Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-16

5-35 Customer Profitability Analysis (25 minutes)

1.

Jerry Inc.

Kate Co.

Customer Unit Level Costs:

Sales return(40×$5;175×$5)

$200

$875

Customer Batch Level Costs:

Order processing (5×$300; 30×$300)

$1,500

$9,000

Sales return (2×$100; 5×$100)

$200

$500

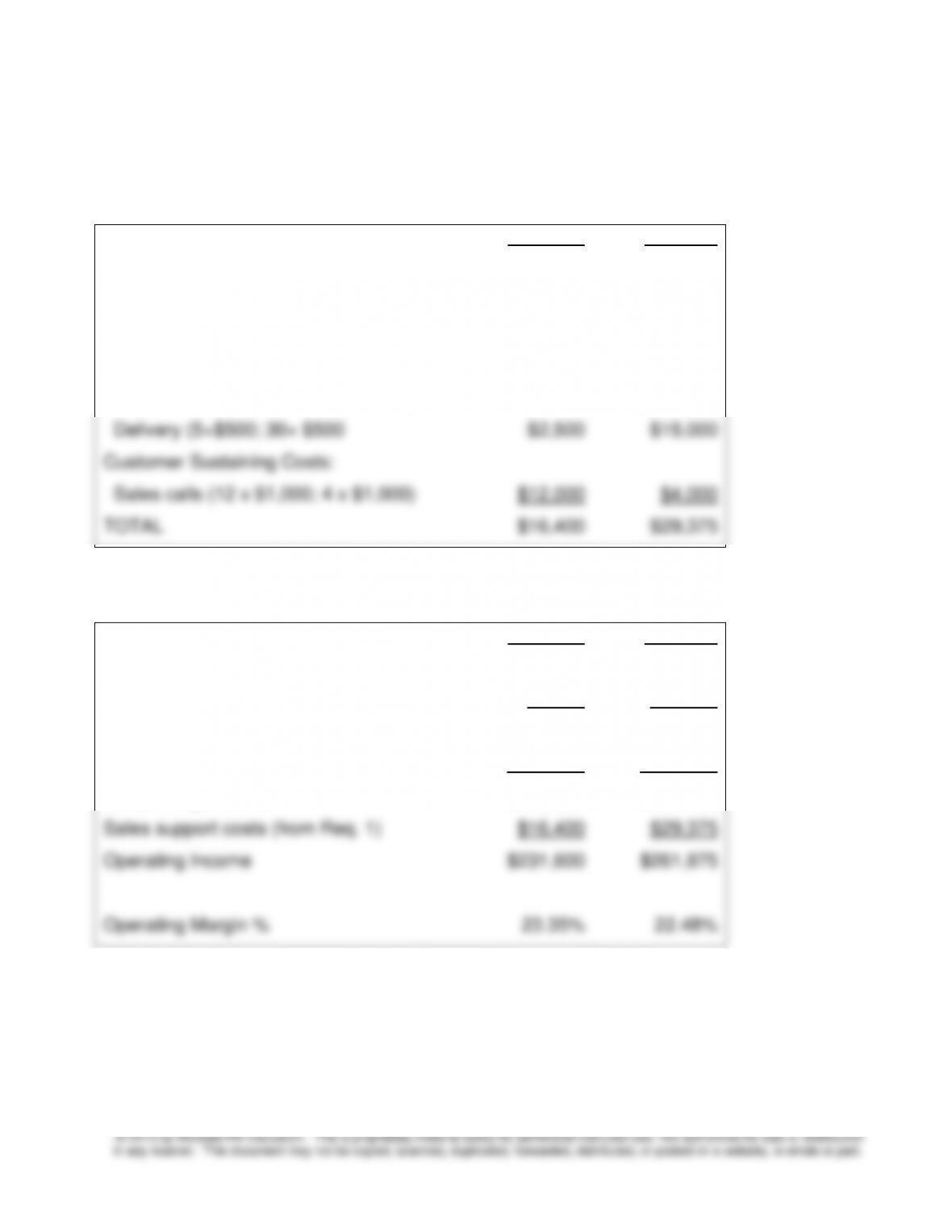

Delivery (5×$500; 30× $500

$2,500

$15,000

Customer Sustaining Costs:

Sales calls (12 x $1,000; 4 x $1,000)

$12,000

$4,000

TOTAL

$16,400

$29,375

2.

Jerry Inc.

Kate Co.

Sales

$1,000,000

$1,200,000

Sales Return (40×$200; 175×$200)

$8,000

$35,000

Net Sales

$992,000

$1,165,000

Cost of goods sold

$744,000

$873,750

Gross margin (25%)

$248,000

$291,250

Sales support costs (from Req. 1)

$16,400

$29,375

Operating Income

$231,600

$261,875

Operating Margin %

23.35%

22.48%

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-17

5-36 Customer Profitability Analysis (25 min)

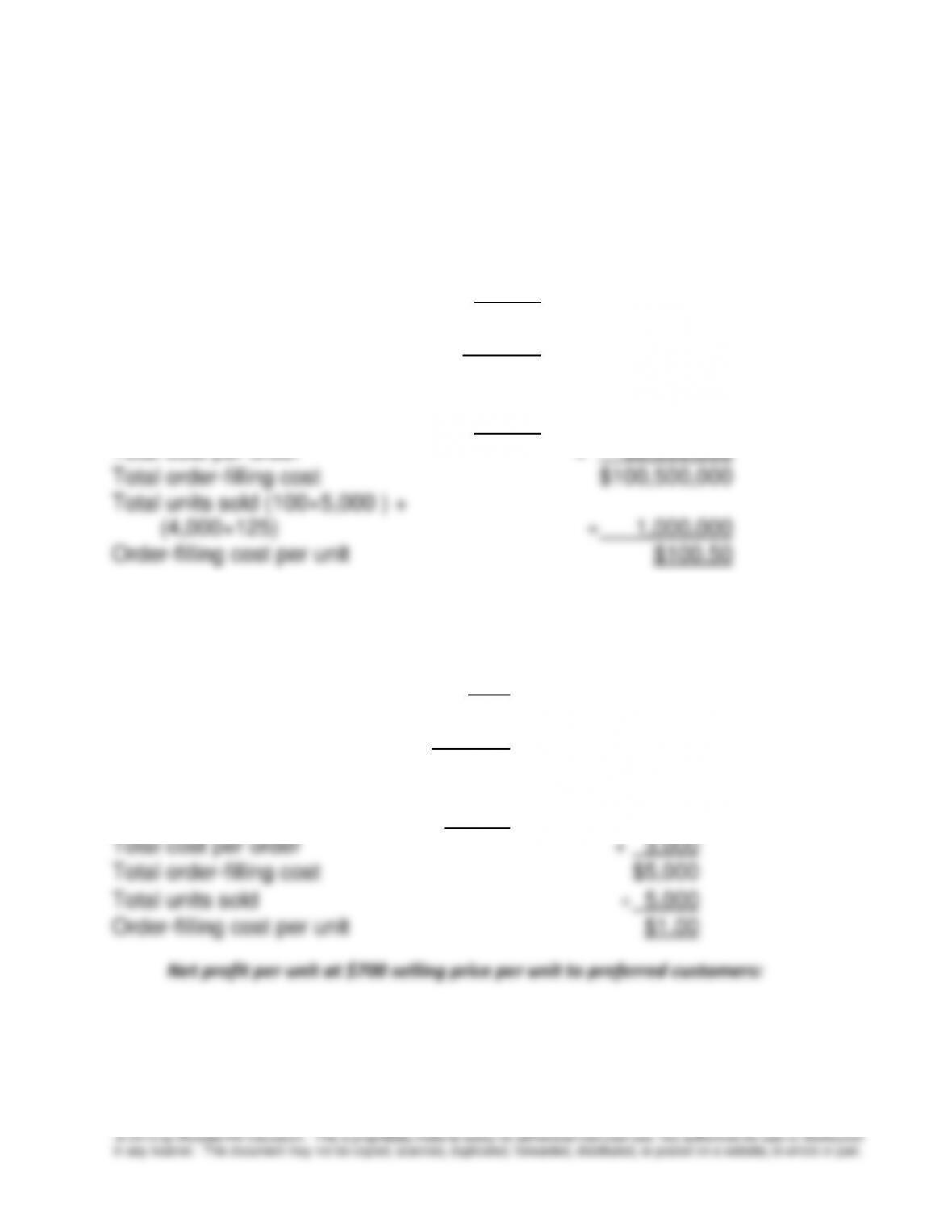

1. Determination of the $100.50 order-filling cost per unit

Total number of orders:(2 × 100 PCs) + (10 × 4,000 SCs) = 40,200

Total number of orders

40,200

Number of orders per block

60

Total number of blocks

670

Cost per block

× $60,000

Total cost of order blocks

$ 40,200,000

Total number of orders

40,200

Per order order-filling cost

× $1,500

Total cost per order

+ 60,300,000

Total order-filling cost

$100,500,000

Total units sold (100×5,000 ) +

(4,000×125)

1,000,000

Order-filling cost per unit

$100.50

2. Order filling cost per unit sold to PC:

Total number of orders

2

Number of orders per block

60

Total number of blocks

1/30

Cost per block

× $60,000

Total block cost

$2,000

Total number of orders

2

Order-filling cost per order

× $1,500

Total cost per order

+ 3,000

Total order-filling cost

$5,000

Total units sold

5,000

Order-filling cost per unit

$1.00

Net profit per unit at $700 selling price per unit to preferred customers:

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-18

5-36 (continued)

3. Order filling cost per order by SC:

Cost per block

$60,000

Number of orders per block

÷ 60

Block cost per order

$1,000

Number of orders per SC

× 10

Total block cost per SC

$10,000

Order-filling cost per order

$1,500

Number of orders per SC

× 10

Total cost per order

+ 15,000

Total order-filling cost

$25,000

Total units sold

÷ 125

Order-filling cost/unit

$200

Profitability per unit at $800 selling price per unit to SC

Selling price per unit

$800.00

Manufacturing cost

$600.00

Order-filling cost/unit

+ 200.00

Total cost per unit

800.00

Net profit or loss per unit

$ 0

Preferred Customer

Selling price per unit

$700.00

Manufacturing cost

$600.00

Order-filling cost/unit

+ 1.00

Total cost per unit

601.00

Net Profit per unit

$ 99.00

Profit margin per unit

14.14%

5-19

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution

in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

5-37 Tools for Successful ABC/M Implementation (10 min)

Other guides or tip for successful implementation are noted in the text, but

some are listed below:

• Choose a type of context where ABC is likely to succeed, such as a

Additional Sources: Dan Swenson and Douglas Barney, “ABC/M: Which

Companies Have Success?” The Journal of Corporate Accounting & Finance,

March/April 2001, pp 35-44. See also, Douglas T. Hicks, “Good Decisions

Require Good Models: Developing Activity-Based Solutions that Work for

Decision Makers,” Cost Management, March/April 2005, pp 32-40, and

Michael D. Shields and Michael A. McEwen, “Implementing Activity-Based

Costing Systems Successfully,” Cost Management, Winter, 1996, pp15-22.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-20

PROBLEMS

5-38 Activity-Based Costing, Value Chain Analysis (25 min)

1. Manufacturing cost (total, and per unit):

Prime manufacturing cost (80 ×$1,250) =

$100,000

Manufacturing overhead:

Materials handling (80 × 105 × $0.50) =

$4,200

Machining (80 × 3 × $51.00) =

$12,240

Assembly (80 × 105 × $2.85) =

$23,940

Inspection (80 × $30.00) =

$2,400

Total Manufacturing Cost =

$142,780

Number of units =

÷ 80

Manufacturing cost per unit =

$1,784.75

2. Computation of full cost:

Upstream activity costs =

$180.00

8.13%

Manufacturing costs =

$1,784.75

80.58%

Downstream activity costs =

$250.00

11.29%

Full Product Cost per Unit =

$2,214.75

100.00%

Strategic implications:

(1) Knowing the full cost of a product including upstream and

downstream costs allows the firm to be aware of all costs attributable

differentiation strategy in both the new product design and the

customer service.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-21

5-38 (continued)

3. The total value chain cost provides the firm a long-term perspective of

the product cost, in addition to the short term manufacturing cost.

5-39 Resource and Activity-Based Cost Drivers (25 min)

1. The activity based cost pools are determined from the percent-of-use

information; for example, total setup cost = $157,500 = (.15 × $850,000)

+ (.2 × $150,000).

Factory

Costs

Setup

Assembly

Inspect

&Finishing

Packaging

Salaries

$ 850,000

$127,500

$ 467,500

$ 170,000

$ 85,000

Supplies

$ 150,000

$ 30,000

$ 90,000

$ 30,000

$ –

Factory

Expense

$ 550,000

$ –

$ 440,000

$ 110,000

$ –

$1,550,000

$157,500

$ 997,500

$ 310,000

$ 85,000

2. The activity rates are determined as follows:

Safe-V

Safe-T

Total Activity

Consumption

Activity

Costs

Activity-

based

Rates

Batches

250

600

850

$157,500

$185.29

Units

60,000

72,000

132,000

$997,500

$ 7.56

Finishing hours,

per unit

0.2

0.3

33,600

$310,000

$ 9.23

Packaging

0.1

0.15

16,800

$85,000

$ 5.06

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-22

3. The per unit activity-based costs are $14.18 for Safe-V and $18.63 for the

Safe-T

Activity Requirements

Activity-Based

Costs/Unit

Safe-V

Safe-T

Safe-V

Safe-T

Setup

250

600

$ 0.77

$ 1.54

Assembly

60,000

72,000

$ 7.56

$ 7.56

Inspect and Finish

0.2

0.3

$ 1.85

$ 2.77

Packaging

0.1

0.15

$ 0.51

$ 0.76

Materials per unit

$3.50

$6.00

$ 3.50

$ 6.00

Total Cost per Unit

$ 14.180

$ 18.628

5-39 (continued)

4. The activity-based information can be used by EEI to set prices and

assess the profitability of its two product lines.

5. The collection of more accurate cost driver data can only be justified when

the cost of data collection and analysis is less than the expected benefit.

Management would have to decide whether they think their decisions would

change based on the more accurate data. If not, then the extra effort and cost

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-23

5-40 Activity-Based Costing; Customer Group Cost Analysis (40 min)

1. First, obtain the total levels for activity cost drivers:

Product Lines

Value

Quality

Luxury

Total

Units produced

15,000

5,000

500

20,500

Direct materials cost per unit

$80

$50

$110

Total direct materials cost

$ 1,505,000

Number of parts per unit

30

50

120

Total parts

760,000

Direct labor hours per unit

4

5

7

Total labor hours

88,500

Machine hours per unit

3

7

15

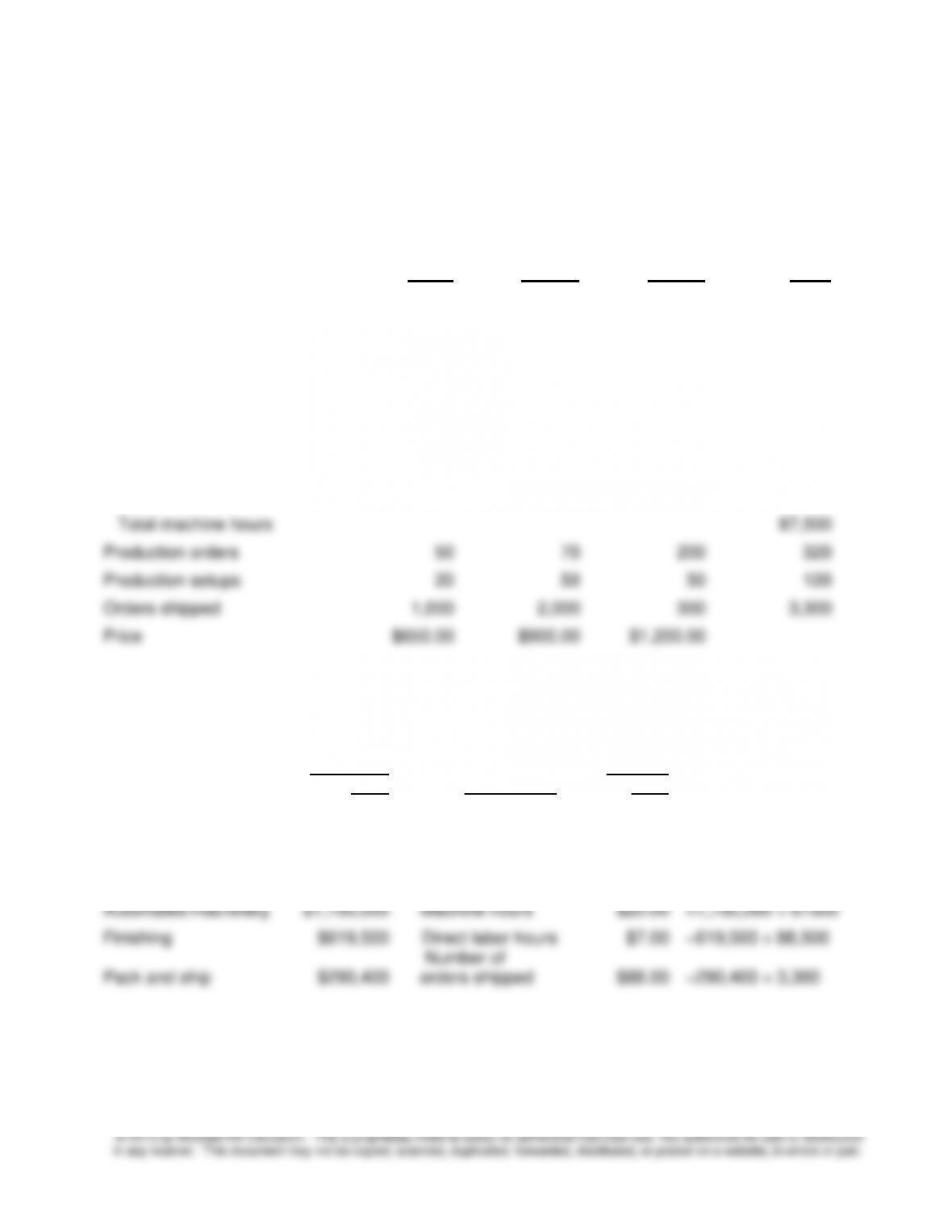

Total machine hours

87,500

Production orders

50

70

200

320

Production setups

20

50

50

120

Orders shipped

1,000

2,000

300

3,300

Price

$650.00

$900.00

$1,200.00

Then, obtain the activity rates:

Budgeted

Cost

Cost Driver

Activity

Rate

Materials handling

$349,600

Number of parts

$0.46

=$349,600 ÷ 760,000

Product scheduling

$160,000

Number of

production orders

$500.00

=160,000 ÷ 320

Setup labor

$216,000

Number of setups

$1,800.00

=216,000 ÷ 120

Automated machinery

$1,750,000

Machine hours

$20.00

=1,750,000 ÷ 87500

Finishing

$619,500

Direct labor hours

$7.00

=619,500 ÷ 88,500

Pack and ship

$290,400

Number of

orders shipped

$88.00

=290,400 ÷ 3,300

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-24

5-40 (continued –1)

The activity-based cost per unit and total cost is as follows:

Value

Quality

Luxury

Direct Materials

$80.00

$50.00

$110.00

Direct Labor

$48.00

$60.00

$84.00

Overhead:

Materials handling

$13.80

$23.00

$55.20

Product Scheduling

$1.67

$7.00

$200.00

Setup Labor

$2.40

$18.00

$180.00

Automated Machinery

$60.00

$140.00

$300.00

Finishing

$28.00

$35.00

$49.00

Pack and Ship

$5.87

$35.20

$52.80

Total ABC Overhead

$111.74

$258.20

$837.00

Unit ABC Cost

$239.74

$368.20

$1,031.00

Total ABC Cost

$3,596,100

$1,841,000

$515,500

2. Volume-based results $3,385,500 ÷ 88,500 DLH = $38.25 per DLH

Value

Quality

Luxury

Direct Materials

$80.00

$50.00

$110.00

Direct Labor

$48.00

$60.00

$84.00

Overhead

$153.00

$191.25

$267.75

Cost per unit

$281.00

$301.25

$461.75

Total Cost

$4,215,000

$1,506,250

$230,875

Note how the volume-based method significantly undercosts the Luxury

group (the low-volume group), while overcosting the Value group (the

high-volume customer group).

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-25

5-40 (continued –2)

3. The new activity rates based on practical capacity are as follows.

Budgeted

Cost

Cost Driver

Practical

Capacity

Practical

Capacity-Based

Rates

Materials handling

$ 349,600

Number of parts

990,000

$ 0.35

Product scheduling

160,000

Number of

production orders

800

200.00

Setup labor

216,000

Number of setups

200

1,080.00

Automated machinery

1,750,000

Machine hours

100,000

17.50

Finishing

619,500

Direct labor hours

123,900

5.00

Pack and ship

290,400

Number of

orders shipped

5,000

58.08

$ 3,385,500

Note that the rates have changed significantly from the calculations in part 1

above, because there is a significant level of unused capacity in many of the

activities. This information could be used by management to calculate unit

ABC-based costs using the practical capacity rates, and thereby identify the

cost of unused capacity. Moreover, the information about capacity utilization

can be used to help bring resource spending in line with resource usage. As

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-26

5-40 (continued – 3)

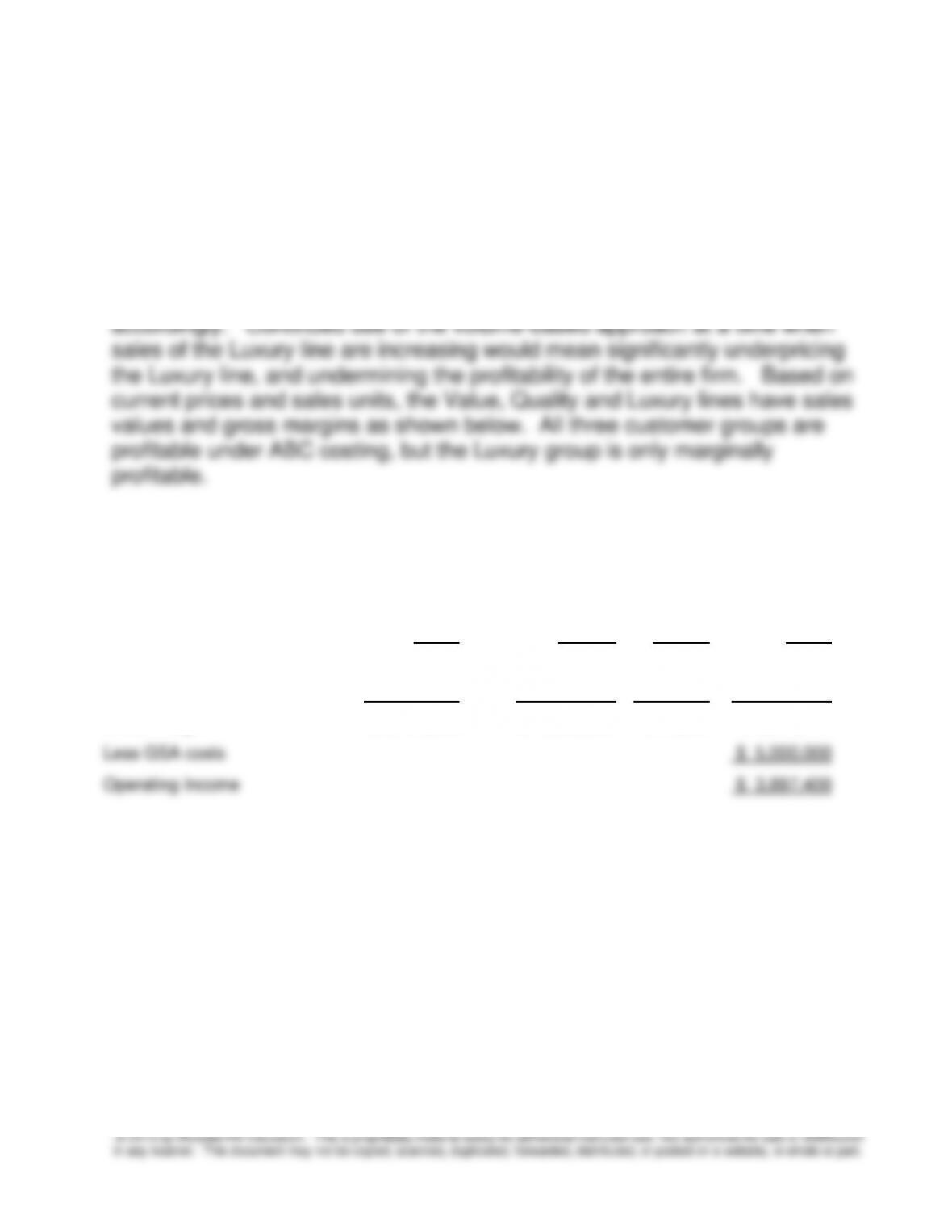

4. The ABC costing shows clearly how expensive the Luxury group is to

produce. The volume-based approach fails to account for the activity usage

of the Luxury line, and undercosts it significantly. ABC allows LFI to better

understand how its costs will increase with the expected increased production

of the Luxury line, and how it will have to adapt its pricing practices

Profitability by Customer Group

Profitability by Customer Group

Value

Quality

Luxury

Total

Sales Value of each product

$ 9,750,000

$ 4,500,000

$600,000

$ 14,850,000

Less ABC Manufacturing cost

$ 3,596,100

$ 1,841,000

$515,500

$ 5,952,600

Gross Margin

$ 6,154,000

$ 2,659,000

$ 84,500

$ 8,897,400

Less GSA costs

$ 5,000,000

Operating Income

$ 3,897,400

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-27

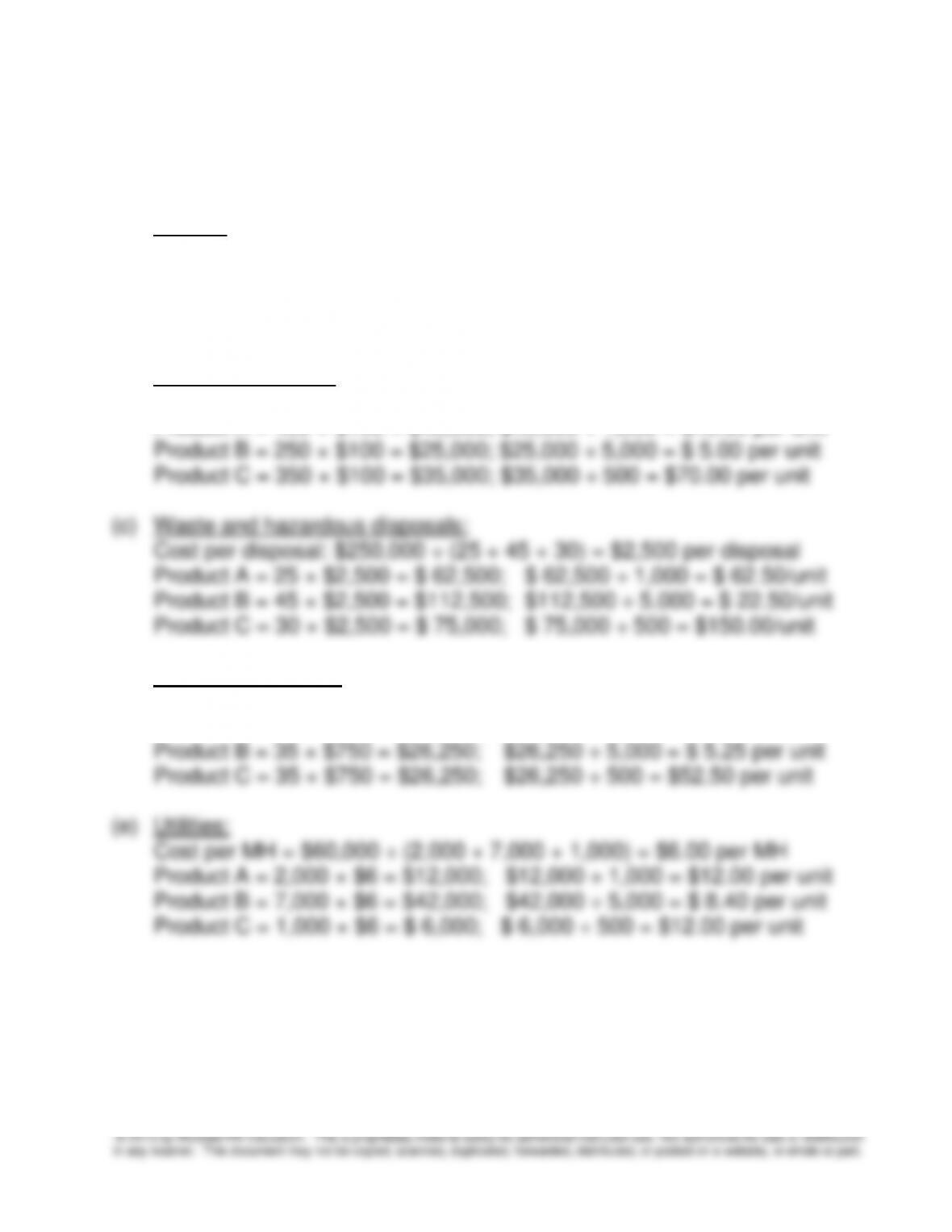

5-41 Volume-based Costing Versus ABC (35 min)

Product A

Product B

Product C

Materials

$50.00

$114.40

$65.00

Labor

$20.00

$12.00

$10.00

Overhead*

$116.00

$69.60

$58.00

Total Cost

$186.00

$196.00

$133.00

*overhead is applied based on direct labor dollars so the rate is:

$5.80 per Direct labor dollar = $493,000 ÷

[($20×1,000)+($12×5,000)+($10×500)]

$116 = $5.8×20; $69.60 = $5.8×12; $58 = $5.8×10

1. Current Costing system

Product A

Product B

Product C

Actual Selling Price

$280.00

$250.00

$300.00

Product Manufacturing Cost

$186.00

$196.00

$133.00

Gross Margin

$94.00

$54.00

$167.00

Gross Margin Ratio

33.57%

21.60%

55.67%

Based on the current cost data, product B is the least profitable product

with a gross margin per unit of $54.00 (21.6%) and product C is the most

profitable product with a gross margin per unit of $167.00 (55.67%).

Product costs based on the activity-based costing system

(calculate on per unit basis)

Product A

Product B

Product C

Direct Materials

50.00

114.40

65.00

Direct Labor

20.00

12.00

10.00

Factory Overhead:

Setups (a)

1.60

0.80

4.80

Materials Handling (b)

40.00

5.00

70.00

Hazardous Control (c)

62.50

22.50

150.00

Quality Control (d)

22.50

5.25

52.50

Utilities (e)

12.00

8.40

12.00

TOTAL

208.60

168.35

364.30

Actual Selling Price

$280.00

$250.00

$300.00

Product Manufacturing Cost

208.60

168.35

364.30

Gross Margin

$71.40

$81.65

($64.30)

Gross Margin Percentage

25.50%

32.66%

-21.43%

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-28

5-41 (continued –1)

Notes:

(a) Setups:

Cost per setup: $8,000 ÷ (2 + 5 + 3) =$800 per setup

Product A = 2 × $800 = $1,600; $1,600 ÷1,000 = $1.60 per unit

Product B = 5 × $800 = $4,000; $4,000 ÷5,000 = $0.80 per unit

Product C = 3 × $800 = $2,400; $2,400 ÷500 = $4.80 per unit

(b) Materials handling:

Cost per pound = $100,000 ÷ (400 + 250 + 350) = $100 per pound

Product A = 400 × $100 = $40,000; $40,000 ÷ 1,000 = $40.00 per unit

(d) Quality inspections:

Cost per inspection = $75,000 ÷ (30 + 35 + 35) = $750 per inspection

Product A = 30 × $750 = $22,500; $22,500 ÷ 1,000 = $22.50 per unit

5-29

5-41 (continued-2)

2. Comparison of reported product costs, new target price, actual selling price,

and gross margin (loss):

Product A

Product B

Product C

Product Costs:

Direct-labor system

$186.00

$196.00

$133.00

Activity system

$208.60

$168.35

$364.30

ABC– based product costs:

Target price

$312.90

$252.53

$546.45

Actual selling price

$280.00

$250.00

$300.00

Difference in price

-32.90

-2.52

-246.45

Direct-labor system:

Gross Margin

$94.00

$54.00

$167.00

Gross Margin ratio

33.57%

21.60%

55.67%

ABC system:

Gross Margin

$71.40

$81.65

-$64.30

Gross Margin ratio

25.50%

32.66%

-21.43%

3. Strategic and Competitive Analysis

a. Emphasizing Product C as suggested by the current direct-

labor-cost based overhead costing system is likely to harm the

b. If the actual selling prices of products A & B are fair market

prices for these products and a markup of 150% is a common

industry practice, the firm needs to examine the manufacturing

cost of product A. The fact that the firm’s target price,

A.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-30

5-42 Activity-Based Costing (35-40 min)

(“Miami Valley Architects, Inc.” by Beth M. Chaffman, and John Talbott,

Management Accounting Campus Report, Fall 1992, p.4)

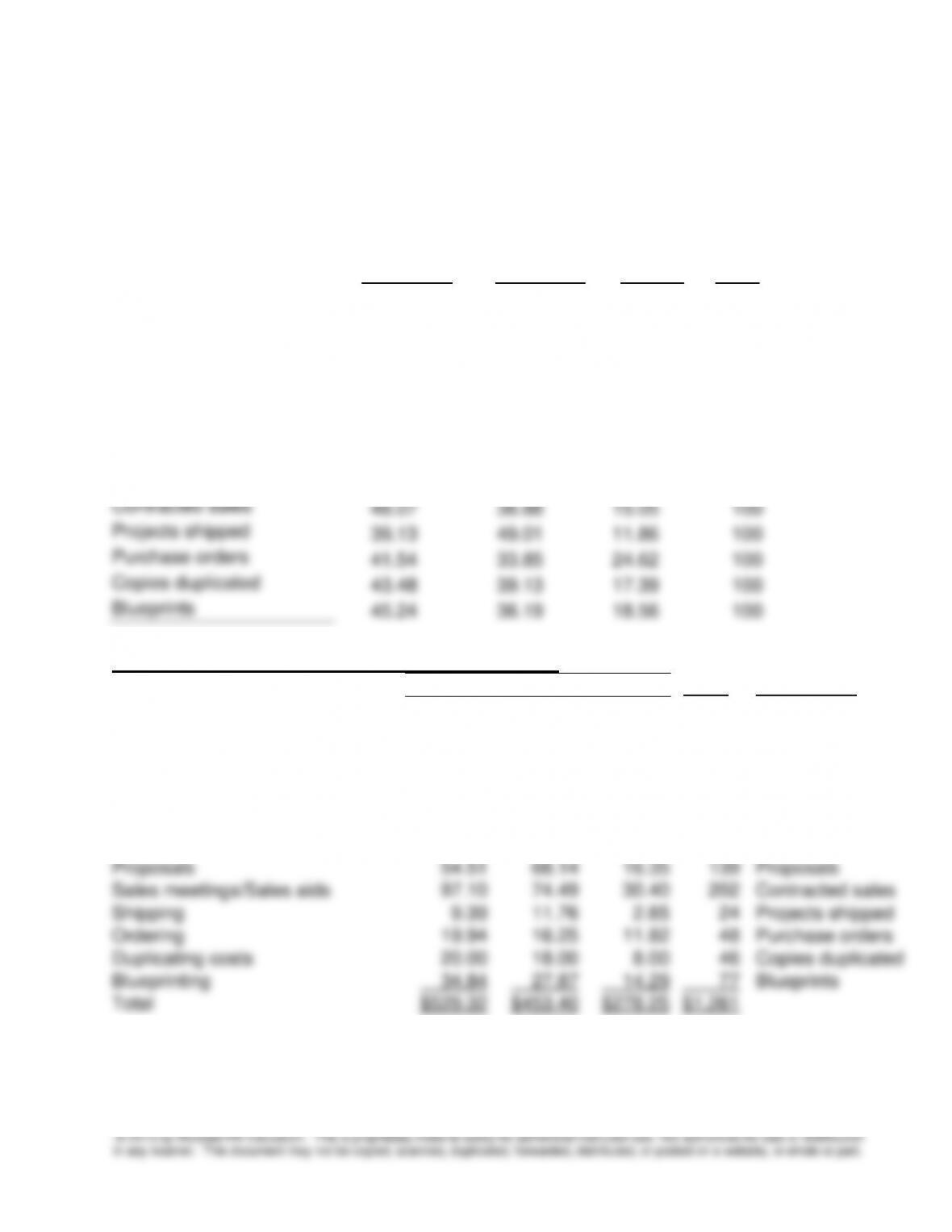

1. Overhead Cost assigned to each branch under the ABC costing:

Columbus

Cincinnati

Dayton

Total

Direct labor dollar

37.61%

31.19%

31.20%

100%

Timesheet entries

45.11

28.57

26.32

100

Vendor invoices

44.93

37.44

17.62

100

Client invoices

52.13

39.36

8.51

100

Employees

34.33

38.81

26.87

100

New hires

42.11

21.05

36.84

100

Insurance claims filed

34.33

38.81

26.87

100

Proposals

39.22

49.02

11.76

100

Contracted sales

48.07

36.88

15.05

100

Projects shipped

39.13

49.01

11.86

100

Purchase orders

41.54

33.85

24.62

100

Copies duplicated

43.48

39.13

17.39

100

Blueprints

45.24

36.19

18.56

100

Activity-based overhead allocation (000s)

Colum.

Cinci.

Dayton

Total

Cost Driver

General administration

$153.82

$127.56

$127.60

$ 409

Direct labor dollar

Project costing

21.65

13.71

12.63

48

Timesheet entries

Accounts payable/receiving

62.46

52.05

24.49

139

Vendor invoices

Accounts receivable

24.50

18.50

4.00

47

Client invoices

Payroll/Mail sort & delivery

10.30

11.64

8.06

30

Employees

Personnel recruiting

16.00

8.00

14.00

38

New hires

Employee insurance process.

4.81

5.43

3.76

14

Insurance claims filed

Proposals

54.51

68.14

16.35

139

Proposals

Sales meetings/Sales aids

97.10

74.49

30.40

202

Contracted sales

Shipping

9.39

11.76

2.85

24

Projects shipped

Ordering

19.94

16.25

11.82

48

Purchase orders

Duplicating costs

20.00

18.00

8.00

46

Copies duplicated

Blueprinting

34.84

27.87

14.29

77

Blueprints

Total

$529.32

$453.40

$278.25

$1,261

Note: Results will vary slightly if % used from part 1 are rounded to 2 places