8-56

8-54 (continued –1)

2. The limitations of this regression are somewhat unique since the

independent variables (except for average pay) and the dependent

variable are rankings (ordinal numbers rather than real numbers).

Thus, the issue of nonlinearity arises, but in a different manner than

in most regressions applications. As noted in the text, nonlinearity

often arises because of trend or seasonality in the data when the data

is from a time-series. In this case, the data is cross-sectional, so we

do not have time-series nonlinearity problems. However, the

not capture that difference. Our linear analysis assumes that the

rankings have equal increments, an assumption that is likely to be

wrong at least to some degree.

Chapter 8 – Cost Estimation

8-57

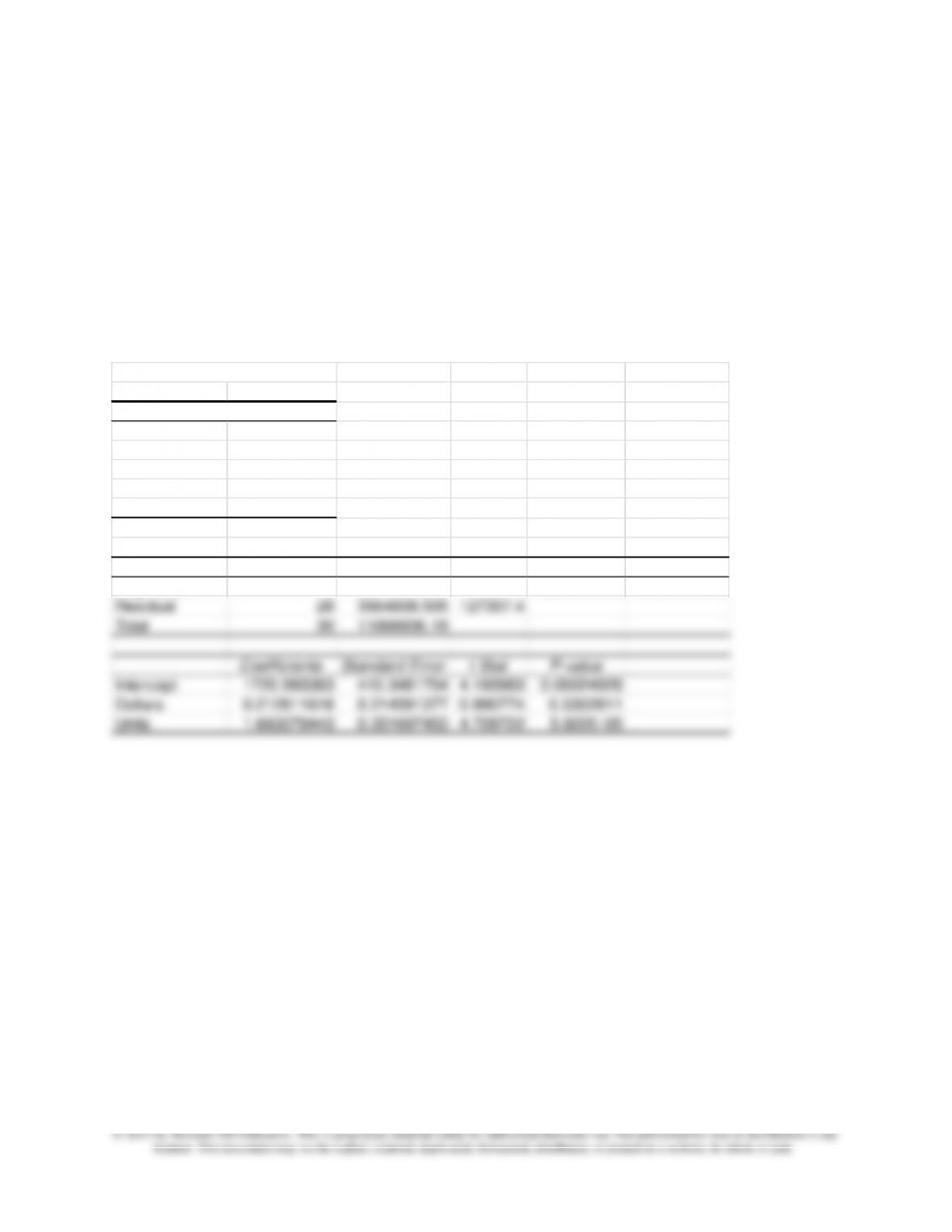

8-55 Cost Estimation; Regression Analysis (50 min)

1. The spreadsheet regression output for Plantcity is shown in

Exhibits 8-55A, B and C. Exhibit 8-55A shows the regression which

includes both predictors, sales dollars and sales units, while Exhibit

8-55B shows sales dollars only, and Exhibit 8-55C shows sales units

only.

Exhibit 8-55A (Units and Dollars)

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.836460729

R Square 0.699666551

Adjusted R Squa

0.678214162

Standard Error 356.8016909

Observations 31

ANOVA

df SS MS F

Significance F

Regression 2 8304227.689 4152114 32.6148545 4.85794E-08

Residual 28 3564608.505 127307.4

Total 30 11868836.19

Coefficients Standard Error t Stat P-value

Intercept 1720.993363 410.3481754 4.193983 0.00024928

Dollars 0.212611616 0.214591377 0.990774 0.3302811

Units 1.663079443 0.351697453 4.728722 5.822E-05

8-58

Problem 8-55 (continued –1)

Exhibit 8-55B (Dollars)

Regression Statistics

Multiple R 0.678100395

R Square 0.459820145

Adjusted R Square 0.441193254

Standard Error 470.1909447

Observations 31

ANOVA

df SS MS F Significance F

Regression 1 5457529.985 5457530 24.68582 2.76888E-05

Residual 29 6411306.209 221079.5

Total 30 11868836.19

Coefficients Standard Error t Stat P-value

Intercept 650.5468079 451.0275889 1.442366 0.159913

Dollars 0.956144724 0.192441985 4.968483 2.77E-05

Exhibit 8-55C (Units)

Regression Statistics

Multiple R 0.830142974

R Square 0.689137358

Adjusted R Square 0.678417956

Standard Error 356.6886878

Observations 31

ANOVA

df SS MS F

Regression 1 8179258.414 8179258 64.28879

Residual 29 3689577.78 127226.8

Total 30 11868836.19

Coefficients

Standard Error

t Stat P-value

Intercept 2112.01648 112.3290416 18.80205 8.7E-18

Units 1.918401433 0.239260971 8.018029 7.66E-09

Chapter 8 – Cost Estimation

8-59

8-55 (continued –2)

The precision of the regression shown in 8-55A is good, with a

standard error of the estimate of 357 relative to a dependent variable

with values averaging about 3,000. Also, the reliability of the model is

errors values to the model with both units and dollars. Because the

regression on sales units only is simpler and has a lower standard

error and higher R-squared, the model using only sales units is a

logical choice for the cost estimation model in this case.

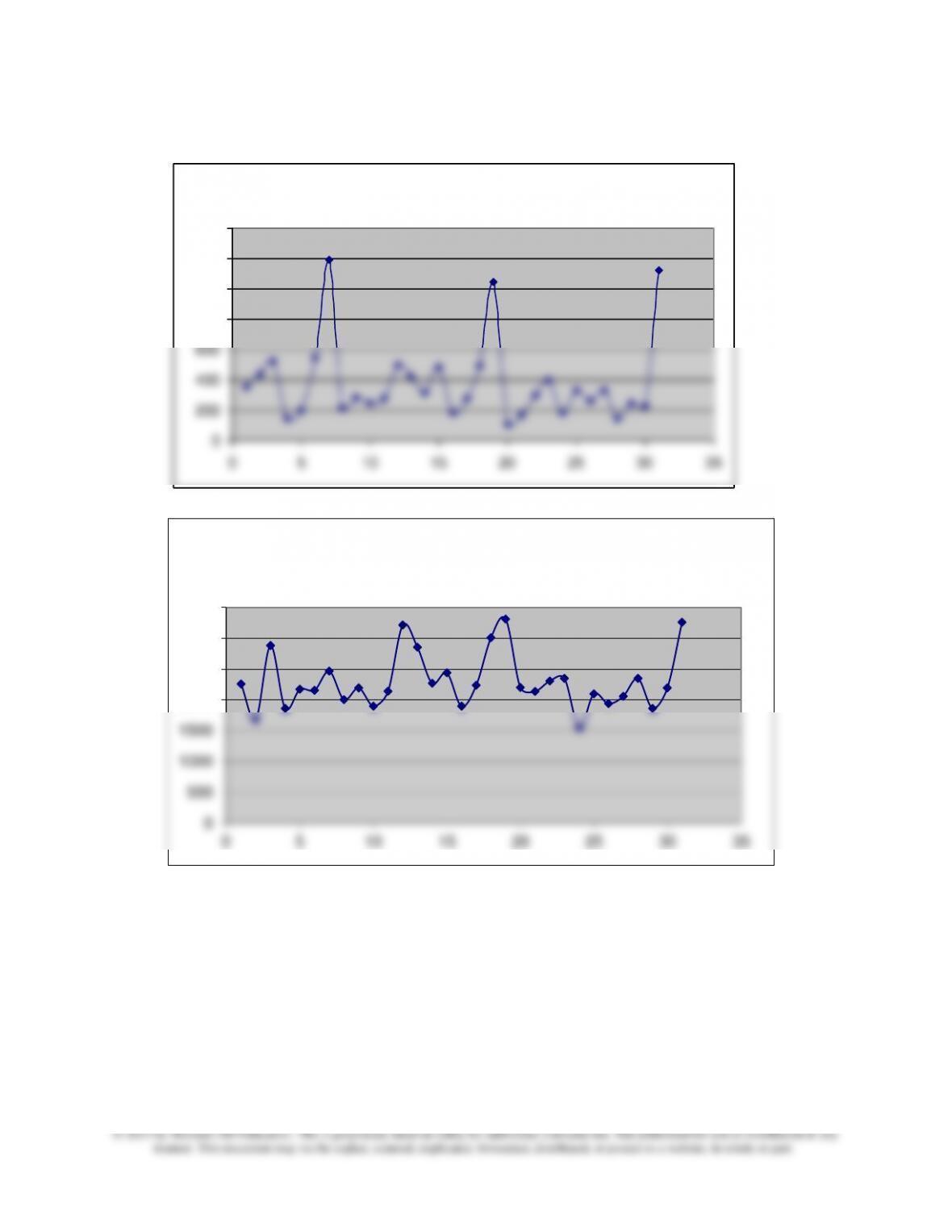

For further regression analysis on this data, consider the graphs

below which shows evidence of seasonality in the data.

Expense

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0 5 10 15 20 25 30 35

8-60

8-55 (continued –3)

Since the graphs show clear evidence of seasonality, another try of

the model with seasonality included would be a useful next step. The

addition of a seasonal variable for the month of December improved

the model in Exhibit 8-55C substantially.

Units

0

200

400

600

800

1000

1200

1400

0 5 10 15 20 25 30 35

0

500

1000

1500

2000

2500

3000

3500

0 5 10 15 20 25 30 35

Dollars

8-61

8-55 (continued -4)

The seasonal model is shown in Exhibit 8-55D. Note the substantial

improvement in R-squared; also note that the seasonal variable is

significant. The coefficient on the seasonality variable is negative

because supplies expense does not rise as fast as units sold in

December.

Exhibit 8-55D

Regression Statistics

Multiple R 0.859051742

R Square 0.737969895

Adjusted R Square 0.719253459

Standard Error 333.2733966

Observations 31

ANOVA

df SS MS F

Regression 2 8758843.802 4379422 39.42898

Residual 28 3109992.392 111071.2

Total 30 11868836.19

Coefficients Standard Error t Stat P-value

Intercept 1815.233657 167.0183648 10.86847 1.48E-11

Units 2.949465938 0.503693179 5.85568 2.7E-06

Season -1042.036219 456.1679284 -2.284326 0.030136

2. Predicted monthly figures for supplies expense using the

regression in Exhibit 8-55D:

Units Seasonality Predicted Expense

Jan 180 0 2,346$

Feb 230 0 2,494

Mar 190 0 2,376

Apr 450 0 3,142

May 350 0 2,848

Jun 350 0 2,848

Jul 450 0 3,142

Aug 550 0 3,437

Sep 300 0 2,700

Oct 300 0 2,700

Nov 450 0 3,142

Dec 950 1 3,575

8-62

8-56 Cross-Sectional Regression (30 min)

1.

Regression Statistics

Multiple R

0.976518934

R Square

0.953589229

999

Adjusted R Square

0.95001917

Standard Error

25458.32309

Observations

15

ANOVA

df

SS

MS

F

Significance F

Regression

1

1.73119E+11

1.73E+11

267.1074

4.77053E-10

Residual

13

8425640789

6.48E+08

Total

14

1.81545E+11

Coefficients

Standard Error

t Stat

P-value

Intercept

-5225.263287

10780.40244

-0.4847

0.635954

TPD

157.5079291

9.637390778

16.34342

4.77E-10

Construction Cost Equation

2. The regression has strong statistical measures. The R-squared is

relatively high at 95.35%; the t-value for the independent variable TPD is

high and the risk level (p) is low; the standard error of the estimate, at

25,458, is relatively small given the amounts predicted for the dependent

variable, so overall, the regression looks very strong, and the management

accountant should feel comfortable to rely on it in cost estimation. One

Chapter 8 – Cost Estimation

8-63

simple to apply method is to convert the data by taking the natural log (ln)

of each data point and then running the regression with the logged data.

8-56 (continued -1)

The conversion of logs removes the multiplicative type of non-linearity from

the equation. To see this, review the discussion in footnote 14 in the

Appendix (on learning curves).

3. From the standpoint of sustainability, the focus of the analysis needs to

move from construction costs to environmental metrics that measure the

effect on ground water, air quality, overall energy consumption in the

process of wastewater treatment, and other environmental variables. This

would add to the analysis such factors as the location of the facility, the

design of the facility, and other environmental considerations. Regression

Source: Richard K. Ellsworth, “Cost–to-Capacity Analysis for Estimating

Project Costs,” Construction Accounting and Taxation, September/October

2005, pp 5-10.

8-64

8-57 Cost Estimating for Defense Contracting; Using the Internet (25

min)

1.The cost estimation methods described in the document are called CERs

(cost estimating relationships) which are defined as mathematical

expressions relating the cost as the dependent variable to one or more

independent variables. The CERs described in the document include

simple and multiple linear regression and curvilinear regression. Cost

aviation industry.

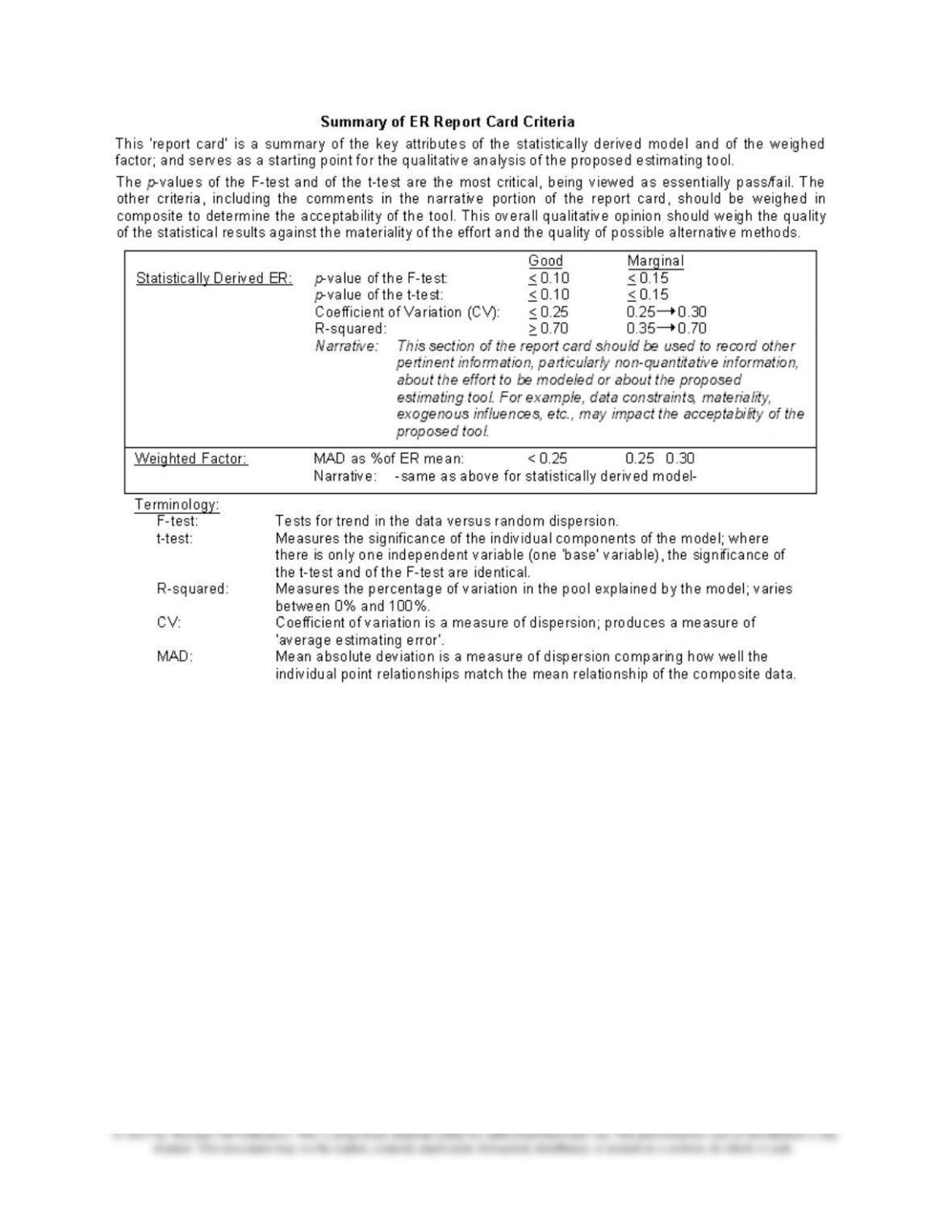

2. The model validation criteria in “Summary of ER Report Card Criteria” on

p 84 in chapter 3 of the handbook are very similar to those suggested in the

text for most statistical measures, and less restrictive than the text for other

measures. For example, the requirements for R-square are relatively

The “Summary of ER Report Card Criteria” is shown on the following page.

Chapter 8 – Cost Estimation

8-65