Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-1

CHAPTER 16:

OPERATIONAL PERFORMANCE MEASUREMENT: FURTHER

ANALYSIS OF PRODUCTIVITY AND SALES

QUESTIONS

16-1 Productivity is the ratio of output to input. It is a measure of the amount of output

16-2 To be a successful low cost provider in its industry a firm needs to be able to

manufacture the product using fewer resources - materials, labors, or other

16-3 Two of the most often used criteria for assessing productivity and their

advantages and disadvantages are:

1. Prior year’s productivity

Advantages:

Disadvantages:

• Difficult to assess adequacy of productivity improvements

2. Best performance of the industry or practice

Advantages:

• Uses of the best practice in the industry or anywhere as the benchmark. A

Disadvantages:

• The standard might be too high and can be frustrating to workers.

the operation.

16-4 Operational productivity is the conversion ratio of an input resource to the output.

It is a physical measure on the unit of output produced from one unit of a

resource.

Financial productivity measures the relationship between the output and the cost

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-2

of one or more of the input resources. It is a measure of the unit of output or the

sales values of output produced per dollar of one or more resources.

16-5 Partial productivity is a productivity measure that focuses only on the relationship

between the amount of one input and the output attained. Both the input

(denominator) and the output (numerator) can be either in unit or in dollar

16-6 Financial productivity contains more information only in the sense that it

facilitates comparisons of different resources.

A financial productivity, however, can be confusing or less useful to

resources.

16-7 To say that a total productivity measure encompasses all partial productivity

measures is a misnomer. A total productivity measure may not examine the

16-8 The primary purpose of calculating productivity is to improve the operation.

Improvements on high-value-added activities decrease costs of the activities

16-9 Manufacturing personnel often prefer operational productivity measures to

financial productivity measures because data for computing operational

16-10 Measurements of productivity help managers to improve operations of both JIT

and non-JIT firms. However, a JIT firm is more likely to have less low-value-

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-3

16-11 (b). (a) is false because a higher productivity would be reflected by a higher, not

lower, partial productivity ratio. (c) is false because an operational partial

16-12 Measures for assessing marketing effectiveness include market share, market

size, selling price, sales mix, and sales quantity, and sales volume variances.

16-13 The components of sales variance include selling price and sales volume

variances. A sales volume variance is the total of sales quantity and sales mix

16-14 A selling price variance measures the effects of deviations in actual selling prices

from the budgeted selling prices on operating results, including effects on

16-15 A sales volume variance is the difference between the flexible budget for the

units sold during a period and the budgeted units in the master budget of the

period. For a firm with multiple products the sales volume variance can be the

The sales volume variance = the sales quantity variance plus the sales mix

variance

16-16 This statement is not always true. A multi-product firm can still have an

unfavorable sales volume variance even if it sold more units than the budgeted

16-17 Selling price and sales volume variances are the two major components that

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-4

16-18 A market size variance measures the effect of changes in the size of a product’s

total market on a firm’s total contribution margin or operating income. A market

market on its total contribution margin or operating income.

16-19 A firm benefits from a favorable sales quantity variance only if there are no

adverse changes in selling prices or sales mix variances. A favorable sales

quantity variance may not be beneficial to the firm if the firm lowered its selling

prices or sold more of low-priced, low-margin and less of high-priced, high-

margin products.

An increase in the total market size often leads to a favorable sales

quantity variance. Strategically, the favorable sales quantity variance may not be

favorable to the firm if the firm has an unfavorable market share variance.

However, a firm can have a favorable market size variance and an

variance and an unfavorable market share variance when the increase in the

number of units sold is less than the proportional to the increase of the total

market. The sales quantity variance would be unfavorable if a firm sold fewer

units than the budgeted units although the firm experienced a favorable market

share variance when the decrease in the total number of units was less than the

decrease in the total market.

16-20 A sales volume variance can be divided into sales quantity and sales mix

16-21 A firm can increase its earnings through reducing expenses, even if it sold fewer

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-5

BRIEF EXERCISES

16-22

a. First, calculate the Sales Mix Ratios:

Budget Actual

Quantity Ratio Quantity Ratio

R66 1,200 .75 1,000 .5

R100 400 .25 1,000 .5

16-23

16-24

a. Total sales volume variance:

R66: (1,000 - 1,200) x $10 = $ 2,000 U

16-25

a.

Market share:

Actual: 3,000 / 100,000 = 3%

Budget: 1,600 / 32,000 = 5%

16-6

16-26

a. Market size variance: (100,000 - 32,000) x 5% x $25 =

16-27

16-28

a.

Operational Partial Productivity = Actual Production/Actual Input

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-7

EXERCISES

16-29 Productivity and Strategy; Manufacturing (15 min)

1. The companies mentioned in the exercise (Harley-Davidson,

General Electric, Texas Instruments, and Coca-Cola) have different

competitive strategies: some are differentiators and others are cost

leaders. In each case, the workforce reductions were intended to

improve profits. The important question is how the workforce

reductions will affect the long-term competitiveness of each of the

companies. For example, Harley-Davidson’s management believes

that it is preparing for a long-term decline in sales, and that the

reduction in capacity is needed to match the future demand. This is

an appropriate response for the projected sales decline. Harley can

maintain its differentiated product line, and continue to succeed as a

smaller company. The strategic issue centers on this projection of

lower sales for the indefinite future; if sales do pick up due to

improving economic conditions, then Harley will be at a competitive

disadvantage since it will not be able to meet the rising demand. The

highly-experienced workforce will be hard to replace in a short

amount of time.

The same strategic issues face General Electric (GE) and

Texas Instruments (TI). For both companies, it is critical to project

long-term demand accurately. General Electric, like Harley, has

product lines that require highly-skilled labor, such as the GE unit that

manufactures aircraft engines. In contrast, the highly automated

manufacturing plants at Texas Instruments means that workforce

reductions (a) will not improve profits as quickly since most costs are

tied up in manufacturing facilities and equipment, and (b) will be more

easily replaced since the factory is automated. The case of Coca-

Cola is similar to TI.

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-8

16-29 (continued -1)

2. The companies’ main focus is to maintain and improve profits,

through workforce reductions. These reductions are likely to improve

productivity, at least in the short run, as the cuts in labor costs must

be larger than the decline in output in order to improve profits.

Whether or not the productivity gains can be maintained depends on

the companies’ ability to maintain expected levels of output with the

smaller workforce, through improvements in efficiency, manufacturing

methods, and workplace policies and procedures which promote

efficiency.

Source: Kate Lindebaugh, “Lean Companies Ready to Cut,” The Wall

Street Journal, October 24, 2011, p. B1; Scott Thurm and Joe Light,

“Propelling the Profit Comeback,” The Wall Street Journal, October 3,

2010; Nelson D. Schwartz, ”Industries Find Surging Profits in Deeper

Cuts,” The New York Times, July 25, 2010.

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-9

16-30 Productivity; Sustainability (15 min)

1. UPS succeeds by having on-time delivery of packages worldwide.

On-time performance is essential for competitive success, while cost

control in the delivery process is key to profitability. To achieve cost

control, UPS uses a variety of techniques including GPS software for

drivers to avoid left turns (because they take longer and use more

fuel than right-hand turns), instructing drivers to carry ignition keys on

attention to any of the vehicle’s parts that are worn or damaged.

Overall, this means a more efficient and reliable fleet of trucks.

2. The telematics system not only allows for fuel savings (25 gallons per

truck per year) but it also makes it possible for UPS to promptly

correct any problems with a truck’s emission controls. On balance,

the system provides an important means for the company to improve

Source: “Squeezing More Green Out of Brown,”

BloombergBusinessweek, September 20, 2010, p. 43.

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-10

16-31 Productivity and Quality Improvement in Retail (15 min)

This exercise introduces the contrast between productivity and quality, the

latter a topic covered in the following chapter, chapter 17. See also 16-35.

The question is intended for class discussion, to prompt some thinking

about the nature of productivity, quality, efficiency and similar terms. How

do productivity and quality differ?

The discussion can take many directions, but some key points should be

pointed out:

1. Productivity as described in this chapter is a measure of output to

input, and thus fits very well a manufacturing context. It can also be

applied to service and retail contexts if the output is properly defined.

firms use to reduce waste and improve efficiency. Quality

improvement will likely increase productivity.

In sum, productivity is a measure, and quality improvement

methods such as Six Sigma are the means that improve the

productivity measure.

2. Lean manufacturing, also explained in chapter 17 along with quality

improvement, is another means of reducing waste, improving

as Six Sigma) and lean manufacturing in the context of productivity.

3. Toyota and the Toyota Production System (TPS) described at the

beginning of this chapter are often referred to as leaders in lean

manufacturing and quality improvement. While TPS was developed

Source: “The Six Sigma Black Belts are Back,” Business Week,

September 21, 2009, p. 64-65.

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-11

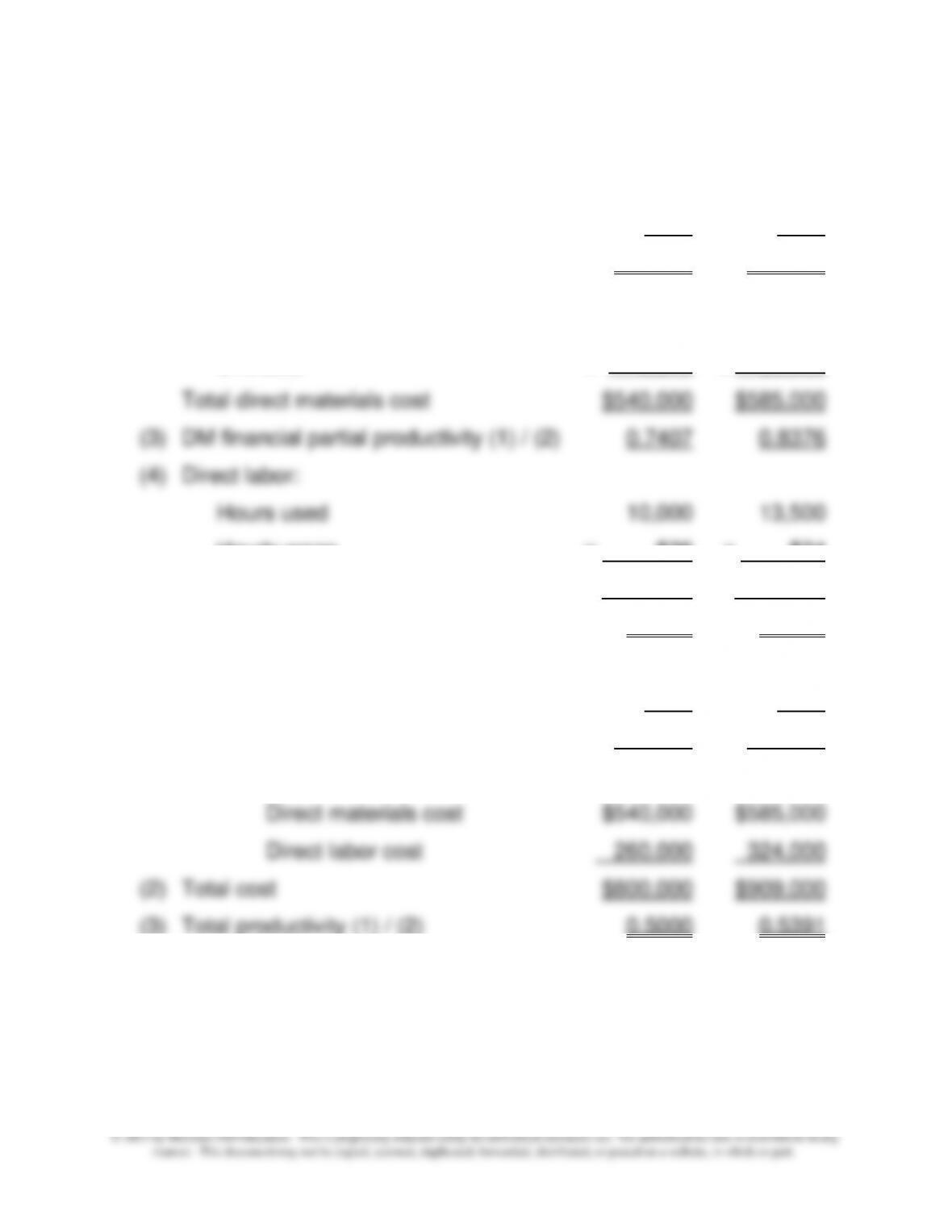

16-32 Financial Partial Productivity and Total Productivity (20 min)

1. Financial partial productivity:

2012 2013

(1) Output 400,000 490,000

(2) Direct materials:

Quantity 160 180

Unit cost x 3,375 x $3,250

Hourly wage x $26 x $24

Total direct labor cost $260,000 $324,000

(5) DL financial partial productivity (1) / (4) 1.5385 1.5123

2. Total productivity:

2012 2013

(1) Output 400,000 490,000

Total cost:

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-12

16-32 (continued -1)

3. The decision was a good one. The direct labor productivity per direct

labor dollar decreased from 1.5385 units of output in 2012 to 1.5123 in

2013. However, direct materials productivity improved from 0.7407

units of output per direct materials dollar in 2012 to 0.8376 in 2013.

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-13

16-33 Operational and Financial Partial Productivity (20 min)

1. Operational Partial Productivity: number of calls handled per

engineer

2012: 100,000 /10 = 10,000

2013: 108,000 / 8 = 13,500

2. Financial Partial Productivity

3. Hiring of engineers with two years’ experience increased financial

partial productivity slightly. Although the firm paid the experienced

engineers higher salaries, on average each of these engineers was

able to answer more calls than newly graduated engineers.

Experienced engineers are likely to provide better services in

4. Among other factors that the firm needs to consider are:

• quality of the service provided

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-14

16-34 Productivity: Which Way to Lean? (15 min)

1. Productivity measures can help a company become more efficient

by providing key measures that the company can track on a

2. The Toyota Production System (TPS) is a system designed to

reduce waste and improve quality in manufacturing. The main

elements of TPS are:

(1) a long term focus on relationships with suppliers, and

for a variety of tasks.

For additional resources on lean manufacturing and lean accounting,

see two Statements on Management Accounting by the Institute of

Management Accountants: Frances A. Kennedy and Brian H.

Maskell, “Accounting for the Lean Enterprise: Major Changes to the

Accounting Paradigm,” and Frances A Kennedy and Brian H.

Maskell, “Lean Enterprise Fundamentals”; at

http://www.imanet.org/resources_and_publications.aspx

Chapter 16 - Operational Performance Measurement: Further Analysis of Productivity and Sales

16-15

16-35 Quality and Productivity (20 min)

This question is intended for class discussion. The objective is to try to

balance the strategic success factors within an automotive company. The

answers are likely to vary. Here are some points to bring out in the

discussion:

• In the longer term, a car’s success in the market is determined by its

acceptance by the customer, not productivity. This means attention

in manufacturing, thus making these funds available for other

purposes.

• As noted in chapter 17, the cost of quality can be quite high, when

warranty costs and rework costs are considered. Thus, the savings

Useful reading on this matter: Dan Slater, “In the Race for Success,

Quality is More Important than Productivity,” Manufacturing & Technology

News (www.manufacturingnews.com/news/editorials/slater.html ). See

also, Matthew Boyle, “Cutting Costs Without Cutting Jobs,” Business

Week, March 9, 2009, p. 55.