Chapter 3 – Basic Cost Management Concepts

3-26

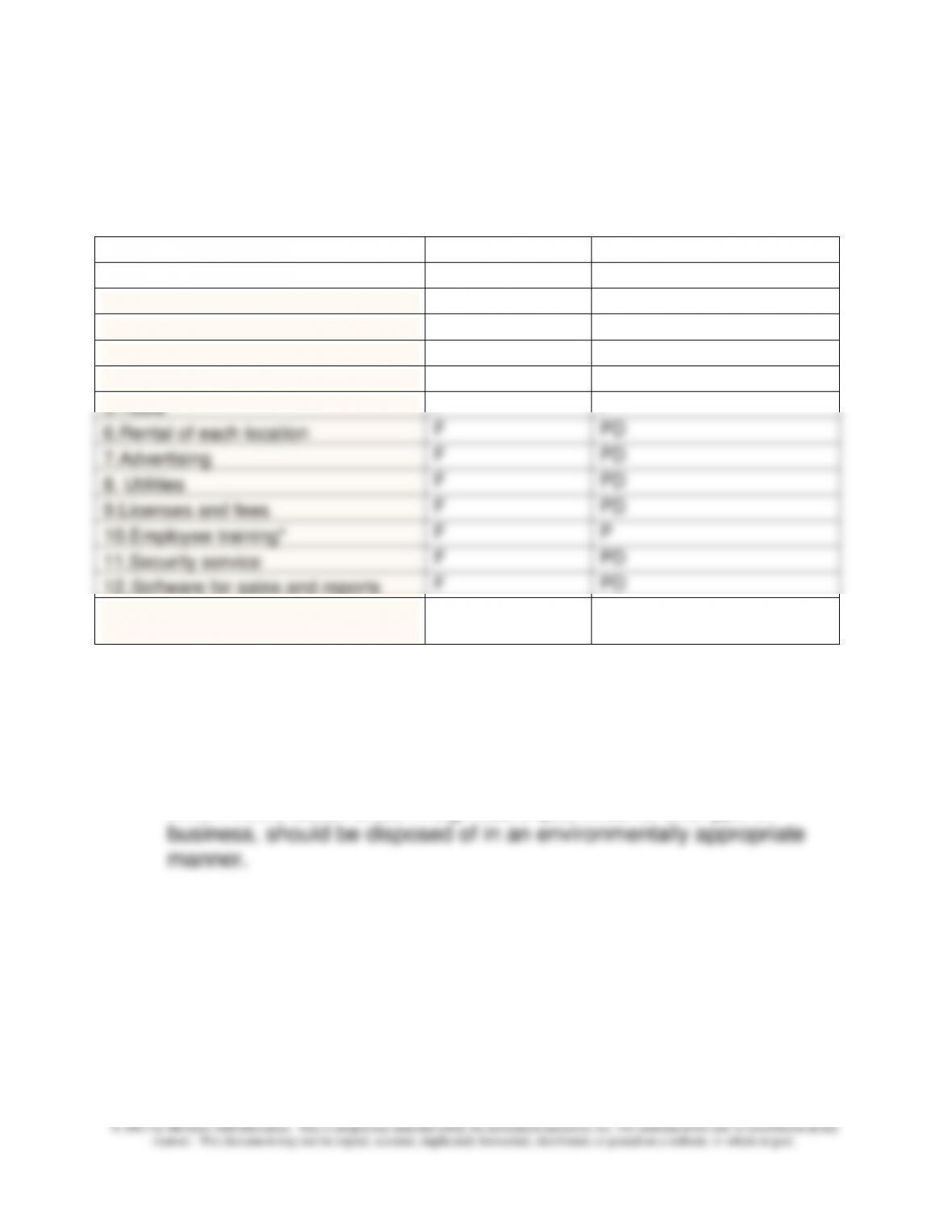

3-51 Classification of Costs (15 Min)

Parts 1 and 2

Fixed(F) or

Product (P)

Variable (V)

Period (PD)

1.Technicians

F

P

2.Parts

V

P

3.Purchase of oil and tires

V

P

4.Supplies

V

P

5.Tools

F

P

6.Rental of each location

F

PD

7.Advertising

F

PD

8. Utilities

F

PD

9.Licenses and fees

F

PD

10.Employee training*

F

P

11.Security service

F

PD

12. Software for sales and reports

F

PD

13. Disposal of waste oil and used

tires

V

PD

Employee training is considered a product cost because it is related to

direct labor of the technicians.

3. The disposal of waste oil and used tires is the critical environmental

issue for Speedy Auto Service. Both the waste oil and used tires,

which would accumulate in significant quantities for this type of

Chapter 3 – Basic Cost Management Concepts

3-27

PROBLEMS

3-52 Executional Cost Drivers: Internet Retailer (20 min)

The example of an internet retailer such as Bikes.com is a good

example of the type of firm that must pay close attention to

executional cost drivers. The reason is that its success depends on

execution, execution. The fall off in sales growth could be an

indication of problems in customer sales returns, that is customer

satisfaction and loyalty. Bikes.com can review sales records to

investigate.

Specific executional steps that Bikes.com can take include

looking for possible improvements in the purchase and stocking of

merchandise and the shipping of customer orders – the upstream and

downstream activities that must work smoothly to get the orders to

the customers quickly and accurately. Also, Bikes.com should

consider the work flow in the company. Can it be streamlined? Are

there non-value-adding activities that can be eliminated? What are

the bottlenecks, if any, that slow the process of accurately filling a

customer’s order? Also, are employees aware of the importance of

executional issues? Are the employees working together to achieve

effective cost management can lower the costs of operation and

speed the arrival of profits.

3-28

3-53 Structural Cost Drivers (25 min)

Case A: A key structural issue for Food Fare is complexity. As the

menu has changed, so will costs and service. More complexity

means higher food purchasing costs, higher operating costs, and

more complex operations. This will require new types of training for

technology to streamline the process of order taking and order filling

are likely to be necessary. Scale might also be an important issue in

this case – how large must each restaurant become, and how many

restaurants must the chain have in order to justify the increased

purchasing and stocking costs, and the new training and technology

costs?

Case B: A key issue in this case is the speed with which Gilman can

provide customer service. The speed of service provides value to the

customer and also increases profitability. In order to increase the

speed of service, Gilman needs effective communication and

coordination among the service teams. This is probably being

accomplished now by cell phone. Gilman can research new and

more effective ways to accomplish this, perhaps using hand-held

internet access devices, iphones, or other modem-equipped devices.

The advantage of computer-based access is that computer-based

demand and profitability – in order to better understand which

services and which types of customers are most profitable.

3-29

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

3-53 (continued –1)

Is it in installation or service, Brand X or Brand Y, residential or

Chapter 3 – Basic Cost Management Concepts

3-30

3-54 Cost of Goods Manufactured and Sold (30 min)

Statement of Cost of Goods Manufactured

For The Year Ended December 31, 2013

Direct Materials Used

Direct Materials Inventory, Beginning 25,000$

Direct Materials Purchases 555,000

Total Direct Materials Available 580,000

Direct Materials Inventory, Ending $40,000

Direct Materials Used 540,000$

Direct Labor 310,000

Factory Overhead

Indirect Mateials 66,000$

Utilities for Plant 38,000

Indirect Labor 70,000

Factory Rent 380,000

Total Factory Overhead 554,000

Total Manufacturing Costs Incurred during year 1,404,000

Work-in-Process Inventory, Beginning 45,000

Total Manufacturing Costs to Account for 1,449,000

Work-in-Process Inventory, Ending 40,000

Cost of Goods Manufactured 1,409,000$

Cost of Goods Sold

Finished Goods Inventory, Beginning 135,000$

Cost of Goods Manufactured 1,409,000

Total Goods Available for Sale 1,544,000

Finished Goods Inventory, Ending 75,000

Cost of Goods Sold 1,469,000$

Hamilton, Inc

Chapter 3 – Basic Cost Management Concepts

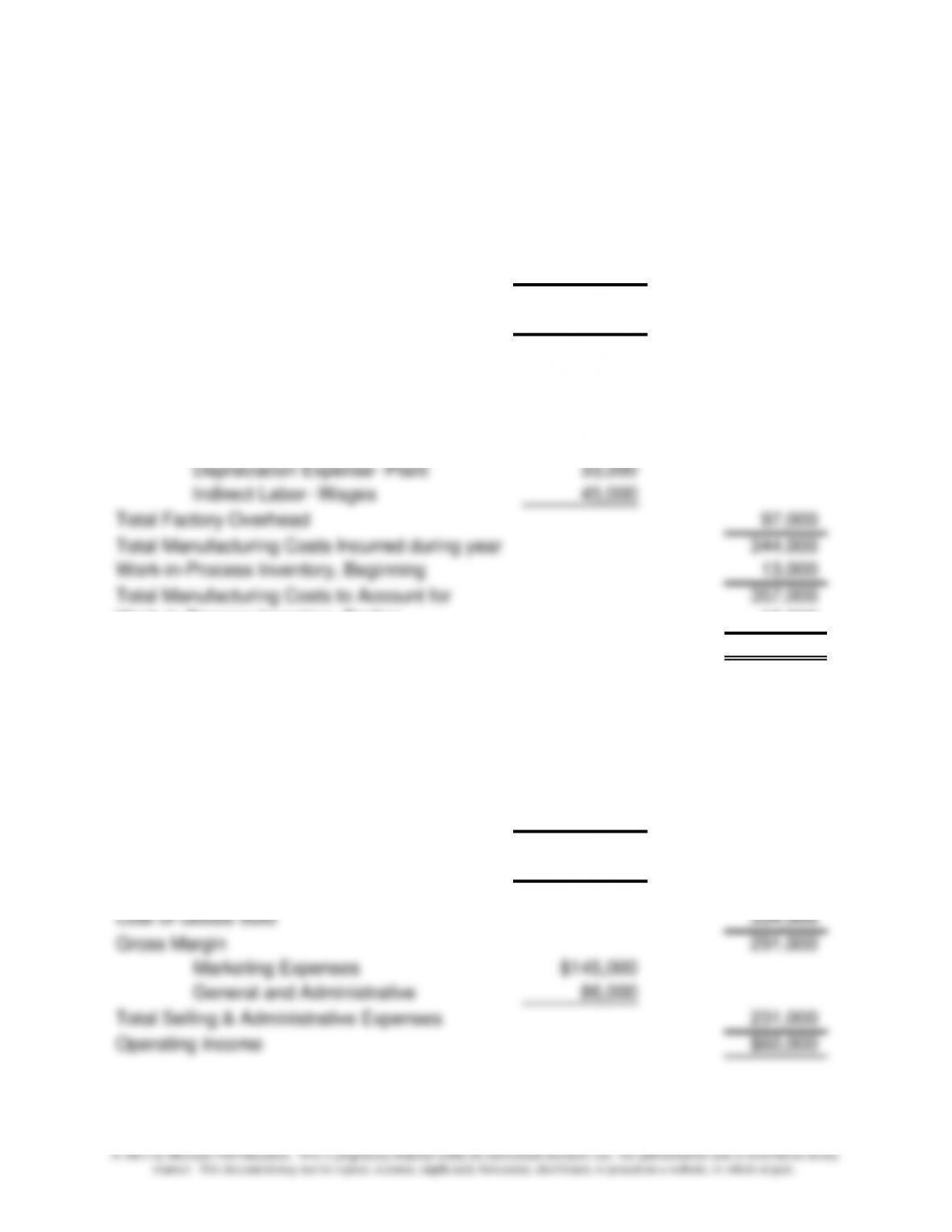

3-55 Cost of Goods Manufactured and Sold (30 min)

Blazek Company

Direct Materials Used

Direct Materials Inventory, Beginning $22,000

Direct Materials Purchases 165,000

Total Direct Materials Available 187,000

55,000

Direct Materials Used $132,000

Direct Labor–Wages 115,000

Factory Overhead

Repairs and Maintenance $11,000

Factory insurance 8,000

Depreciation Expense–Plant 33,000

Indirect Labor–Wages 45,000

Total Factory Overhead 97,000

Total Manufacturing Costs Incurred during year 344,000

Work-in-Process Inventory, Beginning 13,000

Total Manufacturing Costs to Account for 357,000

Work-in-Process Inventory, Ending 16,000

Finished Goods Inventory, Beginning $17,000

Cost of Goods Manufactured 341,000

Total Goods Available for Sale 358,000

Finished Goods Inventory, Ending 24,000

Cost of Goods Sold 334,000

Gross Margin 291,000

Marketing Expenses $145,000

General and Administrative 86,000

Total Selling & Administrative Expenses 231,000

Operating Income $60,000

For the Year Ended December 31, 2013

Statement of Cost of Goods Manufactured

Direct Materials Inventory, Ending

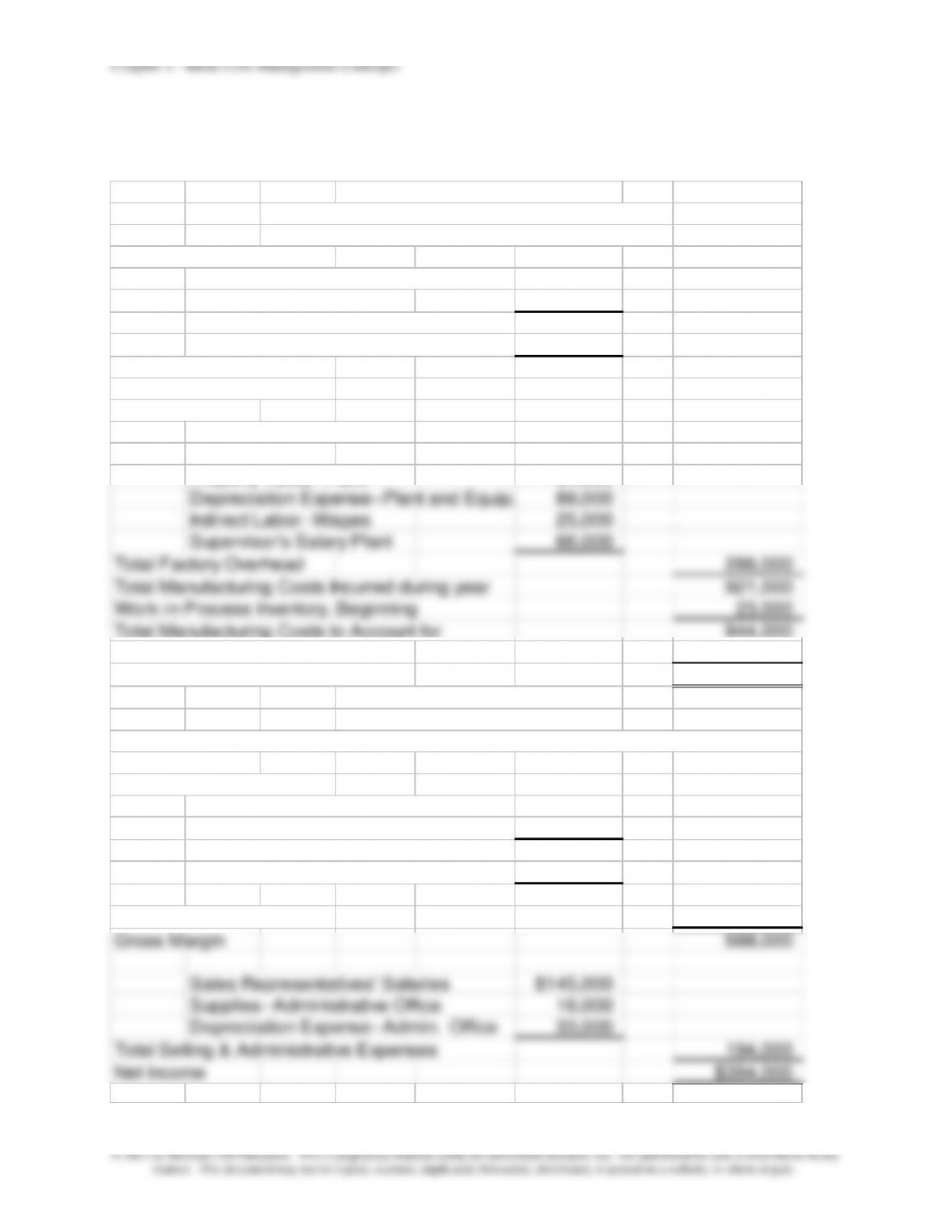

3-56 Cost of Goods Manufactured and Sold (30 min)

Household Furnishings, Inc.

Statement of Cost of Goods Manufactured

For the Year Ended December 31, 2013

Direct Materials Used

Direct Materials Inventory, Beginning $18,000

Direct Materials Purchases 155,000

Total Direct Materials Available 173,000

Direct Materials Inventory, Ending 25,000

Direct Materials Used $148,000

Direct Labor-–Wages 487,000

Factory Overhead

Heat, Light, & Power—Plant $44,000

Supplies–Plant 29,000

Property Taxes–Plant 34,000

Depreciation Expense–Plant and Equip.

88,000

Indirect Labor-–Wages 25,000

Supervisor’s Salary Plant 66,000

Total Factory Overhead 286,000

Total Manufacturing Costs Incurred during year 921,000

Work-in-Process Inventory, Beginning 23,000

Total Manufacturing Costs to Account for 944,000

Work-in-Process Inventory, Ending 9,000

Cost of Goods Manufactured $935,000

Household Furnishings, Inc.

Income Statement

Sales Revenue $1,500,000

Cost of Goods Sold

Finished Goods Inventory, Beginning $15,000

Cost of Goods Manufactured 935,000

Total Goods Available for Sale 950,000

Finished Goods Inventory, Ending 38,000

Cost of Goods Sold 912,000

Gross Margin 588,000

Sales Representatives’ Salaries $145,000

Supplies–Administrative Office 16,000

Depreciation Expense–Admin. Office 33,000

Total Selling & Administrative Expenses 194,000

For the Year Ended December 31, 2013

Chapter 3 – Basic Cost Management Concepts

3-33

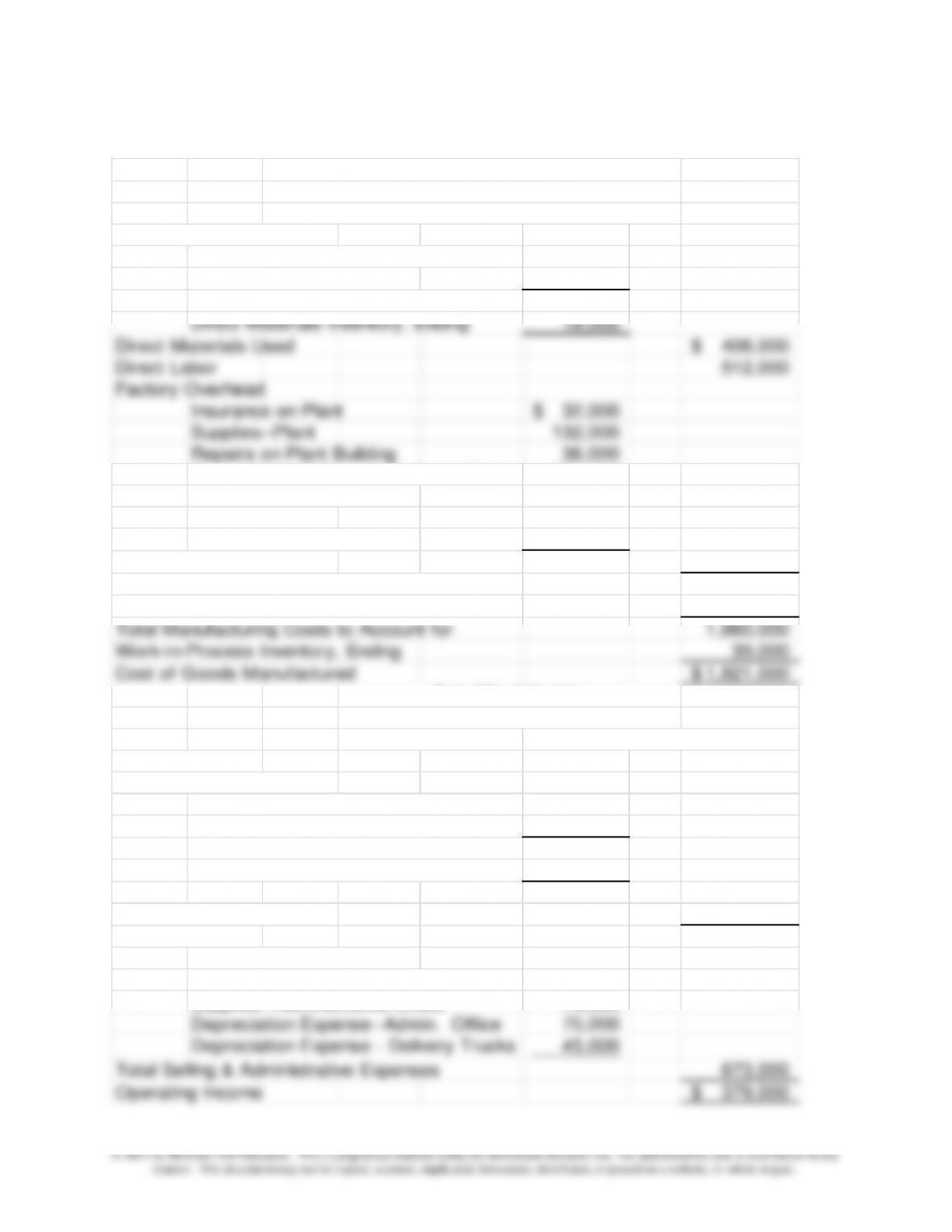

3-57 Cost of Goods Manufactured and Sold (30 min)

Statement of Cost of Goods Manufactured

For The Year Ended December 31, 2013

Direct Materials Used

Direct Materials Inventory, Beginning 16,000$

Direct Materials Purchases 410,000

Total Direct Materials Available 426,000

Direct Materials Inventory, Ending 18,000

Direct Materials Used 408,000$

Direct Labor 512,000

Factory Overhead

Insurance on Plant 32,000$

Supplies–Plant 132,000

Work-in-Process Inventory, Beginning 31,000

Total Manufacturing Costs to Account for 1,860,000

Work-in-Process Inventory, Ending 39,000

Cost of Goods Manufactured 1,821,000$

For the Year Ended December 31, 2013

Finished Goods Inventory, Beginning 55,000$

Cost of Goods Manufactured 1,821,000

Total Goods Available for Sale 1,876,000

Finished Goods Inventory, Ending 43,000

Cost of Goods Sold 1,833,000

Gross Margin 1,052,000

Advertising Expenses 150,000$

Sales Representatives’ Salaries 325,000

Supplies–Administrative Office 78,000

Depreciation Expense--Admin. Office 75,000

Depreciation Expense – Delivery Trucks 45,000

Total Selling & Administrative Expenses 673,000

Operating Income 379,000$

Fair Wind Yachts

Fair Wind Yachts

Income Statement

Chapter 3 – Basic Cost Management Concepts

3-58 Cost of Good Manufactured and Income Statement (40 min)

Direct Materials Used

Direct Materials Inventory, April 30 28$

Direct Materials Purchases 510

Freight in 15

Total Direct Materials Available 553

Direct Materials Inventory, May 31 23

Direct Materials Used 530$

Direct Labor-Wages 260

Factory Overhead

Indirect factory labor 90$

Utilities 108

Property taxes–-Plant 60

Insurance 12

Depreciation 50

Total Factory Overhead 320

Total Manufacturing Cost Incurred During Month 1,110

Work-in–Process Inventory, April 30 150

Total Manufacturing Costs to Account for 1,260

Work-in–Process Inventory, May 31 220

Cost of Goods Manufactured 1,040$

Norton Industries

Statement of Cost of Goods Manufactured

For the Month Ended May 31, 2013

($000) omitted

Chapter 3 – Basic Cost Management Concepts

3-58(continued -1)

Sales Revenue 1,488$

Less: Sales Discounts 20

Net Sales 1,468

Cost of Goods Sold:

Finished Goods Inventory, April 30 247$

Cost of Goods Manufactured 1,040

Total Goods Available for Sale 1,287

Finished Goods Inventory, May 31 175

Cost of Goods Sold 1,112

Gross Margin 356$

General, Selling, & Administrative Expense:

Office Salaries 122$

Sales Salaries 42

Depreciation 4

Interest 6

Total General, Selling, & Administrative Expense 218

Income from operations 138

Other revenue 2

Net Income 140$

Norton Industries

Income Statement

For the Month Ended May 31, 2013

($000) omitted