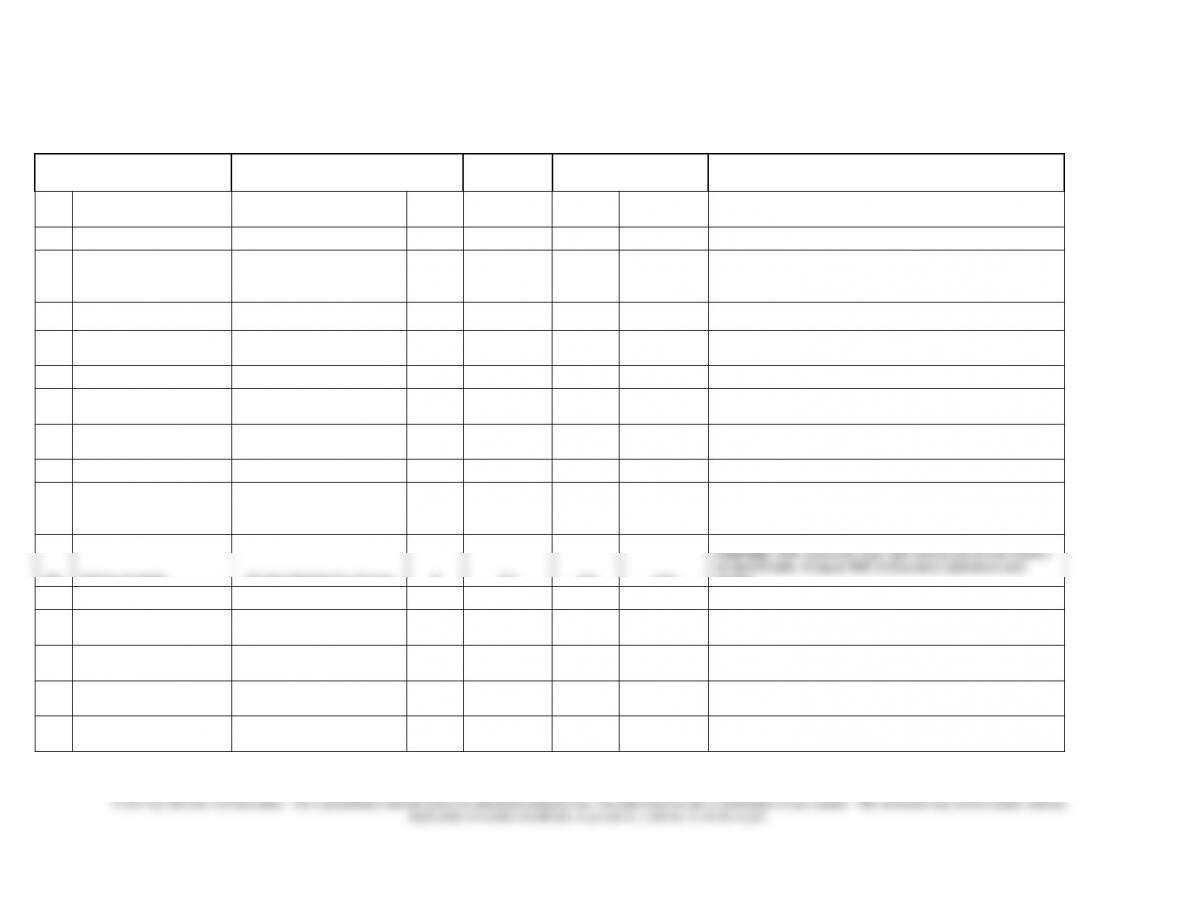

Exhibit 6

COBAA: Activity Evaluation & Suggestions

Activity

University Performance

Measure

Goal

COBAA

Performance

Strategic

Performance

Action Suggested

A1

Disseminate graduation

requirements

Units at graduation

124

units

147

Yes

Poor

Improve. Get details of AMC’s and Education’s operations and

reorganize in a similar way.

Student Satisfaction Survey

5.5

2.6

A2

Correct graduation checks

% needing intervention at

university level

n/a

21%

Short run

yes, long

run no

Poor

Continue until the university revises the graduation check

process. Improve. Study how this activity is performed by AMC

and copy in COBAA.

A3

Monitor academic

progress

Average semesters on

probation

1.5

1.5

yes

good

Continue

A4

Issue readmission

contracts

No measure

n/a

yes

Continue

A5

Enroll freshmen

Freshman satisfaction survey

6

6

yes

good

Continue

A6

Review substitution &

waiver requests

Chair Satisfaction Score

n/a

2.3

no

poor

Drop. Duplicate activity. Department chairs do not like what

COBAA is doing.

A7

Develop advising materials

% major/options with advising

materials

100%

100%

yes

good

Improve. Transfer more items to the Web. Test them with

students so they are user friendly.

Student Satisfaction Survey

5

3.1

marginal

A8

Maintain website

No measure; new initiative

n/a

yes

unknown

Improve. Shift advising materials & paths to graduation on the

Web. Create interactive sections where students can plan their

own four- or five-year plan.

A9

Advise students

Student Satisfaction Survey

5

2.1

yes

poor

Continue. Shift resources here; little activity performed relative

to benchmarks. Analyze AMC & Education operations and

model.

Time to graduation-FTF

5

6.8

A10

Check prerequisites

Student Satisfaction Survey

n/a

2.1

maybe

poor

Continue. Discontinue in long run; computer system should be

reprogrammed. Use student focus group to improve.

A11

Recruit students

% women & other minority

students

n/a

67%

no

good

Drop/ Creative Solution. This activity is done well, transfer

activity to university outreach.

A12

Tutor students

Hours provided

n/a

390

no

good

Drop/ Creative Solution. Transfer to the clubs and redeploy the

computers to the lab or a tutoring room.

A13

Arrange career fairs

% Students with jobs in field

at graduation

n/a

72%

no

good

Drop/Creative Solution. Transfer responsibility to the Career

Center.

2

10–35

Exhibit 7

Suggested Strategy Map

COBAA STUDENT RESULTS

ACTIVITIES

UNIVERSITY

ACTIVITIES

Understand

Graduation

Requirements &

Course

Prerequisites

Higher GPA

& Academic

Progress

Higher

Retention Rate

Lower Advising

Cost per FTE

Reduced Time

to Graduation

Enrolling in

Proper Courses

Understand how to

use computer

registration

Higher

Student

Satisfaction

Reduced Units

at Graduation

Disseminate

Advising

Materials

A1 A7 &8

Checking

Prerequisites

A10

Graduation

Checks

A2

Monitor

Academic

Progress

A3 &4

Course

Registration

Training

A5

Advising

Students

A9

10–37

Exhibit 8

Summary of Action

COBAA Activities

Performance

Strategic

Non-Strategic

Perform Well

A3, A4, A5

Continue

A11, A12, A13

Creative Solution or Drop

Perform Poorly

A1,A2*,A7,A8, A9, A10

Improve

A2*, A6

Drop

*Shown in two cells: long run, drop; short run, keep.

10–38

Exhibit 9

COBAA

Proposed Budget for 2008

Item

Amount

Change

Revised

Comment

Manager

$ 85,000

$ 85,000

Refocus manager to mission relevant

activities

Advisors

342,000

342,000

85% of manager & 10% of advisors

redeployed by eliminating A6, A11, & A13.

Use time on activities needing

improvement.

Office Staff

73,000

16,500

56,500

Cut 1/2 of part-time hours equal to 1 full-

time equivalent staff person ($33,000 part

time * 1/2)

Equipment & Software

106,400

68,096

38,304

Cut 15 stations used for tutoring; 1 for

headcount reduction; return to physical

plant for redeployment

Reproduction

135,000

13,500

121,500

Remove the amount for A11; ultimately

transfer advising materials to web

Office supplies & phone

69,700

6,970

62,730

Reduce by one headcount

Travel

40,000

40,000

–

Eliminate travel, A11

Hospitality

23,400

23,400

Eliminate hospitality, A13

$874,500

$706,034

Per FTE

$ 141.05

$ 113.88

Budget Reduction

Achieved

19%

10–39

Exhibit 10

COBAA

Scorecard

Perspective

Measures

Financial

Advising cost per FTE

Customer

Student satisfaction with Advising, retention rate, units at graduation, FTF time to

graduate, semesters to graduate for transfer students

Internal

Processes

FTE/Headcount, % advising problems solved by interactive website, % graduation

checks with deficiencies, % student population on probation contracts, % options with

online requirements and suggested paths to graduation

Learning &

Growth

Advisor retention, student suggestions implemented, manager’s report on causes of

student interactions & Web inquiries, # FAQs added to website based on analysis of

frequent causes for questions

10–40

Teaching Notes for Readings

Reading 10-1: “How to Set Up a Budgeting and Planning System”

This article describes the experience in setting up a formal budgeting system for a medium-sized public

utility holding company that provides natural gas storage and transportation services. The task is not as

easy as it might seem. The budget manager had to review the chart of accounts, account classification and

the reporting system of the firm, consider all the users’ diverse information needs, and update the current

accounting information system.

Discussion Questions:

1. What motivates PFG to install a budgeting and planning system?

restoring a common stock dividend. In addition, management wanted to improve expense and cash

flow tracking.

2. Why is flexibility very important for PFG’s budgeting system to be effective?

3. What problems that the budget manager at PFG had to resolve before setting up a budgeting system? Do

you find these problems unique to PFG?

Among the problems that the budget manager at PFG had to resolve include:

b. Divisions have different internal reporting systems and use different accounting software.

The problems that the budget manager at PFG faced were not unique, especially when the firm grew

through mergers and acquisitions.

10–41

4. Why the authors suggest that a thorough review of the firm’s chart of accounts, account

classifications, and reporting systems is a must before initiating a budgeting and planning

system?

Once a system has been installed it is difficult to change. In many cases, a firm’s accounting system

did not keep pace with the changes in the company. Expanded product lines and changes in customers

and geographical areas served could have led to changes in accounting systems. It is best if the budget

manager resolved information classification and reporting issues up front so that budgets are

comparable.

5. Describe budgetary games that people play. What are the reasons for PFG to experience

minimal budgetary gamesmanship?

Budgetary games that people play include padding the budget such as low-balling revenues or

overestimating expenses.

PFG has experienced minimal budgeting gamesmanship for two reasons:

10–42

Reading 10-2: “Strategic Budgeting: A Case Study and Proposed Framework”

This article applies to the budget-preparation process the Critical Chain technique proposed by Eliyahu

Goldratt. All department budgets are reduced by 50%. The savings are grouped in a “Group Budget

Buffer.” Department heads can request additional funds from the buffer but the request would be discussed

openly with other department heads. This reduction method allows costs to be cut where the cuts will not

negatively affect the performance of service departments. At the same time, it identifies areas of “bloat”

where cost reduction can be significant increases communication between departments, lowers overall

spending levels, and assures output integrity.

Discussion Questions:

1. What is the lawnmower method of cost reduction?

This term refers to the process of effecting “across-the-board” cuts in budgetary appropriations when

2. What will be the size of a division’s total budgeted amount after 4 years if the division includes

10% slack each year? after 10 years?

As indicated in Table 1c, with an assumed 10% slack built into the budget each year, the indicated

budget for a Research & Development Division at the end of four years contains slack equal in amount

to 112% of the original budget amount (for year 1). When the time horizon is extrapolated to year 10

(Table 1d), the amount of slack in the budget as a percentage of the original budget amount will have

3. What is the strategic budgeting (SB) model?

This approach to budgeting is borrowed from the “Critical Chain” model for project management

developed by Eliyahu Goldratt in his 1997 book. One way to think of SB is a structure plan to eliminate

10–43

4. What are the strengths of strategic budgeting (SB)? The authors of this article propose the following

benefits of using SB:

(1) Ease of Implementation—especially relative to other approaches to budgeting, such as Zero-Base

Budgeting (ZBB). Note that this conclusion holds particularly for the time of SB implementation

discussed in the article: each subunit initially received a 50% budgetary reduction.

(2) Increased Communication—sharing of information regarding the use of buffer resources helps

achieve coordination of activities and more valid spending (consumption of resources).

(3) Reduced Spending—with traditional approaches to budgeting, managers (having built in slack