Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-1

Chapter 20

Management Compensation, Business Analysis, and Business

Valuation

Teaching Notes for Cases

20-1. Midwest Petro-Chemical Company: Evaluation of a Firm; Strategy

Adapted from teaching note provided by the case authors, David A. Kunz and Keith A. Russell

1. The case does not provide much information about the competitive environment for the firm, but we

know this is a commodity business, and the nature of the competition is therefore most likely to be cost

leadership. Appropriate compensation plans would be tied directly to managers’ ability to manage costs.

2. Analysis of company performance using ratio and industry norms as a benchmark.

Ratio/2013 Value Line Midwest

Profit margin 7.5% 2.4% ($2,315/$95,962)

Return on Assets 15.0% 5.3% ($2,315/$44,006)

(% earned total capital)

Return on Equity 17.5% 12.4% ($2,315/$18,657)

(% earned net worth)

Price Earning Ratio 18.5 7.3 ($22.50/$3.08)

Price to Book Value — .38 ($22.50/$58.74)

Operating Margin 17.0% 4.4% ($4,221/$95,962)

Income Tax Rate 35.5% 30.0% ($992/$3,307)

Per cent (%) Retained

to Common Equity 12.0% 85.0% ($16,698/$19,702)

Clearly, Midwest Petro-Chemical is a weak firm relative to industry norms, based on financial ratio

analysis.

Strengths of ratio analysis:

a. Provides an excellent historical profile of a firm.

b. Comparative information is readily available for public firms.

Weaknesses of ratio analysis:

a. Ratio analysis is an art; users have to make important judgments.

b. As firms diversify, become conglomerates, and/or multi-national, specific

differentiated.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-2

3. Why did ratio analysis serve as an effective tool for Tom Williams?

As a banker, Williams was more concerned about loan repayment ability than about value.

4. Discuss each valuation method. What are strengths and weaknesses of each? What difficulties are

encountered when applying each method?

a. Asset-based or market value: The firm’s value can be determined by valuing the assets.

Three approaches to this method are;

i.) Modified book value⎯adjusts book value to show differences between historical

Strengths of the asset method: Best used to value firms in natural resources or the securities

industry.

Weaknesses of the asset method: Not a popular method; techniques do not consider firm as a

going concern; historical or book value may bear little, if any, relationship to market value.

b. Market Comparison: Uses market values for similar forms to determine value.

c. Discounted cash flow: This method assumes that the value of a firm is a direct function of

future cash flows from the firm’s operations. A discount rate, sometimes stated as the required rate of

return, is the most important part, albeit subjective, of this method. The discount rate is viewed as the

opportunity cost of funds by the investor. The rate typically contains two components:

1. a risk-free element equal to the rate earned on a short-term government instrument

d. Capitalization of earnings: Based on the value of historical or future earnings divided by a

capitalization rate.

Historic earnings: An average of the firm’s net incomes is divided by the capitalization rate. If

there is a discernible earnings trend, let’s say earnings are increasing each year, greater emphasis is placed

on most recent earnings.

Projected earnings: Project future earnings, three to five years out; average these earnings, and

again, divide by the capitalization rate.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-3

The capitalization rate is determined by the risk associated with the firm’s earnings and the

growth rate of the projected earnings. As a rule of thumb, the capitalization rate is based on the following:

Strengths: Used by knowledgeable investors; solid method for evaluating a low-risk firm.

Weaknesses: Capitalization rate determination is subjective (estimated); the method may be

somewhat difficult to understand.

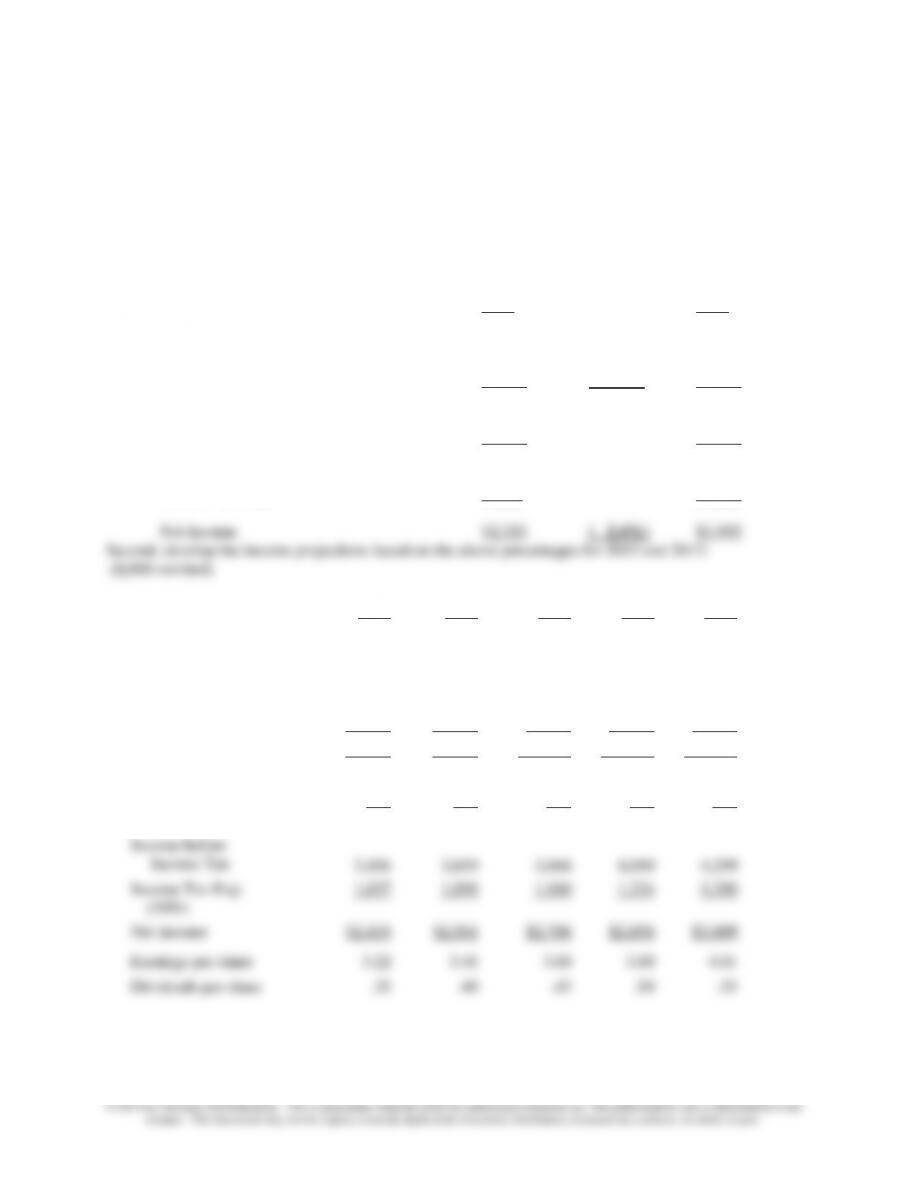

5. Develop values for Midwest’s Petro–Chemical’s stock using the methods discussed in part 4.

A. Asset-based or market value (000s omitted)

Exhibit One: Appraisal Value (Replacement) for land,

plant, property, and equipment $24,335

B. Market Comparison:

Year Earnings per share

2013 $3.08

2012 $2.66

2011 $1.08

2010 $1.15

$7.97/ 4 years = $1.99 x 16* = $31.84

* sales price x earnings for Western Solvents (given in case)

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-4

C: Discounted Cash Flow

First, determine the cost of sales and income as a percent of sales as a basis for projecting income

for 1996-2000.

Statement of Income

for years ending December 31

($, 000s omitted)

2013 2012

Net Sales $95,652 (100%) $92,333

Cost and Expenses

Cost of Sales 77,719 (81.2%) 74,882

Selling G & A 13,712 (14.4%) 13,388

Total cost & Exp 91,431 (95.6%) 88,270

Operating Income 4,221 ( 4.4%) 4,063

Interest Expense 914 1,214

Income before Income Tax 3,307 2,849

Income Tax Exp. 992 854

2014

2015

2016

2017

2018

Sales

Cost of Sales

$99,000

$102,466

$106,050

$109,764

$113,605

Costs & Expenses

80,388

83,202

86,113

89,128

92,247

Selling G & A

14,256

14,755

15,271

15,806

16,359

Total Cost & Exp

94,644

97,957

101,384

104,934

108,606

Operating Income

4,356

4,509

4,666

4,830

4,999

Interest Expense

900

850

800

750

700

Income before

Income Tax

3,456

3,659

3,866

4,080

4,299

Income Tax Exp.

(30%)

1,037

1,098

1,160

1,224

1,290

Net Income

$2,419

$2,561

$2,706

$2,856

$3,009

Earnings per share

3.22

3.41

3.60

3.80

4.01

Dividends per share

.35

.40

.45

.50

.55

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-5

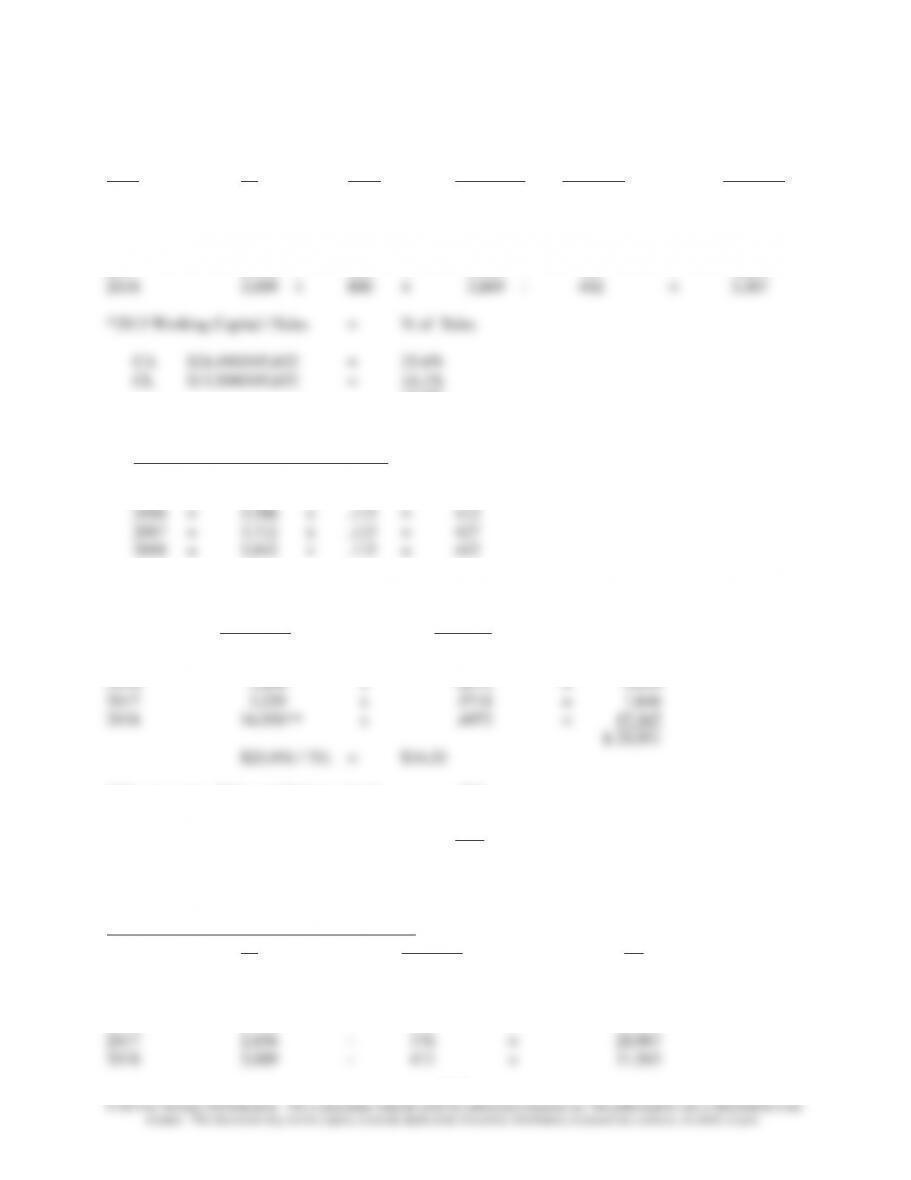

Third, develop Cash Flow Projections:

Cash Flow WC Cash Cash

Year NI Depr In Flow Out* Flow Net

2014 $2,419 + $800 = $ 3,219 – $385 = $2,834

2015 2,561 + 800 = 3,361 – 398 = 2,963

2016 2,706 + 800 = 3,506 – 412 = 3,094

2017 2,856 + 800 = 3,656 – 427 = 3,229

11.5%

Supporting data for developing the cash flow projections:

WC Cash Flow Out: Changes in Sales

2014 = 3,348 x .115 = 385

2015 = 3,465 x .115 = 398

Fourth, develop the valuation based on discounted cash flow:

Present Value

Cash Flow @ 15%*

2014 $2,834 x .8696 = $2,464

2015 2,963 x .7561 = 2,240

*Discount rate: Debt cost (balance sheet) .095

+ Premium (equity) .030

+ Premium (small firm) .025

.150

** Cash Flow plus stockholder equity ($,367 + 31,563)

Supporting data for the above:

Changes in Stockholder Equity (000s omitted):

NI Dividend SE

2013 $ $ $ 19,702

2014 2,419 – 263 = 21,858

2015 2,561 – 300 = 24,119

2016 2,706 – 338 = 26,487

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-6

Dividends (rounded to nearest 000s):

2014 .35 x $751,000 = $ 263,000

2015 .40 x 751,000 = 300,000

2016 .45 x 751,000 = 338,000

2017 .50 x 751,000 = 376,000

2018 .55 x 751,000 = 413,000

D. Capitalization of Earnings (000s omitted)

Net Income Begin SE* Return on Equity

2013 $ 2,315 / $17,612 = 13.1%

2014 1,995 / 15,805 = 12.6%

* Year Begin SE NI – Dividends

2013 $19,702

2012 17,612 2,315 – 225 ($.30 x 751)

2011 15,805 1,995 – 188

2010 14,446 809 – 165

2009 15,161 865 – 150

Historic EPS

2013 – $3.08

2012 – 2.66

2011 – 1.08

2010 – 1.15

$7.97 / 4 = $1.99

$1.99 / .0925 = $21.51

Projected EPS

2014 – $ 3.22

2015 – 3.41

2016 – 3.60

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-7

6. Based on your previous answers, develop a fair-market value for Midwest’s common stock.

Use an average for each of the values produced in part 5 above:

A. Asset-based: $ 32.51

B. Market comparison: $ 31.84

C. Discounted cash flow: $ 34.55

7. Have Frank Armstrong draft a response to Georgia Chemical in Atlanta covering the following

points:

• The Board’s surprise at the purchase inquiry since Midwest has not made public an interest to

sell the firm.

• On behalf of the Board, Armstrong should offer to meet with Georgia Chemical officers to

by the Board and provide time for reflection by Fletcher.

However, it should be noted that Fletcher owns 41.8% of Midwest shares. Also, the pension funds own

10.4% of the shares voted by Allen. These two blocks of stock give Fletcher 52.2% of the voting shares.

Allen will vote the pension fund shares the way Fletcher, his boss, tells him to vote the shares. In short,

Fletcher still controls Midwest. No sale will take place until Fletcher agrees to the sale no matter what

negotiations take place.

8. Once a price is agreed upon by a buyer and a seller, sales terms must be structured.

A. Will the price be paid in cash at closing?

Rarely is the full purchase price paid in cash at closing.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-8

B. Will stock and assets be sold?

Will the sales terms affect the price? YES.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-9

20-2. Evaluating a Firm

This case describes the financial analysis of the W. T. Grant retail firm in the five years prior to

its bankruptcy in 1975. To disguise the case, the actual dates are not used in the text. The year 19X8

represents the actual year 1968, and so on. The case is useful to point out some of the limitations of

financial analysis based primarily on ratio analysis, and to point out the importance of analyzing cash

flows, especially for firms under financial stress, as was W. T Grant in the early 1970s.

The article by Largay and Stickney in the August, 1980 Financial Analysts Journal (“Cash

Flows, Ratio Analysis, and the W.T. Grant Company Bankruptcy”) is the basis for the following

discussion.

“Although they surfaced as a gusher rather than a trickle, the problems that brought the W.T.

Grant Company into bankruptcy and ultimately, liquidation, did not develop overnight. Whereas

traditional ratio analysis of Grant’s financial statements would not have revealed the existence of many of

the company’s problems until 1970 or 1971, careful analysis of the company’s cash flows would have

revealed impending doom as much as a decade before the collapse.”

Grant’s profitability, turnover, and liquidity ratios have trended downward over the 10 years

preceding bankruptcy. But the most striking characteristic of the company during that decade was that it

generated no cash internally. Although working capital provided by operations remained fairly stable

through 1973, this figure (which constitutes net income plus depreciation and is frequently referred to in

the financial press as “cash flow”) can be a very poor indicator of a company’s ability to generate cash.

Through 1973, the W. T. Grant Company’s operations were a net user, rather than provider, of cash.

Grant’s continuing inability to generate cash from operations should have provided investors with

an early signal of problems. Yet as recently as 1973, Grant stock was selling at nearly 20 times earnings.

Investors placed a much higher value on Grant’s prospects than an analysis of the company’s cash flow

from operations would have warranted.” (Largay and Stickney, p51)

The analysis of liquidity and profitability ratios is shown below.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–10

Liquidity

Ratios

Relevance

2008

2009

2010

2011

2012

2013

A/R

Turnover

The average number of times per yr.

net receivables turn into cash.

Indicates effectiveness of credit policy

and collections. Should be compared

to prior years and to industry averages.

3.74

3.57

3.20

3.07

3.23

Current

Ratio

An important measure of liquidity.

Should be compared to prior years,

industry averages and debt restriction,

if any.

3.57

3.30

3.40

3.38

3.50

4.03

Quick

Ratio

(Acid Test)

A measure of liquidity like the current

ratio, but more conservative. Includes

only highly current assets-cash,

marketable securities, and receivables.

2.19

2.03

2.17

2.13

2.22

2.36

Inventory

Turnover

Indicates the average number of times

that inventory is replaced during the

year. Measures inventory management

policies and can give an unsalable

inventory.

3.77

3.80

3.49

3.33

3.22

Cash flow

Ratio

Measures the degree to which cash

flows from operations covers current

liabilities

.29

.20

.14

.11

(.25)

Looks OK overall, but for recent buildup in inventory and receivables; all ratios look stable. The key is to see that the cash flow ratio is falling steadily, with a

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–11

sharp drop in the recent year. This shows that the company is beginning to fund operations through long term debt, a signal of sever liquidity problems. Note

that the conventional liquidity measures do not tend to show this, and disguise the rapid build up in receivables in inventory.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–12

Profitability

Ratios

Relevance

2008

2009

2010

2011

2012

2013

Return on

Total Assets

A measure of management’s

efficiency and effectiveness in using

available assets.

6.46%

6.29%

5.23%

4.02%

3.68%

Return on

Equity

A measure of management’s

effectiveness in providing returns to

shareholders

14.55%

14.65%

13.35%

11.22%

11.45%

Gross

Margin %

An important measure of profitability.

Should be compared to prior years

and to relevant industry data.

Reflects control over costs and

pricing policies.

31.83%

32.47%

32.68%

33.03%

32.43%

31.74%

Earnings per

Share

A measure of profitability available to

shareholders; is often used to asses

the value of the firms stock, using the

“price/earnings ratio”

$2.54

$2.78

$3.05

$2.89

$2.51

$2.79

Profitability is mediocre but stable in the years shown, showing also how the profitability ratios, as well as the liquidity

ratios, disguise the troubles of the firm, which are shown so clearly in the falling cash flow from operations.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–13

20-3. Economic Value Added; Review of Chapter 18; Strategy

(Adapted from teaching note prepared by the case writer, Paul Dierks, Wake Forest University)

1. Economic Value Added, or EVA, is a measure of financial performance that combines the familiar

concept of residual income with principles of modern corporate finance NI⎯specifically, that all capital

has a cost and that earning more than the cost of capital creates value for shareholders. EVA is after-tax

net operating profit (NOPAT) minus cost of capital. If a company’s return on capital exceeds its cost of

capital, it is creating true value for shareholders. Companies consistently generating high EVAs are top

performers that are highly valued by shareholders.

How does EVA stack up against the conventional financial measures of performance? Advocates

of EVA are quick to point out that financial measures based on reported accounting earnings ⎯ earnings

growth, earnings per share, and return ratios calculated on either investment, equity or assets ⎯ are

misleading measures of corporate performance. This is based on their view that accountants place their

primary emphasis on placating the interests of a firm’s lenders in order to provide a conservative

assessment of the firm’s liquidation value. Thus, the quality of reported earnings are diminished by

various financial accounting rules, like incorporating charge-offs of such value-building capital outlays as

R&D and bookkeeping entries that have little to do with recurring cash flow. This group also feels that

many investors may be fooled by accounting “shenanigans,” but investors who matter are not misled.

They know that stock prices are set by a select group of “lead steers” who look through misleading

accounting results to arrive at true values. Although blissfully ignorant of why the price is right, the rest

of the “herd” is well protected by the lead steers’ informed judgments.

One comparison is to the standard accounting return on common equity (ROE), which is

generally understood and easily calculated by dividing net income available to common stockholders by

the amount of accounting equity capital. However, ROE suffers from distortions of accounting earnings

by, among other things, expensing R&D, selecting LIFO or FIFO for inventory costing, recording

acquisitions as a purchase or a pooling, and burying recurring cash flows generated from operations in

reserves because of accrual accounting methods.

Also, ROE reacts to changes in the debt-to-equity mix a company employs and in the rate of

interest it pays on its debts, making it difficult to determine if ROE rises or falls for operating or financial

reasons without examining the return on assets and the firm’s debt–to-equity ratio. With ROE as its goal,

management may be tempted to accept substandard projects that happen to be financed with debt and pass

by very good ones that are financed with equity. To avoid such situations, managers shouldn’t associate

sources of funds with the uses of those funds. Such association distorts the desirability of undertaking a

project by mixing operating and financing decisions. Instead, all projects should be thought of as being

financed with a target blend of debt and equity no matter how they might indeed be financed. Moreover,

by focusing just on ROE, managers may pass up good (wealth creating) projects that are safer than the

average assets of the firm because the return on the project would lower the firm’s ROE. Similarly,

managers may take on bad (wealth reducing) projects that are riskier than the average asset of the firm

because the project’s return increases the firm’s ROE. It should be kept in mind that by focusing on ROE,

the manager ignores the risk associated with a specific project and hence the appropriate return needed for

that investment.

An alternative measure of performance is return on assets (ROA), but it too ignores the cost of

capital, which can lead a firm to make decisions that reduce economic value. For example, IBM, in its

most profitable year, had a return on assets that was over 11 %, but its cost of capital was almost 13 %.

Assuming their cost of capital remains at 13 %, accepting projects with risks similar to existing assets, but

with a return below 13 %, reduces shareholder value.

Another comparison to make is against earnings per share (EPS). In contrast to EVA, EPS tells

little about the cost of generating those profits. Since EPS is directly influenced by the amount of earnings

relative to the number of shares outstanding, financing new investments through debt capital can increase

EPS. Large or rapid earnings growth can be manufactured by pouring capital into riskier projects; earning

an adequate rate of return relative to risk is far more important than growing rapidly. Thus, at best, EPS

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–14

measures only the quantity of earnings, but the quality of earnings reflected in the price-to-earnings

multiple also matters.

Calculating EVA

In The Quest for Value (Harper Collins Publishers, 1991), G. Bennett Stewart calculates a firm’s

EVA in two ways: an Operating Approach, and a Financing Approach. The Financing Approach builds

up to the rate of return on capital from the standard return on equity in three steps: eliminating financial

leverage, eliminating financing distortions, and eliminating accounting distortions. As a result of the first

two steps, NOPAT is a sum of the returns attributable to all providers of funds to the company, and the

NOPAT return is completely unaffected by the financial composition of capital. What matters is simply

the productivity of capital employed in the business. The financial form in which the capital has been

obtained does not matter. Only the financial approach is presented here; for the development of the

operating approach, consult Stewart’s text.

Before developing the calculations for EVA it is important to first cover the concepts of the

equity equivalent adjustments, or EE’s.

Understanding / Use of Equity Equivalents

Equity equivalents, or ‘EE’s’, per Bennett Stewart’s book, are adjustments that turn a firm’s

accounting book value into “economic book value,” which is a truer measure of the cash that investors

have put at risk in the firm and upon which they expect to accrue some returns. In this way, capital-related

items are turned into a more accurate measure of capital that better reflects the financial base investors

expect to accrue their returns on. Also, revenue- and expense-related equity equivalent adjustments are

included in a NOPAT that is a more realistic measure of the actual cash yield generated for investors from

recurring business activities.

Stewart has identified a total of 164 equity equivalent reserve adjustments; however, only about

20 to 25 have to be addressed in detail, and only a portion of these may actually be made in practice. In

our published rankings and illustrations we have chosen to make only a handful of such adjustments in

the calculation of EVA ⎯ typically those which can be made with information contained in the

Compustat database and easily explained to the general business reader. They recommend making an

adjustment only in cases that pass four tests:

1.) Is it likely to have a material impact on EVA?

2.) Can the managers influence the outcome?

3.) Can the operating people readily grasp it?

4.) Is the required information relatively easy to track and derive?

R&D expenditures provide a good example of an equity equivalent adjustment. Under accounting

conventions, outlays for R&D are charged off to the income statement in the period when they are

incurred. These immediate charge-offs as operating expenses say there is no future value to be derived

from R&D. Thus, the firm’s profits are reduced and its capital is undervalued. For EVA purposes, all

outlays over the life of successful R&D projects should be removed from the income statement, be

capitalized into the balance sheet and amortized against earnings over the period benefiting from the

successful R&D efforts. In calculating EVA, R&D is seen as an investment and amounts spent for it

must be included in a firm’s capital base to accurately reflect the amount of capital employed. Only the

portion of R&D that no longer has future value should be charged to the income statement in order to

properly reflect the costs and profit of a period. The portion of R&D expenditures that has future value

should appear as an asset. These equity equivalent adjustments are made in calculating EVA.

The following list of equity equivalents and their effect on capital and NOPAT is taken from

Stewart’s book. The asterisked items are equity equivalents in the OSI case. They are described further in

the paragraphs after the list.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–15

Add to Capital: Equity Equivalents

Deferred income tax reserve*

LIFO reserve*

Cumulative goodwill amortization*

Unrecorded goodwill

(Net) capitalized intangibles

Full-cost reserve

Cumulative unusual loss (Gain) after tax

Other reserves, such as:

Bad debt reserve Inventory obsolescence reserve

Warranty reserve Deferred income reserve

Add to NOPAT: Increase in Equity Equivalents

Increase in deferred tax reserve*

Increase in LIFO reserve*

Goodwill amortization*

Increase in (net) capitalized intangibles

Increase in full-cost reserve

Unusual loss (gain) after tax

Increase in other reserves

Deferred Income Tax Reserve. Deferred taxes arise from a difference in timing when revenues

and expenses are recognized for financial reporting versus when they are reported for tax purposes. The

difference between the accounting provision for taxes and the tax amount paid is accumulated in the

reserve for deferred income taxes account. If long-term assets that give rise to tax deferrals are

replenished, a company’s deferred tax reserve increases, which constitutes the equivalent of permanent

equity. Adjusting NOPAT for the change in deferred tax reserve results in NOPAT being charged only

with the taxes actually paid instead of the accounting tax provision. This provides a clearer picture of the

true cash-on-cash yield actually being earned in the business. Action(s) to be taken:

Add to Capital: Amount of the deferred tax reserve

Add to (Deduct From) NOPAT: Amount of increase (decrease) in the deferred tax reserve

The LIFO Reserve. In periods of rising prices, firms save taxes by using a LIFO basis of

inventory costing. Under LIFO, recently acquired goods are expensed and the costs of prior periods are

accumulated in inventory, resulting in an understatement of inventory and equity. A LIFO reserve account

captures the difference between the LIFO and FIFO value of the inventory and indicates the extent that

the LIFO inventories are understated in value. Adding the LIFO reserve to capital as an equity equivalent

adjustment converts inventories from a LIFO to a FIFO basis of valuation, which is a better

approximation of current replacement cost. Also, adjusting NOPAT for the change in the LIFO reserve

brings into earnings the current period effect of unrealized gain attributable to holding inventories that

appreciated in value. Action(s) to be taken:

Add to Capital: Amount of the LIFO reserve

Add to (Deduct From) NOPAT: Amount of increase (decrease) in the LIFO reserve

Changes in the LIFO reserve can also be viewed as a difference between the LIFO and FIFO cost

of goods sold. Including this change in reported profits converts a LIFO cost of goods sold expense to

FIFO, but LIFO‘s tax benefit is retained. The overall effect of treating a LIFO reserve as an equity

equivalent adjustment is to produce a FIFO balance sheet and income statement but preserve the LIFO tax