Chapter 4 – Job Costing

4-1

Chapter 4

Job Costing

Teaching Notes For Cases

4-1. Constructo Inc. (Under or Overapplied Overhead)

This case has the learning objectives of: (1) explaining when it is appropriate for a company to

use a job costing system, (2) calculating overhead applied to various jobs, (3) determining the total cost of

a finished job and the total cost of an unfinished job, (4) explaining the proper accounting treatment for

over- or underapplied overhead balances at the end of an accounting period.

1. A job costing system is appropriate in any environment where costs can be readily identified

with specific products, batches, contracts, or projects.

2. The only job remaining in Constructo’s work-in-process inventory at May 31, 2001 is DRS114.

The dollar value of DRS114 can be calculated as follows:

DRS114 balance 4/30/01 $250,000

May additions:

Direct materials $124,000

Purchased parts 87,000

Direct labor 200,500

Factory overhead

(19,500 hours x $7.50*) 146,250 557,750

Work-in-process inventory

5/31/01 $807,750

======

* Factory overhead rate = $4,500,000 / 600,000 hours

= $7.50 per hour

3. The dollar value of the playpens remaining in Constructo’s finished goods inventory at May 31,

2001 is $455,600 calculated as follows:

Playpen Units

Finished goods inventory 4/30/01 19,400

Units completed in May 15,000

Units available 34,000

Units shipped in May 21,000

Finished goods inventory 5/31/01 13,400

=====

Since Constructo uses the FIFO inventory method, all units remaining in finished goods

inventory were completed in May.

Chapter 4 – Job Costing

4-2

Unit cost of playpens completed in May

Work-in-process inventory 4/30/01 $420,000

May additions:

Direct materials $ 3,000

Purchased parts 10,800

Direct labor 43,200

Factory overhead

(4,400 x $7.50) 33,000 90,000

Total cost $510,000

======

Unit cost = Total cost / Units completed

= $510,000 / 15,000

= $34 per unit

Value of finished goods inventory

= unit cost x quantity

= $34 x 13,400

= $455,600

4. If the amount of overapplied or underapplied overhead is not material nor the result of an error

in the overhead application rate, the amount is generally treated as a period cost and charged to the cost of

goods sold. If the amount is significant, the amount should be prorated over the relevant accounts, i.e.,

work in process inventory, finished goods inventory, and cost of goods sold.

Chapter 4 – Job Costing

4-3

Case 4-2 East River Manufacturing (A) (Problems of a Traditional Job Costing System)

This case has the learning objectives of:

(1) Describe the major economic and competitive trends affecting the power-generation industry and

its suppliers throughout the eighties.

(2) Understand some of the strategic issues associated which an investment in computer- integrated

manufacturing offers.

(3) Study some of the unique characteristics of accounting systems in a contract environment.

(4) Examine the implications, which an investment in advanced manufacturing technology has for

accounting system design.

Source: 1997 IMA Cases from Management Accounting Practice, Volumes 10 and 11, Case 8.

Suggested Solutions And Important Points

1. Briefly summarize and contrast the competitive environment in the pre-1980 era with that of the late

eighties and early nineties.

The pre- I 980’s competitive environment for steam generation equipment manufacturers was

typical for U.S. industry in general during the post-World War 11 era. A combination of factors

including lack of competition, pent-up demand, rising standards of living, and a population explosion

fed by the baby boom from 1946-1964 drove business demand to unprecedented levels for twenty-five

years after the war. The prime beneficiaries of this boom were the utility and PSI and its OEM

competitors met industrial process firms whose power generation needs. However, for a variety of

reasons -some economic, some technological, some regulatory, and some demographic – the long

expansionary period after WW Il came to an abrupt end by the late seventies.

The competitive structure and the economics of the power business were changing rapidly. Utilities

and process intensive industries experienced dramatic cost increases. OEM orders dried up and the

once-predictable growth in demand for power-generation equipment vanished almost overnight. What

evolved was a highly competitive market fueled by new players, including mature foreign suppliers

like Mitsubishi. Beginning in the early eighties, the industry was to undergo a dramatic shift away from

OEM toward the replacement-parts business. But with overall demand down, the industry was

suffering from severe overcapacity. It was inevitable that a shakeout would occur, during which there

would be severe dislocations within the industry. The economies of scale enjoyed by the OEM

manufacturers dissipated as the market shifted to the low-volume, made-to-order replacement-parts

business. As explained in the case, the key factors of success for the replacement market were, for the

most part, quite different from those for the OEM market.

2. What are the problems that plant management has to resolve?

Plant management, together with marketing, product engineering, and process engineering, needs to

develop strategies to:

• Reduce cost

• Increase flexibility to produce small orders

Chapter 4 – Job Costing

4-4

Prior to 1992, the Tube Shop’s manufacturing process had high manpower requirements, high

in-process inventories, and high maintenance costs. East River and the other OEM manufacturers were

not structured to meet the demands of serving the replacement-parts market- short lead-times, diverse

tube designs, and competitive cost. Changes in the cost of generating power in the late seventies led to a

rapid shift in demand for power-generation equipment away from huge OEM contracts toward

low-volume, highly specialized repair and replacement business. The economics of production for repair

and replacement parts place a premium on cost-efficient flexibility and fast turnaround. Traditionally

times were 3-4 weeks. While East River always tried to accommodate customers’ immediate needs, they

did so at considerable cost and disruption to production schedules.

Furthermore, productivity and product quality were suffering for several reasons. As product variety

increased, the workload was more complex and rework was more frequent. Also, relations among

management, first-line supervisors, and the union workforce were not on the best of terms, which

probably had a residual effect on product quality.

Whatever the solution, East River would continue to face heightened competition for a decreasing

number of orders. Survival was dependent upon their success at reducing cost, improving response time,

and making further inroads into the replacement-parts market.

3. What potential problems may occur between the as-sold cost estimates and the actual contract cost?

Part of the problem is endemic to the business. Cost estimators need to generate expedient bid

proposals. Under the “Proposal Front-end” system, product design engineers and cost estimators consult

historical data bases for information on previous orders – tube geometry, bill -of-materials, routings – to

develop a tube design scenario and estimate the tube’s manufacturing and material cost. There may be

little or no passing of information to the contract stage if the proposal is accepted.

If the proposal becomes a contract, product design engineers create detailed product structures.

changed since then. One study of contract cost overruns described in the case revealed that the

performance of the stud welding machines was not always meeting detailed engineering estimates.

Actual man-hours was overrunning estimated man-hours on studding machines with increasing

frequency, even though no changes had been made in the tube design. It was determined that when studs

were spot welded to tubes, frequent rewelding had to be done because tolerances were not always being

met the first time. Age and wear and tear on the stud welders’ controls had caused tolerances to loosen

4. Diagram the structure of the existing cost system and explain how cost information is used for

decision-making, cost control, and performance evaluation purposes.

Chapter 4 – Job Costing

4-5

Refer to Exhibit TN – 1. The primary cost object is the contract. The as-sold estimate (ASE) for a job

served as the bid on a customer’s request for a quote (RFQ). If the bid was accepted, the ASE became the

budget for the contract and was used for monitoring costs and evaluating performance. Regardless of the

accuracy of the cost assignment methodology, using ASE as the contract budget had major implications.

Cost estimators prepare ASEs based upon specifications supplied by the customer and from parts

and cost records of similar parts and assemblies on past contracts. However, once a quote was accepted, a

more detailed product design process began. (Design work was not necessary for replacement tubes on

PSI original equipment.) Design decisions affected materials composition, process routings, and

resources used. Design engineers did not feel obligated to stay with the original ASE specifications.

Their motivation was to design and build the best component/part for the situation.

engineering and graphics effort, which goes into designing components. Therefore, design engineering

and graphics time was accumulated and charged directly to the contract. However, it is unusual to see

machine setup and material handling costs directly charged to a contract, component, or part as they are

under this system.

Nonetheless, the cost system was prone to some of the same cost distortions typical of cost

systems of this time period. Every project bore some of the costs of every resource – all shop

supervision, all direct overhead, all depreciation, all repair costs of every piece of equipment in the

Tube Shop. This system is a shotgun approach to contract and component costing. All resources were

charged to the contract through the man-hour rate, regardless of the actual resources used in processing

parts and components. The system averaged all costs across contracts in proportion to man-hours

consumed and did not address the different processes utilized for a contract. However, since the old

electromechanical technology was labor-paced, there was a correlation between man-hours and

equipment-related costs. Therefore, cost distortion was not as great as it would be in more automated

environments.

5. Is the labor-based cost system appropriate for this facility? Should activity-based costing be

implemented to analyze product costs?

There was some dissatisfaction with the cost system prior to implementation of the CIM line. The

overall cost competitiveness of the pre- 1992 manufacturing process was the main concern. For instance,

marketing was frequently dissatisfied because they often felt costs were too high to allow a competitive

understanding of what impact decisions throughout the value chain will have on costs and profits at the

project level. As Cooper and Kaplan point out, “… it is more important to measure profit over the life of

the product or the project than to get procedures for allocating costs to stages along the production

Chapter 4 – Job Costing

4-6

process.” (Ingersoll Milling Machine Company, Teaching Note 5-188053, Harvard Business School

(1988): 5.) Given the number and size of OEM projects, it may not be important that individual loose

tubes be costed correctly so long as any distortions at the part level average out at the project level. If

that was the case, the labor-based system was probably adequate when the majority of the workload

related to 20 to 30 large OEM projects being processed at any given time.

and component level would be necessary. With the automation of the Tube Shop line, direct labor has

even less of an association with activities performed on the CIM line. It would be more meaningful for

cost estimation and cost management purposes if cost assignment procedures were developed which

recognize the cost of activities performed throughout the Tube Shop.

6. Prepare a set of recommendations for changes in the cost system. Describe a general framework for

costing products in an automated facility.

Whether the pre- 1992 labor focused cost system was adequate or not is no longer the issue. Given the

nature of the CIM system, clearly there is no longer much of a relationship between direct labor and

work performed by CNC machines. A new cost assignment process was needed to accommodate the

Students will see how project teams may grapple to develop some sense of direction when designing any

new process, especially if the team has no prior experience with that process.

Chapter 4 – Job Costing

4-7

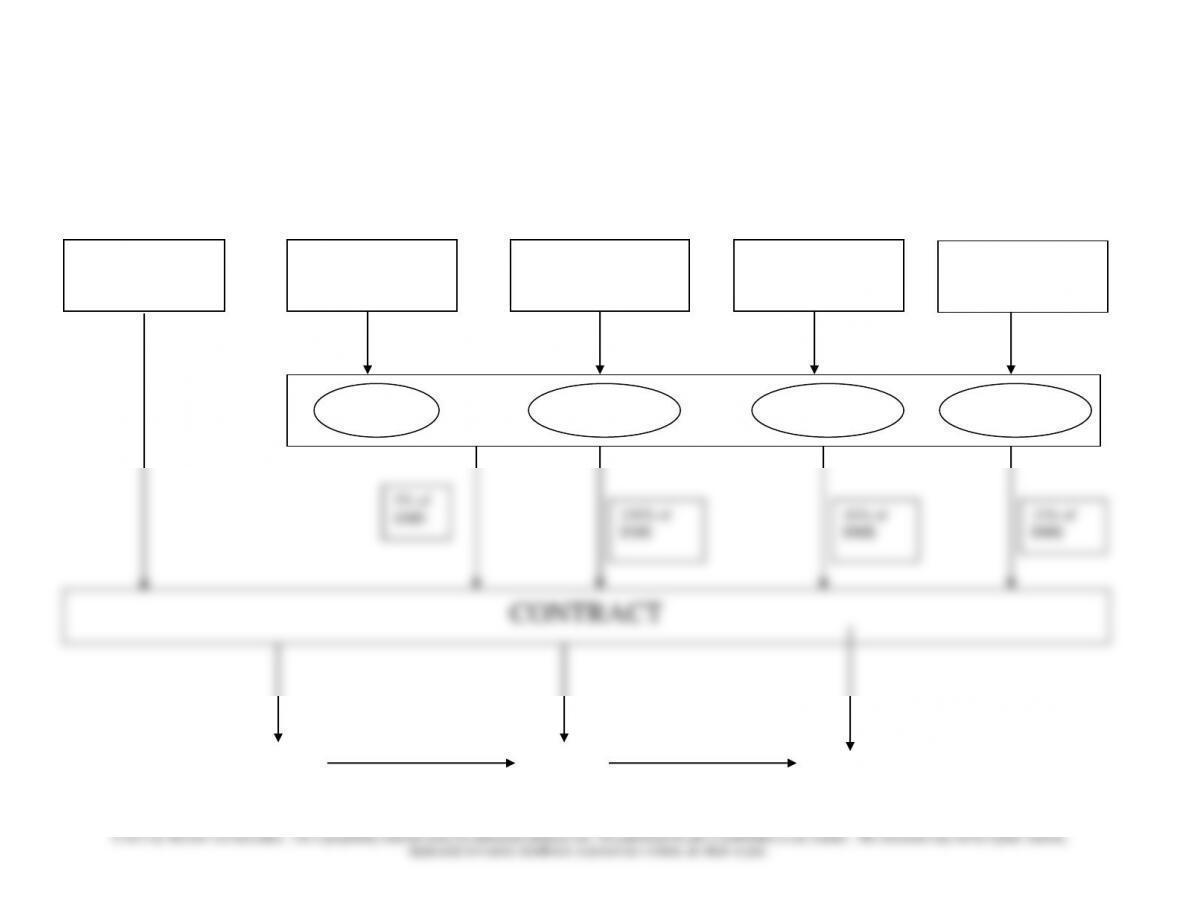

Exhibit TN-1

Existing Overhead Cost Allocation System

Cost Center

Component Component Component

Group Part Group Part Group Part

Direct Costs – Engr.,

Graphics, Setup, Matl.

Hand.

Mat’l. Handling

Procurement – Related

Overhead

Shop 415 Overhead

(Bays 4 & 5)

Plant Support Services

(Works Gen’l)

Central Support

Services

(OAW)

Cost Pool

Cost Pool

Cost Pool

Cost Pool

Chapter 4 – Job Costing

4-8

Teaching Strategies for Readings

4-1: How I Reengineered a Small Business

This article describes both the old and new job costing systems at James Street Fashions (also

called Latt-Greene), a small textile knitting and converting operation in Vernon, California. The author is

the controller of Latt-Greene. He instituted a spreadsheet-based job costing system that helped to reverse

a $5 million loss on $65 million in sales revenue to a $3 million profit on just $32 million in sales

revenue. He also eliminated unnecessary overtime and increased the overall quality of the company’s

product line.

Discussion Questions:

1. Briefly describe the company, its products and customers.

Latt-Greene is a small textile knitting and converting operation in Vernon, California. It knits textiles

2. What problems did the author discover when he conducted his initial interviews with the

company in early 1990.

3. Describe the company’s old financial costing system, and identify its weaknesses as well as

business operating and profit consequences cause by its poor costing system.

The company did not have any costing system. It used a manual system that include only general

ledger, cash receipts journal, customer ledgers, and a cash disbursement journal. As yarn was knitted into

attempt was made to cost the product.

Consequences of the company’s poor costing system:

(1) There was no controlling order number that followed the job through all its steps before the

finished product was delivered to the customer.

4. What are major impacts of the company’s new computerized costing system on its business

operations, product prices and quality, and company’s profit?

Major impacts:

(1) Better-cost data was developed.

Chapter 4 – Job Costing

4-9

(2) Pricing policy changed to reflect on new better-cost data. In some cases, major customers

were lost because the company raised prices. But most customers were retained. Because

(5) The new costing system helped the company to reverse a $5 million loss on $65 million

in sales revenue to a $3 million profit on just $32 million in sales revenue.

5. What are general principles learned by the author for changing or reengineering a company’s

costing system?

Some general principles for changing or reengineering the company’s costing system:

(1) Be open with all employees regarding the process.

(2) Solicit input from all employees.

Chapter 4 – Job Costing

4-10

4-2 Distinguishing Between Direct and Indirect Costs Is Crucial For Internet Companies

This article points out the importance of distinguishing direct and indirect costs for internet companies.

The cost objects are different for internet companies, a focus on customers instead of products.

However, the key issues of pricing, cost allocation, and cost management are still applicable.

Discussion Questions:

1. What characteristic must a company have to be referred to as an internet company?

To be eligible for the Dow Jones Internet Commerce Index, a company must receive 50% or more of its

sales from the internet.

2. What is the key element of competition for an internet company?

The key competitive element is customer service, including all phases of the customer serviced cycle,

3. What is the key cost allocation issue for internet companies?

4. What is the key cost object for an internet company?

The customer.

4-11

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

4-3: Key Project Management Concepts for the Accountants

This article provides an introduction to key project management concepts as this field has become

increasingly important for accountants today. Most accountants have had little exposure to the core

concepts of project management. This article serves as a resource with definitions, the PM life cycle and

an accounting example.

Discussion Questions:

1. According to PricewaterhouseCoopers, why is project management increasingly important?

“In the tight-fisted business environment of 2003 and with increased expectations for transparency and

deployed to support the organization in its strategic and operational goals.”

2. What fields have been traditionally associated with project management concepts?

PM was thought to apply only to activities such as construction, research and engineering, and software

3. Why are project objectives important? What characteristics should these objectives entail?

Project objectives are set to provide direction for project activities and to enable measuring actual results

against prior expectations. They direct resource usage (manpower, materials, etc.) and affect schedule

integrity and the quality of work. Project objectives should be:

Achievable in terms of time, resources, and staff;

Understandable, as opposed to complex;

and procedures; and

Assignable to a specific department or individual.