Chapter 19 – Strategic Performance Measurement: Investment Centers

19–16

19–29 Return on Investment (ROI) for Innovative Companies (30-45

minutes, including reading time)

The objective of this assignment is to engage the class in a discussion of

the limitation of return on investment (ROI) in the specified context. A key

question arises: how have these companies developed their innovative

process and products? If internally developed, then current GAAP requires

that the cost of developing these innovations will not be shown on the

balance sheet and therefore total assets and equity will be understated,

and returns based on the balance sheet numbers could be overstated.

Alternatively, if the firm acquired the innovation through purchasing a

effective management.

Source: Jena McGregor, “The World’s Most Innovative Companies,”

Business Week, April 24, 2006, pp. 76.

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–17

19-30 Transfer Pricing Issues (15 minutes)

In order to provide an incentive for a supplying division to reduce costs,

the transfer pricing agreement should provide an incentive, such as:

1. The cost-based transfer price will not be reduced as a result of the

cost reduction for a given period, say for a period of six months to

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–18

19–31 General Transfer-Pricing Rule (45 Minutes)

1. Transfer prices represent the amount that one division (subunit) of an

organization charges another division (subunit) of the organization for

services and products transferred internally.

Transfer prices serve the following roles:

a) They provide price data (i.e., inputs) for evaluating the financial

performance of profit centers and investment centers. In the

absence of such price information regarding internal exchanges,

rather than externally.

c) They provide the basis for increasing after-tax cash flow by (within

limits allowed by law) helping to minimize income-taxes (and, in an

2. The general transfer-pricing rule presented in the chapter is consistent

with the definition of “relevant costs,” to which students were exposed in

Chapter 11 of the text. That is, one specification of “relevant costs” is:

Out–of-Pocket Costs + Opportunity Costs. This general transfer-pricing

rule will generally reveal when an internal transfer should take place,

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–19

19-31 (Continued-1)

In the current situation, we have:

Transfer Price:

Incremental Cost per unit =

$500

Opportunity Cost per Unit = $650 – $500 =

$150

Transfer Price =

$650

At this price, the Fabrication (i.e., producing) Division would be indifferent

between selling internally and selling externally, as would the Assembly

(i.e., buying) Division. The profit position of the firm as a whole is

unaffected by the local decisions of the two divisional managers. Thus,

the use of this transfer-pricing rule (a) maintained divisional autonomy,

and (b) provided the appropriate “signal” to internal decision-makers (i.e.,

buyers and sellers).

3. If the Fabrication (i.e., producing) Division had excess capacity, this

means that the opportunity cost associated with any internal transfers

would be zero. Thus, the transfer price, as specified by the general

transfer-pricing rule, would be:

Transfer Price = Incremental Cost per Unit + Opportunity Cost per Unit

= $500 + $0

= $500

transfer, might be set a bit higher than the $500 figure. It is for this

situation that we state that the general transfer-pricing rule provides the

minimum transfer price, from the selling division’s standpoint.

4. As might be expected, the general transfer-pricing rule “works” in the

sense that as a model it provides internal decision-makers with

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–20

19-31 (Continued-2)

competitive market (as was assumed in this assignment), this may not be

much of a problem. However, under other market conditions, we know

that demand is partly a function of the quantity sold, both internally and

externally. (In other words, there are demand interactions that complicate

our efforts to estimate an opportunity cost associated with internal

transfers.) Further, implementing the general rule may be impossible (or,

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–21

19–32 Transfer Pricing; Decision-Making (25 minutes)

1. Division A’s purchase decision from the overall firm perspective:

Purchase costs from outside 10,000 ×$150 = $1,500,000

2. As above, but in addition, if Division A buys outside, Division B saves

an additional $200,000:

Purchase costs from outside 10,000 × $150 = $1,500,000

Less: Savings in variable costs 10,000 × $140 = 1,400,000

3. Assuming the outside price drops from $150 to $130:

Purchase costs from outside 10,000 × $130 = $1,300,000

Less: Savings in variable costs 10,000 × $140 = 1,400,000

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–22

19–32 (continued)

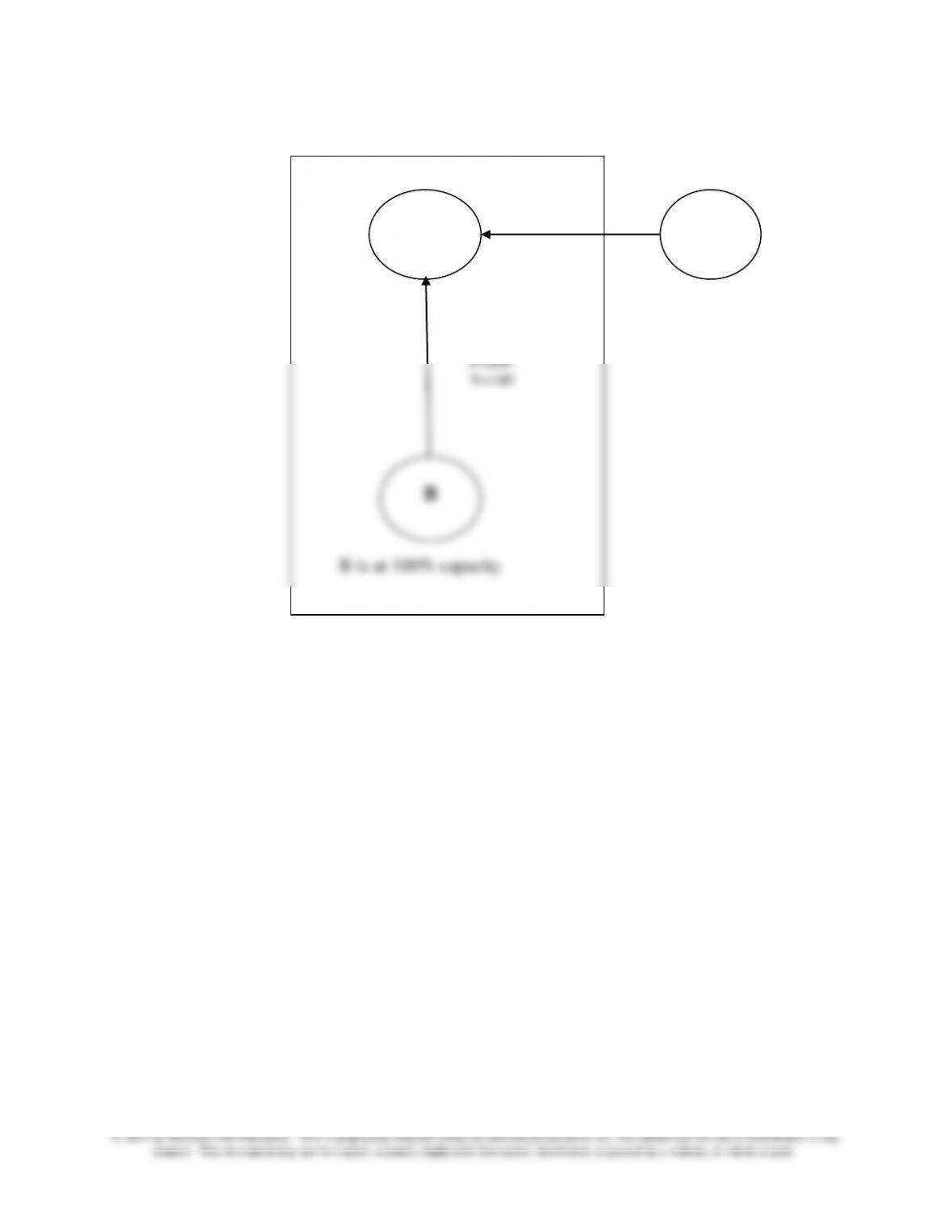

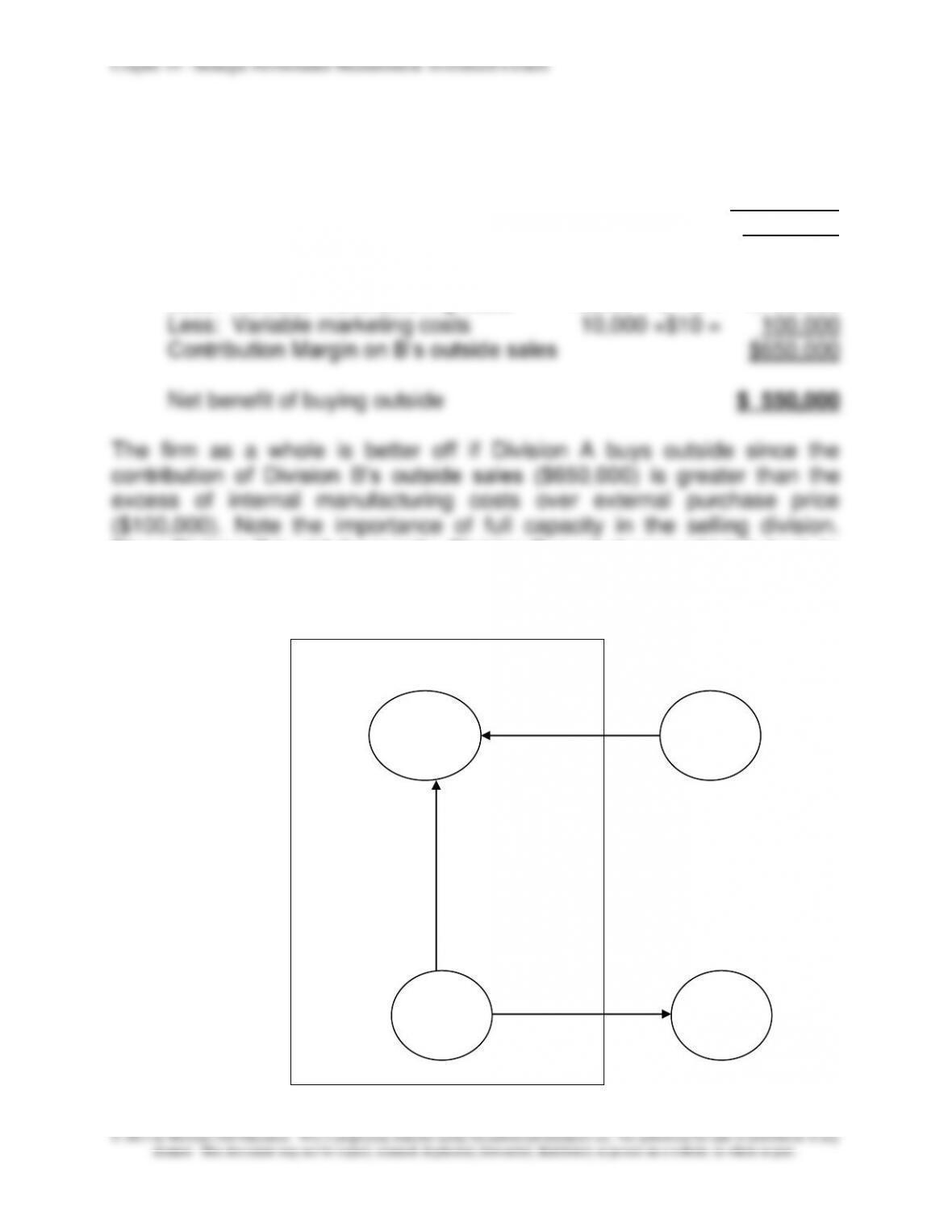

A

O/S

P=200

P=150

19–23

P=215

V=150

19–33 Transfer Pricing; Decision-Making (20 minutes)

Purchase costs from outside 10,000 × $150 = $1,500,000

Less: Savings in variable costs 10,000 × $140 = 1,400,000

Net Cost (Benefit) of External Purchase $ 100,000

B sales to other customers 10,000 × $215 = $2,150,000

Less: Variable manufacturing costs 10,000 × $140 = 1,400,000

Since Division B is at full capacity, Division B must choose which is best, to

sell inside or outside. If there were sufficient excess capacity, Division B

could do both.

A

B

O/S

O/S

P=200

V=140

P=150

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–24

19-34 Transfer Pricing; International Taxation (20-25 minutes)

The change in transfer price would increase the profitability of the

foreign subsidiary where taxes are lower and reduce the profitability of

the U.S. subsidiary, where taxes are higher. The net effect would be a

reduction of total corporate taxes of $65,000 ($932,500 − $867,500).

The following exhibit summarizes the analysis.

Singapore

Subsidiary

United States

Subsidiary

Total

INCOME PRIOR TO INCREASE IN TRANSFER PRICE

Revenues

$2,500,000

$3,500,000

$6,000,000

Direct Costs

1,500,000

2,500,000

4,000,000

Other Costs

350,000

200,000

550,000

Profit Before Tax

650,000

800,000

1,450,000

Tax (33%, 46%)

214,500

368,000

582,500

Profit After Tax

$ 435,500

$ 432,000

$ 867,500

INCOME AFTER INCREASE IN TRANSFER PRICE

Revenues

$3,000,000

$3,500,000

$6,500,000

Direct Costs

1,500,000

3,000,000

4,500,000

Other Costs

350,000

200,000

550,000

Profit Before Tax

1,150,000

300,000

1,450,000

Tax (33%, 46%)

379,500

138,000

517,500

Profit After Tax

$ 770,500

$ 162,000

$ 932,500

The difference in after-tax profit = difference in total income tax

expense = $932,500 – $867,500 = $65,000 (or, $582,500 –

$517,500)

Note: An equivalent short-cut calculation would be:

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–25

PROBLEMS

19–35 ROI; Different Measures for Total Assets (45-60 minutes)

1. Net book value (NBV) of fixed assets for each division (000s):

HEALTHCARE: $70 × 11 years remaining useful life = $770

COSMETICS: $70 × 9 years remaining useful life = $630

ROI using historical cost of divisional assets:

The COSMETICS Division is more profitable than the HEALTHCARE

Division, based on ROI calculated using net book value (NBV) of

divisional fixed assets (plus the current balance sheet value of current

assets).

2. a.

Gross Book Value (GBV) for each division:

HEALTHCARE 15 × $70 = $1,050 (Depreciation ×useful life)

COSMETICS 15 × $70 = $1,050

ROI:

b. (GBV at historical cost) × (construction cost index in 2013 ÷

construction cost in year of construction):

HEALTHCARE $1,050 × (100 ÷ 84) = $1,250

COSMETICS $1,050 × (100 ÷ 80) = $1,313

ROI:

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–26

19–35 (continued-1)

c. (Current NBV of fixed assets) ×(construction cost index in 2013 ÷

construction cost in year of construction)

HEALTHCARE $770 × (100 ÷ 84) = $917

COSMETICS $630 × (100 ÷ 80) = $788

ROI:

HEALTHCARE $130 ÷ ($917 + $300) = 10.68%

COSMETICS $200 ÷ ($788 + $300) = 18.38%

d. ROI Based on Current Replacement Cost of Fixed Assets (plus

current book value of current assets):

3. a. The best measure for evaluating the manager is replacement cost, as

it corresponds to the “going–concern” value of the investment. The

objective is to identify a measure of investment that fairly reflects the

productive capacity of the assets. Often, net book value falls much

faster than the productive capability of the assets, and thus, the ROI

with the older assets overstates the profitability of the unit. The use of

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–27

19–35 (continued-2)

The advantages of the replacement cost measure are fairness, since

it avoids the age bias issues associated with the net book value

measure, and motivation, since it reflects the current value of the

asset and therefore what investment value the manager has to work

extremely high.

b. The evaluation of the division should use replacement cost for the

same reasons as explained in (a) above. The only difference here is

when either division might be sold or relocated, in which case the

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–28

19–36 ROI and Incentive/Goal-Congruency Issues; Spreadsheet

Application (60-75 Minutes)

1. Year-by-Year ROIs, based on average NBV of investment:

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income

After

Depreciation

Average

NBV of

Asset

ROI Based

on NBV

1

$300,000

$200,000

$100,000

$900,000

11.11%

2

$300,000

$200,000

$100,000

$700,000

14.29%

3

$300,000

$200,000

$100,000

$500,000

20.00%

4

$300,000

$200,000

$100,000

$300,000

33.33%

5

$300,000

$200,000

$100,000

$100,000

100.00%

2. Year-by-Year ROIs, based on average gross book value(GBV) of

investment:

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income

After

Depreciation

Average

GBV

ROI

Based on

GBV

1

$300,000

$200,000

$100,000

$1,000,000

10.00%

2

$300,000

$200,000

$100,000

$1,000,000

10.00%

3

$300,000

$200,000

$100,000

$1,000,000

10.00%

4

$300,000

$200,000

$100,000

$1,000,000

10.00%

5

$300,000

$200,000

$100,000

$1,000,000

10.00%

3.This question deals with the incentives effects of using one method for

making long-term investment decisions (DCF, as discussed in Chapter

12) and a different method for evaluating the subsequent financial

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–29

because of a reduced denominator in the ROI calculation. In short, the

use of NBVs produces a misleading increase in ROIs over time,

19–36 (Continued-1)

regardless of whether true (economic) profitability is changing. This

negative incentive effect can, to some extent, be ameliorated through the

use of gross book values when measuring the investment base in the

ROI calculation.

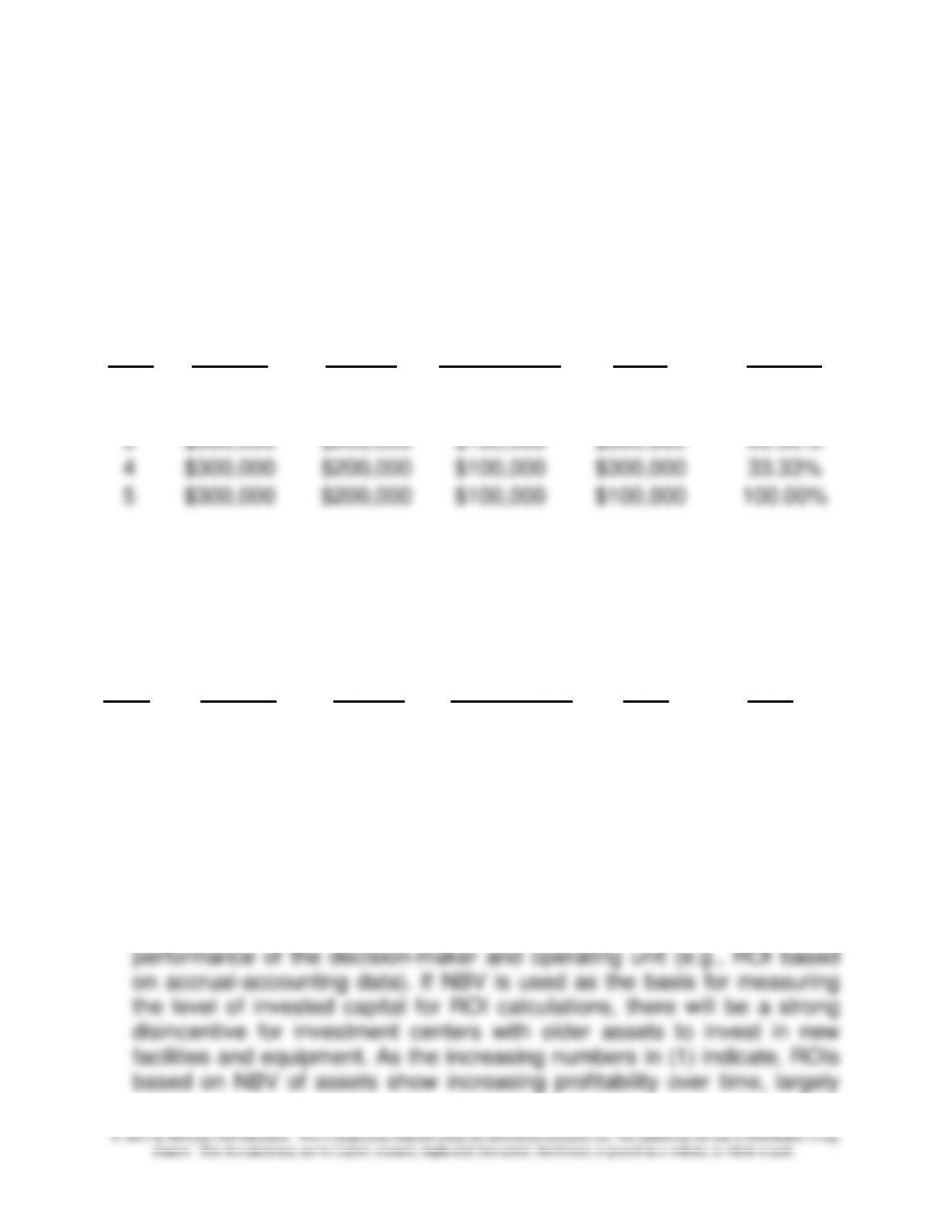

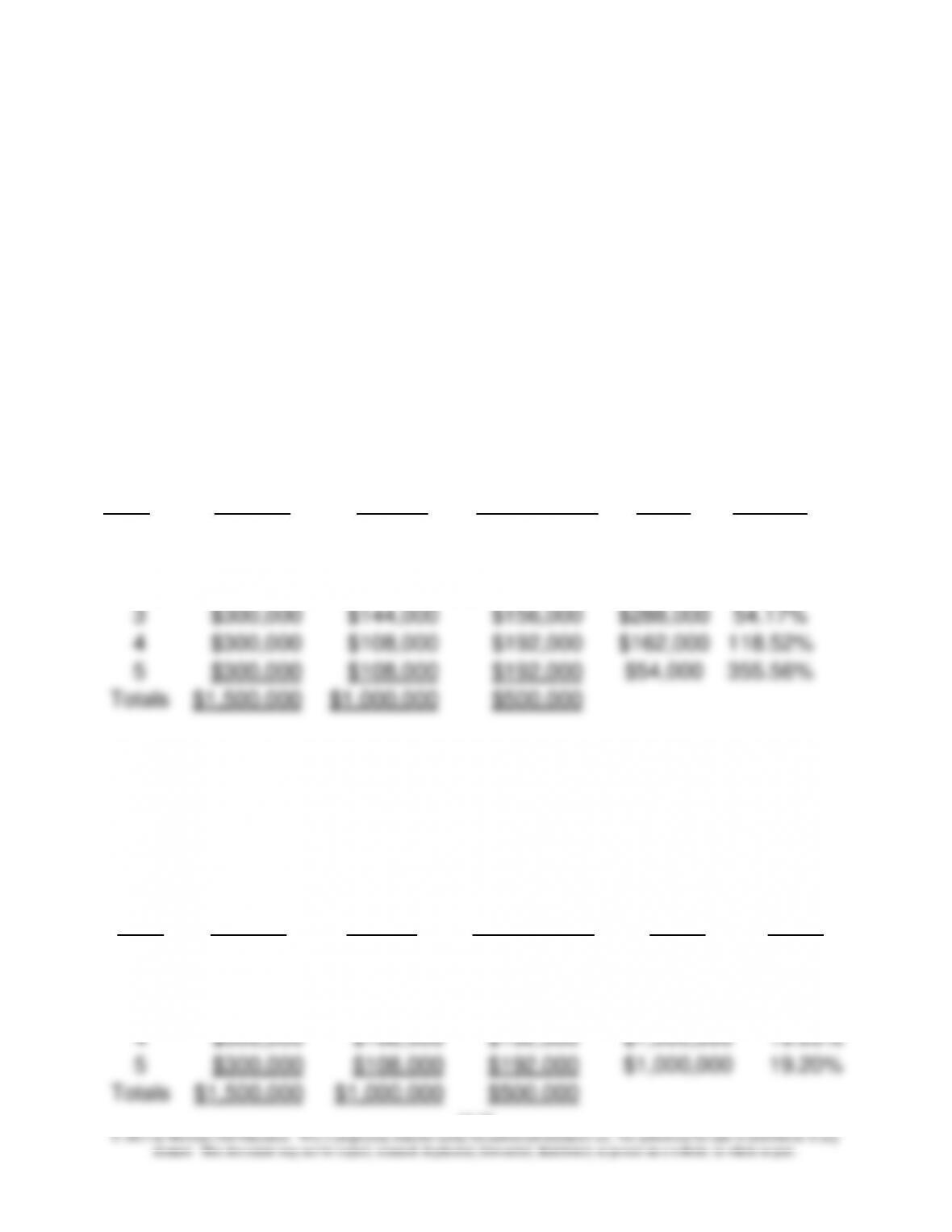

4. Year-by-Year ROIs, based on average NBV of the investment and

accelerated (DDB) depreciation, with a switch to SL depreciation in year

4:

Year

Income

Prior to

Deprec.

DDB

Depreciation

Charge

Operating

Income After

Depreciation

Average

NBV of

Asset

ROI

Based

on NBV

0

1

$300,000

$400,000

($100,000)

$800,000

(12.50%)

2

$300,000

$240,000

$60,000

$480,000

12.50%

3

$300,000

$144,000

$156,000

$288,000

54.17%

4

$300,000

$108,000

$192,000

$162,000

118.52%

5

$300,000

$108,000

$192,000

$54,000

355.56%

Totals

$1,500,000

$1,000,000

$500,000

Year–by-year ROIs, based on GBV of the investment and DDB depreciation

(with a switch to SL depreciation in year 4):

Year

Income

Prior to

Deprec.

DDB

Depreciation

Charge

Operating

Income After

Depreciation

Average

Gross

Book

Value

ROI

Based on

Gross

Book

Value

1

$300,000

$400,000

($100,000)

$1,000,000

(10.00%)

2

$300,000

$240,000

$60,000

$1,000,000

6.00%

3

$300,000

$144,000

$156,000

$1,000,000

15.60%

4

$300,000

$108,000

$192,000

$1,000,000

19.20%

5

$300,000

$108,000

$192,000

$1,000,000

19.20%

Totals

$1,500,000

$1,000,000

$500,000

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–30

19–36 (Continued-2)

Summary: the above results demonstrate that the bias associated with

the use of NBV versus GBV of the asset (investment) base is even more

pronounced if an accelerated depreciation method (such as DDB) is

used. This is because the rate of decrease in the denominator of the

ROI calculation is decreasing more rapidly.

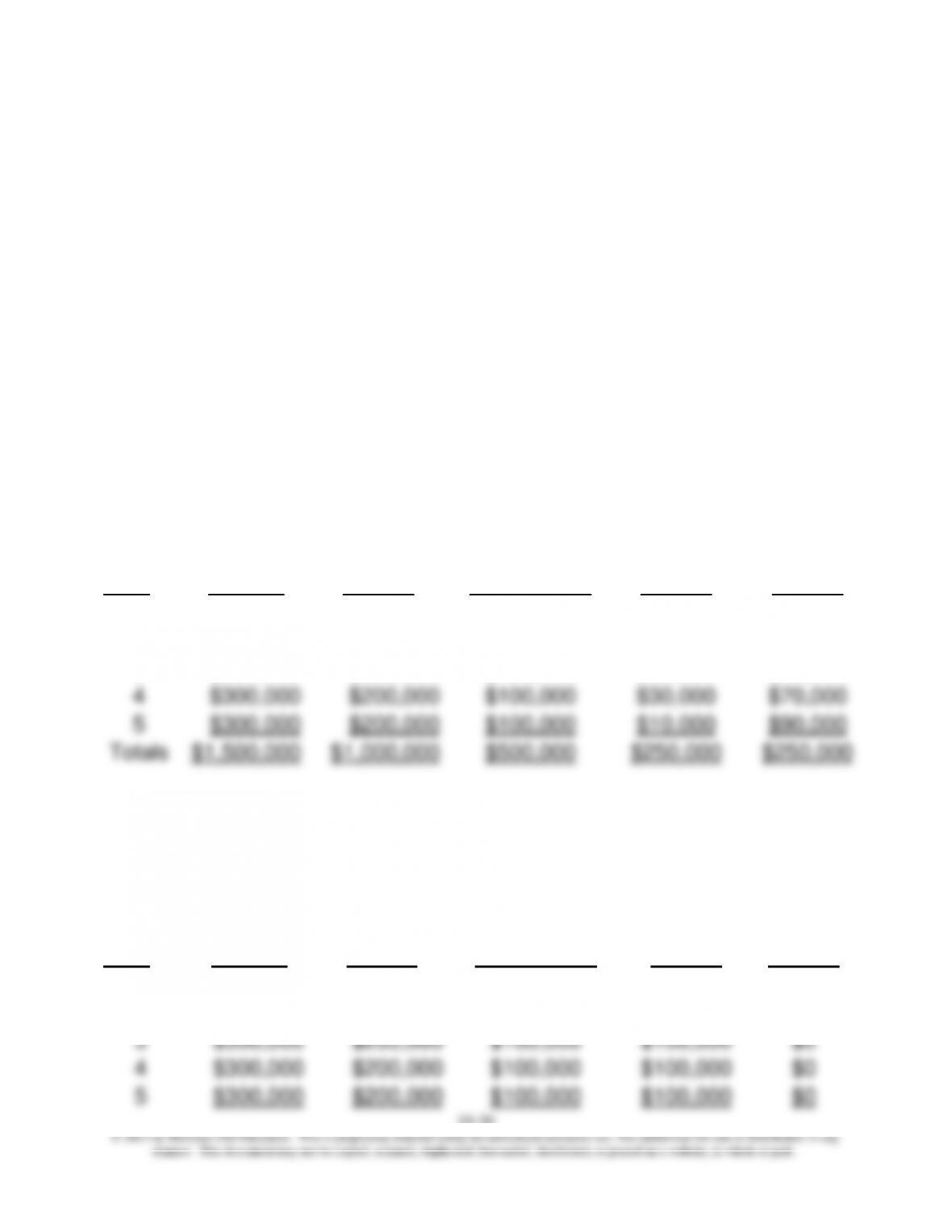

5. Year-by-Year Financial Results: Residual Income (RI)

a. Using average NBV of long-lived asset as the investment base, and SL

depreciation (per requirement 1 above):

Income

Operating

Income

Less:

Imputed

Year

Prior to

Deprec.

Depreciation

Charge

After

Depreciation

Capital

Charge

Residual

Income

1

$300,000

$200,000

$100,000

$90,000

$10,000

2

$300,000

$200,000

$100,000

$70,000

$30,000

3

$300,000

$200,000

$100,000

$50,000

$50,000

4

$300,000

$200,000

$100,000

$30,000

$70,000

5

$300,000

$200,000

$100,000

$10,000

$90,000

Totals

$1,500,000

$1,000,000

$500,000

$250,000

$250,000

b. Using GBV of long-lived assets as the investment base, and SL

depreciation (per requirement 2 above):

Income

Operating

Income

Less:

Imputed

Year

Prior to

Deprec.

Depreciation

Charge

After

Depreciation

Capital

Charge

Residual

Income

1

$300,000

$200,000

$100,000

$100,000

$0

2

$300,000

$200,000

$100,000

$100,000

$0

3

$300,000

$200,000

$100,000

$100,000

$0

4

$300,000

$200,000

$100,000

$100,000

$0

5

$300,000

$200,000

$100,000

$100,000

$0