Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–61

15–48 Proration of Variances (60 minutes)

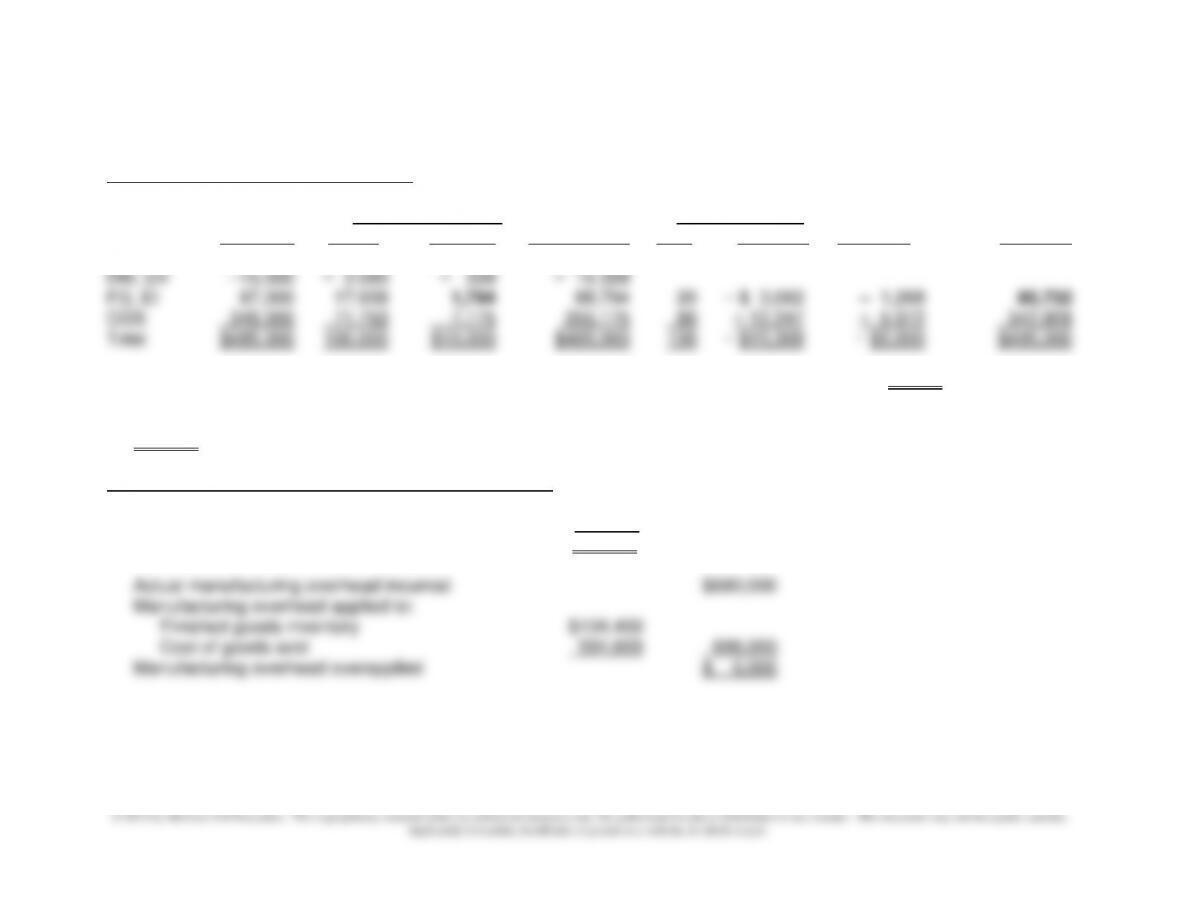

Proration of Direct Materials Variances

Proration of DM Proration of DM Net Change Total $DM

Standard Price Variance, PV Total after Usage Variance After After

DM Cost % Amount Prorating PV % Amount Proration Proration

DM, EI $ 65,000 13.402 $ 1,340 $ 66,340 $ 1,340 $ 66,340

1. The amount of direct materials price variance, PV, prorated to finished goods ending inventory: $1,794

2. The total amount of direct materials in finished goods ending inventory after proration of all materials variances:

$85,732

Proration of Direct Labor & Manufacturing OH Variances

Direct labor rate variance $20,000U

Direct labor efficiency variance 5,000F

Total direct labor variance $15,000U

15–62

15–48 (Continued-1)

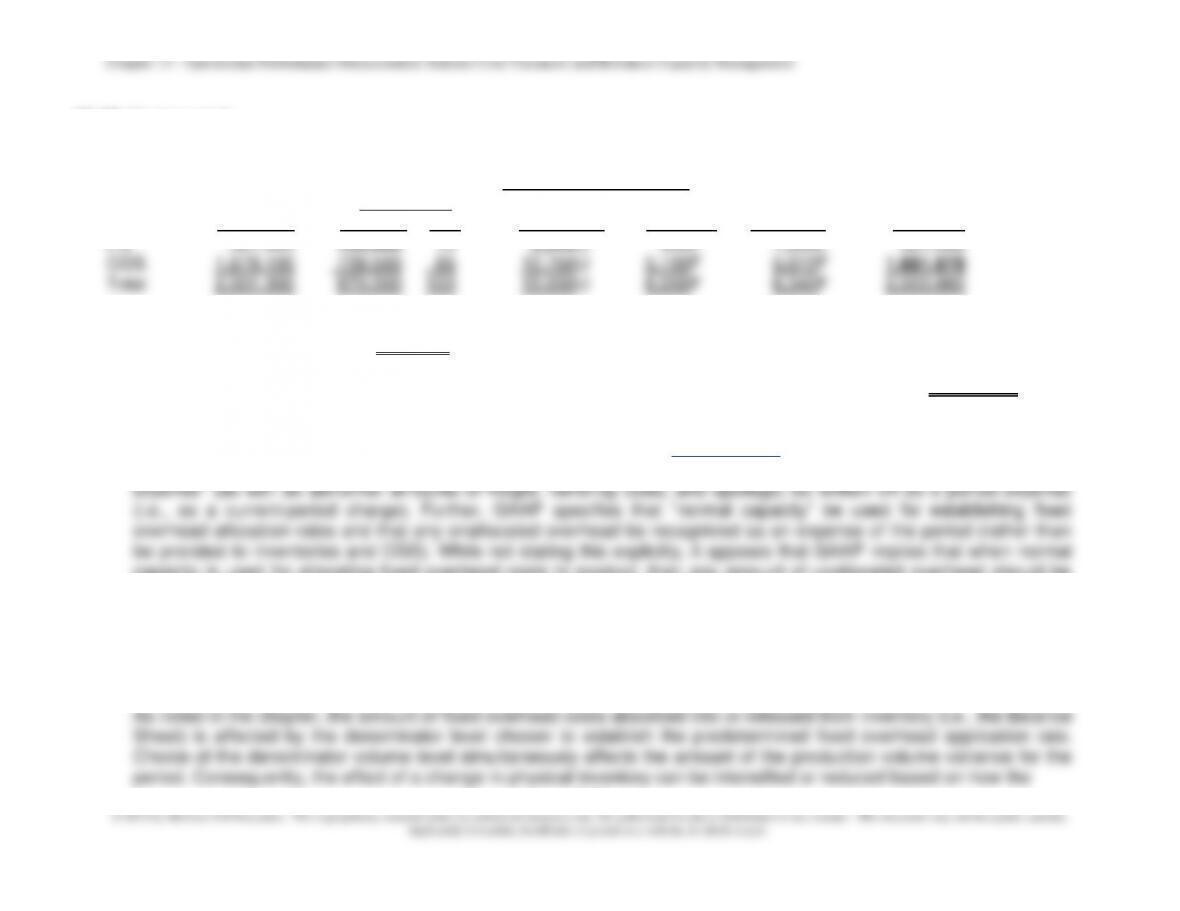

Total Cost DL Cost before Proration of Prorated Total

Before Proration DL OH DM Cost after

Proration Dollar % Variance Variance Variance Proration

FG 321,900 130,500 15 2,250U 900F 1,268F 321,982

3. The total amount of direct labor in finished goods inventory at December 31, after all variances have been prorated:

$130,500 + $2,250 = $132,750

4. The total cost of goods sold for the year ended December 31 after all variances have been prorated: $1,681,678

5. Generally accepted accounting principles (GAAP) (FASB ASC 330–10–30-3 to -7, previously SFAS151—“Inventory

Costs: An Amendment of ARB No. 43, Chapter 4,” and available at www.fasb.org) reaffirms (and brings U.S. reporting

standards more in line with International Accounting Standards in the area) that “abnormal” amounts of “idle facility

capacity is used for allocating fixed overhead costs to product, then any amount of unallocated overhead should be

viewed as “abnormal” and therefore treated as a period cost.

6. The point of this question is to impress upon students the fact that under absorption costing, reported operating income

can be affected by the method used to dispose of any production volume variance associated with fixed overhead. In

other words, the variance-disposition method can be used to “manage earnings” under absorption costing.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–63

15–48 (Continued-2)

production volume variance is disposed of at the end of the period. Specifically, this

ability to affect reported income is confined to the situation where the production

volume variance is written off entirely to cost of goods sold (CGS), as follows:

• If inventory is increasing, choosing a lower denominator-volume level will

enhance the increase in absorption costing income due to the deferral of fixed

overhead in inventory.

denominator levels if they expect inventory to increase. Note, however, that if the

production volume variance is prorated based on the units creating the variance,

then the denominator-level choice has no effect on absorption-costing income. This

is because prorating this variance effectively changes the budgeted overhead

application rate to the actual overhead application rate.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–64

15-49 Four-Variance Analysis and Journal Entries (60-75 Minutes)

1.

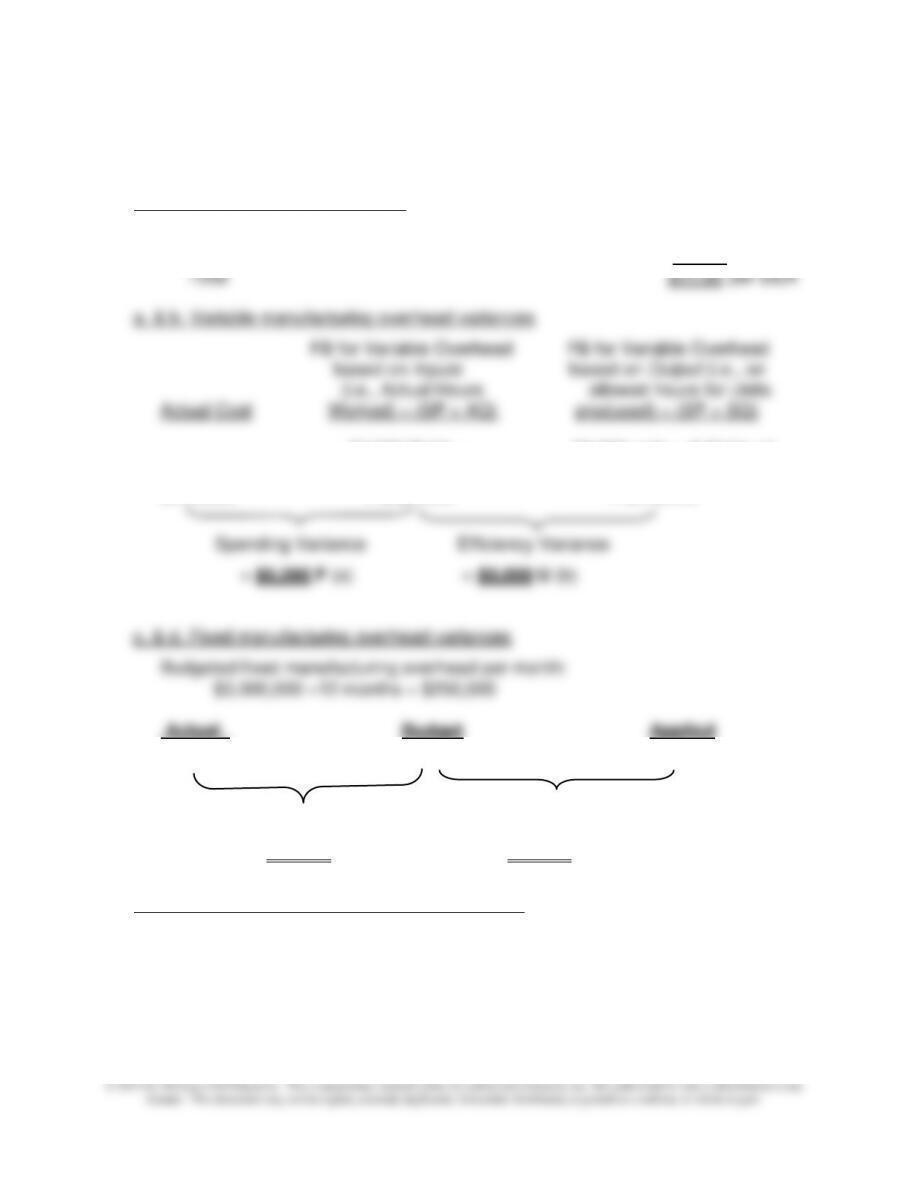

Standard Factory Overhead Rates

Variable factory OH $3,600,000 600,000 DLHs = $ 6.00 per DLH

Fixed factory OH $3,000,000 600,000 DLHs = $ 5.00 per DLH

53,500 DLHs × 26,000 units × 2 DLH/unit

$6.00/DLH = 52,000 DLHs × $6/DLH

$315,000 = $321,000 = $312,000

$260,000 $250,000 26,000 × 2 × $5 = $260,000

Spending Variance Production Volume Variance

= $10,000 U (c) = $10,000 F (d)

e. Under- or overapplied manufacturing overhead

($315,000 + $260,000) − ($312,000 + $260,000) = $3,000 underapplied

or, $6,000F − $9,000U − $10,000U + $10,000F = $3,000 underapplied

15–65

15–49 (Continued-1)

2. Summary Journal Entries (this solution assumes that the company uses an actual

and an applied account for variable overhead and an actual and an applied account

for fixed overhead costs):

Dr. Variable Factory Overhead—Actual 315,000

Cr. Utilities Payable, wages payable, etc. 315,000

To record actual variable overhead costs for the period.

Dr. WIP Inventory 312,000

Cr. Variable Factory Overhead—Applied 312,000

To apply standard variable overhead costs to production.

Dr. Variable Factory Overhead—Applied 312,000

Dr. Variable Overhead Efficiency Variance 9,000

Cr. Variable Overhead Spending Variance 6,000

Cr. Variable Factory Overhead—Actual $315,000

To record variable overhead variances for the period.

Dr. Fixed Factory Overhead—Actual 260,000

Cr. Salaries payable, accumulated depreciation, etc. 260,000

To record actual fixed overhead costs for the period.

Dr. WIP Inventory 260,000

Cr. Fixed Factory Overhead—Applied 260,000

To apply standard fixed overhead costs to production.

Dr. Fixed Factory Overhead—Applied 260,000

Dr. Fixed Factory Overhead Spending Variance 10,000

Cr. Production Volume Variance 10,000

Cr. Fixed Factory Overhead—Actual 260,000

To record fixed overhead variances for the period.

3. Closing Journal Entry:

Dr. Variable Overhead Spending Variance 6,000

Dr. Production Volume Variance 10,000

Dr. Cost of Goods Sold (CGS) 3,000

Cr. Variable Overhead Efficiency Variance 9,000

Cr. Fixed Overhead Spending Variance 10,000

4. Generally accepted accounting principles (GAAP) (viz., FASB ASC 330–10–30-3 to -7,

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–66

line with International Accounting Standards in the area) that abnormal amounts of

15–49 (Continued-2)

idle facility expense (as well as abnormal amounts of freight, handling costs, and

spoilage) be written off as a period expense (i.e., as a current-period charge).

5. The point of this question is to impress upon students the fact that under absorption

costing, reported operating income can be affected by the method used to dispose

of any production volume variance associated with fixed overhead. In other words,

the variance–disposition method can be used to “manage earnings” under absorption

costing.

inventory can be intensified or reduced based on how the production volume

variance is disposed of at the end of the period. Specifically, this ability to affect

reported income is confined to the situation where the production volume variance is

written off entirely to cost of goods sold (CGS), as follows:

• If inventory is increasing, choosing a lower denominator-volume level will

Thus, it is through the interaction of how the fixed overhead rate is set and how the

resulting production volume variance is accounted for that provides management an

opportunity to manage earnings under absorption costing. The above points suggest

that managers can increase short-run operating income by: (1) choosing larger

denominator levels if they expect inventory to decrease, or (2) choosing smaller

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–67

15–50 Research Assignment: Control of Overhead Costs; Strategy (45-60 Minutes)

74-82.

1. In general, how does this article relate to the material covered in Chapter 15?

Chapter 15 deals with the accounting for and the management of indirect costs—

principally, indirect manufacturing costs (i.e., manufacturing overhead). The

discussion in Chapter 15 extends the discussion from Chapter 14 and as such uses

standard costs and flexible budgets at the end of an accounting period to generate

various standard cost variances. The framework presented in Chapters 14 and 15 is

a traditional model for achieving short-term financial control.

The article in question extends the discussion in Chapter 15 by focusing on the

control of administrative costs (what are referred to in the title of the article as

“overhead” costs). As such, the discussion should be of interest to a wider audience.

The beginning of the article notes an important context: you, as the decision

2. The authors state (p. 75) that “administrative cost-reduction opportunities follow

similar patterns virtually everywhere.” What two major conclusions do the authors

offer, based on the accumulated experience in implementing successful cost-cutting

programs?

One, organizations typically are not able to meet their cost-cutting goals with a single

idea or plan. In fact, as a rule-of-thumb, the authors suggest that typically a

On the other hand, a combinations of less-disruptive (i.e., more locally confined)

action plans would be entirely appropriate for a lower cost-reduction goal (e.g.,

10%).

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–68

15-50 (Continued-1)

3. The authors of this article also state (p. 75) that cost-reduction goals typically require

10% Cost-Reduction Goal (“Incremental Ideas”)

1. Consolidate incidentals (e.g., combining training days or celebrations into a single

event; cross-scheduling the use of external resources, such as facilities or

trainers)

2. Take overdue personnel actions (e.g., job restructuring, underperformers)

3. Reduce spending on department managers (e.g., can the organization get by with

cycles for such investment opportunities that may now be viable)

20% Cost-Reduction Goal (“Redesign Ideas”)—can the demands on your

department be reduced so that resource savings can accrue?

1. Talk to your counterparties (to reveal cost-saving opportunities in terms of

4. Can resource spending tied to preventing against low-probability, low–

consequence events be reduced? (For example, is it necessary to check 100% of

data 100% of the time?)

30% Cost-Reduction Goal (Cross-Department and Program-Elimination Ideas;

1. Coordinate parallel activities (e.g., purchasing of supplies, travel

planning/discounts)

2. Shift the burden to the most efficient location (e.g., are there outsourcing

possibilities?)

cross-departmental initiatives, transfers, programs, etc.)

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–69

15-50 (Continued-2)

4. Eliminate low-value meetings and forums (to free employees to do more

creative/productive tasks)

5. Eliminate certain tasks performed by or programs conducted by your department

6. Reduce the burden your department places on others (e.g., how are other

departments overserving your department?

4. Provide a concise summary of the authors’ recommended approach for determining

the “right level of overhead.”

The authors’ thoughts in this regard are presented at the top of pages 78 and 79.

From management’s perspective, the underlying issue is “are we cutting enough—or

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–70

15–51 ABC Data, Capacity-Resource Planning, Non-Financial Performance Indicators

(40-45Minutes)

1.

2.

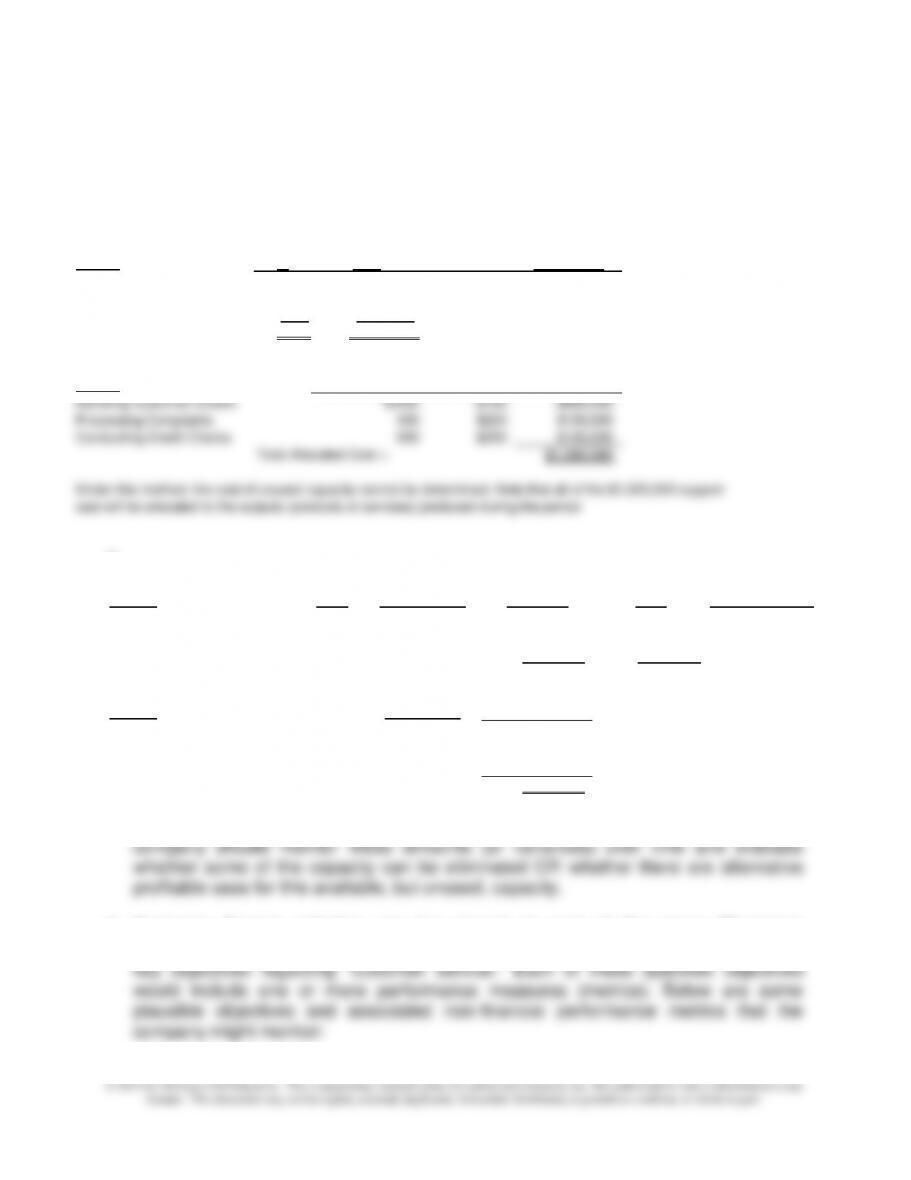

Actual Cost Budgeted Unused

Activity Rate Activity Units Assigned Cost

Capacity (units)

Handling Customer Orders $80 8,000 $640,000 $800,000 2,000

Processing Complaints $200 400 $80,000 $100,000 100

Conducting Credit Checks $200 500 $100,000 $100,000 0

Unused Cost of Unused

Activity Capacity % Capacity

Handling Customer Orders 20.00% $160,000

Processing Complaints 20.00% $20,000

Conducting Credit Checks 0.00% $0

$180,000

3. For each activity, we calculate in (2) an estimated cost of “unused capacity.” The

4. Customer Service activities can be viewed as part of the larger “Customer

Management” process. Conceptually, the company should establish one or more

Estimated

(Budgeted)

Allocated

Cost-Driver

Activity Cost-

Activity

%

Cost

Quantity

Driver Rate

Handling Customer Orders

80%

$800,000

8,000

$100

per customer order

Processing Complaints

10%

$100,000

400

$250

per customer complaint

Conducting Credit Checks

10%

$100,000

500

$200

per credit check conducted

100%

$1,000,000

Actual Cost-

Activity-Cost

Allocated

Activity

Driver Quantities

Driver Rates

Cost

Handling Customer Orders

8,000

$100

$800,000

Processing Complaints

400

$250

$100,000

Conducting Credit Checks

500

$200

$100,000

Total Allocated Cost =

$1,000,000

Under this method, the cost of unused capacity cannot be determined. Note that all of the $1,000,000 support

cost will be allocated to the outputs (products or services) produced during the period.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–71

15-51 (Continued)

Respond Quickly to Customer Feedback and Complaints:

a) Average time needed to resolve customer complaint

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–72

15–52 Managing Resource Capacity through Activity-Based Costing (ABC) (60

Minutes)

1. “Variable” and “fixed” costs represent descriptions of how a given cost changes in

response to one or more specified activities or “cost drivers.” (Mathematically, we

would say that “cost” is the dependent variable and the cost drivers represent

independent variables. A mathematical equation, in linear or non-linear form, can be

used to depict the underlying “behavior” of a given cost.)

We say a given cost is “variable” if, in the short run, that cost changes in response to

one or more cost drivers. In other words, such costs change, in total, as related

of how much of the resource is used in a given period. Examples include things such

as engineering salaries, production scheduling, sales and marketing managers, and

depreciation expense (or most rental expenses).

For many organizations today, their support costs are significant in amount and

largely short-term fixed. That is, many (if not most) support costs, including

manufacturing overhead, are incurred regardless of short-term demands. This, in

turn, presents an important managerial challenge: how to manage the demand for

2. In implementing an ABC system, management has several options at its disposal in

terms of how the ABC cost-allocation rates are determined. For example, the

denominator in each calculation can be either actual or budgeted activity. The former

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–73

15–52 (Continued-1)

prices, and order acceptance, the company may set an increased price to offset the

seemingly increased activity cost rates. Predictably, the effect is even lower demand,

lower activity volume, and higher activity cost rates. This situation is referred to in the

literature as the death-spiral effect. Eventually, there are no customers left to bear

the (basically fixed) support costs!

we might define “practical capacity” as the amount of work (or activity) that can be

performed without creating unusual delays, forcing overtime work, or requiring

additional resources to be supplied. Operationally, we might define “practical

capacity” as a percent (e.g., 85%) of maximum/theoretical capacity.

3. Determination of Activity-Cost Rate for “Handling Customer Orders” Activity

Budgeted Resource Spending (i.e., the numerator) = $560,000

No. of Orders @ Practical Capacity (i.e., the denominator) = 10,000

Support Cost Rate: Per Order Handled = $56.00

The management of support costs for companies like Zen is of strategic concern

because, more than likely, the company is competing on the basis of a differentiation

strategy. Thus, managing resource spending in support areas (e.g., manufacturing

support, customer support) is strategically important. Further, the dollar amount of

such costs are likely to be large and therefore worthy of special attention (monitoring

and control).

4. The point of this question is to demonstrate that the ABC data, based on practical

capacity, can be used to reveal the increased efficiencies associated with the TQM