Chapter 11 – Decision Making with a Strategic Emphasis

11–31

11–30 (continued-2)

More generally, the minimum selling price per unit = incremental

costs (variable + fixed + opportunity):

Out-of-pocket costs:

Variable out-of-pocket costs per meal $2.00

Fixed out-of-pocket costs per meal $0

Therefore, short-term profits increase by taking on the additional

business.

The idea of agreeing to serve 200 patrons on any given day presents

a problem with limited capacity. In this case, 100 of the regular

customers would have to look elsewhere for lunch on these days, at a

follows:

Number of patrons per month 200

Special-order price offered by tour company $3.00 (given)

Incremental costs per tour-bus meal:

Variable out–of-pocket costs per meal $2.00

Fixed out-of-pocket costs per meal $0.00

Chapter 11 – Decision Making with a Strategic Emphasis

11–32

PROBLEMS

11–31 Special Order; Strategy; International (60 min)

1. The standard direct labor hour (DLH) per finished valve is ½ hour.

Therefore, 30,000 units per month would require 15,000 DLHs.

2. The analysis of accepting the Glasgow proposal is presented below.

Totals for

Per unit 120,000 units

Incremental revenue $21.00 $2,520,000

Incremental costs

Variable costs:

Direct materials 6.00 720,000

Direct labor 8.00 960,000

Variable overhead 3.00 360,000

3. The minimum unit price that Williams could accept without reducing

operating income must cover variable costs plus the additional fixed

costs; in this case, there are no opportunity costs. The $30 suggested

selling price is irrelevant for the special order:

Incremental variable costs, per unit:

Chapter 11 – Decision Making with a Strategic Emphasis

11–33

Problem 11-31(continued-1)

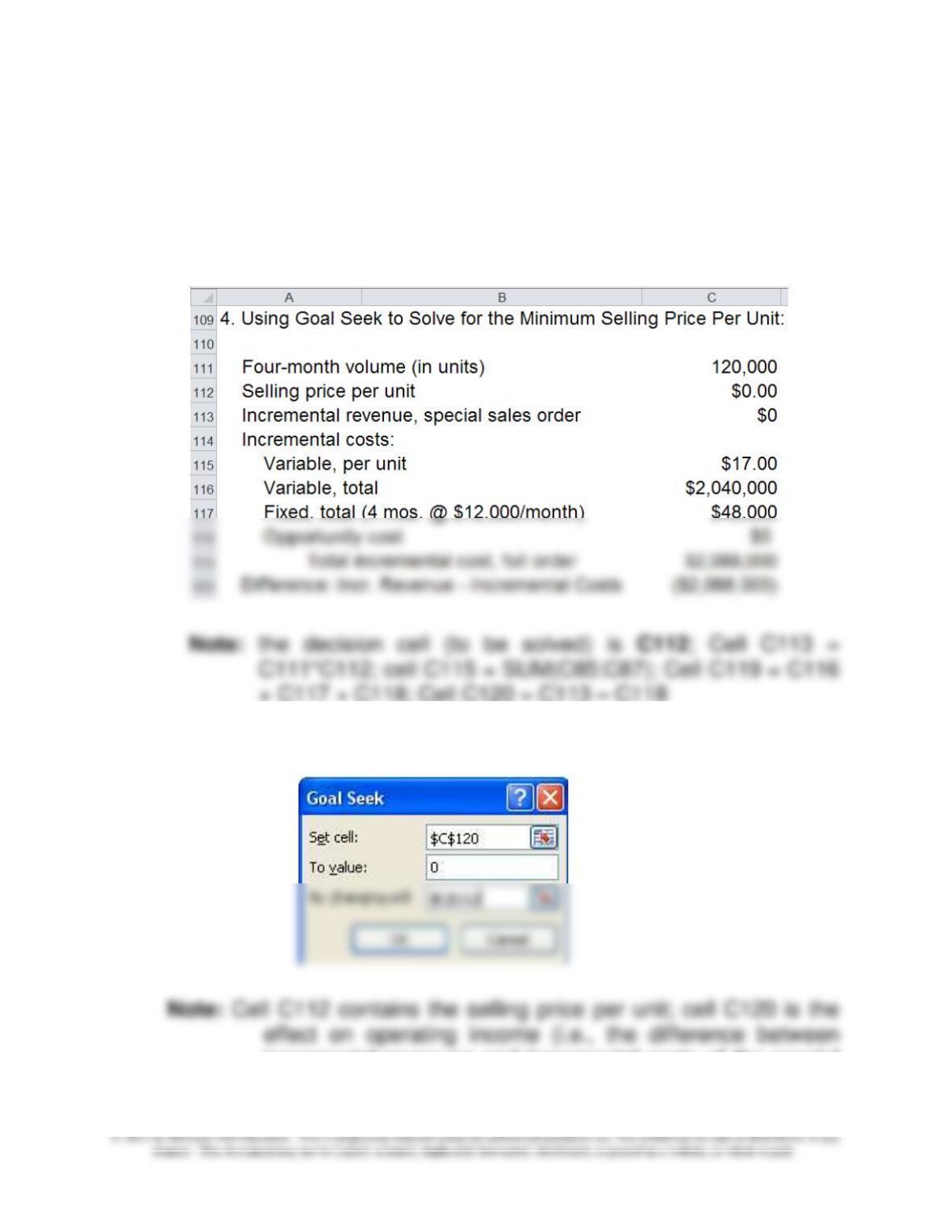

4. Use the Goal Seek option in Excel to solve for the minimum unit price

determined in 3 above.

Step #1: Define the Appropriate Equation to Be Solved

+ C117 + C118; Cell C120 = C113 – C118

Step #2: Run Goal Seek (to Solve the Equation)

incremental revenues and incremental costs of the special

sales order).

Chapter 11 – Decision Making with a Strategic Emphasis

11–34

Problem 11-31 (continued-2)

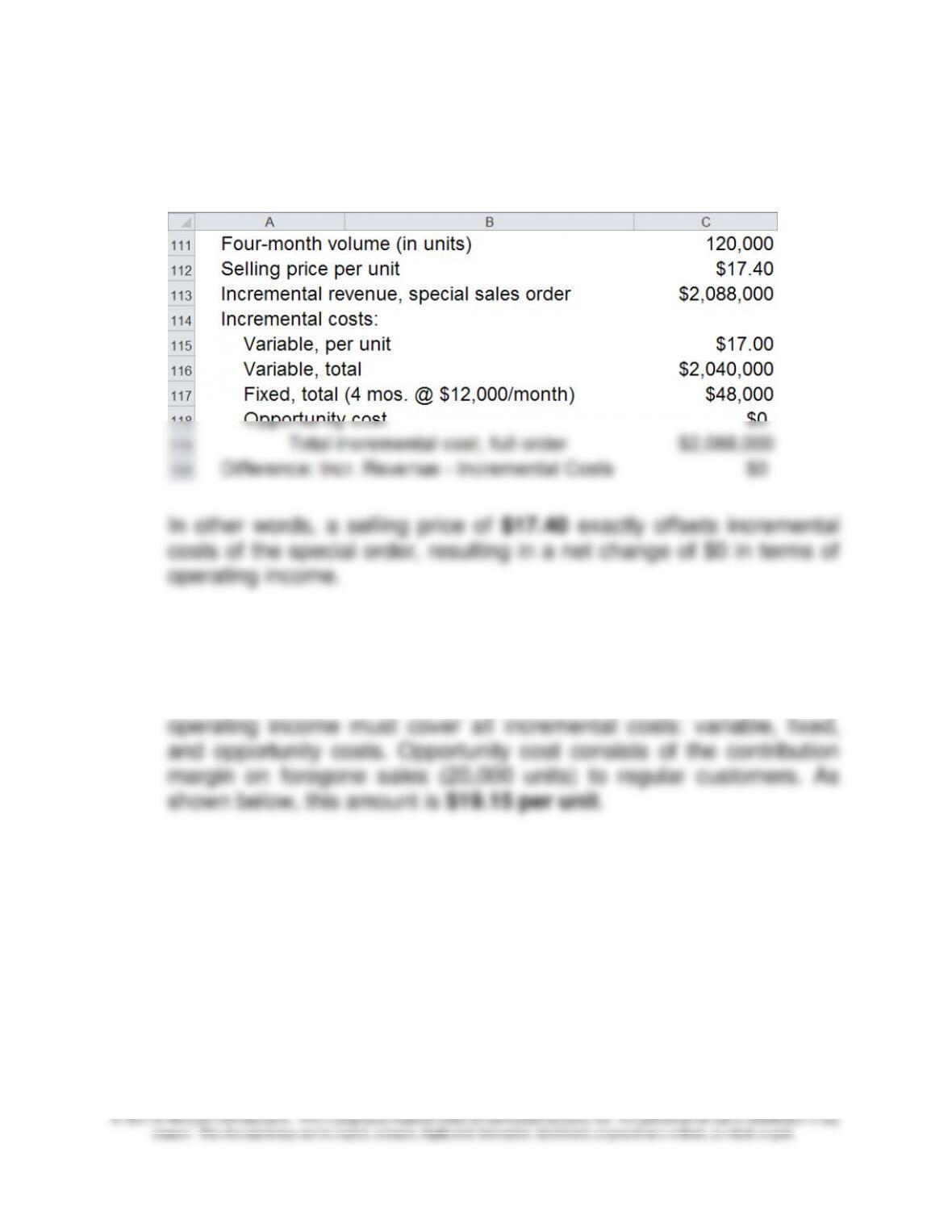

Step #3: Results

5. Determination of minimum (i.e., breakeven) selling price per unit in

the face of opportunity costs (lost sales to regular customers):

The minimum unit price that Williams could accept without reducing

Chapter 11 – Decision Making with a Strategic Emphasis

11–35

Problem 11-31 (continued-3)

Incremental variable cost, per unit:

Direct materials $6.00

Direct labor $8.00

Variable overhead $3.00 $17.00

Incremental fixed costs, per unit ($48,000 ÷ 120,000 units) 0.40

Opportunity Cost:

Total lost sales (in units) (4 × 5,000 units) 20,000

Regular selling price per unit $30.00

6. Williams Company should consider the following strategic factors before

accepting the Glasgow Industries order:

• The effect of the special order on Williams’ sales at regular

prices.

• The possibility of future sales to Glasgow Industries and the

effects of participating in the international marketplace.

• The company’s “relevant range” of activity and whether or not

equipment.

Chapter 11 – Decision Making with a Strategic Emphasis

11–36

Problem 11-31(continued-4)

• The strategic advantage of the long-term commitment from

• The ethical and competitive issues of helping a competitor in

distress.

7. The international issues Williams should consider include:

• What customs duties and import/export restrictions might affect

the special order and any future business with Glasgow?

11–37

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

11–32 Special Order (40-45 min)

1. Average cost-per-unit calculations, with and without the special sales

order:

Old (prior to special order) average cost per unit:

Total Cost/month $1,275,000

Total Output/month 7,500

Average cost/unit $170.00

Recalculated Average Cost, including Special Sales Order:

Neither of the above two cost figures is relevant to the decision at hand:

both include sunk costs in the form of fixed manufacturing overhead and

fixed marketing costs, both of which are “sunk” with respect to the

decision at hand. That is, these costs will likely be the same (in total)

regardless of whether or not we accept the special sales order. As such,

they are not relevant to this decision.

2. Short-term profit effect of accepting the special sales order:

Price of special order $100

Positive contribution accept the special sales order

3. Breakeven selling price per unit on the special sales order:

Chapter 11 – Decision Making with a Strategic Emphasis

11–38

11-32 (Continued)

The breakeven selling price is the price that would leave the operating

profit for the company unchanged. Alternatively, this can be defined as

the sum of “relevant costs,” that is, incremental variable costs,

incremental fixed costs (if any), and opportunity cost (if any).

In the present case, relevant cost includes only incremental variable cost

(i.e., there is no opportunity cost and there are no incremental fixed

costs):

Relevant Costs:

4. Other considerations:

a. Is the order likely to lead to further regular business with this

customer?

b. Is the order in the strategic best interest of the firm, for example,

tooling or set up costs, etc.

d. See part 5 below.

Chapter 11 – Decision Making with a Strategic Emphasis

11–39

5. The controller, LePenn, has a conflict of interest in the sourcing of raw

materials for the firm. Cathy has the ethical responsibility under the IMA

Chapter 11 – Decision Making with a Strategic Emphasis

11–40

11–33 Special Order (45-60 min)

1. In general, relevant cost equals the sum of out–of-pocket costs (variable

+ fixed), plus opportunity cost (if any). In the present case, these costs

total $140,000, as follows:

Out-of-Pocket Costs:

Variable costs:

Manufacturing cost ($15 per unit) $75,000

Fixed costs:

One-Time Packing & Delivery Cost $2,000

Opportunity Cost:

2. Operating income with the special order will decrease by $15,000. The

only relevant variable costs are the $15 variable manufacturing cost

($15 × 5,000 = $75,000 total), since marketing costs are not charged for

the special order. Other relevant costs include the one-time delivery/

packing cost of $2,000 and the (opportunity) cost of lost sales. Since the

Summary of relevant costs:

Variable manufacturing costs ($15 × 5,000) $ 75,000

One-time delivery costs 2,000

Cost of lost sales (per above) 63,000

11-33 (Continued-1)

Since the relevant costs of $140,000 exceed the price of the special

order ($125,000), operating income would decrease by $15,000 if the

special order is accepted.

3. The breakeven selling price is the price that just equals total relevant

cost of the special sales order. Put another way, the breakeven price is

the selling price per unit that would leave operating income unchanged.

Total relevant cost (from Part 1 above) = $140,000

4. Comparative income statements (contribution format), with and without

special order:

Sales:

Regular (@$38/unit) $760,000 $646,000

Special order (@ $28/unit) $0 $760,000 $140,000 $786,000

Less: Variable Costs:

Manufacturing (@$15/unit) $300,000 $330,000

Marketing (@ $2/unit) $40,000 $340,000 $34,000 $364,000

Contribution Margin $420,000 $422,000

Less: Fixed Costs:

Manufacturing $240,000 $240,000

Marketing $40,000 $40,000

One-Time Packing/Delivery

$0 $280,000 $2,000 $282,000

Operating Income $140,000 $140,000

Current Situation

Current Situation +

Special Sales Order

Chapter 11 – Decision Making with a Strategic Emphasis

11–42

Note: Variable selling costs ($2/unit) are not incurred on the special

sale units. Thus, if the special sales units are sold at $28.00 per

unit, operating income is left unchanged.

11–33 (continued-2)

5. There are both ethical and strategic issues for GGI. From a strategic

view, GGI would suffer severe damage to its reputation if APAC were to

have any problems with the purity of the special order. One of the

reasons APAC has requested the special order from GGI is because of

its reputation for quality. It is clear that GGI competes on differentiation,

with quality being a critical success factor.

Also, there is an ethical issue. The use of a competitor’s materials would

deceive APAC who is expecting the highest quality product from GGI.

Chapter 11 – Decision Making with a Strategic Emphasis

11–34 Special Order; ABC Costing (25-30 min)

1. Total Fixed Manufacturing Cost and Breakdown into Components:

Total fixed manufacturing costs are $12/unit × 20,000 units = $240,000:

Total batch-related costs ($8/unit × 20,000 units) = $160,000

Incremental costs ($5,000/batch × 20 batches) = $100,000

2.

3. The total relevant cost of $135,000 is greater than the special order

price of $125,000, so GGI should not accept the special order. If they did

No. of incremental batches, special order = (22,000-20,000)/1,000 =

= [current capacity (in units) – current usage (in units)] ÷ 1,000 units/batch 2

Relevant cost for the special order:

Variable manufacturing cost ($15/unit × 5,000 units) = $75,000

Incremental batch-related ovh costs (2 batches × $5,000/batch) = $10,000

One-time delivery cost = $2,000

CM on lost sales (opportunity cost):

Sales ($38/unit × 3,000 units) = $114,000

Less: variable costs ($15 + $2) × 3,000 units = $51,000

Less: cost for three batches (@$5,000 per batch) = $15,000 $48,000

Total relevant cost for the special order $135,000

Chapter 11 – Decision Making with a Strategic Emphasis

11–44

11-35 Make or Buy (45 minutes)

1. Since the per-unit contribution margin for manufactured fans ($24) is

higher than for purchased fans ($12), the company should manufacture as

many fans as possible (15,000), and purchase the remainder (5,000) from

Harris Products.

Total Relevant Costs Relevant Costs

Cost to Manufacture to Purchase

Selling price per unit $72.00 $72.00 $72.00

Cost per unit: $46.00

Electric motor $6.00 $6.00

Other parts $8.00 $8.00

Direct labor ($15.00/hr.) $15.00 $15.00

Manufacturing overhead $15.00 * $5.00

Selling and adm. cost $20.00 $64.00 ** $14.00 $14.00

Contribution per unit $24.00 $12.00

* Of the total per unit manufacturing overhead of $15, $10 is fixed ($100,000/10,000

units) and the remaining $5 is variable.

** Of the total per unit selling and administrative cost, $6 is given as fixed, and the

remaining $14 is variable.

The total contribution margin from this plan would be:

(15,000units × $24/unit) + (5,000units × $12/unit) = $420,000

2. The total contribution margin for the marine pumps = $21 per unit ×

25,000 units = $525,000

Since the total contribution margin from making pumps ($525,000) is

Chapter 11 – Decision Making with a Strategic Emphasis

11-35 (Continued-1)

3. Some of the possible strategic factors to consider are:

Re: The pumps:

• Will the sale of pumps introduce Martens to new markets and new

customers that might benefit other product lines?

• Can Martens compete in the marine pump market? How

competitive is this market, and what are the critical success factors

that are likely to lead to success for Martens?

• How reliable are the estimates used to develop the predictions for

revenues and costs for the pumps? How reliable is the market

research that predicted growth in pump sales?

• Will the sale of pumps affect Martens’ image in either a positive or

negative fashion? For example, will Martens’ current customers

view Martens as a high quality/innovative manufacturer of pumps?

• How long is the expected growth in pump sales expected to

Selling price per unit 60.00$

Costs per unit

Electric motor 5.50

Other parts 7.00

Direct labor ($15.00/hr.) 7.50

Manufacturing overhead 5.00 (1)

Selling and adm. cost 14.00

(2)

fixed, and the remaining $14 is variable.

Relevant Costs

for Pumps

Price and