Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-16

7-28 (continued -1)

Premium Dept.

Advertising Dept

Sales Dept

Allocation of

Actuarial Dept

$80,000 x .8 =

$64,000

$80,000 x .1 =

$8,000

$80,000 x .1 =

$8,000

Allocation of

Premium Dept

($64,000 +

$15,000) x .25 =

$19,750

($64,000 +

$15,000) x .75 =

$59,250

Add: Initial

Production Dept

Costs

$60,000

$40,000

Total Cost for

Each Production

Department

$87,750

$107,250

3. The Reciprocal Method

Solve the Simultaneous Equations: (S1=actuarial; S2=premium)

S1 = $80,000 + (.2 x S2)

S2 = $15,000 + (.8 x S1)

Advertising

Department

Sales Department

Actuarial Department

cost allocation

$98,810 x .1 = $9,881

$98,810 x .1 = $9,881

Premium Department

cost allocation

$94,048 x .2 =

$18,809.60

$94,048 x .6 =

$56,428.80

Add: Initial Production

Dept. Costs

$60,000

$40,000

Total Cost for Each

Production Dept.

$88,690.60

$106,309.80

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-17

7-29 Departmental Cost Allocation (30 min)

First, find the unknown service rates:

From S1 to P2 = 100% – 10% – 20% = 70%

From S2 to P1 = 100% – 10% – 30% = 60%

1. The Direct Method

Net service to both Production Departments for Service

Department 1: 100% – 10% = 90%

Production Department 1 share: 20%/90% = 2/9

Production Department 2 share: 70%/90% = 7/9

Production department

1

Production department

2

Service department 1

cost allocation

$180,000 x 2/9 =

$40,000

$180,000 x 7/9 =

$140,000

Service department 2

cost allocation

$60,000 x 2/3 =

$40,000

$60,000 x 1/3=

$20,000

Add: Initial

Production Dept.

Costs

$50,000

$120,000

Total Cost for Each

Production Dept.

$130,000

$280,000

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-18

7-29 (continued -1)

2. Step Method

Both service departments serve each other the same percentage of

total service; hence, either can go first. Here, Service Dept 1 goes

first on the basis that it has the highest total cost:

Service Dept 2

Production Dept

1

Production Dept

2

Allocation of

Service Dept 1

$180,000 x .1 =

$18,000

$180,000 x .2 =

$36,000

$180,000 x .7 =

$126,000

Allocation of

Service Dept 2

($60,000 +

$18,000) x 2/3 =

$52,000

($60,000 +

$18,000) x 1/3 =

$26,000

Add: Initial

Production Dept

Costs

$50,000

$120,000

Total Cost for

Each Production

Department

$138,000

$272,000

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-19

7-29 (continued -2)

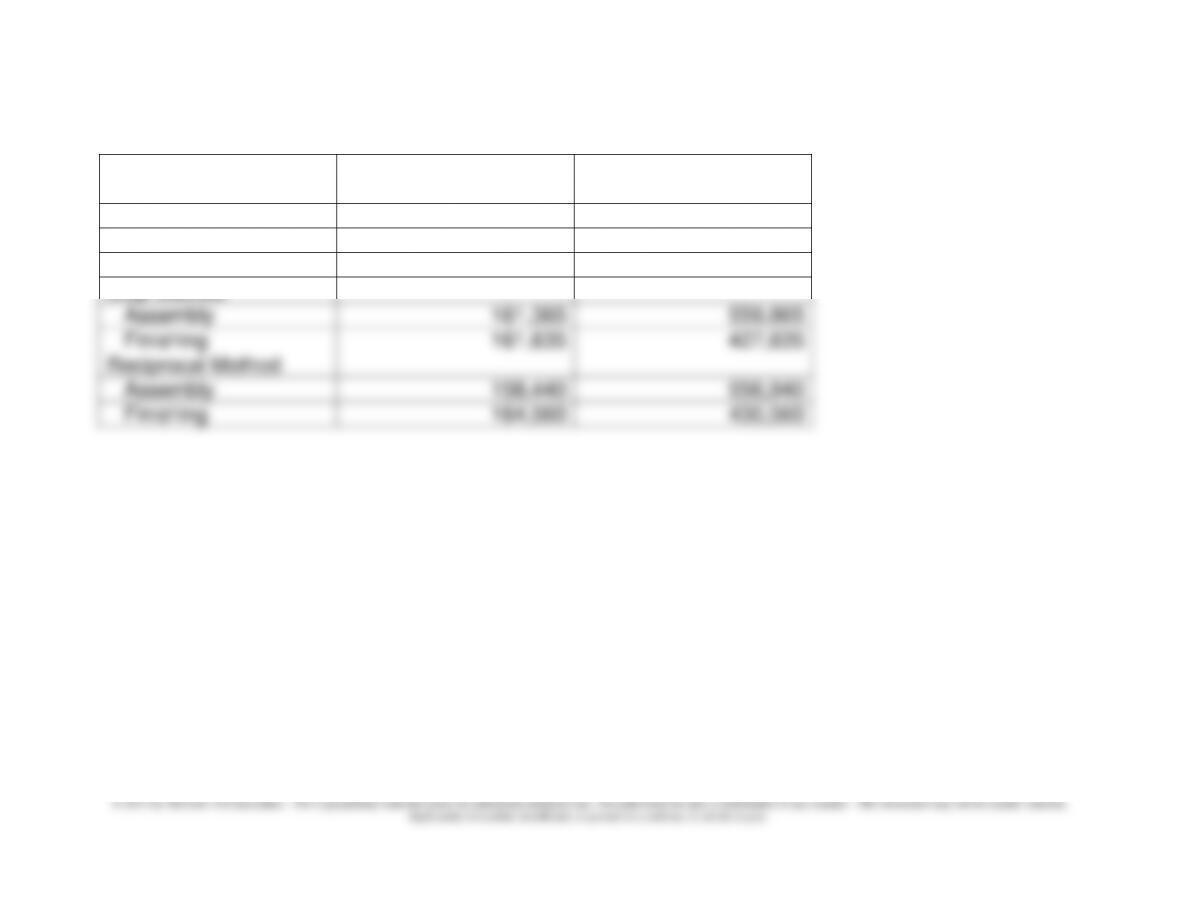

3. The Reciprocal Method

Solve the Simultaneous Equations:

S1 = $180,000 + (.1 x S2)

S2 = $60,000 + (.1 x S1)

S2 = $78,788

Production Department 1

Production Department 2

Service Dept 1

cost allocation

$187,879 x .2 =

$37,576

$187,879 x .7 = $131,515

Service Dept 2

cost allocation

$78,788 x .6 = $47,273

$78,788 x .3 = $23,636

Add: Initial

Production Dept.

Costs

$50,000

$120,000

Total Cost for Each

Prod. Dept.

$134,849

$275,151

7-20

7-30 Joint Products;

As the text notes, the physical units method often involves inappropriate

allocation of costs as the physical measure may be unrelated to the

ultimate value of the different joint products. This appears to be true in the

production of the three blood products, as reported by the U.K. National

Blood Authority (NBA). The result is that prices, when based on allocated

cost, can vary widely as the volumes of each product vary from time to time

due to changes in supply or demand. The NBA’s solution was to charge

all joint costs to the red cells product (a product used primarily in surgery);

additional processing costs are involved, as in this case. So these

methods deserve consideration.

Postscript: a Chartered Institute of Management Accountant’s (CIMA; a

U.K.-based professional organization) study proposed that both the current

and prior allocation methods be replaced with one based on the usefulness

of the three blood products, as assessed by hematologists. This approach

appears to be closer to the net realizable method we have discussed in the

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-21

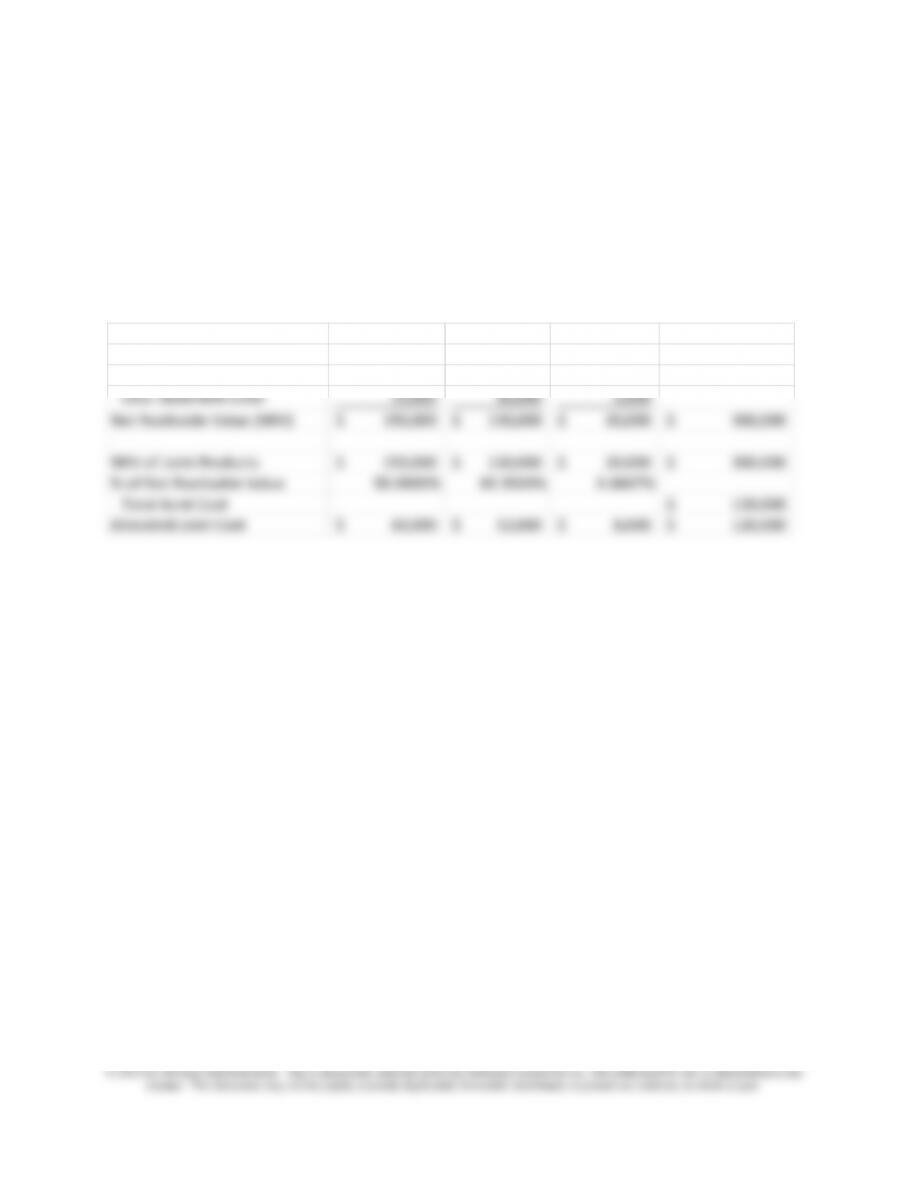

7-31 Joint Products (10 min)

The allocation for the net realizable value method is shown below. Note

however, that Product T has a very small sales value relative to the two

other products. Should it more properly have been treated as a by-

product?

Product M Product N Product T

Units Produced and Sold 10,000 4,000 5,000

Sales Value of Production 160,000$ 140,000$ 25,000$

Less: Separable costs 10,000 10,000 5,000

Net Realizable Value (NRV) 150,000$ 130,000$ 20,000$ 300,000$

NRV of Joint Products 150,000$ 130,000$ 20,000$ 300,000$

% of Net Realizable Value 50.0000% 43.3333% 6.6667%

Total Joint Cost 120,000$

Allocated Joint Cost 60,000$ 52,000$ 8,000$ 120,000$

7-22

7-32 Joint Products (20 min)

A B

Gallons produced 5,000 1,000

Sales price at Split-off 2.00$ 30.00$

Sales Value at Split-off 10,000$ 30,000$ 40,000$

% of Sales Vale at Split Off 25.00% 75.00%

Total Joint Cost 5,600$

Allocated Joint Cost 1,400$ 4,200$ 5,600$

Separable cost per gallon – 2.50

Total Separable Cost – 2,500

Total Product Cost 1,400$ 6,700$

Note, since the sales value at split off for product A is significantly less than

for product B, the company should consider using by-product costing for

this product.

7-23

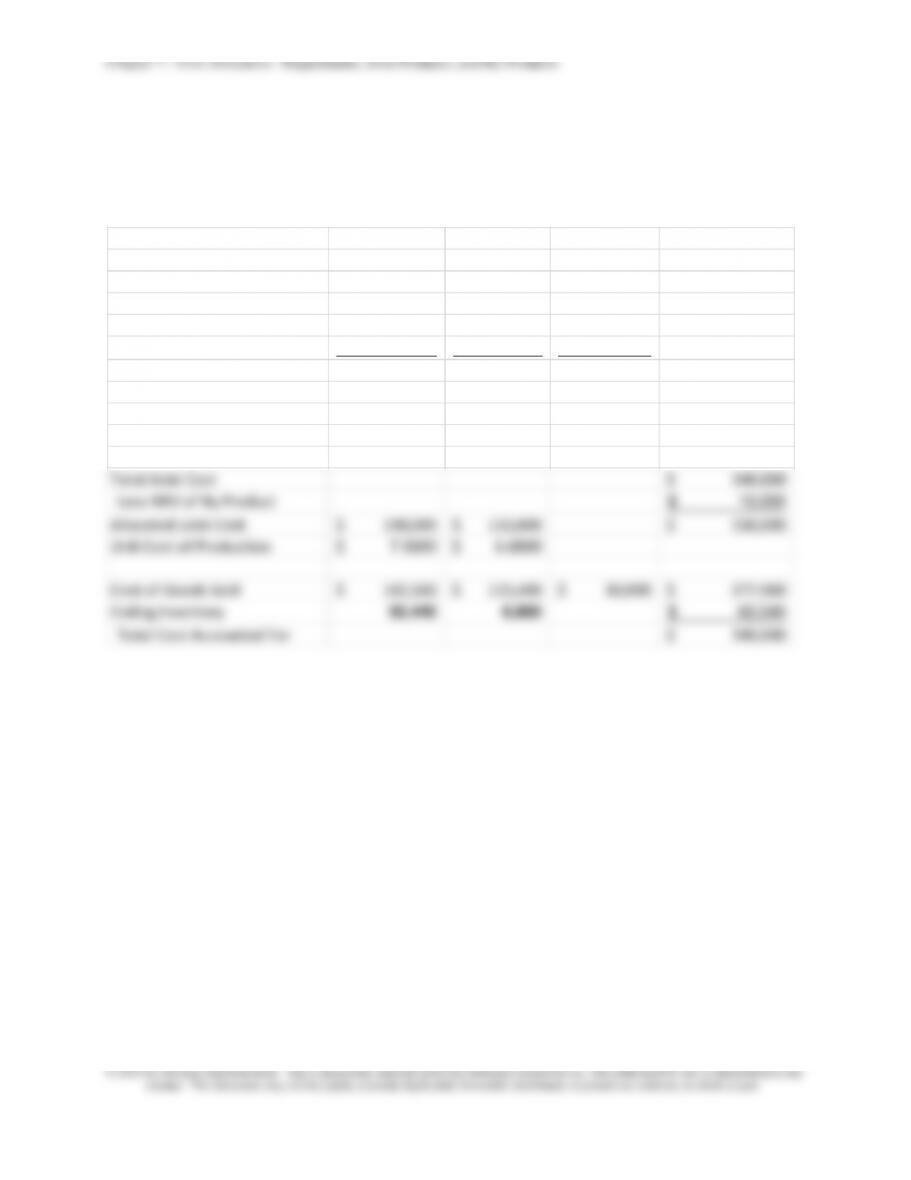

7-33 Joint Product Costing; By-Products (Appendix) (25 min)

1. Ending inventory of Product A $55,440

2. Ending inventory of Product B$ 6,600

Product A Product B Product C Total

Unists Sold 18,000 19,000 10,000

Units Produced 25,000 20,000 10,000

Sales Price 30$ 25$ 1$

Sales Value of Production 750,000$ 500,000$ 10,000$

Less: Separable costs – – –

Net Realizable Value (NRV) 750,000$ 500,000$ 10,000$ 1,260,000$

NRV of Joint Products 750,000$ 500,000$ 1,250,000$

% of Net Realizable Value 60% 40%

Total Joint Cost 340,000$

Less NRV of By Product 10,000$

Allocated Joint Cost 198,000$ 132,000$ 330,000$

Unit Cost of Production 7.9200$ 6.6000$

Cost of Goods Sold 142,560$ 125,400$ 10,000$ 277,960$

Ending Inventory 55,440 6,600 62,040$

Total Cost Accounted For 340,000$

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-24

PROBLEMS

7-34 Departmental Cost Allocation; Outsourcing (30 min)

1. Departmental Cost Allocation: Direct Method

Design Programming Dept A Dept B Total

DEPARTMENTAL ALLOCATION BASES

Design – 5,000 1,000 9,000 15,000

percent 0.0% 33.3333% 6.6667% 60.00% 100.00%

Programming 200 200 600 1,000

percent 20.0% 20.0% 60.0% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

70,000$ 50,000$ –$ –$ 120,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Design Service % to producing departments 6.6667% 60.00% 66.667%

Allocation % per the direct method 6.67/66.7=10%; 60/66.7=90% 10.00% 90.00% 100.0%

Allocation amount

7,000$ 63,000$ 70,000$

Programming Service % to producing departments 20% 60% 80.0%

Allocation % per the direct method 20/80=25%; 60/80 = 75% 25.00% 75.00% 100.0%

Allocation amount 12,500 37,500 50,000$

Totals for Production Departments

19,500$ 100,500$ 120,000$

Departments

Service

Production

7-25

7-34 (continued -1)

b. Step Method (Design Department goes first)

Design Programming Dept A Dept B Total

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Design 5,000 1,000 9,000 15,000

percent 33.3333% 6.6667% 60.00% 100.00%

Programming 200 200 600 1,000

20.0% 20.0% 60.0% 100.0%

70,000$ 50,000$ –$ –$ 120,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Design Service % 33.3333% 6.6667% 60.00% 100.00%

Amount

(70,000)$ 23,333$ 4,667$ 42,000$

Second Step

Programming Service % 20% 60% 80%

Allocation percent per service share % 20/80=25%; 60/80=75% 25.00% 75.00% 100%

Amount (73,333) 18,333 55,000

Totals for Production Departments 23,000$ 97,000$ 120,000$

Departments

7-34 (continued –2)

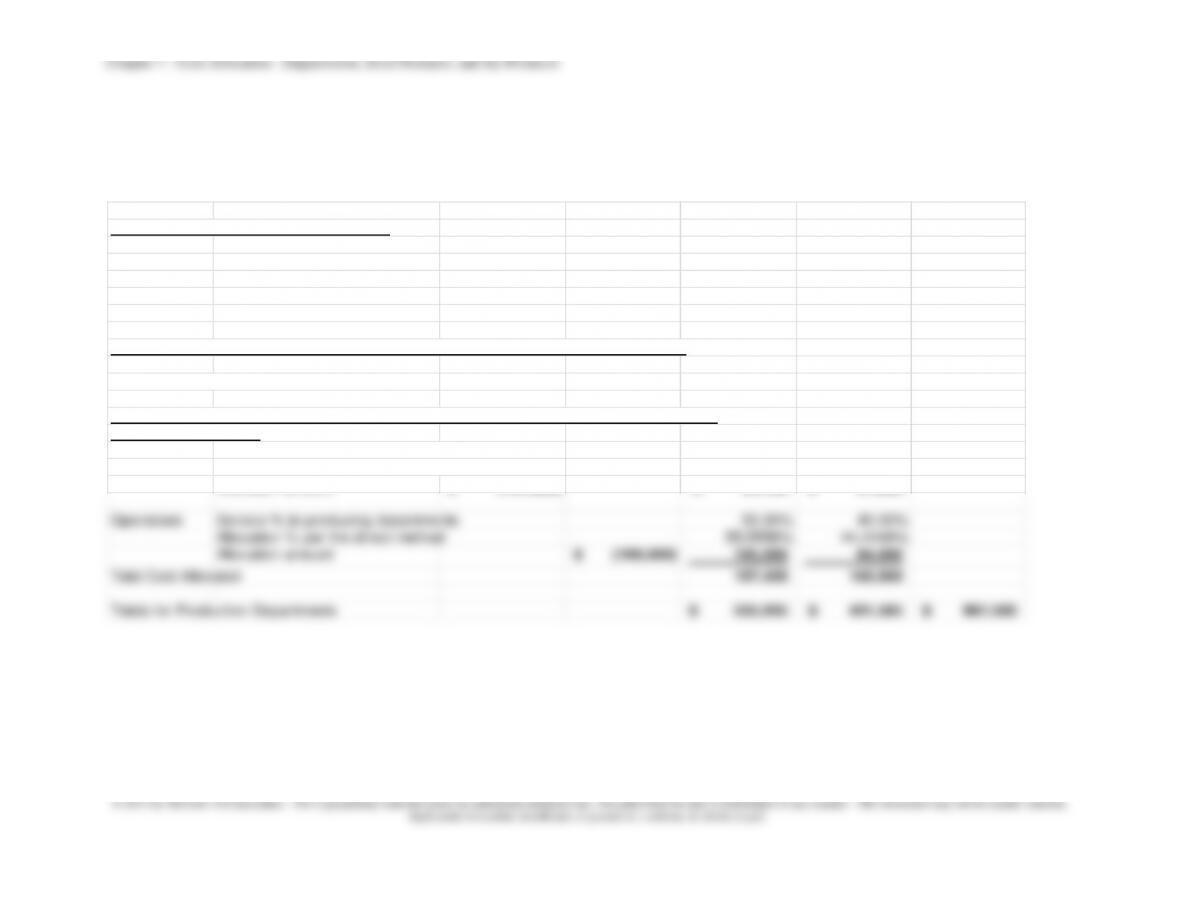

c. The Reciprocal Method (using

Solver)

Base Design Programming Dept A Dept B Total

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Design 5,000 1,000 9,000 15,000

percent 33.3333% 6.6667% 60.00% 100.00%

Programming 200 200 600 1,000

20% 0% 20% 60% 100%

Totals for All Departments

70,000$ 50,000$ –$ –$ 120,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Reciprocal Method

First: Solve the simultaneous equations (see Solver Solution Section below)

Amount Allocated from Design 85,714.29$

Amount Allocated from Programming 78,571.43$

Second: Allocate to Producing Departments:

Design Service % 6.6667% 60.00%

Alloc. Amt

5,714$ 51,429$

Programming Service % 20% 60%

Alloc. Amt

15,714 47,143

Totals for Production Departments 21,429$ 98,571$ 120,000$

Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-27

7-34 (continued –3)

2. Assuming total fixed costs remain the same, the current variable cost is

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-28

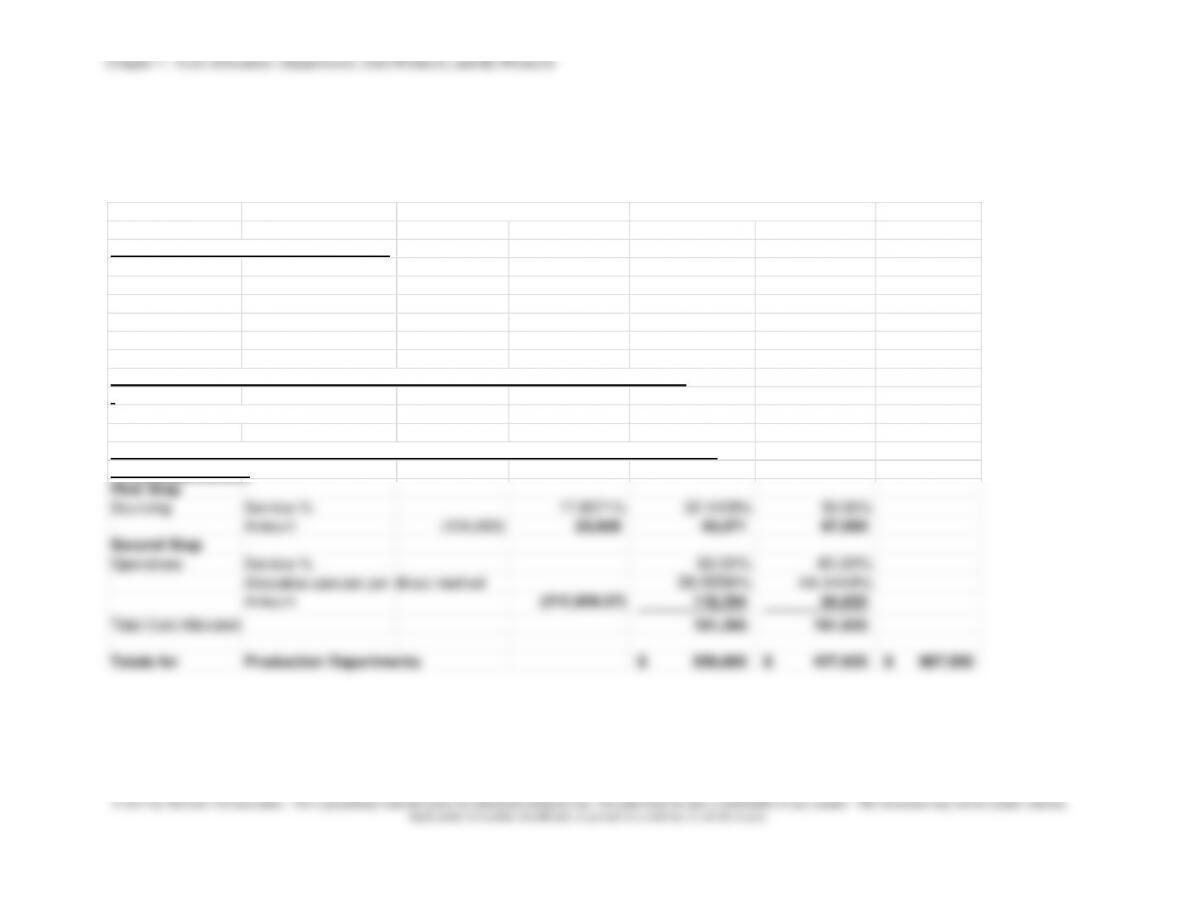

7-35 Departmental Cost Allocation (30 min)

1., 2.

Total Service Dept.

Cost Allocated

Total Production Cost

Direct Method

Assembly

$157,435

$555,935

Finishing

165,565

431,565

Step Method

Assembly

161,365

559,865

Finishing

161,635

427,635

Reciprocal Method

Assembly

158,440

556,940

Finishing

164,560

430,560

See following pages for calculations.

7-29

7-35 (continued –1)

The Direct Method

Sourcing Operations Asssembly Finishing

Total

DEPARTMENTAL ALLOCATION BASES

Sourcing 25,000 45,000 70,000 140,000

percent 17.8571% 32.1429% 50.00% 100%

Operations 10,000 50,000 40,000 100,000

percent 10.00% 50.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 134,000$ 189,000$ 398,500$ 266,000$ 987,500$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Sourcing Service % to producing departments 32.1429% 50.0000%

Allocation % per the direct method 39.1304% 60.8696%

Allocation amount (134,000)$ 52,435$ 81,565$

Operations Service % to producing departments 50.00% 40.00%

Allocation % per the direct method 55.5556% 44.4444%

Allocation amount (189,000)$ 105,000 84,000

Total Cost Allocated 157,435 165,565

Totals for Production Departments 555,935$ 431,565$ 987,500$

7-35 (continued-2)

The Step Method

Sourcing Operations Asssembly Finishing Total

DEPARTMENTAL ALLOCATION BASES

Sourcing 25,000 45,000 70,000 140,000

percent 17.8571% 32.1429% 50.00% 100%

Operations 10,000 50,000 40,000 100,000

percent 10.00% 50.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 134,000 189,000 398,500 266,000 987,500

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Sourcing Service % 17.8571% 32.1429% 50.00%

Amount (134,000) 23,929 43,071 67,000

Second Step

Operations Service % 50.00% 40.00%

Allocation percent per direct method 55.5556% 44.4444%

Amount (212,928.57) 118,294 94,635

Total Cost Allocated 161,365 161,635

Support Departments

Producing Departments