Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–31

15–37 Factory Overhead Analysis–Two, Three, and Four Variances; Spreadsheet

Application (50-60 Minutes)

1. Total Factory Overhead Application Rate:

Fixed factory overhead application rate:

Total machine hours at practical capacity:

Number of units of output at practical capacity = 40,000

Machine hours per unit × 2

2. Total Flexible Budget (FB) for Overhead Based on Units Produced:

Total standard machine hours allowed for the units produced =

42,000 units produced × 2 machine hours per unit = 84,000 hours

Manufacturing overhead in the flexible budget for 42,000 units:

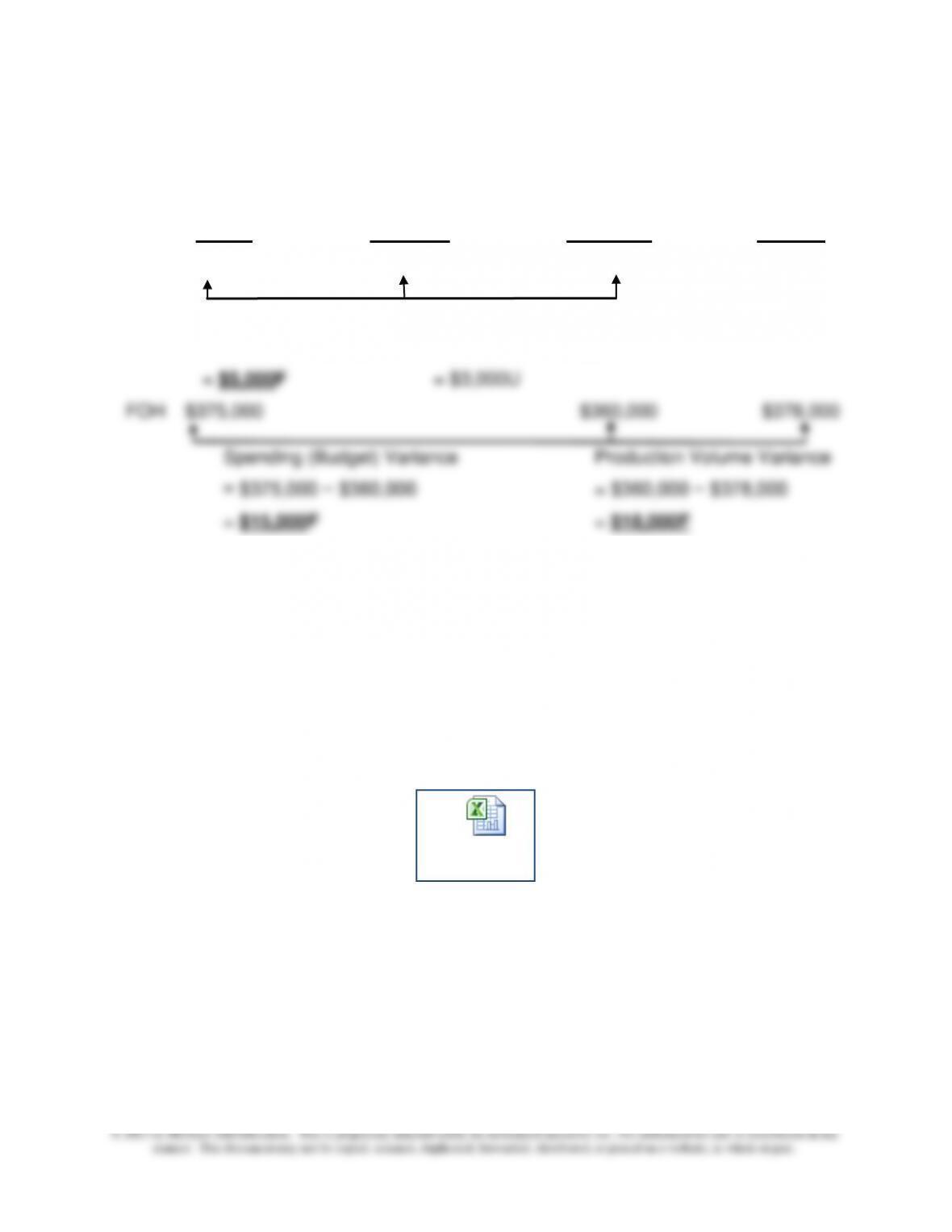

3. Production Volume Variance for 2013:

Fixed Overhead:

Actual Cost Budget Applied

$360,000 $378,000 = 84,000 hrs. × $4.50/hr.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–32

15–37 (Continued-1)

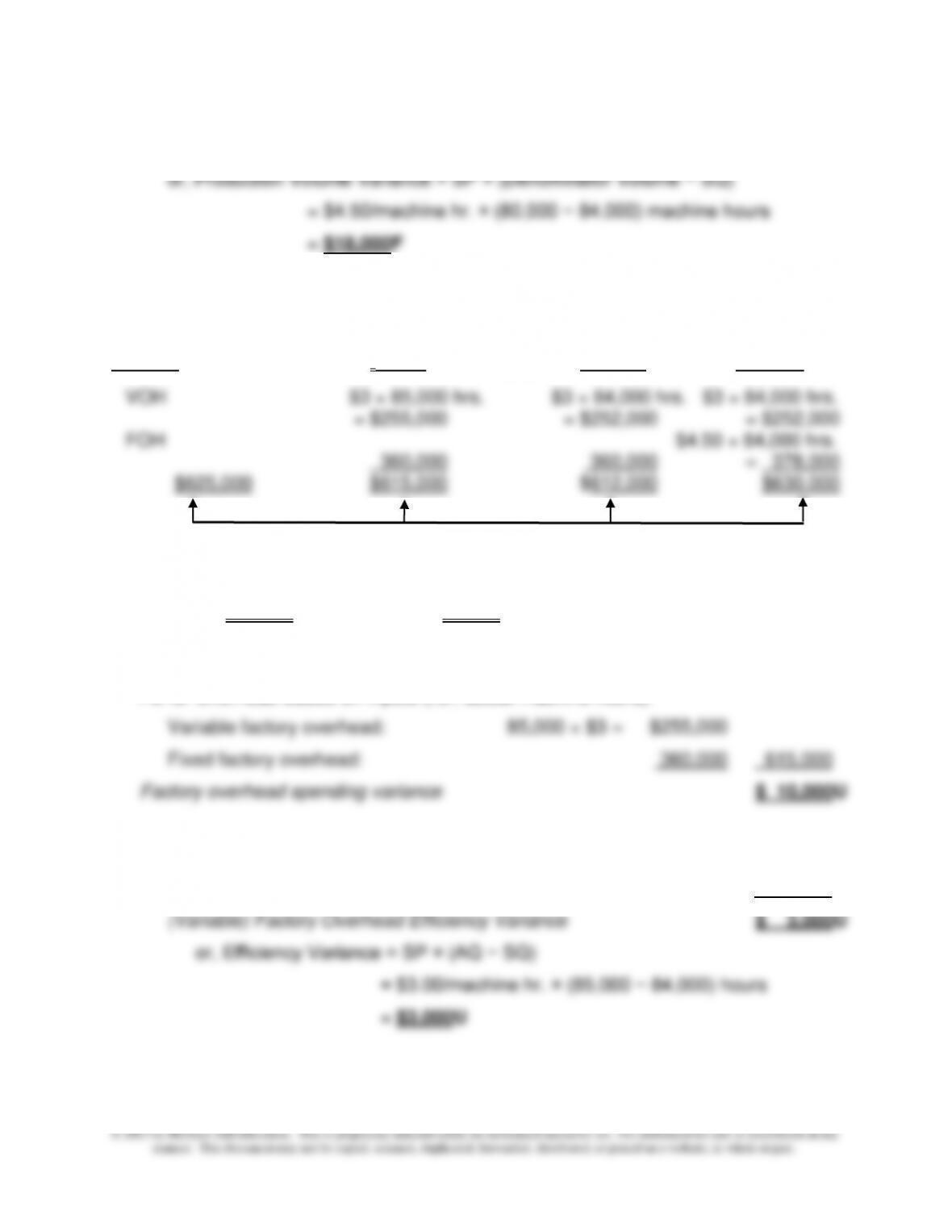

4. and 5.

FB Based on FB Based on

Actual Inputs Output Applied

Spending Variance Efficiency Variance Prod. Volume Variance

= $625,000 − $615,000 = $615,000 − $612,000

= $10,000U = $3,000U

Total factory overhead incurred $625,000

FB for Overhead Based on Inputs (i.e., actual machine hours):

5. FB for Overhead Based on Inputs (i.e., actual machine hours) $615,000

FB for Overhead Based on Output (from 2. above) 612,000

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–33

15–37 (Continued-2)

FB Based FB Based

on Inputs on Output

6. Actual (AQ × SP) (SQ × SP) Applied

VOH $250,000 $255,000 $252,000

Spending Variance Efficiency Variance

= $250,000 − $255,000 = $255,000 − $252,000

An Excel spreadsheet solution file for this assignment is embedded below. You can

open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then

return you to this Word document.

Ex. 15-37.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–34

15–38 Traditional ABC Costing (45-50 minutes)

Standard MH per unit = 32,000 MH 6,400 units = 5 MH per unit

No. of units manufactured during the period = standard allowed MH standard MH/unit

= 30,000MH 5MH/unit = 6,000 units

Budgeted no. of units/setup = 6,400 units 32 set-ups = 200 units/set-up

Standard no. of setups for the units manufactured = 6,000 200 = 30

FB based on Inputs FB based on Output

(i.e., based on actual (i.e., based on standard

1. Actual activity units) allowed activity units)

VOH:

Setup 28 × $600 = $ 16,800 30 × $600 = $ 18,000

MH 35,000 × $5 = 175,000 30,000 × $5 = 150,000

= $48,000U

FB based on Inputs FB Based on Output

(i.e., on actual (i.e., based on standard

2. Actual activity units) allowed activity units)

VOH:

Setup 28 × $2,600 = $ 72,800 30 × $2,600 = $ 78,000

= $52,000U

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–35

15–38 (Continued)

3. Standard variable overhead application rate = budgeted variable manufacturing

overhead in the master budget practical capacity (MH)

Setup cost = $64,000 + ($600 × 32) = $ 83,200

Applied based on machine hours = 32,000 × $5.00 = 160,000

Total variable factory overhead @ practical capacity = $243,200

VOH: 35,000 × $7.60 = 266,000 30,000 × $7.60 = 228,000

FOH: 200,000 200,000

Total OH $480,000 $466,000 $428,000

Spending Variance Efficiency Variance

= $14,000U = $38,000U

Flexible-Budget Variance

= $52,000U

Notice that assumptions made regarding the number and type of activity measures used

to apply standard overhead costs to production can affect both the total flexible-budget

(controllable) variance and the components of this variance. For this reason, the

activities used to construct flexible-budgets for control purposes should be carefully

selected.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–36

15-39 ABC and Practical Capacity; Spreadsheet Application (40–50 minutes)

Note: An Excel spreadsheet solution file for this assignment is embedded below. You

can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then return

you to this document.

Ex. 15-39.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–37

15–40 Use of Payoff Tables (Appendix); Spreadsheet Application (30-45 minutes)

(1) Expected value of the decision to investigate the variance:

E(Investigate) = [(I × (1 −p)] + [(I + C) × p]

= [($1,200 × (1 − 0.25)] + [($1,200 + $3,800) × 0.25]

(3) Let p = the indifference probability, that is, the probability of for a nonrandom

variance such that management is indifferent between the two courses of action,

investigate or do not investigate:

p = I ÷ (L − C)

nonrandom cause.

Thus, if the probability (p) for a nonrandom cause (or causes) is 4.96%,

management would be indifferent, in expected value terms, between investigating

and not investigating the variance. The expected cost of each course of action to

the organization would be the same. If, as in the present case, the probability of

the process being out of control (i.e., the probability of a non-random variance)

exceeds 4.96%, the indicated course of action would be to investigate the

variance.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–38

15–40 (Continued)

Note: An Excel spreadsheet solution for this exercise is embedded below. You can

open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

this document

Ex. 15-40.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

PROBLEMS

15-41 Capacity Levels and Fixed Overhead Rates (60 minutes)

1. As the name suggests, maximum (theoretical) capacity is the maximum output

level for the plant, one that assumes operating at maximum efficiency. This

level of productivity suggests no “down time” for machine maintenance, no

internal disruptions to the manufacturing process, and no slack in external

budgeted (forecasted) activity; practical capacity (i.e., theoretical capacity

reduced by external demand considerations and normal internal losses due to

machine downtime, employee personal time, etc.); and, normal capacity

(expected sales demand over an upcoming three- to five-year period).

2. A revised variance report for Yuba Machine Company using expected

(budgeted) activity as the basis for applying fixed factory overhead is

presented below.

Yuba Machine Company

Revised Variance Report

for Six Months ended May 31, 2014

Applied

Actual Overhead

Costs Costs Variance

Total variable factory overhead $120,220 $120,000 $ (220)

Fixed factory overhead:

Applied Fixed Overhead, First Six Months

Salaries: 40,000 DLHs × $1.00/DLH = $40,000

Depreciation and amortization:

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–40

15–41 (Continued-1)

3. If the fixed factory overhead rate was based on practical capacity rather than

theoretical (maximum) capacity, Yuba Machine Company’s reported operating

income at May 31, 2014 would be $12,000 less, not $90,000 as reported. The

revised CGS calculation follows.

Cost of goods sold (CGS), revised amount:

CGS, as originally reported $380,000

Less: fixed OVH included by Sid Thorpe 48,000

Yuba Machine Company

Interim Income Statement, Revised

For Six Months Ended May 31, 2014

Sales $625,000

CGS ($380,000 + $12,000) 392,000

Gross profit $233,000

Less:

Selling expense $ 44,000

Depreciation expense 58,000

Principal point: Choice of the denominator volume affects product costs. If

resulting overhead variances for a period are closed to CGS (rather than

allocated), then these differences will affect “the bottom line.”

(4) As noted in part (1), the use of theoretical capacity is generally not recommended,

although perhaps some might argue that in an increasingly competitive environment

this alternative has some merit (since it will result in the smallest, that is, tightest,

standard costs). As discussed in the text, the ultimate choice of the denominator

denominator level in setting fixed overhead allocation rates in conventional

accounting systems and in ABC systems as well.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–41

15–41 (Continued-2)

From a managerial standpoint, the use of practical capacity has a number of key

advantages. For one thing, it “reveals” the cost of unused capacity (rather than

“hiding” this cost as part of the cost of good units produced). For another thing, it

helps managers avoid what has been referred to as the “death spiral,” which can

occur if management sets selling prices on the basis of full-cost information (in this

case, to include the cost of unused capacity). The use of practical capacity also is

consistent with the way the numerator in the application rate is defined. That is, the

Finally, we note that for U.S. federal income tax purposes, companies can base their

fixed overhead rates on practical capacity. So, for all of the above reasons, for

managerial purposes we recommend the use of practical capacity as the

denominator activity level used to calculate predetermined fixed overhead allocation

rates.

At this point, the instructor has an opportunity to provide an expanded discussion of

this issue by referencing appropriate financial reporting and income-tax

considerations concerning the setting of predetermined overhead rates, particularly

fixed overhead rates.

As indicated in the chapter, generally accepted accounting principles (viz., FASB

ASC 330-30–10-3, previously SFAS 151, and available at www.fasb.org)deal

specifically with the issue of establishing overhead allocation rates and the

disposition of any resulting overhead variances at the end of the period. GAAP

requires the use of “normal capacity” for allocating fixed overhead costs to

production. Further, “normal capacity refers to a range of production levels … (i.e.,

the amount of) production expected over a number of periods under normal

circumstances.” By this specification, “normal capacity” refers to a range of

production levels within which ordinary variations in production levels are expected.

Further, generally accepted accounting principles require that any “unallocated

overheads be recognized as an expense in the period in which they are incurred”

(FASB ASC 330-10–30-7, previously SFAS 151).

For U.S. income tax purposes, the issue regarding choice of the denominator level

for establishing fixed overhead allocation rates and the end–of-period treatment of

overhead cost variances is provided in the Regulations. Two, in particular, bear on

the subject at hand: Reg. §1.263A and Reg. §1.471-11.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–42

15–41 (Continued-3)

Reg. §1.263A specifies that “indirect (production) costs be allocated…using either…the

standard cost method, or a method using burden rates, such as ratios based on direct costs,

hours, or other items, or similar formulas, so long as the method employed reasonably

allocates indirect costs among production…activities.” (emphasis added)

Reg. §1.471-11(“Inventories of Manufacturers”) extends the guidance provided in

Regulation 1.263A by specifying the following:

• Unless minor in amount, end–of-period overhead cost variances must

be written off as a period cost.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–43

15-42 Ethics and Overhead Variance (60-75 minutes)

1. Operating income as currently reported ($9,600,000)

Production volume variance: $9,000,000 × 0.2 = 1,800,000 U

Operating income before adjusting for volume variance ($7,800,000)

Current fixed overhead application rate per machine hour:

Revised operating income (under given assumptions) ($744,000)

Changes in operating income

Operating income as currently reported ($9,600,000)

Revised operating income ( 744,000)

Change (improvement) in operating income $8,856,000

or,

2. As indicated by the discussion in the text, there is a great deal of judgment

involved in determining the “denominator activity level” used to set the

predetermined fixed overhead application rate. That is, there is not necessarily a

clear-cut answer to this issue. Possible denominator levels include: budgeted

(forecasted) output, normal capacity, practical capacity, or theoretical capacity.

The numbers assumed in this problem might be viewed as extreme or contrived,

decrease reported accounting income).

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–44

15–42 (Continued-1)

Our position is that a certain amount of latitude should be afforded managers in

regard to setting fixed overhead rates (specifically, choice of denominator activity

level) and the manner in which standard cost variances are treated at the end of the

year. Thus, one approach to this question is to focus on intent. Here the IMA’s

Statement of Ethical Professional Practice (www.imanet.org) may be helpful. This

statement refers to four ethical standards of behavior for management accountants:

Competence; Confidentiality; Integrity; and, Credibility. The present case raises

issues regarding the fourth of these standards, Credibility. “Each member (of the

profession) has a responsibility to: communicate information fairly and objectively;

and, to disclose all relevant information that could reasonably be expected to

influence an intended user’s understanding of reports, analyses, or recommendation.”

Under this standard, therefore, one might argue that it would be unethical for the VP

of Finance to change the denominator activity level solely to improve reported

operating results, particularly when these results would then be communicated to

the test of being an “asset”—that is, something that would benefit one or more future

periods. The underlying costs associated with a production volume variance are

capacity-related costs which, by definition, expire with the passing of time. Thus, by

capitalizing the volume variance the VP of Finance may, in fact, be violating a basic

accounting standard.

3. Generally accepted accounting principles GAAP (FASB ASC 330–10–30-3 to -7,

previously SFAS151—“Inventory Costs: An Amendment of ARB No. 43, Chapter 4,”

and available at www.fasb.org) reaffirms (and brings U.S. reporting standards more in

line with International Accounting Standards in the area) that abnormal amounts of

idle facility expense (as well as abnormal amounts of freight, handling costs, and

allocating fixed overhead costs to product, then any amount of unallocated overhead

should be viewed as “abnormal” and therefore treated as a period cost.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–45

15–42 (Continued-2)

4. The point of this question is to impress upon students the fact that under absorption

costing, reported operating income can be affected by the method used to dispose

of any production volume variance associated with fixed overhead. In other words,

the variance–disposition method can be used to “manage earnings” under absorption

costing.

As noted in the chapter, the amount of fixed overhead costs absorbed into or

released from inventory (i.e., the Balance Sheet) is affected by the denominator level

chosen to establish the predetermined fixed overhead application rate. Choice of the

denominator volume level simultaneously affects the amount of the production

volume variance for the period. Consequently, the effect of a change in physical

inventory can be intensified or reduced based on how the production volume

variance is disposed of at the end of the period. Specifically, this ability to affect

reported income is confined to the situation where the production volume variance is

written off entirely to cost of goods sold (CGS), as follows:

• If inventory is increasing, choosing a lower denominator-volume level will

fixed overhead into CGS.

Thus, it is through the interaction of how the fixed overhead rate is set and how the

resulting production volume variance is accounted for that provides management an

opportunity to manage earnings under absorption costing. The above points suggest

that managers can increase short-run operating income by: (1) choosing larger

denominator levels if they expect inventory to decrease, or (2) choosing smaller