Chapter 6 – Process Costing

6-16

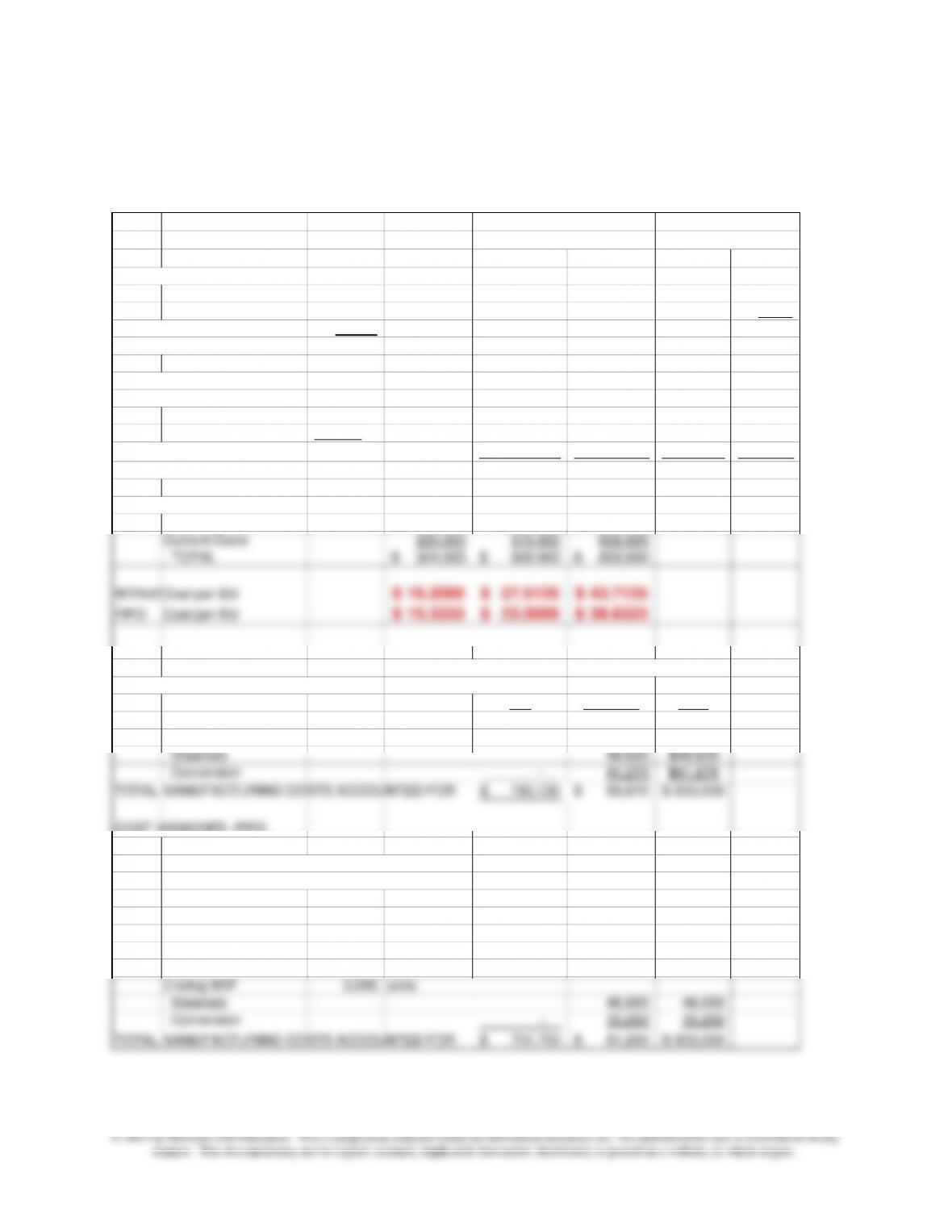

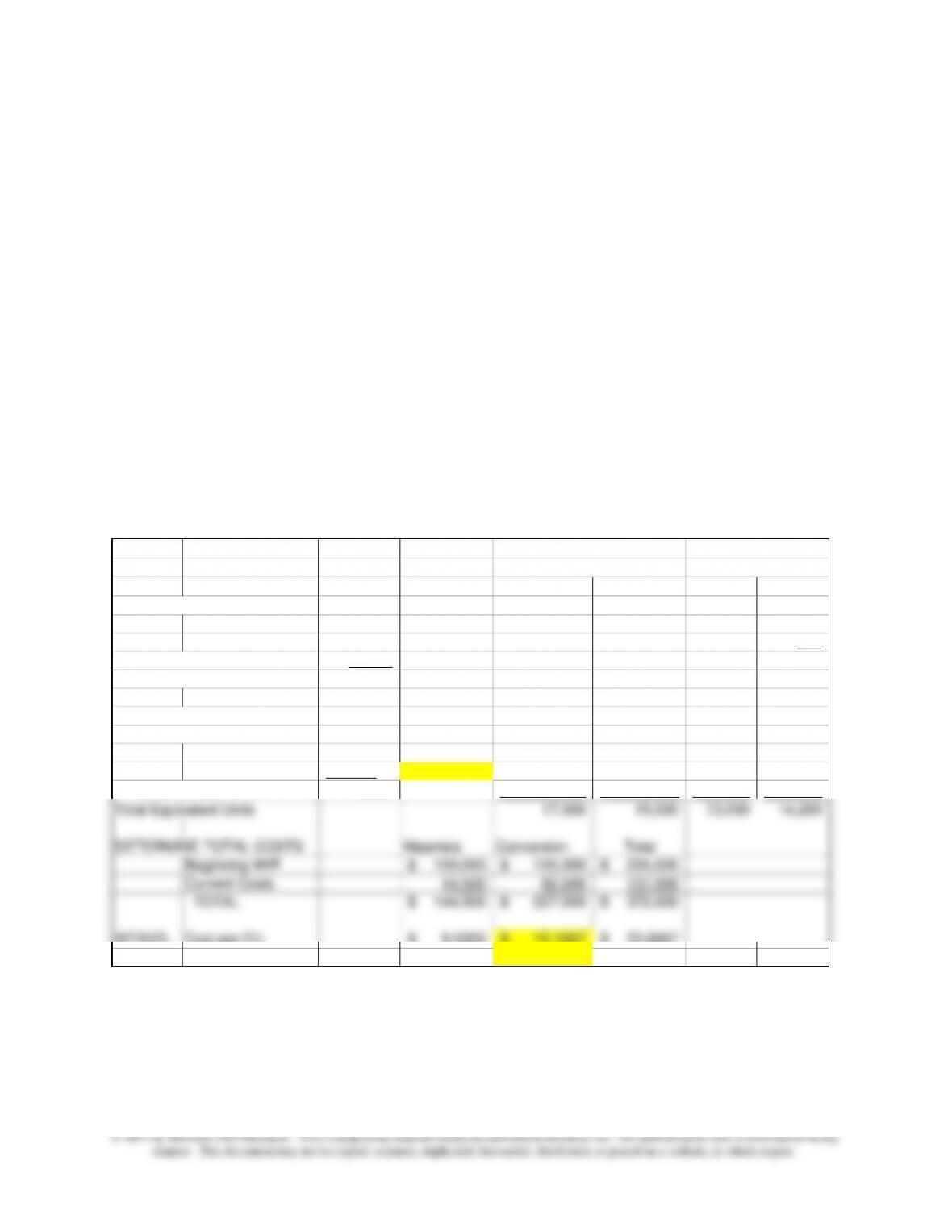

6-37: Weighted Average Method (20 min)

Physical Percentage

Units Completion Materials Conversion Materials

Conversion

Beginning WIP 5,000

Materials 100% 5,000

Conversion 50% 2,500

Units started 15,000

Total to account for 20,000

Units FinIshed 17,000 17,000 17,000 17,000 17,000

Ending WIP 3,000

Materials 100% 3,000 3,000

Conversion –

50% 1,500 1,500

Total accounted for 20,000 – – – –

Total Equivalent Units 20,000 18,500 15,000 16,000

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 94,000$ 133,000$ 227,000$

Current Costs 230,000 376,000 606,000

TOTAL 324,000$ 509,000$ 833,000$

WTAVG

Cost per EU 16.2000$ 27.5135$ 43.7135$

FIFO Cost per EU 15.3333$ 23.5000$ 38.8333$

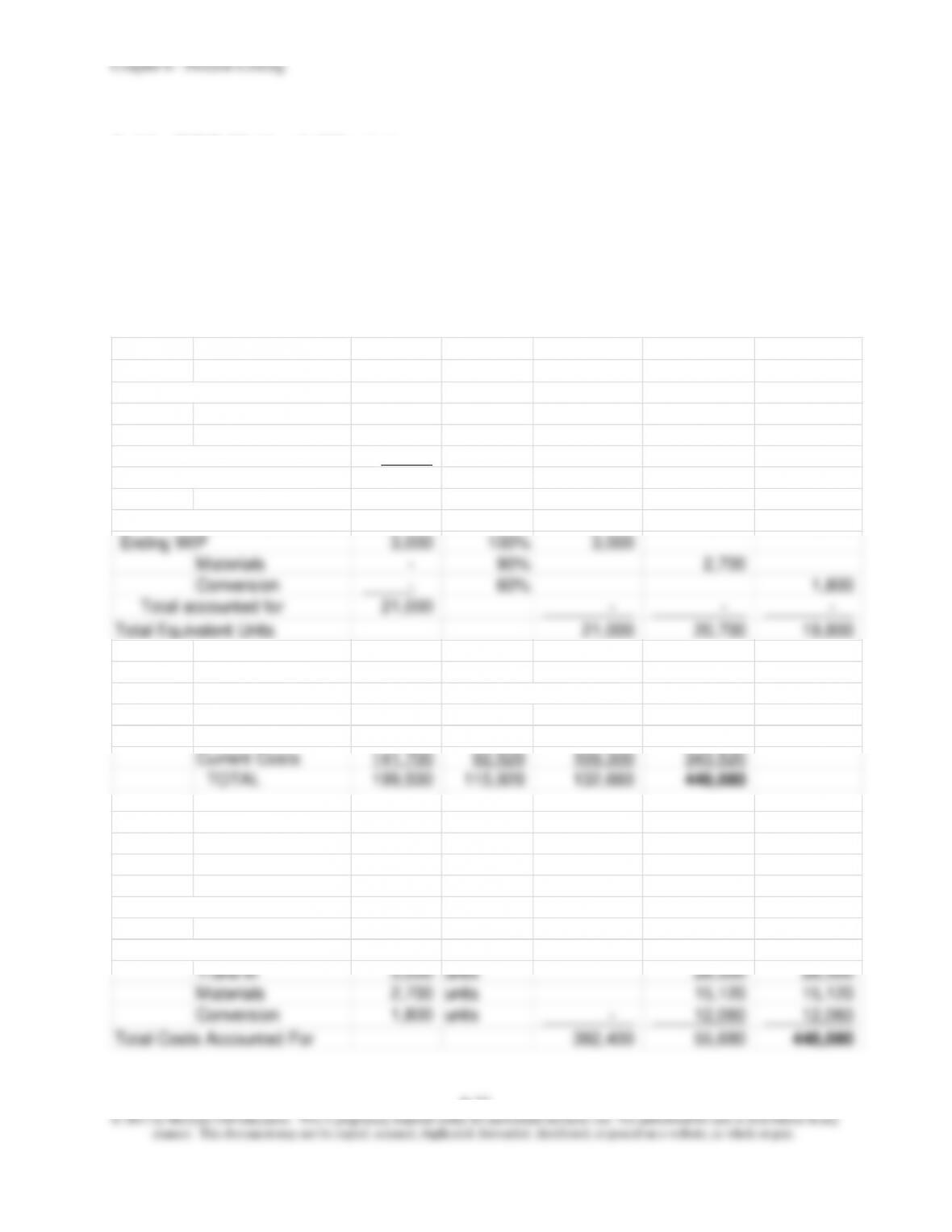

Units Completed

Units in Ending

COST ASSIGNED -WEIGHTED AVERAGE

and Transferred

WIP

Out Inventory Total

COST ASSIGNED -FIFO

Finished Goods 17,000 units

Prior period costs in Beginning WIP 227,000

Current cost to complete Beginning WIP

Materials – Equiv units –

Conversion 2,500 Equiv units 58,750

Units started and finish

12,000 Equiv units 466,000

Ending WIP 3,000 units

Materials 46,000 46,000

Conversion – 35,250 35,250

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 751,750$ 81,250$ 833,000$

Equivalent Units

Equivalent Units

Weighted Average

FIFO

Chapter 6 – Process Costing

6-17

Note: Units finished = units from Beginning WIP completed this period +

units started and finished this period = 5,000 + 12,000 =17,000

6-38 FIFO Method (20 min) — see solution above

6-38 FIFO Method (20 min) — see solution on prior page

6-39 Weighted-Average Method (30-40 min)

1., 2.

Materials X

Materials Y

Conversion

Equivalent Units

87,000

60,000

70,800

Cost per Equiv. Unit

$2.50

$3.75

$6.00

Chapter 6 – Process Costing

6-18

Physical Percentage

Units Completion Material X Material Y Conversion

Beginning WIP 33,000

Material X 100%

Material Y 100%

Conversion 80%

Units started 54,000

Total to account for 87,000

Units Finished 60,000 60,000 60,000 60,000

Ending WIP 27,000

Material X 100% 27,000

Material Y 0% –

Conversion –

40% 10,800

Total accounted for 87,000 – – –

Total Equivalent Units 87,000 60,000 70,800

DETERMINE TOTAL COSTS Material X Material Y Conversion Total

Beginning WIP 64,800$ 89,100$ 119,880$ 273,780$

Current Costs 152,700 135,900

304,920 593,520

TOTAL 217,500$ 225,000$ 424,800$ 867,300$

WTAVG Cost per EU 2.500$ 3.750$ 6.000$ 12.250$

Units Completed

Units in Ending

COST ASSIGNED -WEIGHTED AVERAGE

and Transferred

WIP

Out Inventory Total

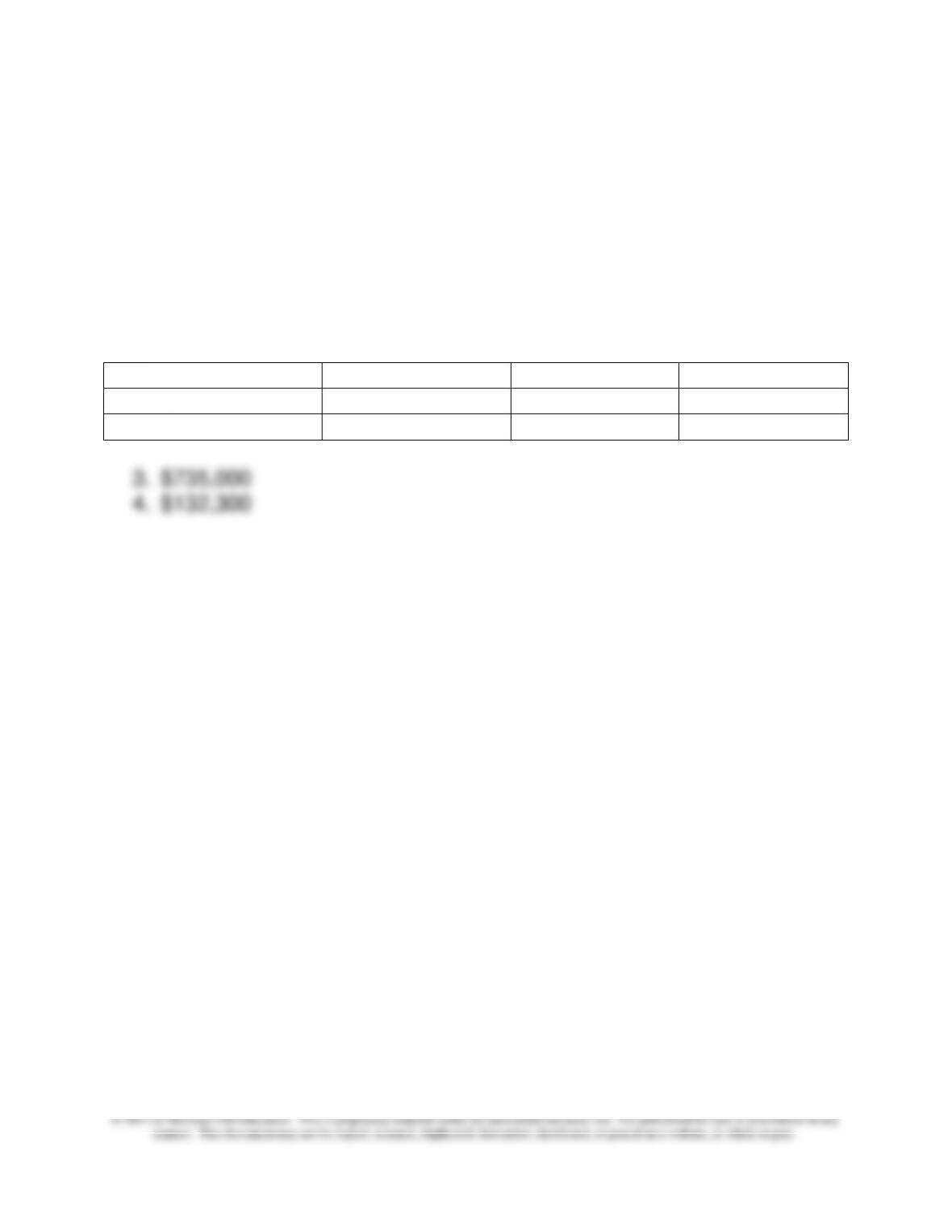

Finished Goods

60,000 units 735,000$ $735,000

Ending WIP

27,000 units

Material X 67,500 $67,500

Material Y – –

Conversion – 64,800 $64,800

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 735,000$ 132,300$ 867,300$

Weighted Average Equivalent Units

6-19

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

6-40 Weighted-Average Method (30 min)

1. Equivalent units:

Direct Materials: 204,000

Conversion: 192,000

2. Cost per equivalent unit:

3. Cost of goods completed and transferred out: ¥ 2,081,636

4. Cost of work-in-process, 10/31: ¥ 190,364

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 40,000

Materials 60%

Conversion 30%

Units started 170,000

Total to account for 210,000

Units Finished 180,000 180,000 180,000

Ending WIP 30,000

Materials 80% 24,000

Conversion –

40% 12,000

Total accounted for 210,000 – –

Total Equivalent Units 204,000 192,000

DETERMINE TOTAL COSTS (all amounts in Yuan)

Materials Conversion Total

Beginning WIP ¥ 57,000 ¥ 45,000 ¥ 102,000$

Current Costs 820,000 1,350,000 2,170,000

TOTAL ¥ 877,000 ¥ 1,395,000 ¥ 2,272,000$

WTAVG Cost per EU ¥ 4.2990 ¥ 7.2656 ¥ 11.5646

Equivalent Units

Weighted Average

Chapter 6 – Process Costing

6-20

6-40 (continued–1)

5. Exchange rate as of March 9, 2012 was $1 US = 6.3109 Yuan, a fall

in the dollar of approximately 7% over the prior three years. The rise

Chapter 6 – Process Costing

6-21

6-41 Weighted-Average Method; Transferred in Units (25 min)

1. Equivalent units

a. Transferred in: 32,000

b. Materials: 27,000

c. Conversion: 29,500

2. Unit costs

a. Transferred-in $6.25

Chapter 6 – Process Costing

6-22

Whole Percent Transferred

Units Completion in Costs Materials Conversion

Beginning WIP 4,000 100%

Materials 0%

Conversion 50%

Units started or Trans-in 28,000 100%

Total to account for 32,000

Units Finshed or Trans-out 27,000 100% 27,000 27,000 27,000

Ending WIP 5,000 100% 5,000

Materials – 0% –

Conversion –

50% 2,500

Total accounted for 32,000 – – –

Total Equivalent Units 32,000 27,000 29,500

COST ADDED

Trans-in Materials Conversion Total

Beginning WIP 50,000$ –$ 30,000$ 80,000$

Current Costs 150,000 60,000 110,000 320,000

TOTAL 200,000$ 60,000$ 140,000$ 400,000$

WTAVG Cost per EU 6.2500$ 2.2222$ 4.7458$ 13.2180$

Completed Ending Work

% Trans-out in Process Total

Finished Goods

27,000 units 356,886$ 356,886$

Ending Work-in-process

5,000 units

Trans-in 5,000 units 31,250$ 31,250

Materials – units – –

Conversion 2,500 units – 11,864 11,864

Total Costs Accounted For 356,886$ 43,114$ 400,000$

—–This Dept—–

Chapter 6 – Process Costing

6-23

6-42 Reconditioning Service; Weighted-Average (20 min)

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 150

Materials 50%

Conversion 30%

Units started 1,200

Total to account for 1,350

Units Finished 1,050 1,050 1,050

Ending WIP 300

Materials 30% 90

Conversion –

20% 60

Total accounted for 1,350 – –

Total Equivalent Units 1,140 1,110

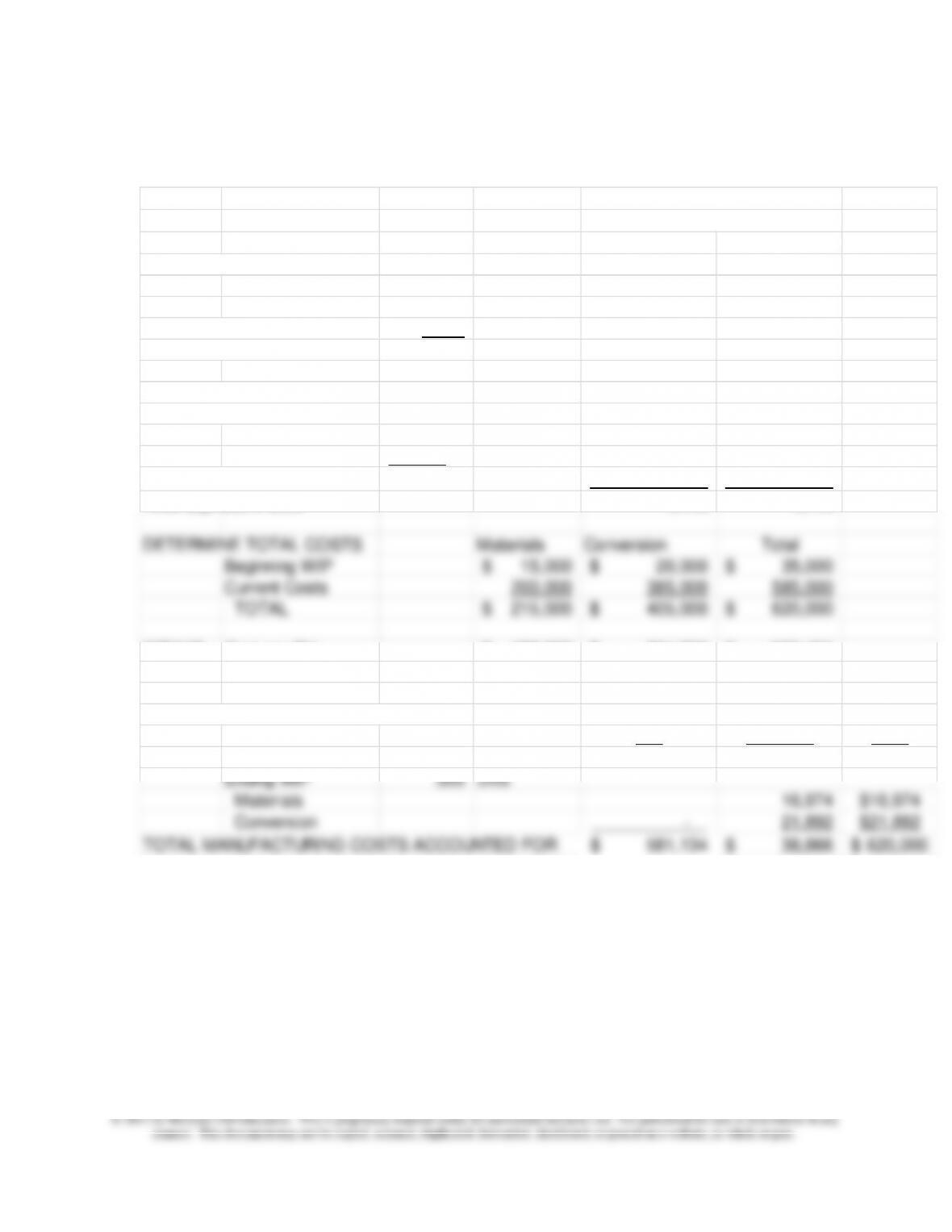

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 15,000$ 20,000$ 35,000$

Current Costs 200,000 385,000 585,000

TOTAL 215,000$ 405,000$ 620,000$

WTAVG Cost per EU 188.596$ 364.865$ 553.461$

Units Completed Units in Ending

COST ASSIGNED –WEIGHTED AVERAGE and Transferred WIP

Out Inventory Total

Finished Goods

1,050 units 581,134$ $581,134

Ending WIP

300 units

Materials 16,974 $16,974

Conversion – 21,892 $21,892

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 581,134$ 38,866$ 620,000$

Equivalent Units

Weighted Average

Chapter 6 – Process Costing

6-24

Problem 6-42 (continued-1)

2. The information in the cost report shows two relevant items of

information regarding planning for the coming month’s work. First,

note there has been an increase in WIP during November, a month in

which there were fewer units in process (1,350 units) . December’s

work will require 1,500 + 300 = 1,800 units in process, somewhat

larger than November’s requirement. GWI should be concerned

about its capacity and ability to meet the December orders on a

Chapter 6 – Process Costing

6-25

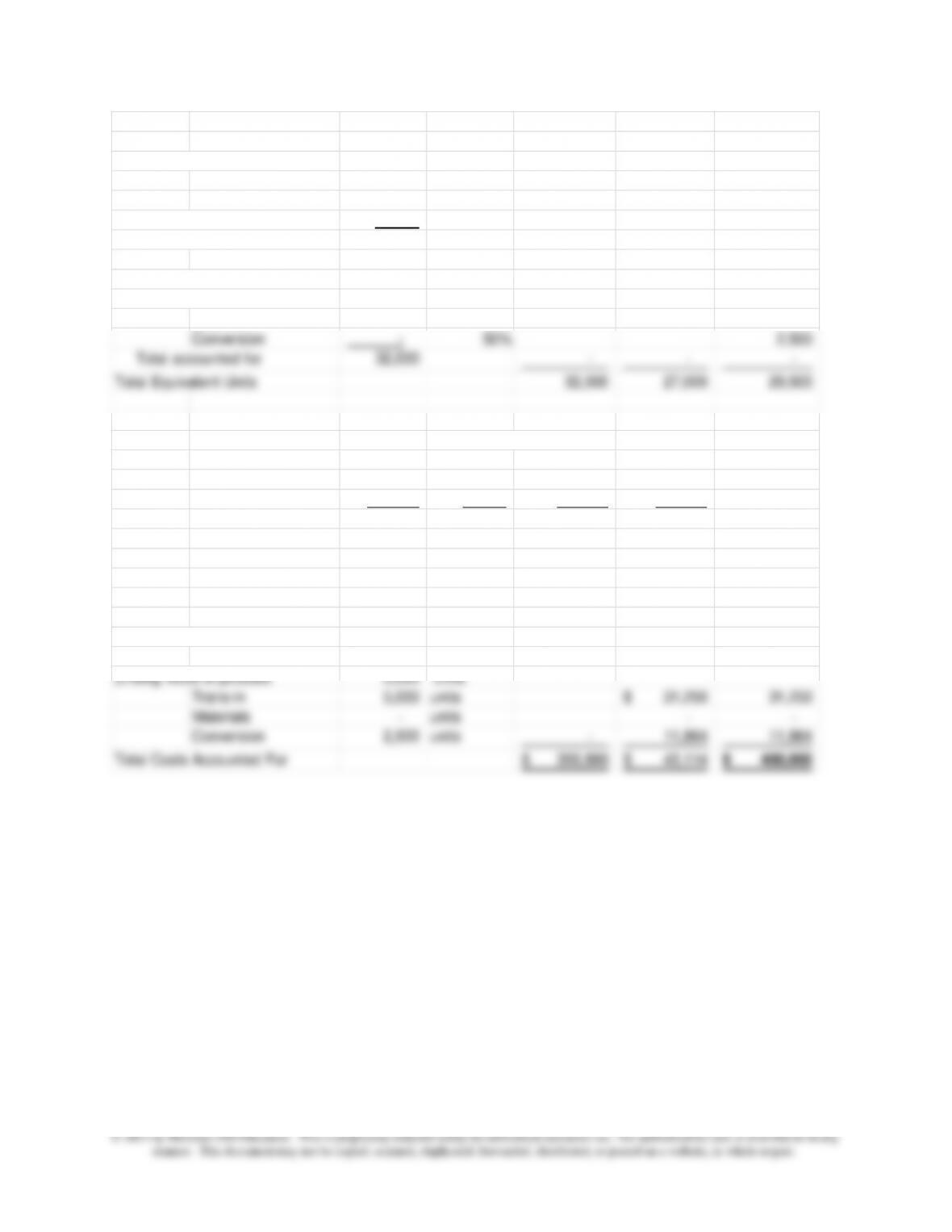

6-43 Weighted Average Method (25 min)

1.,2.,3.

Physical Percentage

Units Completion Materials Conversion Materials Conversion

Beginning WIP 4,000

Materials 100% 4,000

Conversion 20% 800

Units started 13,000

Total to account for 17,000

Units Finished 12,000 12,000 12,000 12,000 12,000

Ending WIP 5,000

Materials 100% 5,000

Conversion –

40% 2,000

Total accounted for 17,000 – – – –

Total Equivalent Units 17,000 14,000 13,000 13,200

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 100,000$ 135,000$ 235,000$

Current Costs 44,500 92,500 137,000

TOTAL 144,500$ 227,500$ 372,000$

Ending WIP (

5,000 units)

Materials 42,500 $42,500

Conversion – 32,500 $32,500

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 297,000$ 75,000$ 372,000$

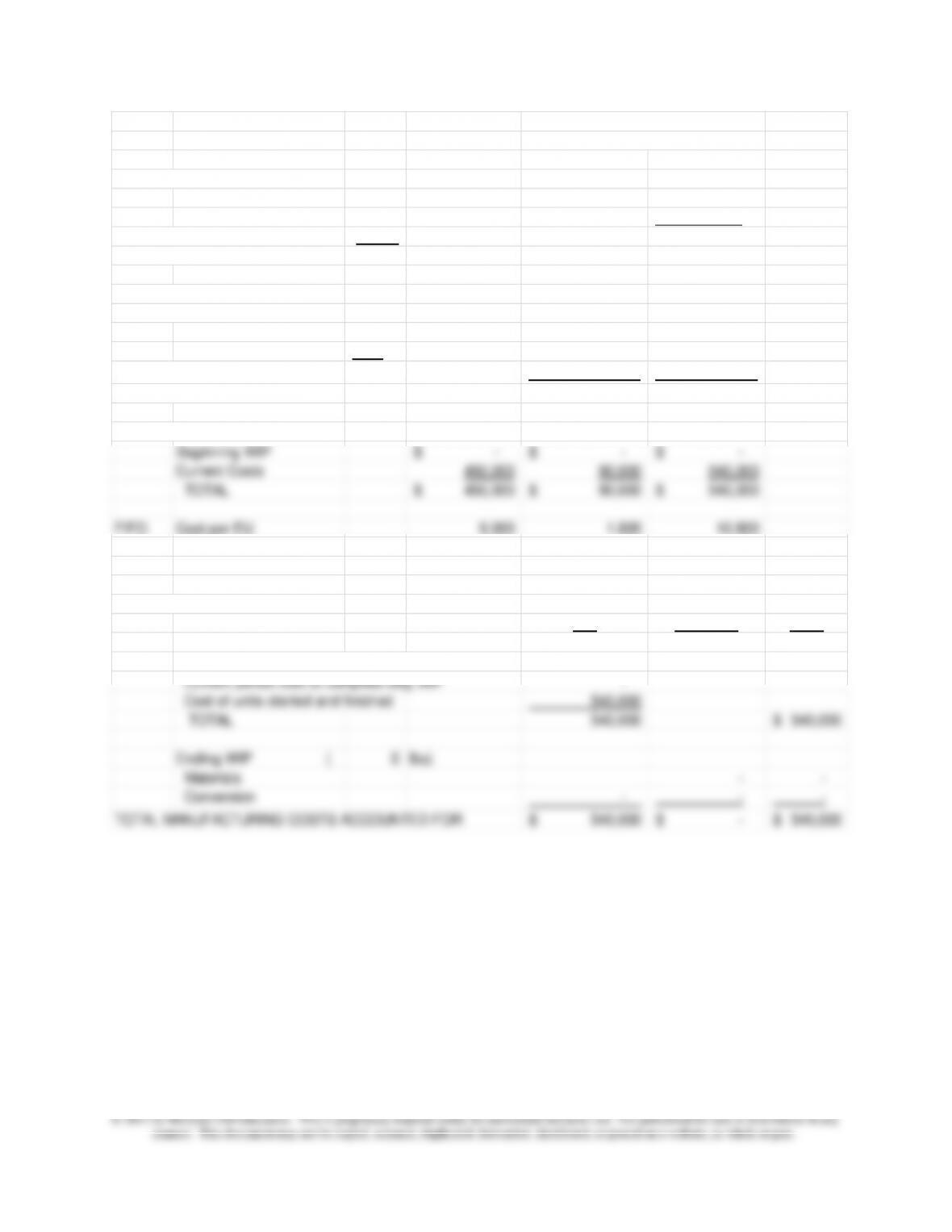

COST ASSIGNED –FIFO

Finished Goods 12,000 units

Prior period costs in Beginning WIP 235,000

Current cost to complete Beginning WIP

Materials – Equiv units –

Ending WIP

Conversion – 14,015 14,015

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 340,869$ 31,131$ 372,000$

Equivalent Units

Equivalent Units

Weighted Average

FIFO

Chapter 6 – Process Costing

6-43 (continued –1)

4. The request is a violation of the controller’s responsibility to prepare

accurate production cost reports. The ethical principles of integrity and

objectivity require the controller to use the best available estimate of

percentage completion.

Since there is a high level of ending WIP, the change from 40% to 60%

would have a significant effect on equivalent units and cost per equivalent

unit, as shown below

The weighted-average conversion cost per equivalent unit decreases from

$16.25 to $15.1667

Physical Percentage

Units Completion Materials Conversion Materials

Conversion

Beginning WIP 4,000

Materials 100% 4,000

Conversion 20% 800

Units started 13,000

Total to account for 17,000

Units Finished 12,000 12,000 12,000 12,000 12,000

Ending WIP 5,000

Materials 100% 5,000 5,000

Conversion –

60% 3,000 3,000

Total accounted for 17,000 – – – –

Total Equivalent Units 17,000 15,000 13,000 14,200

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 100,000$ 135,000$ 235,000$

Current Costs 44,500 92,500 137,000

TOTAL 144,500$ 227,500$ 372,000$

WTAVG Cost per EU 8.5000$ 15.1667$ 23.6667$

FIFO Cost per EU 3.4231$ 6.5141$ 9.9372$

Equivalent Units

Equivalent Units

Weighted Average

FIFO

6-27

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

6-44 FIFO Method (25 min)

See the solution for 6-43 above for the calculation of cost per equivalent

unit under FIFO.

6-45 Weighted-Average Method; Transferred-In Costs (40-50 min)

1. (all currency figures are in Korean won)

Whole Percent Transferred

Units

Completion

in Costs Materials Conversion

Beginning WIP 6,000 100%

Materials 100%

Conversion 80%

Units started or Trans-in 15,000 100%

Total to account for 21,000

Units Finsihed or Trans-out 18,000 100% 18,000 18,000 18,000

Ending WIP 3,000 100% 3,000

Materials – 90% 2,700

Conversion –

60% 1,800

Total accounted for 21,000 – – –

Total Equivalent Units 21,000 20,700 19,800

COST ADDED

Trans-in Materials Conversion Total

WTAVG Cost per EU 9.500 5.600 6.700 21.800

Completed Ending Work

% Trans-out in Process Total

Finished Goods

18,000 units 392,400 392,400

Ending Work-in–process

Trans-in 3,000 units 28,500 28,500

Materials 2,700 units 15,120 15,120

Conversion 1,800 units – 12,060 12,060

Total Costs Accounted For 392,400 55,680 448,080

——–This Dept-–—–

Chapter 6 – Process Costing

6-28

2. On March 9, 2012 the exchange rate was $1 US = 1,116 South Korean

Won (KRW). The dollar had fallen about 15% from a rate of $1 US =

1,253 KRW three years earlier. These economic cycles that affect

currency exchange rates are important in product costing and business

management, as they affect trade between the countries. With the dollar

falling U.S. exports to South Korean are cheaper in Korea, while imports of

Korean goods are more expensive to the U.S. consumer.

6-46 FIFO Method; Two Departments (60-70 min)

Molding Department

Chapter 6 – Process Costing

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 0

Materials 0% –

Conversion 0% –

Units started (lbs) 50,000

Total to account for 50,000

Units Finished or Trans-out (lbs) 50,000 50,000 50,000

Ending WIP 0

Materials 0%

Conversion –

0%

Total accounted for (lbs) 50,000 – –

Total Equivalent Units 50,000 50,000

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP –$ –$ –$

Current Costs 450,000 90,000 540,000

TOTAL 450,000$ 90,000$ 540,000$

FIFO Cost per EU 9.000 1.800 10.800

Units Completed Units in Ending

COST ASSIGNED – FIFO and Transferred WIP

Out Inventory Total

Finished Goods ( 50,000 lbs)

Prior period costs in Beginning WIP –$

Current period cost to complete Beg WIP –

Cost of units started and finished 540,000

TOTAL 540,000 540,000$

Ending WIP ( 0 lbs)

Materials – –

Conversion – –

–

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 540,000$ –$ 540,000$

FIFO

Equivalent Units

Chapter 6 – Process Costing

6-30

Problem 6-46 (Continued –1)

Finishing Department

Physical Percent Transferred

Units

Completion

in Costs Materials Conversion

Beginning WIP 5,000 100%

Materials 0% –

Conversion 40% 2,000

Units started or Trans-in 50,000 100% 50,000

Total to account for 55,000

Units Finished or Trans-out 53,000 100% – 53,000

Ending WIP 2,000 100%

Materials – 0%

Conversion – 40% 800

Total accounted for 55,000 – – –

Total Equivalent Units 50,000 – 51,800

COST ADDED

Trans-in Materials Conversion Total

Beginning WIP ? – ? 15,000

Current Costs 540,000 – 80,000 620,000

TOTAL 540,000 – 80,000 635,000

FIFO Cost per EU 10.8000 0.0000 1.5444 12.3444

Completed Ending Work

Prior period costs in Beginning WIP 15,000

Current per. cost to complete Beg WIP

Materials 5,000 Equiv units –

Conversion 3,000 Equiv units 4,633

Units started & finished

48,000 Equiv units 592,531

Materials – –

Conversion – 1,236 1,236

TOTAL MANUFACTURING COSTS ACCOUNTED FOR 612,164$ 22,836$ 635,000$

——-This Dept–—–

FIFO

Equivalent Units