Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-29

Comparison

Incrrease

Total Total Batch Batch Total Total Batch Batch Total Total Batch Batch (Drop) in

Cost Cost Total Gross Cost Cost Total Gross Cost Cost Total Gross Gross

Product per Reel per Batch Revenues Margin per Reel per Batch Revenues Margin per Reel per Batch Revenues Margin Margin

A9,840$ 492,000$ 630,000$ 138,000$ 11,702$ 585,103$ 630,000$ 44,897$ 119% 119% 100% 33%

-67%

B10,660 21,320 27,000 5,680 15,812 31,625 27,000 (4,625) 148% 148% 100% n/a

-181%

C11,480 401,800 497,000 95,200 13,332 466,606 497,000 30,394 116% 116% 100% 32%

-68%

D15,170 2,654,750 3,412,500 757,750 14,209 2,486,536 3,412,500 925,964 94% 94% 100% 122% 22%

3,569,870$ 4,566,500$ 996,630$ 3,569,870$ 4,566,500$ 996,630$

One Step Cost Analysis

ABC Cost Analysis

ABC Cost / One Step Cost

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-30

Key points from ABC Analysis

1. Products A,B, and C are more costly than thought, because of the high cost of grade change (has to

be averaged over the number of reels, smaller for A,B, and C) and the high cost of slitting (for A and

C). Note that the grade changes are made between batches, while slitting is done for each reel,

so the effect of the slitting is potentially much greater than the effect of grade change. This does not

happen for product B however, since there are so few reels for product B, so for product B, the main

effect on cost is the grade change – so few reels per batch.

2. Gross margins after ABC are much smaller for A, B and C, and B’s gross margin is negative. Need

to consider the pricing issues for B and whether we can make this product more profitable.

3. How should we use the ABC information in pricing, in planning, and in performance evaluation?

Increase the price of B

ABC information is better for planning which products to drop, keep or add

ABC information is better for performance evaluation

4 How would you change the competitive strategy of the company? What is the role of cost

information in determining the strategy of the company?

Reduce product variety

Batch size

Slitting, or charge appropriately for it

Go to a time based costing system

5. How would analysis of the value chain help FHPC meet its strategic goals?

• Look for ways to add value and reduce costs

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-31

The Value Chain

Timber; do we harvest our own timber?

Sorting and preparing timber; receiving the lumber in the pulp plant

Pulp manufacturing

Debarking; a 16×100 ft drum; tumbling the logs

Chipping; into 1” cubes

Digesting; heat and soak with chemicals

Bleaching; brown to white

Paperboard production

Headbox; mix pulp cubes with water and chemicals

Wire; paper mixture is applied to wire mesh that travels through a press and forces the

Pulp mixture against the wire to remove water

Drying; cylindrical dryers and steam are used

Rolling; into “parent” rolls

Further processing

Coating

Rewinding and slitting

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-32

5-5 Harrison Products, Inc

The Harrison Products Inc (HPI) case is based on disguised information and data taken from that of a U.S.

multinational company. Many of the costing and strategic issues addressed in the case are faced by that

company. The main issues are (1) what costing system to use and (2) what manufacturing strategy to

use to best serve the company’s customers and to meet the competitive challenge of low cost. The case

is intended for the undergraduate cost course, the advanced cost/managerial course and the MBA

managerial course.

Because of the amount of data involved and the analysis required, Excel is strongly recommended for the

solution of the case.

The main learning objectives of the case are to examine the application of volume-based and activity-

based costing in a manufacturing context. There are three unique issues in the case:

1. How to determine the cost driver for setup costs. The student is asked to determine the

amount of ABC cost allocated to a sample of jobs using two different assumptions of how

2. To understand the possible influence of batch size not only on batch level costs but also on

unit level costs. In the case data, which (while disguised) reflects the actual experience of

3. To understand how manufacturing strategy can affect product costs. In this case, one of the

company’s plants was designed for relatively large batch sizes and the other was designed for

smaller batches. Both batch-level and unit-level costs are affected by these design decisions.

Answers to Questions:

1, 2, and 3: The answers to parts 1,2 and 3 are shown in TN-1. The solution also shows the

operating margin per unit which is useful in the discussion of the requirement 4. The calculation of the

volume-based and activity-based rates is shown on the right-hand side of the Exhibit. It is highly

4. In comparing the results for parts 1,2 and 3, it is apparent that the volume-based approach, as

it is based only on volume, produces the same unit costs for each job, irrespective of job size.

Thus, the operating margin per unit is the same for each job ($0.30 for the Los Angeles plant

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-33

The standard deviation of the operating margin per unit is shown for each of the three

methods and each plant; the variation is greatest for activity-based costing (part 2 method)

and of course zero for the volume-based method.

The activity-based methods in parts 2 and 3 are preferred over the volume-based method

because they appropriately apply the job-related setup costs to each job and thereby

recognizing the more accurate cost for each job. The method in part 3 would be preferred

since it takes into account the additional clean-up and preparation time required after the

larger jobs. Generally, determining which of the two activity-based methods is best would

require a careful study of what drives setup time and costs, information which is not available

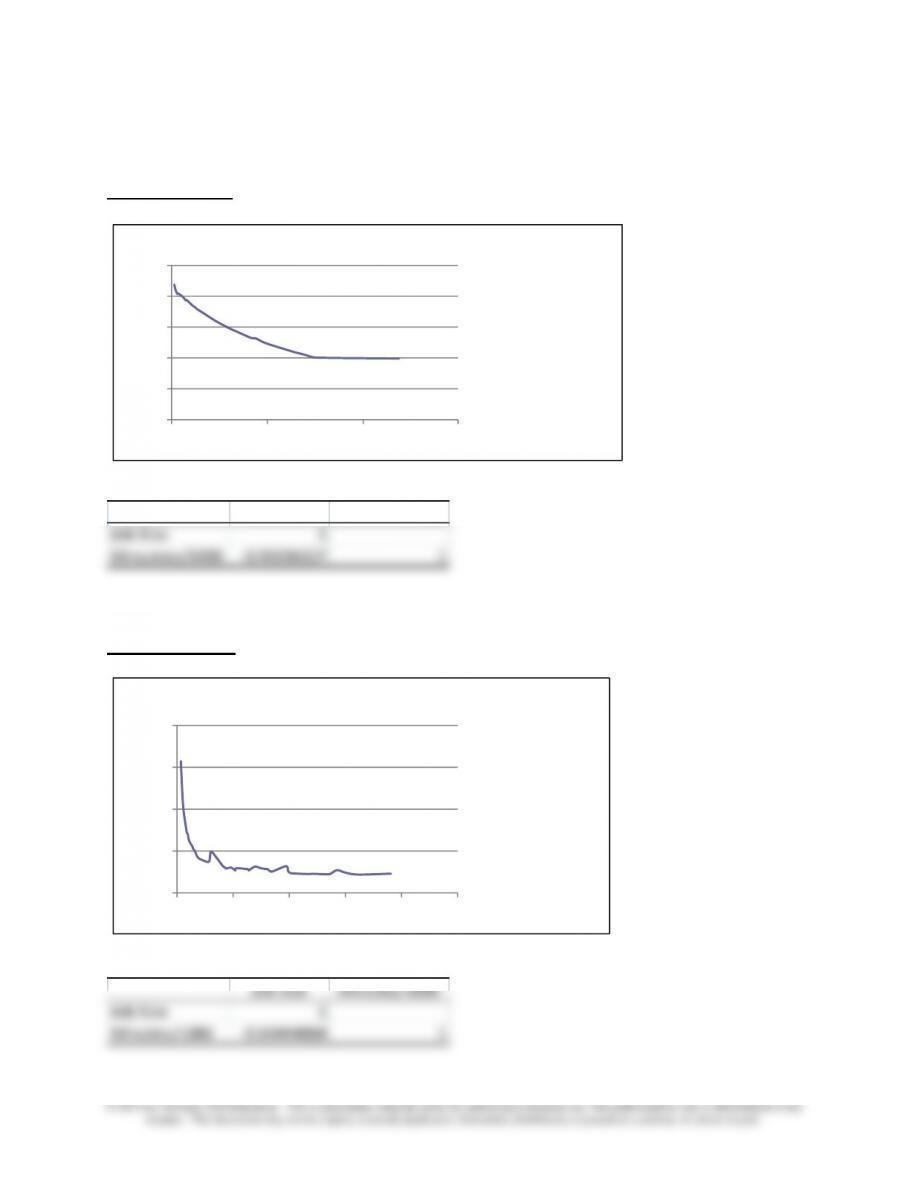

5. A graphical and correlation analysis for both plants, showing the relationship between job

size and runtime is in Exhibit TN-2. The graphs in particular show clearly that the Los

Angeles plant, the newer plant, has faster runtime for smaller jobs. This can be seen from

the graph and also by reviewing the 6-8 smallest jobs in both plants together with the related

runtimes. Small orders at the Youngstown plant have much longer runtimes. Both plants,

with larger orders, show about two minutes per 1,000 units average runtime (though the

Youngstown plant gets to the two minute mark at a slightly lower job size than the Los

Angeles plant). The bottom line: orders under approximately 50,000 units have relatively

high runtimes at Youngstown, and only somewhat elevated runtimes at Los Angeles. There

are two implications of this finding:

a. It is clear that, for small orders, job size affects not only setup costs per unit but also

runtime cost per unit. An operations employee at the company originally studied in

this case explained that a key reason for the effect of batch size on average runtime is

that the equipment operators normally ran the machines slowly at the start of the job

to make sure that the job was running properly, and then increased the processing

speed as the job progressed. Thus, for smaller jobs, there was a longer “wait time”

cost) but also potentially the unit-level costs.

b. The implication for manufacturing strategy is the importance of matching factory

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-34

TN-1 Manufacturing Cost and Operating Margin for Both Plants under Volume-Based and

two methods for Activity Based Costing

Harrison Products Los Angeles Plant

Operating Operating Operating

Job Operating Margin Operating Margin Operating Margin

Number Job Size Cost Margin per unit Cost Margin per unit Cost Margin per unit

1 11,342 12,476$ 3,403$ 0.300$ 14,342$ 1,537$ 0.135$ 13,409$ 2,470$ 0.218$

2 7,089 7,798 2,127 0.30 10,089 (164) (0.023) 8,943 981 0.138

3 2,835 3,119 850 0.30 5,835 (1,866) (0.658) 4,477 (508) (0.179)

4 7,563 8,319 2,269 0.30 10,563 25 0.003 9,441 1,147 0.152

5 1,891 2,080 567 0.30 4,891 (2,244) (1.186) 3,486 (838) (0.443)

6 70,884 77,972 21,265 0.30 73,884 25,354 0.358 75,928 23,309 0.329

7 63,087 69,396 18,926 0.30 66,087 22,235 0.352 67,741 20,580 0.326

8 25,282 27,810 7,585 0.30 28,282 7,113 0.281 28,046 7,349 0.291

9 68,285 75,114 20,486 0.30 71,285 24,314 0.356 73,199 22,400 0.328

10 49,147 54,062 14,744 0.30 52,147 16,659 0.339 53,104 15,701 0.319

11 30,244 33,268 9,073 0.30 33,244 9,098 0.301 33,256 9,085 0.300

12 30,008 33,009 9,002 0.30 33,008 9,003 0.300 33,008 9,003 0.300

13 41,822 46,004 12,547 0.30 44,822 13,729 0.328 45,413 13,138 0.314

14 9,452 10,397 2,836 0.30 12,452 781 0.083 11,425 1,808 0.191

15 13,941 15,335 4,182 0.30 16,941 2,576 0.185 16,138 3,379 0.242

16 12,051 13,256 3,615 0.30 15,051 1,820 0.151 14,154 2,718 0.226

17 119,086 130,995 35,726 0.30 122,086 44,634 0.375 126,540 40,180 0.337

18 5,907 6,498 1,772 0.30 8,907 (637) (0.108) 7,702 567 0.096

19 75,610 83,171 22,683 0.30 78,610 27,244 0.360 80,891 24,964 0.330

20 1,182 1,300 355 0.30 4,182 (2,527) (2.138) 2,741 (1,086) (0.919)

21 3,308 3,639 992 0.30 6,308 (1,677) (0.507) 4,973 (342) (0.103)

22 37,805 41,586 11,342 0.30 40,805 12,122 0.321 41,195 11,732 0.310

23 64,269 70,696 19,281 0.30 67,269 22,708 0.353 68,982 20,994 0.327

24 35,168 38,685 10,550 0.30 38,168 11,067 0.315 38,426 10,809 0.307

25 16,970 18,667 5,091 0.30 19,970 3,788 0.223 19,319 4,440 0.262

26 12,524 13,776 3,757 0.30 15,524 2,010 0.160 14,650 2,883 0.230

27 43,807 48,188 13,142 0.30 46,807 14,523 0.332 47,497 13,832 0.316

28 21,738 23,912 6,521 0.30 24,738 5,695 0.262 24,325 6,108 0.281

Standard Deviation 0.000$ 0.558$ 0.279$

Operating Operating Operating

Harrison Products Youngstown Plant Margin Margin Margin

Job Number Job Size Cost Margin per unit Cost Margin per unit Cost Margin per unit

1 6,695 6,695$ 2,678$ 0.40$ 12,276$ (2,903)$ (0.434)$ 9,485$ (112)$ (0.017)$

2 116,959 116,959 46,784 0.40 111,513 52,230 0.447 114,236 49,507 0.423

3 136,058 136,058 54,423 0.40 128,702 61,779 0.454 132,380 58,101 0.427

4 42,531 42,531 17,012 0.40 44,528 15,016 0.353 43,529 16,014 0.377

5 51,884 51,884 20,754 0.40 52,946 19,692 0.380 52,415 20,223 0.390

6 10,387 10,387 4,155 0.40 15,598 (1,057) (0.102) 12,993 1,549 0.149

7 69,496 69,496 27,798 0.40 68,796 28,498 0.410 69,146 28,148 0.405

8 51,982 51,982 20,793 0.40 53,034 19,741 0.380 52,508 20,267 0.390

9 79,351 79,351 31,740 0.40 77,666 33,426 0.421 78,508 32,583 0.411

10 18,594 18,594 7,438 0.40 22,985 3,047 0.164 20,789 5,242 0.282

11 63,796 63,796 25,518 0.40 63,666 25,648 0.402 63,731 25,583 0.401

12 48,241 48,241 19,296 0.40 49,667 17,871 0.370 48,954 18,583 0.385

13 13,980 13,980 5,592 0.40 18,832 740 0.053 16,406 3,166 0.226

14 97,220 97,220 38,888 0.40 93,748 42,360 0.436 95,484 40,624 0.418

15 84,175 84,175 33,670 0.40 82,008 35,838 0.426 83,091 34,754 0.413

16 41,153 41,153 16,461 0.40 43,288 14,327 0.348 42,220 15,394 0.374

17 9,796 9,796 3,918 0.40 15,066 (1,352) (0.138) 12,431 1,283 0.131

18 98,874 98,874 39,550 0.40 95,237 43,187 0.437 97,055 41,368 0.418

19 22,447 22,447 8,979 0.40 26,452 4,974 0.222 24,450 6,976 0.311

20 142,458 142,458 56,983 0.40 134,462 64,979 0.456 138,460 60,981 0.428

21 63,796 63,796 25,518 0.40 63,666 25,648 0.402 63,731 25,583 0.401

22 120,700 120,700 48,280 0.40 114,880 54,100 0.448 117,790 51,190 0.424

23 80,877 80,877 32,351 0.40 79,039 34,189 0.423 79,958 33,270 0.411

24 149,841 149,841 59,936 0.40 141,107 68,671 0.458 145,474 64,303 0.429

25 8,763 8,763 3,505 0.40 14,137 (1,869) (0.213) 11,450 818 0.093

26 30,885 30,885 12,354 0.40 34,047 9,193 0.298 32,466 10,773 0.349

27 43,712 43,712 17,485 0.40 45,591 15,606 0.357 44,651 16,545 0.379

28 12,160 12,160 4,864 0.40 17,194 (170) (0.014) 14,677 2,347 0.193

29 100,912 100,912 40,365 0.40 97,071 44,206 0.438 98,991 42,285 0.419

30 52,376 52,376 20,950 0.40 53,388 19,938 0.381 52,882 20,444 0.390

31 129,462 129,462 51,785 0.40 122,766 58,481 0.452 126,114 55,133 0.426

32 161,262 161,262 64,505 0.40 151,386 74,381 0.461 156,324 69,443 0.431

33 5,317 5,317 2,127 0.40 11,035 (3,592) (0.675) 8,176 (732) (0.138)

34 15,752 15,752 6,301 0.40 20,427 1,626 0.103 18,089 3,963 0.252

35 14,177 14,177 5,671 0.40 19,009 838 0.059 16,593 3,255 0.230

36 28,354 28,354 11,342 0.40 31,769 7,927 0.280 30,061 9,634 0.340

37 29,535 29,535 11,814 0.40 32,832 8,518 0.288 31,183 10,166 0.344

38 6,895 6,895 2,758 0.40 12,456 (2,803) (0.406) 9,675 (22) (0.003)

39 3,467 3,467 1,387 0.40 9,370 (4,517) (1.303) 6,419 (1,565) (0.451)

40 73,444 73,444 29,378 0.40 72,350 30,472 0.415 72,897 29,925 0.407

41 190,600 190,600 76,240 0.40 177,790 89,050 0.467 184,195 82,645 0.434

Standard Deviation 0.000 0.371 0.185

(setup driver: the job)

(driver: job & job size)

Volume-Based

Activity-Based

Activity-Based

Volume Based Rate:

Unit costs

Los Angeles: $1.10

Youngstown: $1.00

Activity Based Rate (driver: the

job):

Los Angeles:

Setup Costs: $6,000,000/2,000

= $3,000 per job

Youngstown:

Setup Costs: $10,000,000/1,600

=$6,250 per job

Other costs for Los Angeles

($.40+$.40+$.2=$1.00) and

Youngstown : ($.40+$.40+$.01 =

ActivityBased Rate (driver:

job&units) (split setup costs; one–

half to job and one-half to units)

Los Angeles:

Setup Costs: $3,000,000/2,000

= $1,500 per job

plus: $3,000,000/60,000,000

=$.05 per unit

Youngstown:

Setup Costs: $5,000,000/1,600

=$3,125 per job

plus: $5,000,000/100,000,000

=$.05 per unit

Other costs for Los Angeles :

($.40+$.40+$.2=$1.00)

and Youngstown : ($.40+$.40+$.01 =

$.90)

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-35

TN-2: Analysis of the Relationship between Runtime and Job Size for Los Angeles

and Youngstown Plants

Los Angeles Plant

0

1

2

3

4

5

0 50,000 100,000 150,000

Minuntes/1,000

Job Size

Correlation: Job Size and Runtime

Job Size Minuntes/1000

Job Size 1

Minuntes/1000 –0.93236127 1

Youngstown Plant

0

5

10

15

20

0 50,000 100,000 150,000 200,000 250,000

Minutes/1,000

Job Size

Correlation: Job Size and Runtime

Job Size Minutes/1000

Job Size 1

Minutes/1000 –0.64444884 1

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-36

Teaching Strategies for Readings

5-1 Activity-Based Costing and Predatory Pricing: The Case of the Petroleum Retail Industry

1. What are product-cost subsidizations?

Product-cost subsidizations are where excessive costs are charged to one or more products, usually

2. What are possible consequences of product-cost subsidizations?

Undercosted products can lead to the appearance of predatory pricing where it actually does not exist.

3. List alternative approaches to assign costs in a gasoline service center.

Three approaches can be employed to assign gasoline service center costs to products:

4. Identify cost hierarchy level groups in classifying activities at the retail level of a gasoline service

center and give at least one example each.

Unit-level activities are undertaken for each gallon of gasoline sold (such as electricity to power

pumps when dispensing gasoline);

Batch-level activities are the same for each gasoline transaction irrespective of the volume of

gasoline purchased (for example, transactions to process customer payments for gasoline by cash,

5. What are overheads activity-cost pools pertaining to selling gasoline in a retail gasoline service center

and what is the activity level for each of the cost pools?

Gasoline Sales Attendants (Labor): Attendants are needed to receive payments from customers

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-37

Also, it was necessary to determine a “reasonable rental value” for the gasoline-dispensing facility,

which, in general, can be classified as a product-level activity. This activity cost pool includes

assets that are specific to a particular gasoline grade and common gasoline dispensing assets. In a

more comprehensive activity analysis, this cost pool could be divided into two or more activity

cost pools that would be more homogeneous in nature.

6. Identify the activity drivers for overheads activity-cost pools identified in this study and explain the

reasons for the selection?

Gasoline Sales Attendants (Labor): Volume of gasoline sold (a unit-level activity driver).

The principal responsibility of a kiosk attendant is to receive payments from customers for

gasoline purchases, which is a batch-level activity. Given that the average volume of gasoline

sold to each customer is about the same, regardless of the gasoline grade, the volume of gasoline

sold can be used as a proxy activity driver for these payment transactions.

The number of gasoline sales transactions is a major factor in determining the number of kiosk

number of attendants, which directly impacts the imputed rental payments.

The volume of gasoline sales determines the hours a gasoline station is open, which directly

affects the level of repairs and maintenance, utilities costs, and so on.

Gasoline-Dispensing Facility: Number of gasoline grades.

The facilities used for dispensing the three grades of gasoline are identical in size and cost for

each grade of gasoline irrespective of the volume of gasoline sold (for example, the gasoline

tanks).

7. List examples of gasoline-dispensing facilities for a gasoline service center and identify whether each

of the facilities is a common or a gasoline grade-specific asset. (Please refer to Table 3 below for the

answer).

5-38

5-2 Activity-Based Benchmarking and Process Management – Managing the Case of

Cardiac Surgery

1. Describe briefly the hospital’s costing system.

Generally, the hospital’s costing system begins with the division of each general ledger account

into cost types: variable direct cost, fixed direct cost, and fixed indirect cost.

At the cost center or department level, each indirect cost center is assigned an allocation base (such

as total cost, square feet, or gross revenue) to be used to spread the indirect costs to the direct cost

centers. The departmental direct costs and allocated indirect costs become departmental total costs.

The standard unit cost of the primary product/service is then calculated by first allocating the

departmental total cost based on the relative value units (RVUs) multiplied by the budgeted volumes

of each individual product/service to obtain the budgeted total cost of each basic product/service.

2. Describe steps in activity-based benchmarking for medical-care processes.

5-39

5-3 Using ABC to Asses Channel/Customer Profitability

This article explains how ABC was used by a firm (TEC) in the temporary employment industry to better

identify the profitability of its service distribution channels and individual customers.

Discussion Questions:

1. What are the four steps used in implementing ABC costing at TEC?

Step 1. Develop the activity dictionary.

2. What are the activity consumption drivers that TEC has chosen for each of the three activities: filling

work orders, hiring temporaries, and processing payroll?

From Table 2:

• number of hours worked for processing payroll

3. Which customer channel is most profitable, clerical or industrial, and why?

The clerical channel has somewhat higher profitability (Table 3)because the industrial customers

demand lower rates and have significantly higher worker’s compensation rates.

4. Within the industrial channel, which class of customers is most profitable and why?

5. In the study of the four largest customers, which is the most profitable and why?

The newspaper publisher and the food processing company had negative contributions, while the

trailer manufacturer has a modest contribution. The highest contribution was for the chemical company

5-40

5-4 Cost System Redesign at a Medium-Sized Company

This article looks at a company that was experiencing unprofitable growth and weak cash-flow activity.

The authors examine how an ABC method allowed the company to become more competitive, to look at

their current product mix and product lines, and ultimately, to improve cash flow and product

profitability.

Discussion Questions

1. Why for any manufacturer is proper inventory management important?

For virtually any manufacturer, proper inventory management ensures the availability of the right items at

the right time and in the right place. This, in turn, supports organizational objectives of customer service,

2. What are the elements of an ABC system?

3. What is a cost objective?

4. Why are duration drives used in an ABC system?

5. What internal factors limit the ABC model’s ability to influence the decision-making process in a

company?

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-41

5-5 Implementing Time-Driven Activity-Based Costing at a Medium-Sized Electronics

Company

This article revisits the company described in reading 5-4, which has now adopted a traditional ABC

system. In this article the authors examine how a time-driven ABC (TDABC) system might overcome

some of the drawbacks of the traditional ABC system while provide more insightful information about the

demand that products put on the available resources.

Discussion Questions

1. What are the goals of an ABC system?

At one level, the goal of an ABC system is to allocate indirect (support) costs in such a way that the

resulting cost information reflects more accurately the resource demands/resource consumption of an

2. What are the potential drawbacks of a traditional ABC system?

The issues faced by XYZ are representative of a major drawback of a traditional ABC system. First

is the complexity of the implementation. A traditional ABC system is very data intensive and

collecting and analyzing the data can prove to be overwhelming for a small to medium sized firm.

Additionally, there is the difficulty in keeping all the data current in order for management to be able

demanded by various cost objects that use the activity.

In short, a traditional ABC system can be expensive to build, time-consuming to operate and update,

difficult to maintain, and difficult to modify to meet management needs.

3. What benefits does a TDABC system offer over a traditional ABC system?

Advocates of time-driven activity-based costing maintain that this system is an improvement on

traditional ABC systems in the following respects:

• TDABC eliminates the need for the time consuming, subjective, interview-and-survey process to