Chapter 10 – Strategy and the Master Budget

10–76

10–55 (Continued-2)

3. Sensitivity Analysis: Revision of the original 12-month budget created above in (1) to

cancellation rate to 0.75%. (See following page for answer.)

Chapter 10 – Strategy and the Master Budget

10–77

10-55 (Continued-3)

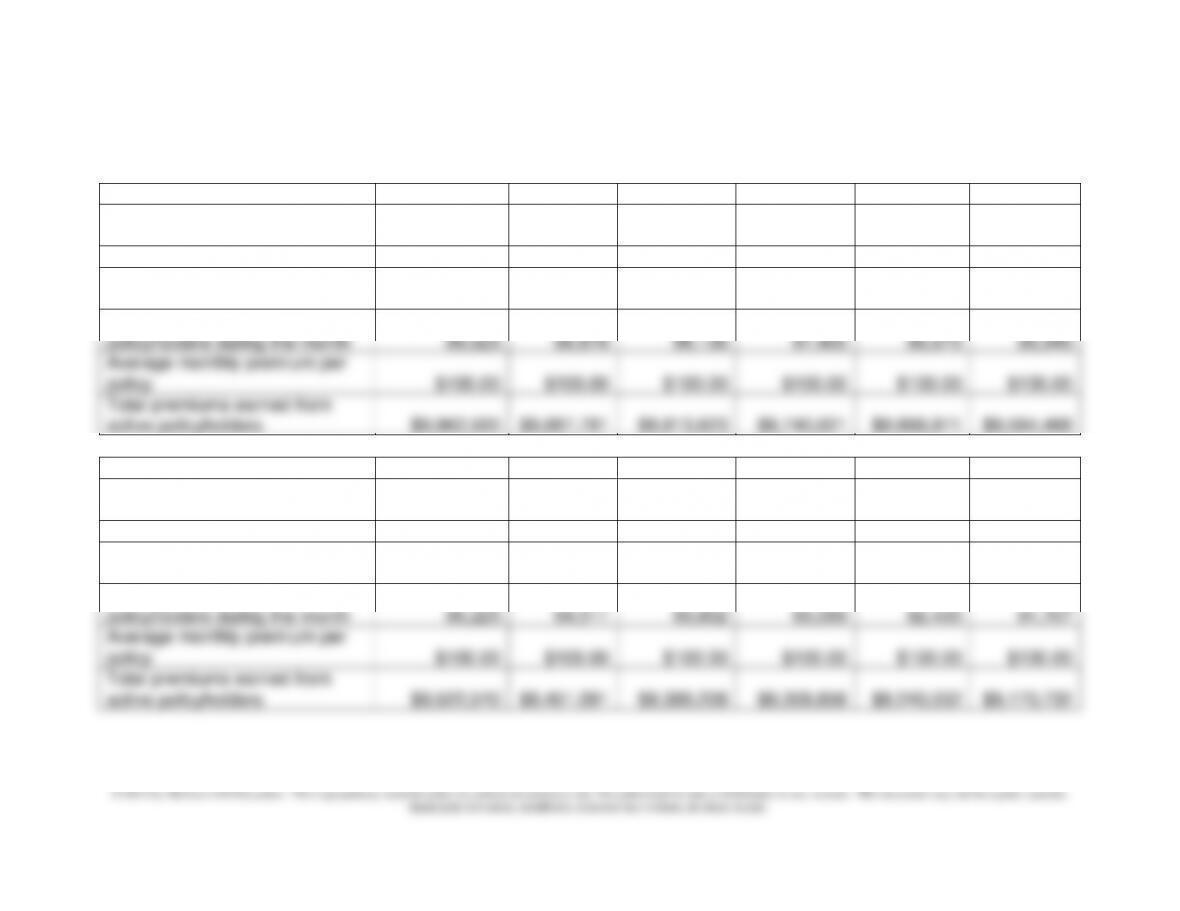

Budget Item

January

February

March

April

May

June

No. of active policyholders,

beginning of the month

100,000

99,250

98,506

97,767

97,034

96,306

Mid-term cancellation rate (%)

0.75%

0.75%

0.75%

0.75%

0.75%

0.75%

No. of active policyholders, end

of the month

99,250

98,506

97,767

97,034

96,306

95,584

Average no. of active

policyholders during the month

99,625

98,878

98,136

97,400

96,670

95,945

Average monthly premium per

policy

$100.00

$100.00

$100.00

$100.00

$100.00

$100.00

Total premiums earned from

active policyholders

$9,962,500

$9,887,781

$9,813,623

$9,740,021

$9,666,971

$9,594,468

Budget Item

July

August

September

October

November

December

No. of active policyholders,

beginning of the month

95,584

94,867

94,155

93,449

92,748

92,053

Mid-term cancellation rate (%)

0.75%

0.75%

0.75%

0.75%

0.75%

0.75%

No. of active policyholders, end

of the month

94,867

94,155

93,449

92,748

92,053

91,362

Average no. of active

policyholders during the month

95,225

94,511

93,802

93,099

92,400

91,707

Average monthly premium per

policy

$100.00

$100.00

$100.00

$100.00

$100.00

$100.00

Total premiums earned from

active policyholders

$9,522,510

$9,451,091

$9,380,208

$9,309,856

$9,240,032

$9,170,732

Chapter 10 – Strategy and the Master Budget

10–55 (Continued-4)

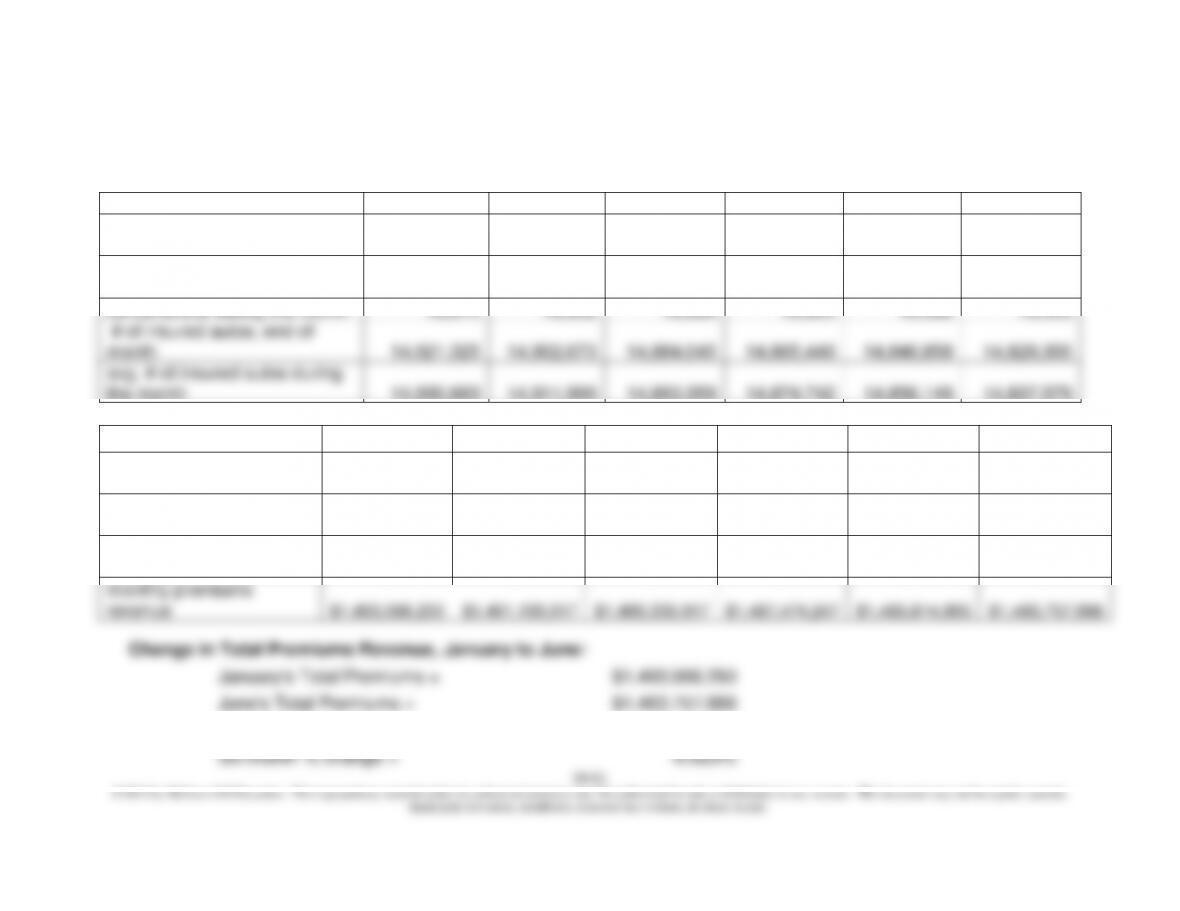

Active policies, end of December

91,362

Policy renewal rate

80.00%

No. of estimated policyholders, beginning of new year

73,090

Recap:

Premiums Earned, original assumptions

$116,462,500

Premiums Earned, revised assumptions

$114,739,793

% change

-1.48%

Estimated policy renewals, end of year:

Original assumption

80,038

Revised assumption

73,090

% change

-8.68%

4. What other information or data would be included in a full budget prepared each

month for this insurance company?

This question is meant to reinforce real-world complexities in the budget-

preparation process and the interrelationship(articulation) of various sub-budgets.

The following are some additional considerations for the present insurance

company example:

a) The schedules presented above assumed that the renewal date for all

policyholders was the end of December. Naturally, this is a simplification. In

reality, policyholders renew their policies throughout the entire year. Thus,

one can view the present analysis as 1/12th of the budgets that would have to

be prepared.

b) Policyholder attrition rate is a variable that has to be modeled. Most

organizations workingin financial services, such as an insurance company

where there are large numbers of policyholders paying monthly premiums,

would have sophisticated policyholder-retention models that measure the

separate elements of mid-term cancellations and policy renewals. With

appropriate predictive models, a company could quickly forecast the number

of active customers in any given period. In the present case, the two

Chapter 10 – Strategy and the Master Budget

10–79

010- 55 (Continued-5)

c) In the case of life insurance, where different policyholders pay different

monthly premiums, the estimation of insurance premiums earned each month

becomes more challenging.

d) For simplicity we assumed a constant monthly mid-term cancellation rate. The

use of sophisticated business intelligence tools might provide finer forecasts

each period.

e) This problem provides an excellent opportunity to introduce, within a financial

services context, the important role that “rolling financial forecasts” can play,

and the associated superficiality of a traditional 12-month fixed budget.

f) It is likely that some of the non-financial indicators in this company’s budget

(e.g., customer attrition rates) would also be included in the “Customer

Perspective” of the company’s Balanced Scorecard (BSC). This is principally

because these nonfinancial performance indicators are leading indicators of

future financial performance.

10–80

10-56: Budgeting Insurance Policy Volume and Monthly Revenues (75 Minutes)

1. Monthly budgets broken down into three parts: marketsize and volume; volume for National Auto Insurance

Company; and, Premium Revenues earned.

January

February

March

April

May

June

Part a: Market Size &

Volumes

Total # of households (market

size)

100,000,000

100,050,000

100,100,025

100,150,075

100,200,150

100,250,250

% of households—car

ownership

80.00%

80.00%

80.00%

80.00%

80.00%

80.00%

avg. # of cars owned per

household

2.2

2.2

2.2

2.2

2.2

2.2

% of car owners with insurance

85.000%

85.085%

85.170%

85.255%

85.341%

85.426%

total # of insured autos

(market-wide)

149,600,000

149,824,475

150,049,286

150,274,435

150,499,922

150,725,747

market share of National Auto

Insurance

10.00%

10.001%

10.001%

10.002%

10.002%

10.003%

# of autos insured by National,

end of mo.

14,960,000

14,983,197

15,006,429

15,029,698

15,053,002

15,076,343

Chapter 10 – Strategy and the Master Budget

10–56 (Continued-2)

Change in Total Premiums Revenue, January to June:

January’s Total Premiums =

$1,493,066,250

June’s Total Premiums =

$1,483,757,886

Six-month Dollar Change =

-$9,308,364

Six-month % change =

-0.623%

January

February

March

April

May

June

Part b: Volume for National

Auto Insurance

# of autos insured, beginning

of month

14,940,000

14,921,325

14,902,673

14,884,045

14,865,440

14,846,858

cancellations during the month

18,675

18,652

18,628

18,605

18,582

18,559

# of insured autos, end of

month

14,921,325

14,902,673

14,884,045

14,865,440

14,846,858

14,828,300

avg. # of insured autos during

the month

14,930,663

14,911,999

14,893,359

14,874,742

14,856,149

14,837,579

January

February

March

April

May

June

Part c: Volume for

National Auto Insurance

# of autos insured during

the month

14,930,663

14,911,999

14,893,359

14,874,742

14,856,149

14,837,579

avg. insurance premium

per auto per month

$100.00

$100.00

$100.00

$100.00

$100.00

$100.00

monthly premiums

revenue

$1,493,066,250

$1,491,199,917

$1,489,335,917

$1,487,474,247

$1,485,614,905

$1,483,757,886

Chapter 10 – Strategy and the Master Budget

10–56 (Continued-3)

2. What additional real-life refinements would you envision for the budgets you

prepared above in (1)? What additional budgets would you anticipate preparing for

the company were you in charge of the budget-preparation process?

a) As the person in charge of the budget-preparation process, one obvious

recommended change would be to report separately the number of new policies

written (the logical offset in Part b to the number of policy cancellations). Currently

the number of new policy-holders is buried somewhere in part a of the budget.

Thus, a significant improvement is to disclose prominently each month the net

change in (average) policies outstanding, which is defined as the difference

between the number of new policies written and the number of policy cancellations.

b) In the example problem we assumed, for simplicity, that all policyholders paid

the same premium. Alternatively, we used an average premium rate per month per

policy, which is acceptable for budgeting purposes as long as the mix of

calendar year, January through December. A fuller, more realistic analysis would

gather similar data for policyholders whose anniversary date is something other

than January 1st. Whether the profiles of such policyholders is different from the

profile assumed above is an empirical question.

d) The cancellation rate, and growth rate in new underwritings, would probably be

monitored carefully since these are key drivers of future financial performers. That

is, they are “leading indicators” of financial performance and as such would

(i.e., policies cancelled before the annual renewal date).It would seem

appropriate, however, to include in the model a policy-renewal rate (85%, 90%,

etc.).

f) The above calculations and budgets deal solely with forecasted volume (# of

policies) and premiums revenue ($). The output of the budgetswe prepared would

then be used to prepare other budgets for the company. In this sense, and similar

to the extended example in thechapter, we say that the budgets articulate with

one another. For example, once a budget for volume and sales has been

Chapter 10 – Strategy and the Master Budget

information from both of these budgets would be used to forecast staffing needs,

what we might call “claims handling.” Claims processing times, the mix of “simple”

versus “complicated” claims, the average time to process a claim, the time

10–56 (Continued-4)

available per day (month) for each claims handler, the % of submitted claims that

are paid, etc. would all be “drivers” that would be incorporated into the claims–

processing budget.

g) The budget as presented is static in nature and covers a fixed period of time.

For reasons discussed more fully in the chapter, the limitations of such budgets

can be addressed by generating “rolling forecasts.”

3. The budgets you prepared above in (1) can be referred to as “driver–based

budgets.” List some of the pros and the cons of such budgets,relative to traditional

budgeting practices.

Pros

1. Driver-based budgeting (e.g., traditional activity-based budgeting (ABB) or

Time-Driven Activity-Based Budgeting) reduces the time to produce a

budget or to re-forecast.

2. Driver-based budgeting requires fewer iterations—that is, it reduces the “give

and take” and time devoted to the “negotiations” aspect of traditional

budgets.

3. Driver-based budgeting saves costs—for example, overtime payments

(required to support time-consuming traditional budgeting processes) can

be eliminated; similarly, part-time (temporary) help to support the traditional

budget-preparation process can be reduced or eliminated. Managers are

“freed” to attend to more strategic imperatives.

4. Driver-based budgets make managers accountable—situations such as

decreases in efficiency or unused capacity become more visible under

driver-based budgeting.

5. Driver-based budgeting provides insight and agility—if drivers are

appropriately chosen, then information about # of transactions and cost-

driver quantities for the period aid in the end–of-month evaluation of

Chapter 10 – Strategy and the Master Budget

10–84

productivity ratios, unit resource costs, etc.).

7. Driver-based budgeting may decrease the amount of “gaming behavior” on

the part of managers and employees. With driver-based budgeting causal

relationships are transparent, a situation that can limit the opportunity for

“gaming.” There is simply less opportunity to fool senior managers if all of

the assumptions in budgets are laid out for everyone to see.

10–56 (Continued-5)

Cons

1. Driver-based budgeting is perceived to be difficult to implement.

2. Driver-based budgets require a sophisticated information processing system–

-that is, the ability to capture, across the organization, key resource drivers,

activity cost drivers, and activities.

Chapter 10 – Strategy and the Master Budget

10–85

10-57 Budgets for a Service Firm (45-50 Minutes)

1. The annual cash budget is presented on the next page.

2. Operating problems that Triple-F Health Club could experience include:

▪ The cash contribution from lessons and classes will decrease because the

projected wage increase for lesson and class employees is significantly greater

than the projected increases in revenues (i.e., in additional volume). Last year,

the cash generated from these operations was $39,000 ($234,000 – $195,000).

The 2015 projection is only $12,675 ($304,200 – $291,525).

▪ Operating expenses are increasing faster than revenues from membership fees.

Last year (2014), cash generated from regular operations was $91,000

avoid cash crises, the club should prepare monthly cash budgets to help cash

management.

▪ Non-operational payments are projected to use up virtually all of the cash

generated from operations. Given the recent declines in mortgage interest rates,

management should consider refinancing this debt to reduce this cash drain.

3. Jane Crowe’s concern with regard to the Board’s expansion goals is justified. The

2015 budget projections show only a minimal increase in the cash balance (i.e., an

increase of only $2,757). The total cash available is well short of the $60,000 annual

Chapter 10 – Strategy and the Master Budget

10–86

10–57 (continued)

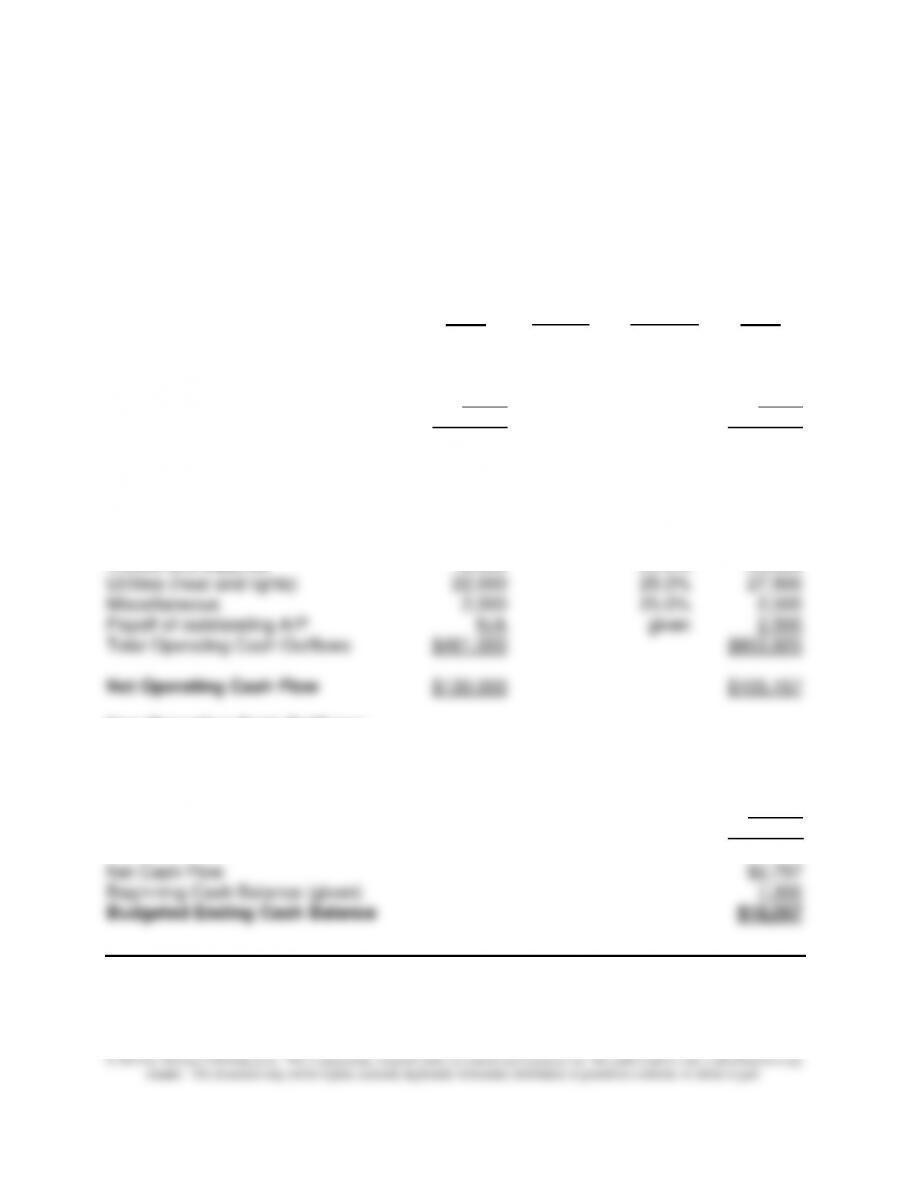

TRIPLE-F HEALTH CLUB

Cash Budget

For the Year Ending October 31, 2015

Price

2014 Growth Increase 2015

Operating Cash Inflows:

Annual membership fees $355,000 3.0% 10.0% $402,215

Lesson and class fees 234,000 30.0% 304,200

Miscellaneous 2,000 33.33% 2,667

Total Operating Cash Inflows $591,000 $709,082

Operating Cash Outflows:

Manager’s salary and benefits $36,000 15.0% $41,400

Employee wages and benefits:

Regular employees 190,000 15.0% 218,500

Lesson and class employees 195,000 30.0% 15.0% 291,525

Towels and supplies 16,000 25.0% 20,000

Non-Operating Cash Outflows:

Payoff of equipment payable given $15,000

Mortgage principal given 30,000

Mortgage interest 32,4001

Planned equipment purchases given 25,000

Total Non-Operating Cash Outflow $102,400

1$360,000 × 0.09 = $32,400($360,000 = principal balance at beginning of the year)

10–87

10–58 Sustainability (60 minutes)

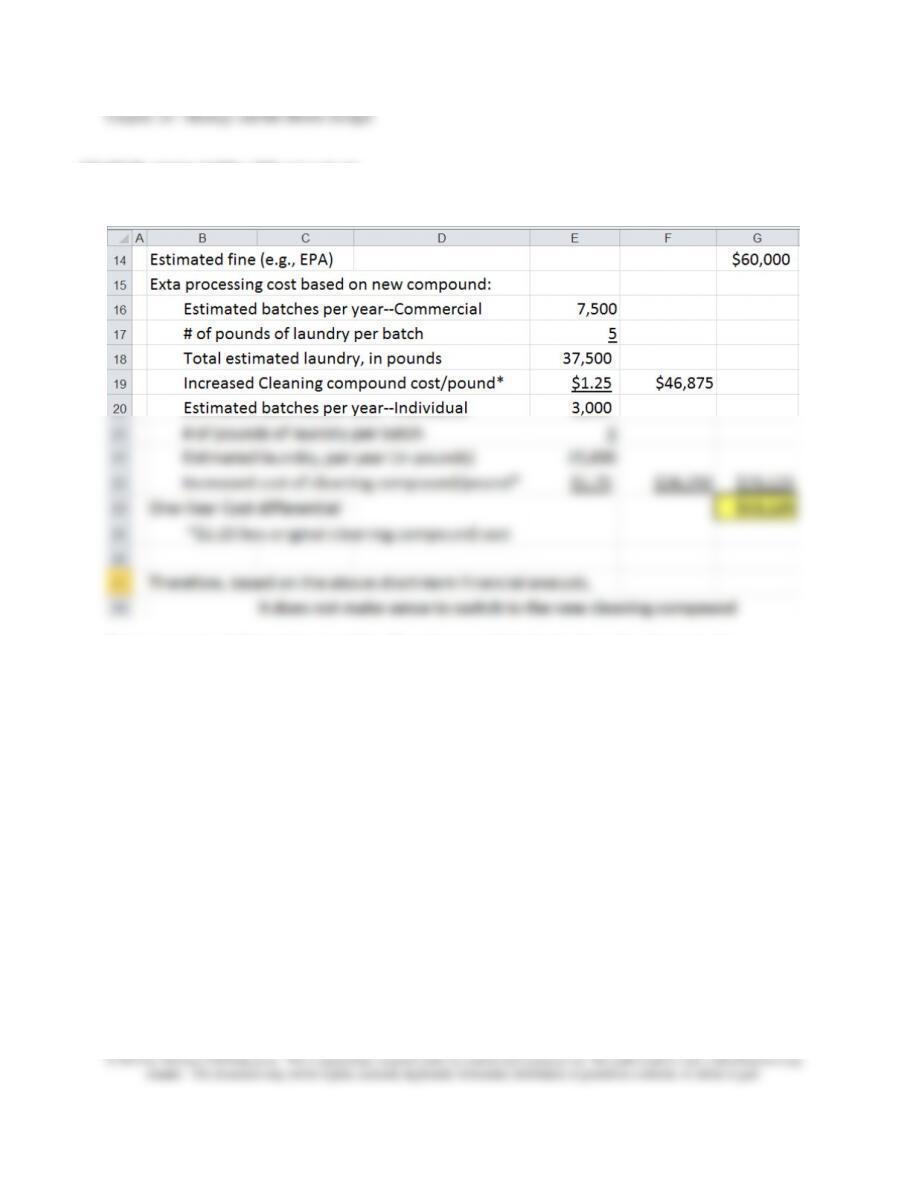

Requirement 1: Short-Term Financial Analysis

For purposes of illustration (and for Requirement 3 below), the cell reference for

$13,125 (above) is G24; the cell reference for $60,000 (above) is G14.

Chapter 10 – Strategy and the Master Budget

10–88

Requirement #2: Assume the Switch to the New Compound and the Introduction of Continuous-

Improvement (Kaizen) Budgeting

Estimated increase in processing cost, per year with new compound (from above) =

$73,125

Estimated annual cost savings, per Kaizen budget:

Original Monthly Processing Costs (other than materials):

Commercial:

Labor ($4.00/batch x 7,500 batches/year ÷ 12 months/year) $2,500.00

Electricity ($1.50/batch x 7,500 batches/year ÷ 12 months/year) $937.50

Individual:

Labor ($4.00/batch x 3,000 batches/year ÷ 12 months/year) $1,000.00

Electricity ($1.00/batch x 3,000 batches/year ÷ 12 months/year) $250.00

Total Monthly Processing Costs (Other than Materials) $4,687.50

Original Annual Processing Costs (other than materials) $56,250.00