Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–16

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then

return you to this Word document.

14–27 Master (Static) Budget Variance and Components (45 minutes)

1. Actual operating income = actual sales revenue − actual variable costs − actual

fixed costs = $380,000 − $210,000 − $145,000 = $25,000

2. Master (static) budget operating income = budgeted sales − budgeted variable

costs − budgeted fixed costs = $450,000 − $270,000 − $135,000 = $45,000

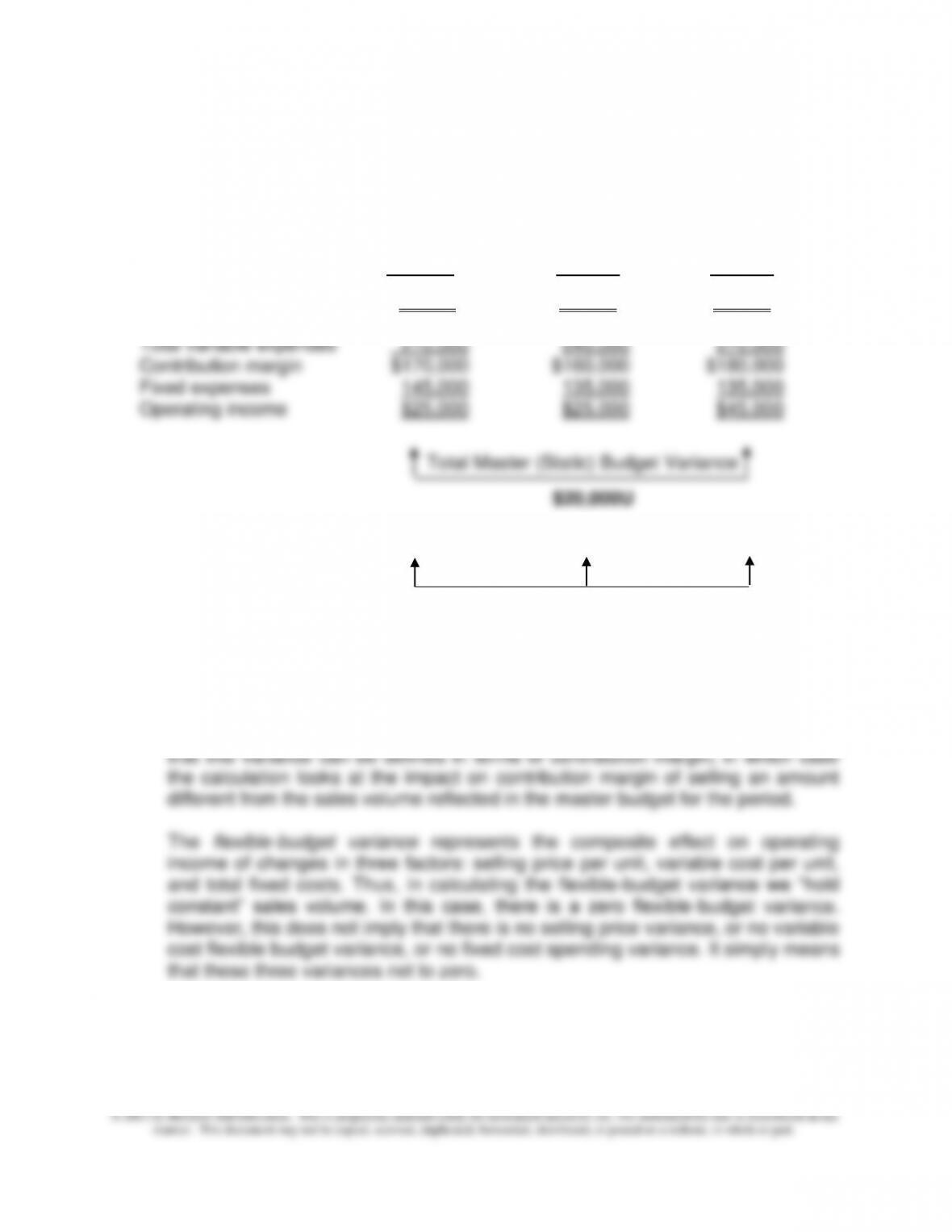

3. Total master (static) budget variance, in terms of operating income = actual

b) Sales volume variance, in terms of operating income = flexible-budget

operating income − master budget operating income = $25,000 − $45,000 =

$20,000U.

c) Master budget variance = Total flexible-budget variance + Sales volume

variance = $0 + $20,000U = $20,000U

Solution to Ex. 14-26

(6e).xlsx

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–17

14–27 (Continued)

In tabular form, we have:

Actual Flexible Master

Results Budget Budget

Unit sales 40,000 40,000 45,000

Sales $380,000 $400,000 $450,000

Flexible-Budget Sales Volume

Variance Variance

$0 $20,000U

5. The sales volume variance represents the impact on operating profit of selling a

different volume of sales compared to the budgeted volume reflected in the

master budget. As such, the calculation of the variance holds three other factors

constant: selling price per unit, variable cost per unit, and total fixed costs. Note

14–18

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

14–28 Flexible Budget and Operating-Income Variances (45 minutes)

1. Flexible budget for June, based on 950 units produced/sold (95% of original master

budget):

Units sold 900

Sales (95% × $800,000) $760,000

2. Refer to text Exhibit 14.1 for master-budget data

a. Sales volume variance, in terms of operating income = flexible-budget

operating income – master (static) budget operating income

= $182,500 − $200,000 = $17,500U

b. Sales volume variance, in terms of contribution margin = flexible-budget

contribution margin −master (static) budget contribution margin

3.

Actual Operating Results

For the Month of June

Sales (950 units × $835/unit) $793,250

Less: Total variable expenses 475,000

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–19

14–28 (Continued)

a. Total flexible-budget variance = actual operating income − flexible-budget

operating income = $138,250 − $182,500 = $44,250U

b. Total variable cost flexible-budget variance = actual variable costs − flexible-

budget variable costs = $475,000 − $427,500 = $47,500U

or, AQ × (AP − SP) = 950 units × ($835 − $800) = $33,250F

NOTE: total flexible-budget variance ($44,250U) = selling price variance ($33,250F)

+ total variable cost flexible-budget variance ($47,500U) + total fixed cost flexible-

budget variance ($30,000U).

The following presentation, similar to text Exhibit 14.4, might be useful for in-class

presentation purposes:

SCHMIDT MACHINERY COMPANY

Analysis of Operating Results

June 2013

Flexible Static (Master)

Actual Budget Budget

Unit sales 950 950 1,000

Sales $793,250 $760,000 $800,000

Total variable expenses 475,000 427,500 450,000

Contribution margin $318,250 $332,500 $350,000

Variance Variance

$44,250U $17,500U

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–20

14–29 Direct Materials and Direct Labor Variances (30 minutes)

Note: Refer to Exhibit 14.5 for standard cost information.

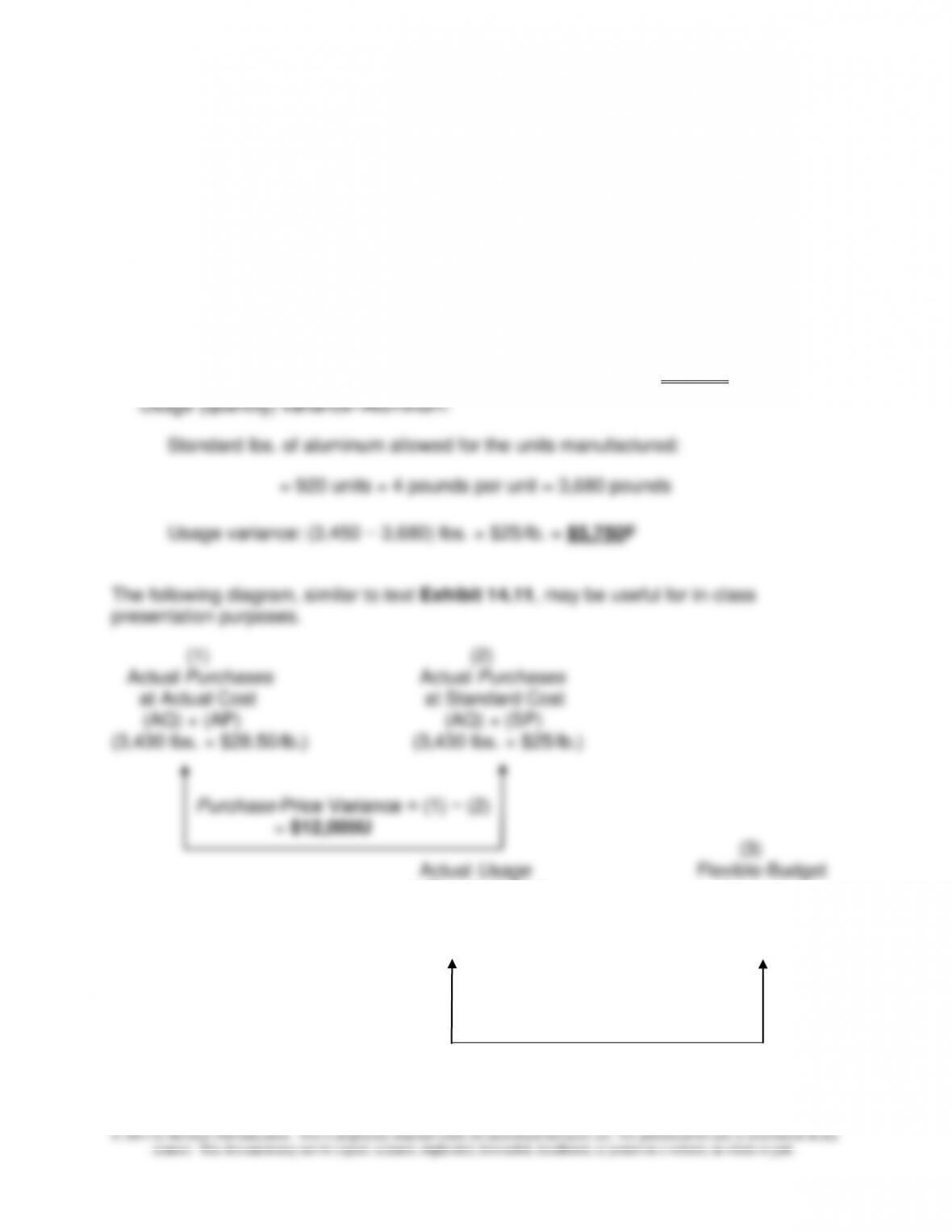

1. Purchase price variance–Aluminum:

Total lbs. aluminum purchased = lbs. used + ending inventory −

beginning inventory = 3,450 + 30 − 50 = 3,430 pounds

Purchase–price variance = ($28.50 − $25)/lb. × 3,430 lbs. = $12,005U

at Standard Cost Amount

(AQ) × (SP) (SQ) × (SP)

(3,450 lbs. × $25/lb.) (3,680 lbs. × $25/lb.)

Usage Variance = (2) − (3)

= $5,750F

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–21

14–29 (Continued)

2. Direct labor rate variance: ($41.50 − $40)/hr. × 4,200 hrs. = $6,300U

920 units × 5 hours/unit = 4,600 hours

Efficiency variance: (4,200 − 4,600) hrs. × $40/hr. = $16,000F

The following diagram, similar to text Exhibit 14.7, may be useful for in-class

presentation purposes:

(2) (3)

(1) Actual Input Flexible-budget

Actual Input Cost at Standard Cost Amount

Total Flexible-Budget Variance = (1) − (3)

= $174,300 − $184,000 = $9,700F

14–22

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

14–30 Standard Labor Rate and Labor Efficiency Variance (15-20 minutes)

Actual Inputs Actual Inputs Flexible-Budget

10,800 hrs. × $28.50/hr. 10,800 hrs. × (SP) 11,000 hrs. × (SP)

1. Total actual direct labor hours worked 10,800

Actual hourly rate × $28.50

2. Direct labor efficiency variance = actual hours at standard cost − standard labor

cost for units produced = [(AQ) × (SP)] − [(SQ) × (SP)] =

14–23

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

14–31 Generating a Flexible Budget; Spreadsheet Application (45–50 minutes)

1. Flexible Budget, sales volume = 55,000 units

Sales (55,000 units × $31.00/unit) $1,705,000

Less: Cost of Goods Sold:

Direct materials (55,000 units × $2.766666/unit) $152,157

Direct labor (55,000 units × $7.50/unit) 412,500

Manufacturing overhead:

Rent 77,000

Depreciation 50,000 $442,450

Operating profit $472,883

Note to Instructor: An Excel file solution for Part 1 and Part 2 of Exercise 14–31 is

embedded below. You can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then

return you to this Word document.

Ex. 14-31.xlsx

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–24

14–31 (Continued)

2. Flexible budget, sales volume = 65,000 units

Sales (65,000 units × $31.00/unit) $2,015,000

Less: Cost of Goods Sold:

Direct materials (65,000 units × $2.7666666/unit) $179,833

Direct labor (65,000 units × $7.50/unit) 487,500

Manufacturing overhead:

Variable (40% × $487,500) 195,000

Fixed [see answer, Part 1] 60,000 $922,333

Gross profit $1,092,667

Less: Operating expenses:

Selling expenses:

Sales commissions [$2,015,000 × ($167,400

$1,860,000)] $181,350

Rent 40,000

3. The text uses the term pro-forma budget to refer to a budget prepared for any

level of operating activity for a given period. We reserve the term “flexible–budget”

to refer to the control budget prepared after the period based on the actual activity

level (e.g., sales volume) achieved. The flexible-budget is key to the financial

control process: it allows us to decompose overall variances into more detailed

components. Normally, the amount of fixed costs reported in the flexible-budget is

multi-product companies, the sales-activity variance can be broken down into finer

components, as discussed in Chapter 16.

14–25

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

14–32 Behavioral Considerations and Continuous Improvement Standards (20-25

minutes)

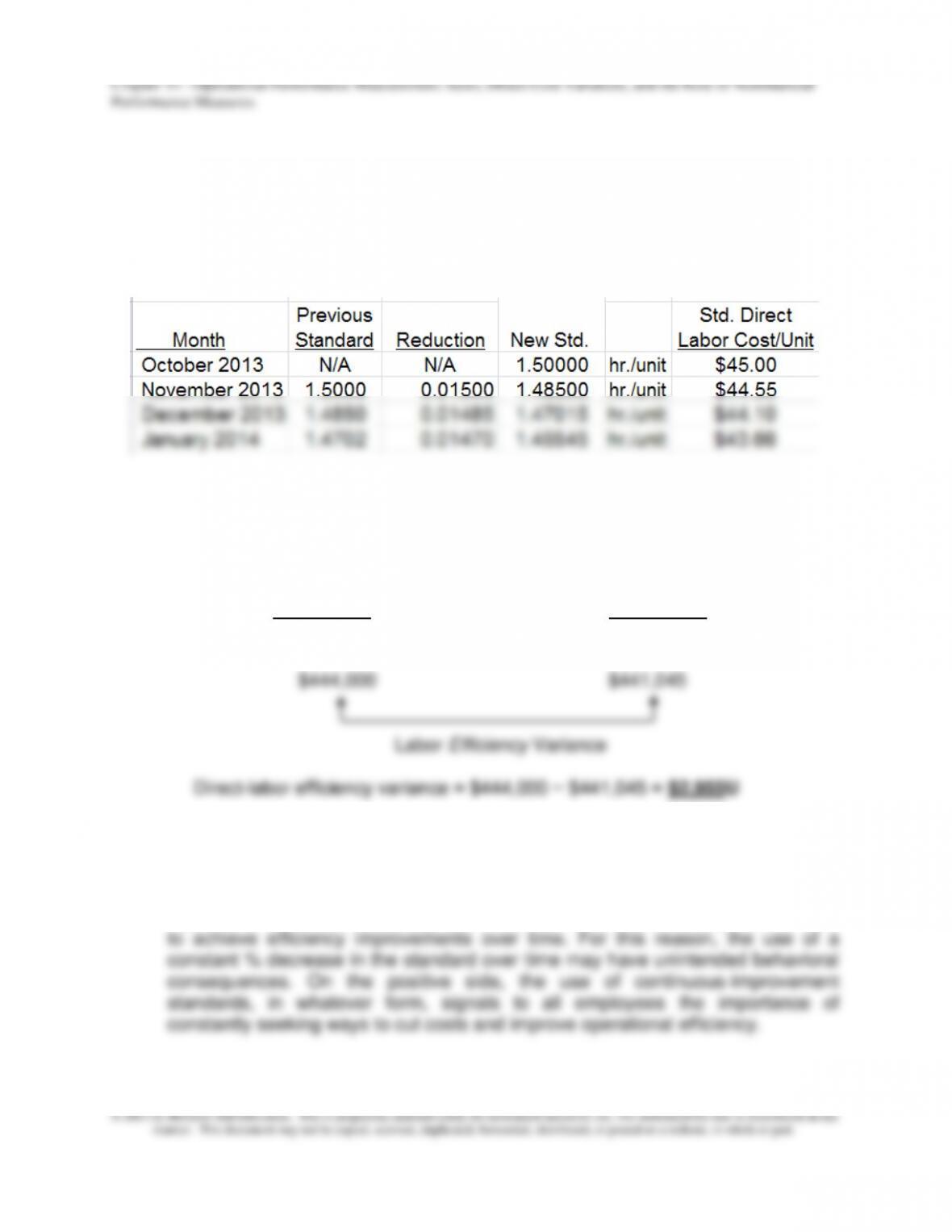

1. Direct labor-hour standards and standard direct labor cost per unit, October 2013–

January 2014:

2. Computation of direct labor efficiency variance, December 2013:

Actual Inputs Flexible-Budget

at Standard Cost Amount

(AQ) × (SP) (SQ) × (SP)

14,800 hrs. × $30.00/hr. (10,000 × 1.47015 hrs./unit) × $30.00/hr.

3. The basic trade-off is a problem similar to the situation with Kaizen: pushing

employees too hard for improvements, month after month. In response, workers

may perceive that the performance goal is simply not achievable, in which case

the standard itself loses its motivational value. In many processes, significant

improvements can occur initially. However, it becomes successively more difficult

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–26

14–33 Flexible Budget and Operating-Income Variances (30-45 minutes)

1. Budget data:

Selling price: $81,000 ÷ 18,000 units = $4.50 per unit

Variable cost : $30,600 ÷ 18,000 units = $1.70 per unit

a. Flexible budget for 20,000 units

Sales 20,000 × $4.50 = $90,000

Variable costs 20,000 × $1.70 = 34,000

Contribution margin $56,000

Fixed costs 20,000

Operating income $36,000

b. Contribution margin earned for the period:

$85,000 − $32,000 = $53,000

The following summary, similar to text Exhibit 14.4, may be helpful for in-class

presentation purposes:

Flexible- Sales Master

Budget Flexible Volume (Static)

Actual Variance Budget Variance Budget

Unit sales 20,000 -0- 20,000 2,000F 18,000

Sales $85,000 $5,000U $90,000 $9,000F $81,000

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–27

14–33 (Continued)

2. As long as both the budgeted and the actual operations are within the “relevant

range,” the flexible budget for the actual operating level and the master budget

3. The actual fixed costs for a period are likely to differ from the budgeted amount.

As a result, the contribution margin flexible-budget variance is likely to differ from

the operating income flexible-budget variance. This difference is equal to the total

14–34 Applicability of Standard Cost Systems (30-40 minutes)

1. The major advantages of using a standard cost accounting system include the

following:

▪ Budgeting. Standard costs can be the building blocks for budget preparations

and allow the development of flexible budgets.

▪ Performance evaluation. By comparing actual costs to standard costs, the

only in terms of physical quantities. As another example, standard costs greatly

simplify the operation of a process cost system: the standard costs represent the

costs per equivalent unit (i.e., these costs do not have to be calculated

separately using FIFO or the weighted-average method).

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–28

2. The setting of physical standards such as materials quantities, labor hours, machine

time, and set-up time generally requires information about materials, laborers,

equipment specifications, production procedures, and work flow; this information is

generated from studies conducted by technical personnel and/or from the production

3. a. Because cash-maximization is important for a product classified as a cash cow,

efficiency of operations is essential. Standard costs provide targets for monitoring

costs and identifying inefficiencies so that such problems can be corrected.

Because a cash cow is a slow-growing established product, costs should be fairly

predictable and easy to track.

b. Because a product classified as a question mark is facing strong competition, the

ability to control product costs may be the difference between success and

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–29

14–34 (Continued)

4. In an advanced manufacturing environment, characterized by the increased use of

technology in the manufacturing process and the existence of world-class

competitors, several important criticisms of standard cost systems have been raised

in the literature, including:

▪ The use of such standards, as defined and used conventionally, does not

motivate continuous improvement (Kaizen), which could put the organization at a

competitive disadvantage.

▪ Conventional standard cost systems focus too much on direct labor, which for

▪ Many highly-automated manufacturing processes, based on advanced

manufacturing technologies, are highly reliable and consistent; in this case, the

incremental information to management from standard-cost variances can be

small.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–30

14–35 Determining Standard Direct Materials Cost (10-15 minutes)

Standard direct material cost per bag of Insect-Be-Gone

Total direct materials per unit of output = 60 lbs.

Divided by: Proportion of direct materials inputs remaining

in one unit of finished product = (1 − evaporation rate) = 75%

Total standard quantity of DM inputs/unit of output 80 lbs.

Purchase price per pound × $2.50/lb.