Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-46

9-43 CVP Analysis; Commissions; Ethics (50 min)

1. Breakeven dollars (dollars in thousands), Y:

Y = total fixed costs ÷ contribution margin ratio

Y = ($6,120 + $1,890) ÷ (1 − VCGS rate − commissions rate)

Supporting Calculations

Variable cost of goods sold rate (dollars in thousands):

$11,700 ÷ $26,000 = 45%

Current fixed costs ($ thousands):

Fixed cost of goods sold $2,870

Fixed advertising cost 750

Fixed administrative cost 1,850

Check:

Sales $17,800

Variable costs:

manufacturing (CGS) $8,010

sales commissions $1,780 $9,790

Contribution margin $8,010

Less: Fixed Costs:

Exisiting $6,120

Incremental $1,890 $8,010

Income before tax $0

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-47

9-43(Continued-1)

2. Required sales (to maintain current level of pre-tax income, $3,500, while

paying the requested increase in commission):

Let Y = required sales level:

$3,500 = Total sales − total variable costs − total fixed costs

3. The general assumptions underlying breakeven analysis that may limit its

usefulness include the following:

• All costs can be divided into fixed and variable elements.

• Variable costs vary proportionally to volume (thus, the variable cost

• The underlying model is deterministic; as such, the inherent assumption

is that the inputs to the CVP model are known with certainty

4. Let sales at the indifference point be Y (in 000s).

Since the two decision alternatives do not affect the selling price per

unit, we can define the indifference point as the volume level that

results in equal total cost between the two decision alternatives:

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-48

9-43 (Continued-2)

Total Cost for Current Agents = Total cost for Our Agents

0.45Y + 0.23Y + $6,120 = 0.45Y + $6,120 + $1,890 + 0.10Y

$26,000, the firm would be better off hiring its own agents, because the

relatively low variable cost offsets the relatively high fixed costs of the

new agents when sales are higher than the indifference point.

5. Markowitz should consider the firm’s ethical responsibility to its

shareholders, employees and agents. The new plan would be a savings

for the firm and thus would have an upward effect on stock price and thus

benefit the shareholders. However, the plan would be a blow to the sales

agents, many of whom may be depend on Marston Corporation for a

significant portion (or perhaps all of) their income. The agents are likely

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-49

9-44 CVP Analysis; Uncertainty/Sensitivity Analysis (60-75 min)

1. In order to break even, during the first year of operations, 3,649 clients

(rounded up) must visit the law office being considered by Don Carson and

his colleagues as calculated below.

Breakeven Calculation:

$0 = Total revenue − variable cost (supplies) − fixed cost (from above)

2. Based on the report of the marketing consultant, the expected number of

new clients during the first year is 12,600 as calculated below. Therefore,

it is entirely feasible for the law office to break even during the first year of

operations as the breakeven point is 3,649 clients (see above).

Expected value = (10 × 0.10) + (20 × 0.30) + (40 × 0.40) + (60 × 0.20)

First-year fixed expenses:

advertising $500,000

rent (6,000 x $48) $288,000

property insurance $22,000

utilities $32,000

malpractice insurance $180,000

depreciation–office equipment

$15,000

wages & fringe benefits:

regular wages (@360 days and 16 hours/day)

$1,641,600

overtime wages 15,000

fringe benefits on total wages 662,640

total = $3,356,240

9-50

9-44 (Continued-1)

Since there is uncertainty in the prediction of the number of clients per

3. Sensitivity Analysis: Sensitivity analysis is used to deal more effectively

with uncertainty or risk. Sensitivity analysis is a “what-if” type of analysis

used to determine the outcomes if any parameters change from the initial

assumptions. For example, revenues or costs could be changed from the

initial assumptions and a new break-even sales volume calculated.

The availability of spreadsheet software has made it very quick and easy

to compute the impact of changing one or more assumptions in a

financial model. At least three factors that make sensitivity analysis

prevalent in decision making include the following:

• As the business environment is becoming more dynamic and

competitive, sensitivity analysis provides management with an

understanding of the impact of changes in the environment. The

clients). Carson can enhance this analysis by using standard

deviations to measure the dispersion of the distributions, as a

means to get at the degree of uncertainty–higher standard

deviations for greater uncertainty.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

b. probability that the firm will generate at least $3,235,760 of incremental operating

income in year one (from new-client acquisitions):

standard deviation of operating income = $5,000,000 (given)

target profit level = $3,235,760 (given)

expected values:

9-44 (Continued-2)

4. Basic simulation analysis using the NORMDIST function in Excel:

a. probability that the firm will at least breakeven, given normally distributed operating

income and a standard deviation of $5,000,000, is ~ 95%:

Operating Income Information

standard deviation of op. income = $5,000,000 (given)

target pre-tax profit level = $0 (given)

mean (expected) value:

mean expected # new clients = 12,600 (above, Part 2)

contribution margin per new client = $920

incremental fixed costs = $3,356,240 (above, Part 1)

expected value of incr. op. income = $8,235,760 (i.e., [cm/unit x mean # of new clients]

– incremental fixed costs)

probability of at least breaking even = 1 – probability of $0 profit

= 95.023660%

The expected operating income for year one is $8,235,760. If, as assumed here, the standard

deviation of operating income is $5,000,000, then it seems entirely reasonable that there is

little probability (~5%) that the company would experience an operating loss on new-client

acquisitions in year one. Note that on a standard normal curve, the breakeven point ($0 of

operating income) is 1.647 standard deviations below the mean. The area under the standard normal

curve from -1.647 standard deviations to the mean is approximately 45%. Thus, the area from

-1.647 standard deviations below the mean to positive infinity is approximately 95%.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-44 (Continued-3)

c. Given a standard deviation of operating income of $5,000,000 and an expected value of 12,600

new clients in year one. What is the probability of generating incremental operating income of at

least $8,235,760?

standard deviation of operating income = $5,000,000 (given)

target profit level = $8,235,760 (given)

expected values:

incremental fixed costs = $3,356,240 (above, Part 1)

new number of clients = 12,600 (above, Part 2)

contribution margin per new client = $920

incremental operating income = $8,235,760

probability of generating at least $8,235,760 of incremental operating income

= 1 – cumulative probability of op. income to $8,235,760

= 50.00%

The above result, 50.00%, makes intuitive sense: the target profit ($8,235,760) is equal to

the expected profit ($8,235,760). Thus, there is a 50% probability that operating profit on

new clients in year one will be greater than the mean predicted value ($8,235,760) and a

50% probability that operating profit will be less than the mean value. This conclusion derives

from the basic interpretation of a standard normal curve.

d. Given a standard deviation of operating income of $2,500,000 and an expected value of 12,600

new clients in year one, what is the probability of generating incremental operating income of at

least $8,235,760?

standard deviation of operating income = $2,500,000 (given)

target profit level = $8,235,760 (given)

expected values:

incremental fixed costs = $3,356,240 (above, Part 1)

new number of clients = 12,600 (above, Part 2)

contribution margin per new client = $920

incremental operating income = $8,235,760

probability of generating at least $8,235,760 of incremental operating income

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-53

9-44 (Continued-4)

What the above result shows, in conjunction with the result from part (c) above, is that if

operating incomes are normally distributed around the mean, then the probabilityof generating

an operating income of at least the mean value is unaffected. Note, however, that the size of

the standard deviation of operating income does affect the size of the confidence interval

around a given targeted value. Note, too, that for a given standardard deviation of

operating income, a change in the standard deviation of operating incomes would affect the

probability of generating a given targeted level of operating income. For example, assume a

targeted operating income of $10,000,000. Given the assumptions in ( c) above, the probability

of generating at least this income is 36.21%; under the situation reflected in (d), the probability

drops to 24.02%.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-54

9-45 CVP Analysis; Strategy; Critical Success Factors (50-60 min)

1. a. A total of 480 seminar participants are needed for the joint venture to

break even, calculated as follows:

The break-even number of participants equals the fixed costs divided by

the contribution margin per participant

b. A total of 700 seminar participants are needed for the joint venture to

earn an after-tax profit (πA) of $169,400, calculated as follows.

The target number of participants equals the fixed costs (F) plus the

desired pre-tax profit (πB), divided by the contribution margin per

participant. Note that: πB = πA ÷ (1 − t), where t = the income tax rate.

πB = $169,400 ÷ (1 − 0.30)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-55

9-45 (Continued-1)

2. A minimum of 1,055 participants is needed in order for GSI to prefer the 40

percent fee option rather than the flat fee, calculated as follows (where Q =

number of seminar participants):

GSI fees for flat fee option

= 0.40 × [($1,100 ×Q) − $210,000)] = ($440 × Q) − $84,000

Pre-tax profit (operating income) would be equal for the two options when

total revenue is equal (since fixed costs of GSI are being ignored for the

present analysis) at the following number of participants, Q.

Therefore, GSI will earn more revenue and prefer the 40 percent option

when the number of participants is 1,055 or higher.

3. Some of the strategic and implementation issues facing GSI in this

decision are the following:

• Are the CVP assumptions satisfied? That is, total costs can be divided

into a fixed component and a component that is variable with respect

to volume. Total costs and total revenues have a linear relationship to

costs and revenues are known with certainty.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-56

9-45 (Continued-2)

• Alternative uses of capacity? Since the Eastern U seminars would

occupy all GSI’s available capacity, GSI should consider whether

there might be more profitable uses for that capacity before making

• Does the collaboration make sense strategically? Are Eastern and

GSI likely to enhance each other’s reputation and to provide operating

synergies and efficiencies that will make the alliance a profitable one?

For example, if the Eastern University’s academic reputation might

suffer from this alliance, then this should be considered in the

decision.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-57

9-46 CVP Analysis; Strategy; Uncertainty (60-75 min)

1. Total variable costs per unit for the current plan are

$6+$12.50+$25+$10=$53.50, and $15+$13.75+$30+$10=$68.75 under

the proposed plan. Thus, the contribution margin per unit and breakeven

point (in units) for each of the two plans are as follows:

Current Plan

Proposed Plan

Contribution

Margin/Unit

$100 − $53.50 = $46.50

$100 − $68.75 = $31.25

Breakeven*

($6,000,000 + $1,250,000) ÷

$46.50 per unit =

155,914 units

($3,000,000 + $1,250,000)

÷ $31.25 per unit =

136,000 units

*Fixed manufacturing overhead costs are determined from the fixed

overhead rates:

Current Plan

Proposed Plan

150,000 units × $40/unit =

$6,000,000

150,000 units × $20/unit =

$3,000,000

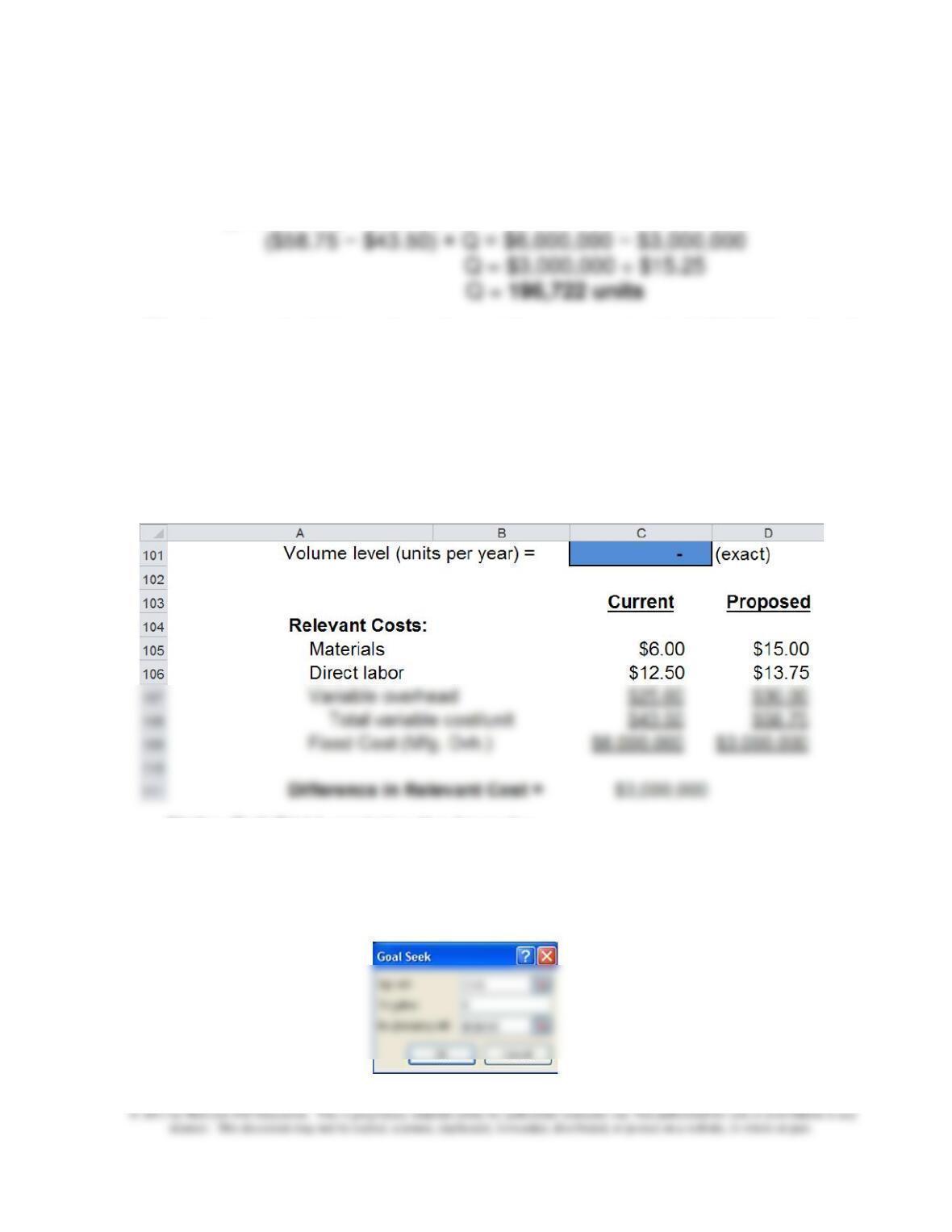

2. To determine the sales volume (in units) at which CG would be indifferent

between the current manufacturing plan and the proposed plan, solve for

the point, Q, in which total relevant cost is the same for the two decision

alternatives. (Revenue from sales is unaffected by choice of production

The indifference point, Q, can be found at the point of cost equality, as

follows:

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-58

9-46 (Continued-1)

Total Relevant Cost, Current = Total Relevant Cost, Proposed

($43.50 × Q) + $6,000,000 = ($58.75 × Q) + $3,000,000

(The above calculations show that at the current level of 150,000 units, the

firm would prefer the low-fixed-cost strategy, that is, the new plan.)

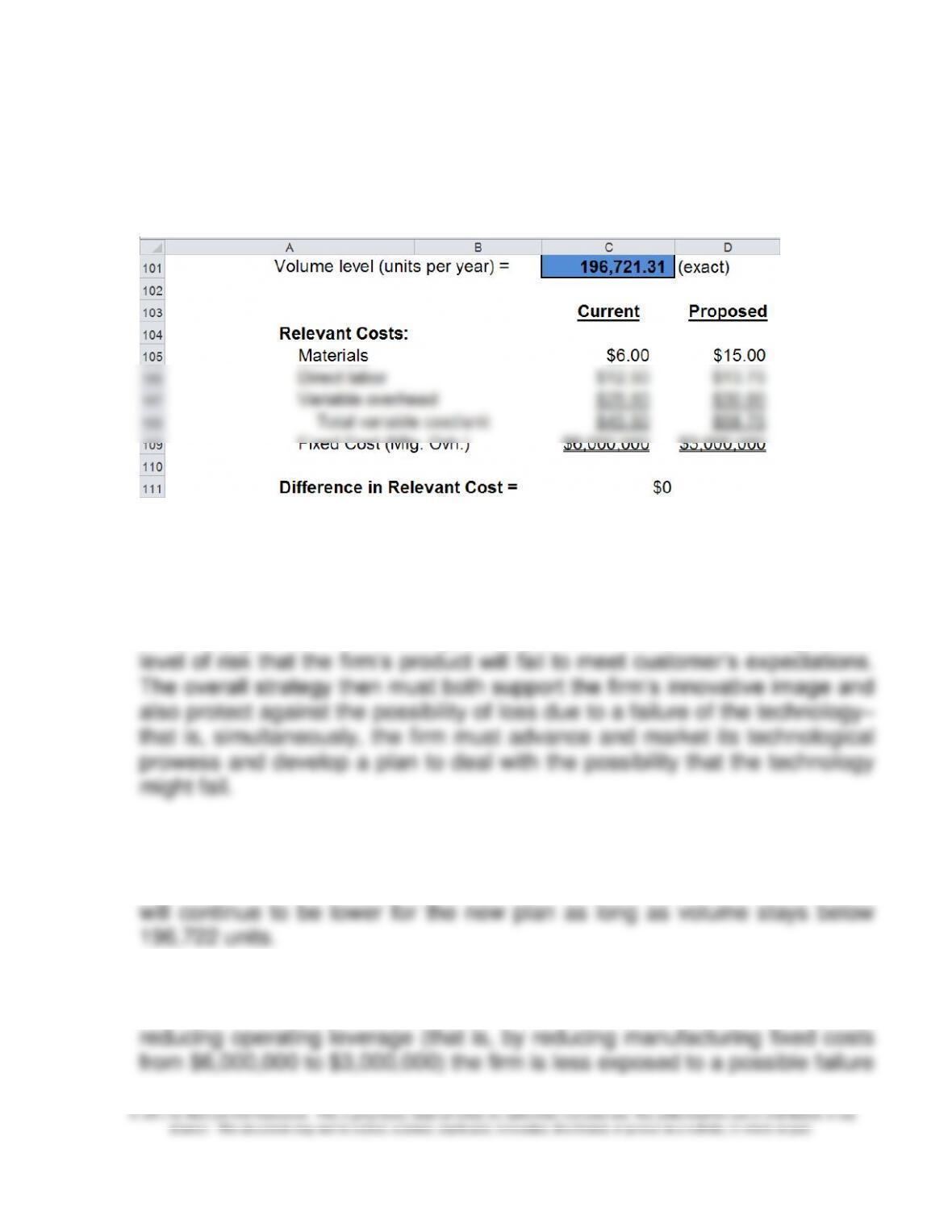

3. Use Goal Seek in Excel to confirm the answer found above in Requirement

2:

Step #1: Define the Cost-Differential Equation (i.e., Relevant Cost of

Current Production Plan – Relevant Cost of Proposed Plan)

Note: Cell C111 contains the formula:

((C101*C108) + C109) – ((C101*D108) + D109)

Step #2: Run Goal Seek, as follows:

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-59

9-46 (Continued-2)

Step #3: Generate Results, as follows:

4. CG’s strategy is best described as differentiation, since the firm has

succeeded by innovation in product design. Further, the firm operates in an

industry in which innovation and product design are critical to success. An

important element of the firm’s strategy is also the fact that the technology,

as for many firms in the industry, is not proven. That is, there is a significant

5.

a) The calculations in part 2 above support a decision to go to the new plan;

at the current level of 150,000 units, costs are lower for the new plan, and

b) Thinking strategically, the new plan is also preferred since it is an

appropriate response to the firm’s risk, as noted in Part 3 above. By

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

of the innovation and the drop off in sales. The reduction in fixed costs also

helps the firm to manage cash flows. Thus, the new plan is more consistent

Also, one could look at the proposal as consistent with the firm’s core

strength, which appears to be product innovation. There is no evidence that

the firm is particularly innovative or cost-effective in manufacturing. Thus, a

strategy which goes to less focus on manufacturing would be consistent

with this strategy; more focus should be retained in product design and

development.

c) Sensitivity analysis: since uncertainty is important in this case, CG

Graphics should use some of the tools as illustrated below. Note that the

current method looks good if projected demand rises.

Current Proposed Difference

Materials and purchased parts 6.00$ 15.00$

Direct labor 12.50 13.75

Variable GS&A 10.00 10.00

Variable overhead 25.00 30.00

Total Variable cost 53.50$ 68.75$ 15.25$

Price 100 100

CM 46.50$ 31.25$

Fixed Cost 7,250,000.00$ 4,250,000.00$ 3,000,000$