Chapter 10 – Strategy and the Master Budget

10–31

10-40 Activity–Based Budgeting (ABB) (20-30 Minutes)

1. Budgeted Cost-

Activity Activity Driver Rate Total Cost

Storage 400,000 $0.4925 $ 197,000

Requisition Handling 30,000 $12.50 $ 375,000

Pick Packing 800,000 $ 1.50 $1,200,000

2. Activity-related data are not available. The only data you have is that budgeted

fixed cost per month is $1,000,000 and budgeted variable cost per carton is

$1.30. Using this approach, what is the estimated cost for the month? Compare

and comment on how your answer here differs from the answer to Requirement 1.

Budgeted Cost for the Month:

based cost driver will not likely capture the underlying economics of the

company’s support activities and associate cost.

3. Expected saving in costs—January 2013:

Requisition Handling (@ $12.50/requisition) = $ 375,000

Data Entry: number of lines (@ $0.80/line) = 640,000

Chapter 10 – Strategy and the Master Budget

10–32

10-40 (Continued)

The ABC cost-rate data included above represent the estimated cost of resources

that are currently supplied by the company but which could be eliminated by the

introduction of an electronic order-processing system. Note, however, that in order

to achieve these savings, management of the company must take actions to cut

model does not reflect the resource demands/resource consumption of the current

process regardingthe processing of customer orders.

Chapter 10 – Strategy and the Master Budget

10-41 Activity–Based Budgeting (ABB) with Kaizen (40 Minutes)

1. Unit-Level: Pick packing, Data entry—Lines

Batch-Level: Requisition handling, Data entry—Requisitions,

Desktop delivery

2. Cost-driver rates:

Cost-Reduction Cost-Driver Rates

Activity Rate (per month) January February March

Requisition Handling 98% $12.50 $12.250 $12.0050

Pick Packing 99% $ 1.50 $ 1.485 $ 1.4702

Data Entry—Lines 99% $ 0.80 $ 0.792 $ 0.7841

Data Entry—Requisitions 98% $ 1.20 $ 1.176 $ 1.1525

Desktop Delivery 98% $30.00 $29.400 $28.8120

Budgeted Costs:

Activity

Activity Volume February March

Requisition Handling 30,000 $ 367,500 $ 360,150

Pick Packing 800,000 $1,188,000 $1,176,120

3. Factors that may influence the success of a continuous improvement

(Kaizen)program include:

▪ Reasonable or achievable cost reductions.

▪ Awareness of all employees on the expected (scheduled) cost improvements

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

10–34

10-41 (Continued)

4. Primary criticisms of Kaizen (continuous improvement) budgets include the

following:

▪ The budgeting process tends to place enormous pressure on employees

Chapter 10 – Strategy and the Master Budget

10–35

10-42 Time-Driven Activity-Based Budgeting (TDABB) (45-60 minutes)

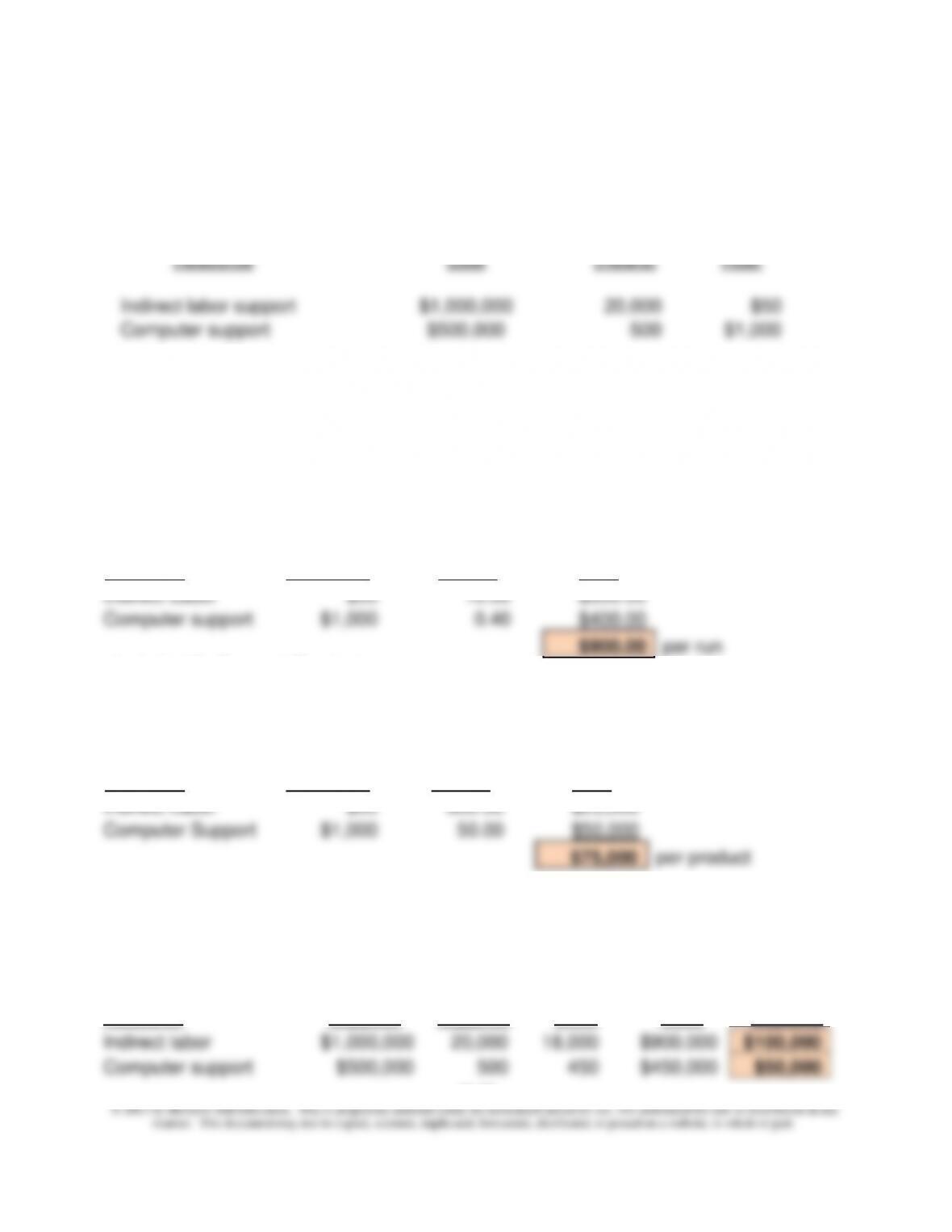

1. Calculation of budgeted resource costs per hour:

(Item 6)

(Item 5)

Practical

Budgeted

Budgeted

Capacity

Cost per

Resource

Cost

(Hours)

Hour

Indirect labor support

$1,000,000

20,000

$50

Computer support

$500,000

500

$1,000

2. Determination of the cost-driver rates for each activity (handle production runs, and

support product):

Activity #1: Handle Production Runs

(From 1

above)

(Item 3a,

4a)

Unit

Budgeted

Budgeted

Times

Cost-Driver

Resource

Cost/Hour

(hours)

Rate

Indirect Labor

$50

10.00

$500.00

Computer support

$1,000

0.40

$400.00

$900.00

per run

Activity #2: Support Products

(From 1

above)

(Item 3b,

4b)

Unit

Budgeted

Budgeted

Times

Cost-Driver

Resource

Cost/Hour

(hours)

Rate

Indirect Labor

$50

500.00

$25,000

Computer Support

$1,000

50.00

$50,000

$75,000

per product

3. Cost of unused capacity for the quarter, by resource:

(Item 6)

(Item 5)

(Given)

Cost of

Resource

Resource

Cost of

Cost of

Resource

Units

Units

Resources

Unused

Resource

Supplied

Supplied

Used

Used

Capacity

Indirect labor

$1,000,000

20,000

18,000

$900,000

$100,000

Computer support

$500,000

500

450

$450,000

$50,000

Chapter 10 – Strategy and the Master Budget

10–42 (Continued)

4. After implementing a TQM program, the company was able to implement process–

efficiency changes, the end result of which was a 10% reduction in the indirect labor

time associated with the activity “handling production runs.” Re-estimate the indirect

labor cost component of the cost to handle a production run. Also, recalculate the

Generally speaking, the cost of unused capacity should not be assigned to

actual units produced or customers served during the period. However, the cost

of unused capacity should not be ignored—it is someone’s responsibility in the

organization. That is, the cost of unused capacity for a period should be

assigned to the person or office that authorized the level of capacity when that

capacity was acquired. Typically, this assignment would be made on a “lump–

sum” basis. This assignment provides feedback to managers regarding their

resource supply/demand decisions.

Chapter 10 – Strategy and the Master Budget

10–37

10-43 Rolling Financial Forecasts (20 minutes)

1. “Rolling forecasts” of sales:

Month of

Forecast for Month of

Forecast

January

February

March

April

May

June

December

100

95

100

110

120

125

January

90

100

105

110

120

February

95

105

105

120

March

105

100

110

April

90

105

May

105

2. Three-month forecast error rates, March through June. (Note: Error rate = 1 –

absolute forecast error.) For example, the forecast error rate for March’s sales is

found by dividing the absolute value of the forecast error for this month by the actual

sales volume for the month. The forecast error for any month (e.g., March) is defined

Actual Sales

98

95

92

108

98

100

Forecast error rate

–

–

8.70%1

1.85%

22.45%

25.00%

Direction of error

–

–

Below

Below

Below

Below

1Example: (ABS(100 – 92)) ÷ 92 = 8.70% (below forecast)

Chapter 10 – Strategy and the Master Budget

10–38

10-44 Kaizen Budgeting (30-40 minutes)

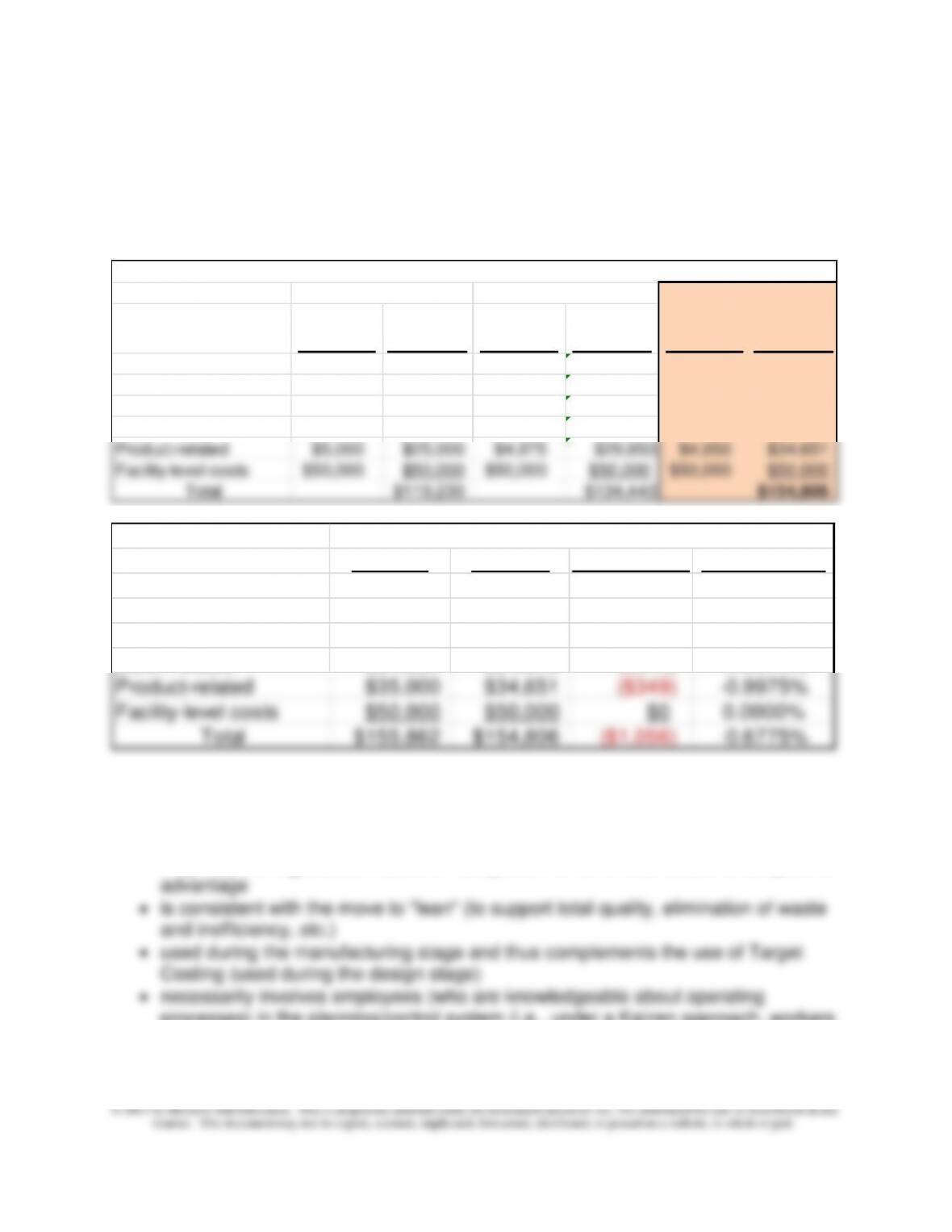

1. Recalculated budgeted factory overhead cost for June, under the assumption that,

starting in May, each budgeted cost-driver rate decreases by 0.5% relative to the

preceding month.

Cost Pools

Activity-

Cost Rate

Budgeted

Overhead

Activity-

Cost Rate

Budgeted

Overhead

Activity-

Cost Rate

Budgeted

Overhead

Semi-skilled, hour-relate

$0.60 $6,750 $0.597 $8,358 $0.594 $10,841

Skilled, hour-related $0.20 $900 $0.199 $1,114 $0.198 $1,445

Machine-hour-related $3.20 $21,280 $3.184 $26,172 $3.168 $33,297

Batch–related $1,700 $15,300 $1,692 $18,945 $1,683 $24,572

Product–related $5,000 $25,000 $4,975 $29,850 $4,950 $34,651

Facility-level costs $50,000 $50,000 $50,000 $50,000 $50,000 $50,000

Total $119,230 $134,440 $154,806

April

May

June

Activity-Based Budget (ABB)

Recap:

Cost Pools Original Revised $ Difference % Difference

Semi-skilled, hour-relate

$10,950 $10,841 ($109) –0.9975%

Skilled, hour-related $1,460 $1,445 ($15) –0.9975%

Machine-hour-related $33,632 $33,297 ($335) –0.9975%

Batch-related $24,820 $24,572 ($248) –0.9975%

Product-related $35,000 $34,651 ($349) –0.9975%

Facility-level costs $50,000 $50,000 $0 0.0000%

Total $155,862 $154,806 ($1,056) –0.6775%

Budgeted Amount for June

2. In general, the benefits associated with a move to continuous (i.e., Kaizen) budgeting

include the following:

• helps ensure that the budget is a forward-looking tool

• may help the organization stave off competition or otherwise secure a competitive

processes) in the planning/control system (i.e., under a Kaizen approach, workers

are assumed to have better knowledge as to how cost-saving goals can be

Chapter 10 – Strategy and the Master Budget

10–39

achieved); as such, its use is consistent with theories of decentralization and

worker empowerment

10-44 (Continued)

3. Principal concerns or limitations associate with Kaizen budgeting:

• a Kaizen approach places pressure on employees to meet continually revised (and

4. Examples of how Kerry Company could realize the cost savings referenced above in

Requirement 1: the activity cost rates are calculated as budgeted spending (on

resources) divided by the practical capacity (i.e., supply) of resources acquired.

Therefore, the rate can go down either because total budgeted spending is decreased,

or the supply of activities is increased while holding spending constant. Both would

seem to rest on notions of increasing efficiency. Some examples, referenced to text

Exhibit 10.19 might include the following:

• move to a JIT production system

• incorporate technology into (i.e., automate) the order-processing system used by

• requiring minimum order sizes (to eliminate short, unprofitable, production runs)

• effecting changes in the layout of the facility (e.g., to reduce movement and

storage of inventory

Notice, too, that in order to reduce spending (on resources), management has to take

direct and deliberate action to do so. This is due in large part because some of the

Chapter 10 – Strategy and the Master Budget

10–40

10-45 Resource Capacity Planning (20 minutes)

1. Likely result of the decision to raise prices?

Current calculation, fixed operating cost per meal = $1,100 ÷ 175 meals/day

= $6.29/meal

Recalculated fixed operating cost per meal, based on available capacity (meals per

attempt to recover “cost.” In all likelihood, however, the rising prices of meals would

exacerbate the situation, leading the business to a downward (or what some refer to

as “death”) spiral.

2. Alternative approach for allocating daily fixed operating cost to each meal:

The owners of this business should consider calculating the fixed operating cost per

meal based on “practical capacity.” This practice would avoid the downward business

spiral referred to above and attributable to an escalating “cost” per meal. In fact,

using some notion of capacity would allow the owners to make an assessment of the

Chapter 10 – Strategy and the Master Budget

10–41

10-46 Budgetary Pressure and Ethics (20-30 minutes)

1. The use of alternative accounting methods to manipulate reported earnings is

professionally unethical because it violates the Standards contained in the IMA’s

Statement of Ethical Professional Practice (see: www.imanet.org). The

Competence standard is violated because of failure to perform duties in

objectively.

2. Yes, costs related to revenue should be expensed in the period in which the

revenue is recognized (“matching principle”). Perishable supplies are purchased

for use in the current period, will not provide benefits in future periods, and should

therefore be matched against revenue recognized in the current period. In short,

the accounting treatment for supplies was not in accordance with generally

3. The actions of Gary Woods were appropriate. Upon discovering how supplies

were being accounted for, Wood brought the matter to the attention of his

immediate superior, Gonzales. Upon learning of the arrangement with P&R,

Wood told Gonzales that the action was improper; he then requested that the

accounts be corrected and the arrangement discontinued. Wood clarified the

approaching Lin without Gonzales’s knowledge and by having a confidential

discussion with an impartial advisor.

Chapter 10 – Strategy and the Master Budget

10–42

10–47 Comprehensive Profit Plan (90 minutes)

1. Sales Budget

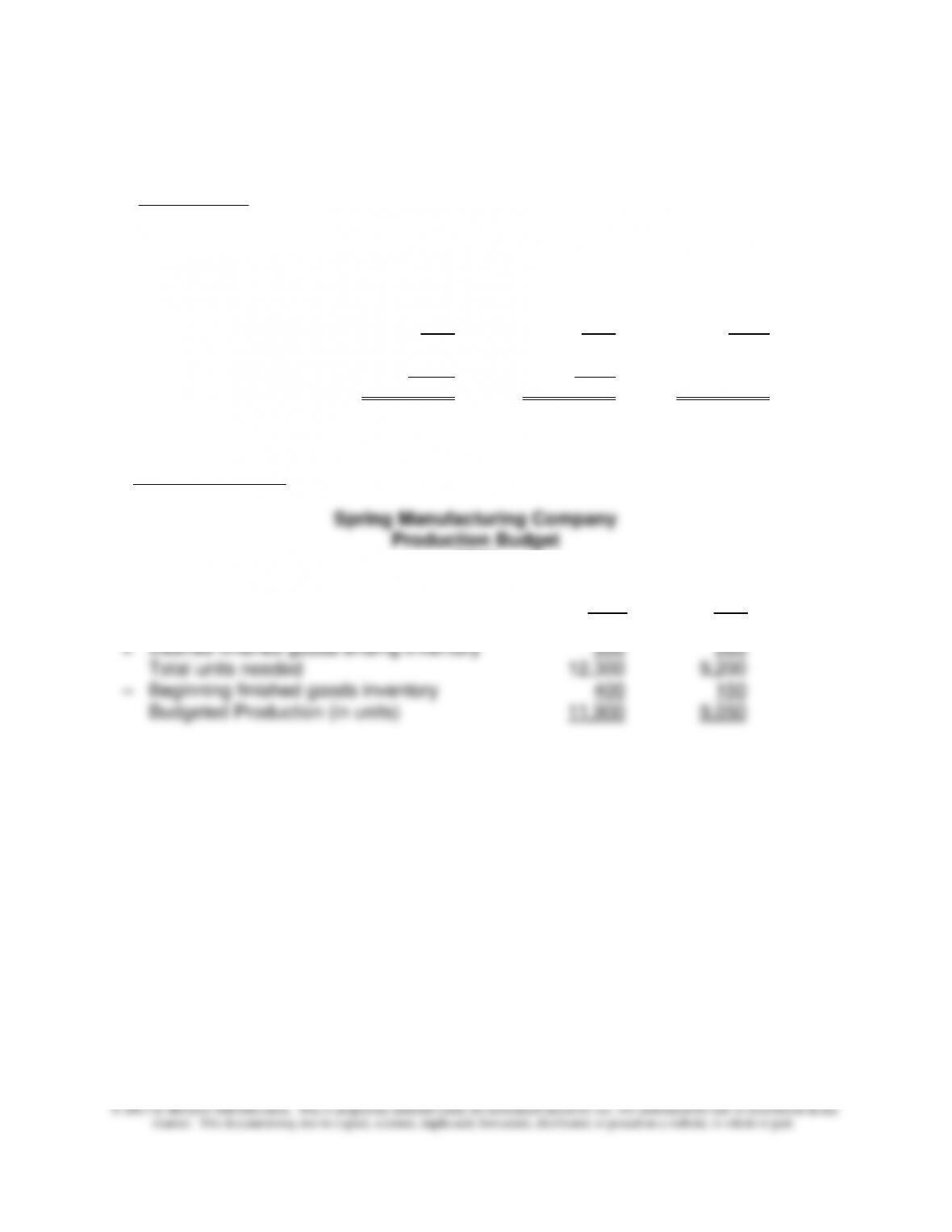

Spring Manufacturing Company

Sales Budget

2013

C12 D57 Total

Sales (in units) 12,000 9,000 21,000

× Selling Price Per Unit $150 $220

Total Sales Revenue $1,800,000 $1,980,000 $3,780,000

2. Production Budget

2013

C12 D57

Budgeted Sales (in units) 12,000 9,000

10–43

10-47 (Continued-1)

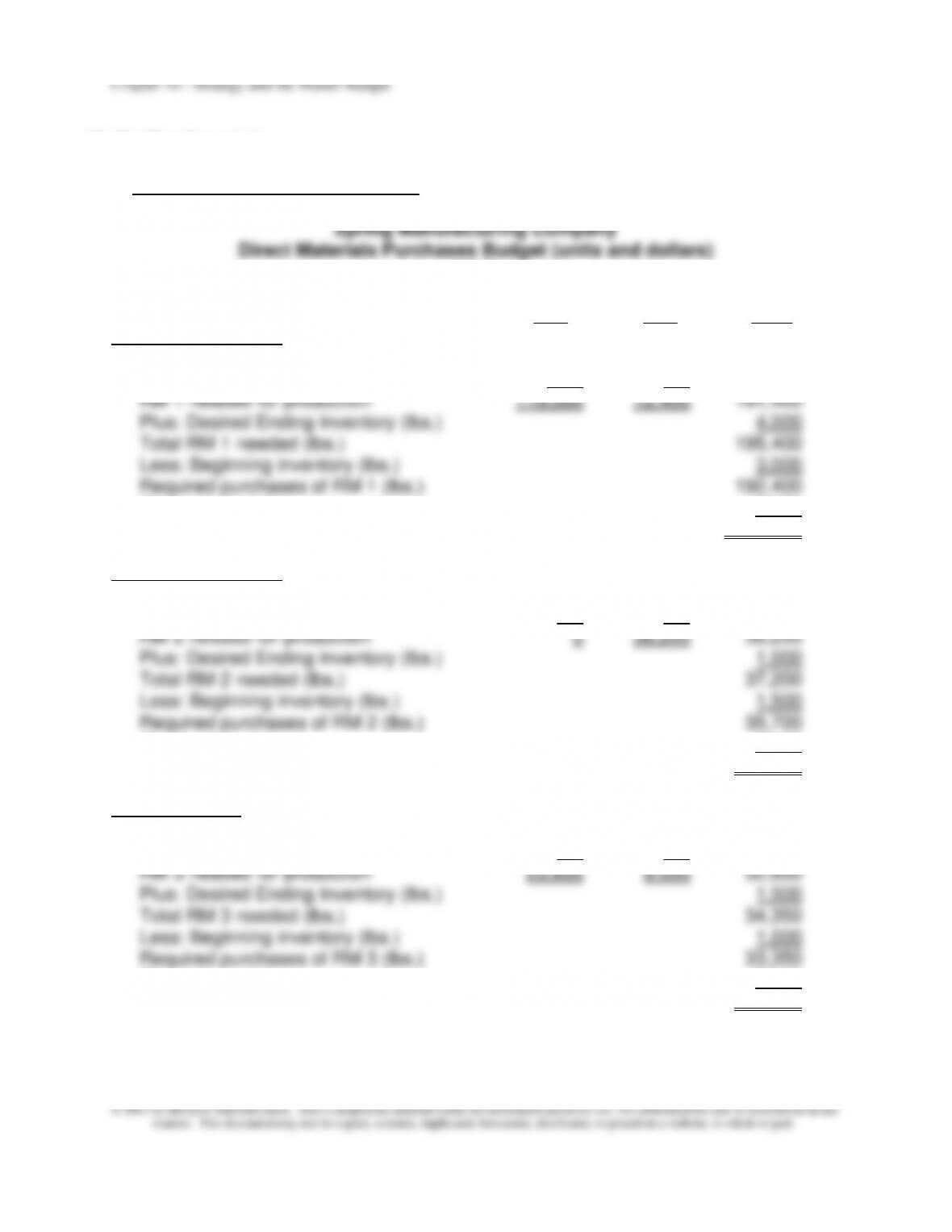

3. Direct Materials Purchases Budget

2013

C12 D57 Total

Raw Material (RM) 1:

Budgeted Production 11,900 9,050

Pounds per Unit × 10 × 8

Cost per pound $2.00

Budgeted purchases, RM 1 $384,800

Raw Material (RM) 2:

Budgeted Production 11,900 9,050

Pounds per Unit × 0 × 4

Cost per pound $2.50

Budgeted purchases, RM 2 $89,250

Raw Material 3:

Budgeted Production 11,900 9,050

Pounds per Unit × 2 × 1

Cost per pound $0.50

Budgeted purchases, RM 3 $16,675

10–44

10–47 (Continued-3)

4.Direct Manufacturing Labor Budget

Spring Manufacturing Company

Direct Labor Budget

2013

C12 D57 Total

Budgeted production 11,900 9,050

Direct labor hours per unit × 2 × 3

Budgeted direct labor costs $1,273,750

5. Factory Overhead Budget

Spring Manufacturing Company

Factory Overhead Budget

2013

Variable Factory Overhead:

Indirect materials $10,000

Miscellaneous supplies and tools 5,000

Indirect labor 40,000

Fixed Factory Overhead:

Supervision $120,000

Maintenance costs 20,000

Heat, light, and power 43,420

10–45

10-47 (Continued-4)

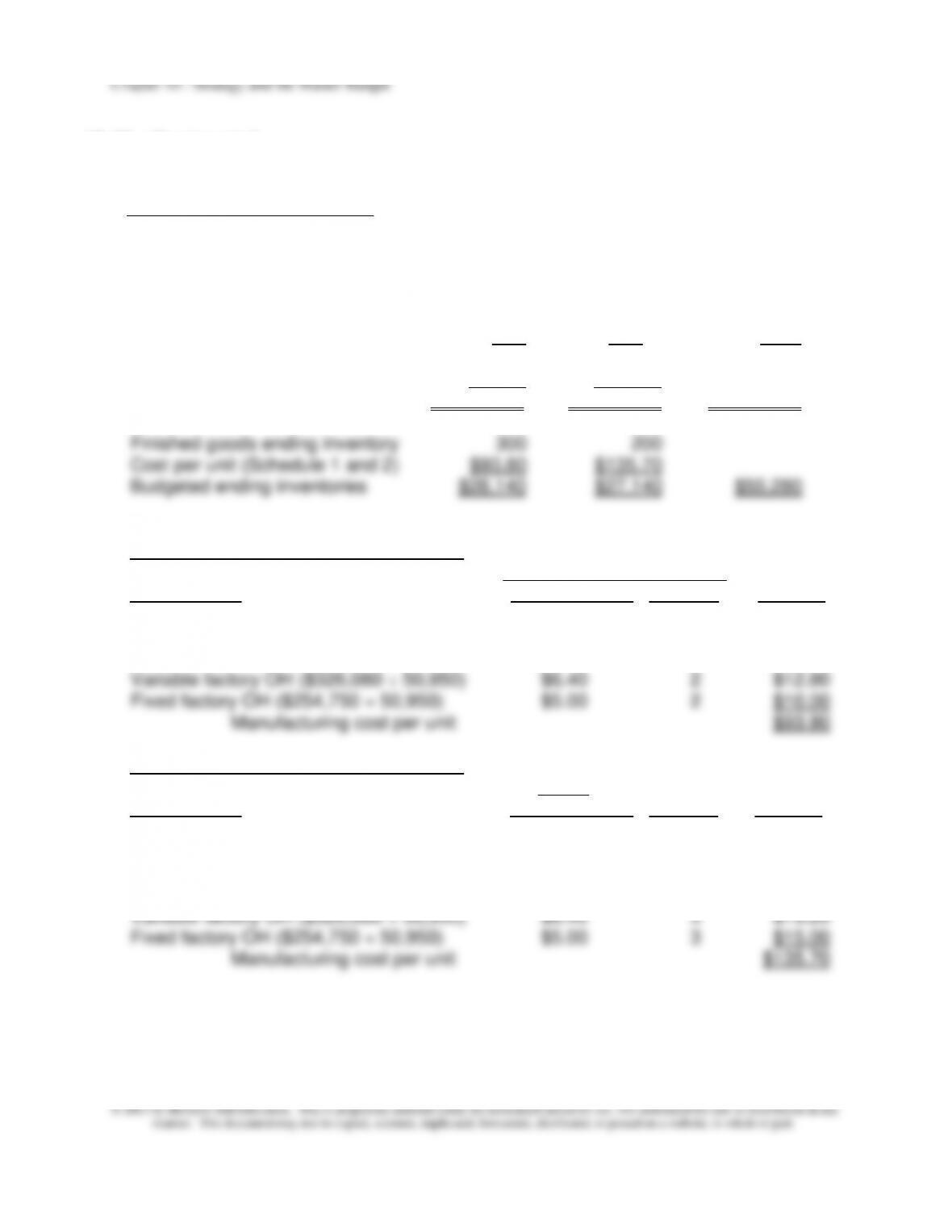

6.Budgeted Cost of Goods Sold

Spring Manufacturing Company

Ending Finished Goods Inventory and Budgeted CGS

2013

C12 D57 Total

Sales volume 12,000 9,000 21,000

Cost per unit (Schedule 1 and 2) $93.80 $135.70

Cost of goods sold $1,125,600 $1,221,300 $2,346,900

Schedule 1: Cost per Unit—Product C12:

Inputs_____ Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 10 $20.00

RM-3 $0.50 2 $1.00

Direct labor $25.00 2 $50.00

Schedule 2: Cost per Unit—Product D57:

Inputs Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 8 $16.00

RM-2 $2.50 4 $10.00

RM-3 $0.50 1 $0.50

Direct labor $25.00 3 $75.00