Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 1 - Cost Management and Strategy

1-1

Chapter 1

Cost Management and Strategy

Teaching Notes for Cases

1-1. Critical Success Factors

The critical success factors for Kirsten’s business, including the proposed new publishing

business are related to the needs of these customers, which probably includes, now and into the future:

• timeliness of the information in the publishing business

• reliability of the repair and consulting business

• expertise and ability to solve problems which competitors may not be able to solve

• ability to respond quickly, faster than her competitors

• since her business probably grows primarily on the basis of references and recommendations

from satisfied customers, the ability to consistently satisfy her current customers is critical;

she should not try to grow too fast or to move into new areas in which she cannot be

immediately successful

The cost information she will need will be primarily in the management functions of (1) strategic

management and (2) management and operational control. In the strategic management area, she will

need cost information to understand which of her businesses is most profitable, which she can be most

competitive in from a cost perspective, and to provide a basis for analysis of potential new businesses.

Strategic management methods are covered in Parts One, Two and Six of the book. In management and

operational control, she will need cost information to provide a fair and effective basis for identifying the

most inefficient operations, and for rewarding the most effective managers. Operational control is covered

in Part Five and management control is covered in Part Six.

Chapter 1 - Cost Management and Strategy

1-2

1-2. Contemporary Management Techniques

Delight competes in both a low-cost/low-price market (wholesale) and in a less price-sensitive

market where its innovation and product leadership are critical. The benchmarking, continuous

improvement, activity-based costing, and theory of constraints techniques are likely to be used in the low-

cost market. These techniques are used to assist in reducing production costs. In addition, target costing

can be used for those products which have significant development costs, to focus the design effort on

developing a profitable product.

Total quality management is probably used by Delight in both market segments. Quality is

important to both types of customers. Also, life-cycle costing can be used in either market segment, to

give Delight a basis for analyzing the profitability of each of its products over its entire life cycle. This

will be especially important for products which require substantial development costs.

Chapter 1 - Cost Management and Strategy

1-3

1-3. Pricing; Ethics

The staff cost analyst has the responsibility to notify immediate supervisors that the decision to

cancel plans for the new cost system, without appropriately informing the U.S. Government of the

implications for the contract, is unethical. Because of the accountant’s responsibility for confidentiality,

the accountant should not report the matter outside the firm. The only exception to this confidentiality

requirement would be a legal requirement to disclose the matter, as would be the case in a court order.

The accountant should also carefully consider whether the ethical climate in the company is

sufficiently weak that it would be appropriate to leave the company. Is this an isolated incident or one of a

pattern of incidents which reflect a pervasive unethical climate?

Chapter 1 - Cost Management and Strategy

1-4

1-4 Selected Ethics Cases

1. The action of the COO is both unethical and illegal. If the beer was near to (but not past) its

shelf life, potential customers should be advised, but if the beer is past the shelf life, the sale of the beer is

illegal as well as unethical. It is also likely, depending on the degree of care taken by local authorities,

that an inspection of the firm’s records will disclose the illegal act. If Jim is directly involved in the

decision, then he should clearly state to immediate supervisors that the action is illegal and unwise, and

refuse to take part in it. If Jim on the other hand becomes indirectly involved as an observer or becomes

aware of it from others, then he should again state clearly to his immediate supervisors that the action is

improper and unethical. In either case, Jim should not inform anyone outside the firm, because of his

ethical responsibility to maintain the confidentiality of his employer.

2. As in part 1 above, the action of the firm appears to be in conflict with local laws. While the

ethical principles are not as clear in this case, Jim is obliged to comply with local laws and ordinances,

and as such should refuse to become directly involved in the act, and to report the impropriety to his

immediate supervisor.

3. Since disclosure of insider information is in conflict with SEC regulations, Jim should be

careful to say nothing that would provide assistance to his friends, even if it appears they may have

already heard the information from another source. Jim would be subject to SEC penalties, and from an

ethical standpoint, the disclosure would be unfair to the current and potential investors in the firm.

4. The salesman’s action is an unethical attempt to manipulate the financial report of the firm and

to cause his or her sales commission to be received earlier than is appropriate. An evaluation of an action

like this is likely to consider also the materiality of the amount. If the amount is small, then the effect on

the financial report is not material, and Jim might then view the action as improper, but not requiring

disclosure. On the other hand, if Jim finds that the salesperson has been doing this for some time, or if the

amount involved is material, then it would be appropriate to inform the salesperson and the salesperson’s

immediate supervisor.

5. The marketing executive’s action is unethical, in effect, stealing from the company. There is

also a possibility from what the executive has said that there is an outside business which might compete

with the company. This would also be unethical. As in part 4 above, the materiality of the amount and the

possibility of a pattern to the action would have an important effect on Jim’s evaluation of the incident.

Chapter 1 - Cost Management and Strategy

1-5

1-5 Strategy; Branding Beef

1. The meatpacking industry overall is probably best described as a commodity business. The product is

hard to differentiate other than by USDA grade or preparation (percent lean,…). On the other hand,

some meatpackers and supermarkets are able to differentiate their product through careful selection of the

meat, and focus on freshness and customer service. Husker Beef Company (huskerbeefco.com) and

Kansas City Steak Company (kcsteak.com) are two examples of firms in the industry that differentiate.

2. The meatpackers plan to address some of the issues with preparing meat meals that are likely to be the

cause of the decline in beef purchases over the last few decades. The new focus is on convenience for

the customer by reducing food preparation time, and by making the food preparation process simpler so

that the product is can be served with the best possible flavor and nutritional benefit.

Two of the largest meatpackers, Hormel and IBP Inc. are developing new products that improve

convenience for the customer. For example, one new Hormel product, called “Always Tender” is

prepared with a patented solution of salt, vinegar, and sugar to keep the meat moist, even if it is

overcooked.

Also, the firms are putting more effort into marketing their product, with the goal of developing a

brand image and brand loyalty. For example, IBP Inc is using the Wilson brand, and will advertise it as

the centerpiece of family time, not just a meal. Together, these efforts change the nature of the

competition from a commodity-based, cost leadership type to a differentiated type of competition based

on customer convenience.

1-6

1-6 Top 10 Companies

This question is intended for class discussion in which a number of different views are likely to be

expressed. I would make the observation that many of the top 10 firms in sales are cost leaders, either

low cost retailers (Wal-Mart) or commodity producers (the energy companies). One might also observe

that the global demand for oil products and the price increases in these products in recent years have

affected the energy companies significantly, and is a reason why they are in the top 10. I would also

point out that many cost leadership firms are very large because they succeed on very low margins, and

therefore attain a very large size to sustain the low margins and still show strong earnings growth. Note

for example that Wal-Mart is top in sales and 6th in earnings. Large manufacturers such as GM, Ford and

GE are not easily identified as cost leaders or differentiators, but are established companies that have

attained large size.

The list of most profitable firms includes both costs leaders and differentiators. Berkshire Hathaway and

J.P Morgan Chase (financial firms), Apple, and IBM can be identified with differentiation, as innovation

and customer service are key elements of their success. Alternatively, ExxonMobil and Chevron deals

with a global commodity, and Microsoft and AT&Tare not easily identified as cost leaders or

differentiators.

Source: Fortune.com

An interesting note is that the 2001 list for Largest Revenue has 8 of the same firms from the 2008 list;

also 8 of the Top Firms in profits are on both the 2008 and 2011 lists.

Chapter 1 - Cost Management and Strategy

1-7

Teaching Strategies for Articles

1-1 “Are You a Business Partner?”

This article is based on interviews of 100 accountants who have made the transition to business partner.

For firms such as McDonalds, Trane, and Boeing, they explain the transition from traditional accountant

to accountant as business partner.

Discussion Questions

1. What are the key findings of the recent research of 100 accountants, now business partners?

The article begins by defining a business partner as one who works in teams with members of

other disciplines to improve business processes and work for the overall success of the firm or

become part of the decision making team.

In contrast, the accountant as business partner uses a broad knowledge of the firm’s strategy and

operations and competitive position to work with managers in developing the information needed to help

the firm be successful, and in participating with these managers in the decision making process.

2. What are the implications of these findings for the education and training of management accountants?

The accountant as business partner needs an entirely different skill set from that of the traditional

Chapter 1 - Cost Management and Strategy

1-8

1-2 Creating an Ethical Culture

This article takes a look at the financial fraud at WorldCom and other companies in recent years, and

examines the role of controls and the ethical culture in the frauds that occurred in these companies. In

considers the following questions. How does the ethical culture effect the risk of fraud? How does a

company develop an ethical culture?

Discussion Questions:

1. According to the article, did World Com lack internal controls to detect fraud? Why was the fraud not

detected earlier, or prevented all together?

The article suggests that internal controls were adequately in place at World Com, but the fraud

company supported the unethical environment there.

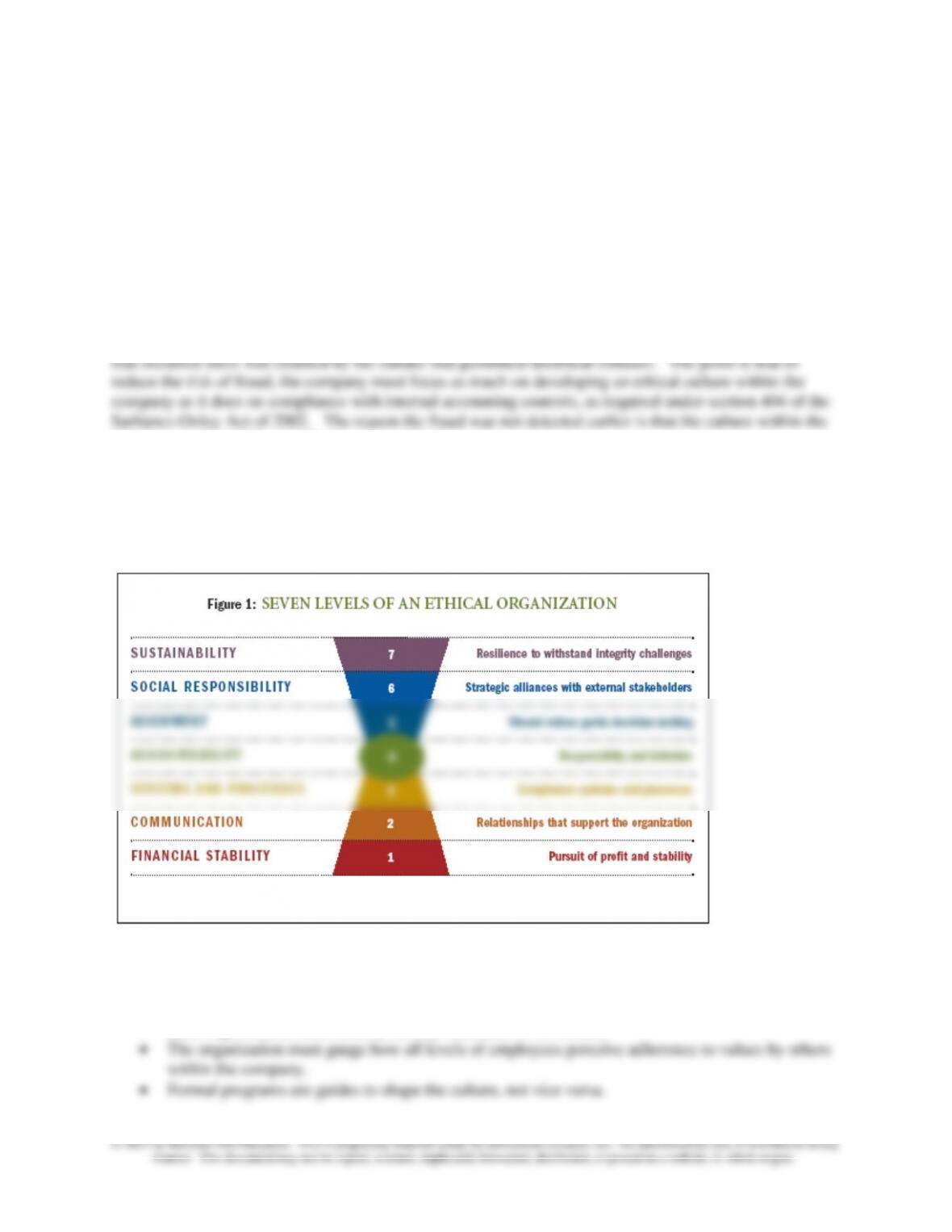

2. According to the Culture Risk Assessment model, what are the levels of values of an organization and

what are the objectives of each?

The levels and objectives of each are identified in Figure 1 in the article:

3. What are some of the ways a company can help to develop an ethical culture?

• The criteria for success of an ethics program must be outcomes based.

• Each organization must identify the key indicators of its culture.

Chapter 1 - Cost Management and Strategy

1-9

1-3 POGS at the Park, POGS at home: C-ing Business Expansion Opportunities

This article explains the competitive environment for a minor league baseball team. An innovative

manager of the team uses strategic cost management concepts for achieving greater profitability.

Discussion Questions

1. Explain whether Greg uses a cost leadership or a differentiation strategy, and why. How does his plan

for the POG oven initiative fit with this strategy?

The Pikesville Lightning team is best described as a differentiator. The special elements Greg uses to

promote the team, as illustrated in Table 1, are a good example of how the team differentiates itself not

So during the off-season, the fans can enjoy a POG and look forward to the start of the next season.

2. Use the C-Framework in Figure 1 to outline your advice to Greg for improving the strategic financial

management function. Be sure to discuss how your advice will assist the organization in achieving Greg’s

goals.

The CFO Framework in Figure 1 is a useful summary of the many ways in which the accounting function,

as represented here by the CFO (Chief Financial Officer), supports the success of the firm. The CFO

expertise and the knowledge of the team’s business and competitive environment to make the decisions

and introduce the initiatives that will help the team succeed.

Chapter 1 - Cost Management and Strategy

1-10

1-4 Leading with Your Soul

This article focuses on ethical leadership. Today’s business environment is not often conducive to ethical

practices. The author points out that everyday ethics do not differ from business ethics, although the

hindrances to ethical practices in the business world are many. An in-depth examination of the

Comprehensive Ethical Leadership ModelTM explains the six ethical leadership traits. These traits are

given in the article and then a discussion of applying the traits follows.

Discussion Questions:

1. What are some of the main reasons, according to the article, that professionals struggle with ethics in

the professional world today?

2. In looking at the example of a CFO who overworks his or her employees due to financial and

performance pressures, what are the main deterrents for this CFO to act ethically?

The hindrances to ethical actions can be summarized as:

1. Professional and social pressures,

5. Conflicting priorities.

3. How do the four-dimensions of a person contribute to ethical behavior?

“The fundamental reality is human beings are not things needing to be motivated and controlled; they

are four-dimensional—body, mind, heart, and spirit.” Stephen Covey (renowned author of time

management books and the book on “Seven Habits”), writing in the Summer 2006 issue of Leader to

own voice and who, regardless of formal position, inspire others to find theirs.”

The four dimensions: body, heart, mind, and spirit

4. What are the six ethical leadership traits?

1. Purpose driven

2. Courage of conviction

Chapter 1 - Cost Management and Strategy

1-11

1-5 Seven Habits

This article points out that the role of CFOs today is multi-faceted and not as specialized as it used to be.

CFOs play an especially important role in forming the strategies of companies. This excerpt walks the

reader through seven critical steps: setting clear expectations for each business line, using synergies

across portfolios, the tradeoff between cost-savings and customer loyalty, what to do in downturn

business cycle and honing in on key growth opportunities.

Discussion Questions:

1. Describe how CFOs today are different from CFOs in the past.

In this charged environment, many CFOs have had to evolve from specialists in accounting to

profits. Traditional CFOs were also gatekeepers, ensuring that company initiatives didn’t go forward

unless they promised to generate acceptable rates of return.

2. What does it mean to grow a business organically and how does that contribute to managing to the

portfolio?

In addition to managing diverse business lines, another dimension of managing to the portfolio involves

acquisitions.

3. What are the seven habits of strategic CEOs?

1. Take a seat at the strategy table

2. Define and manage return expectations

Chapter 1 - Cost Management and Strategy

1-12

1-6 Test Your Ethical Judgment

This reading provides you with the opportunity to use scenarios from the WorldCom accounting

standards in 2001 to test your own response to ethical issues. It also provides recommended solutions to

each instance presented.

Discussion Questions:

1 Recommended solutions for 14 cases:

All 14 scenarios are taken directly from WorldCom activities occurring during 2001.While the WorldCom scandal

has many more facets to it than can be presented in a few short scenarios, these scenarios are indicative of both the

work environment at WorldCom and the types of accounting fraud that occurred.

While 2001 is quickly becoming a distant memory, we must never forget the lessons learned. Fraud at WorldCom—

along with Enron and others—brought our stock market prices down, tarnished the reputations of all accountants,

felled a global accounting firm that was once known as the “gold standard” of accounting firms, revealed gaping

flaws in U.S. Generally Accepted Accounting Principles (GAAP), and eventually brought about the rise in

International Financial Reporting Standards (IFRS). In short, it changed our world.

The information in the scenarios and in some of the suggested solutions comes from published information listed in

the References sidebar. Each answer below is keyed to the corresponding reference number so you can look up

further information if you want. The references are to the reference list at the end of the article.

ANSWER to 1: C. A certain amount of stock market

pressure is to be expected, but the additional pressure

ANSWER to 2: C. Employees shouldn’t be paid significantly more than they are worth in the marketplace for a

variety of reasons. First, overpaying employees is an inefficient use of corporate funds. Second, and most important,

Chapter 1 - Cost Management and Strategy

1-13

ANSWER to 3: D. This scenario goes well beyond an issue of confidentiality. Employees need full access to the

information necessary to make competent decisions related to their positions. Denial of proper access appears to

indicate that something is being hidden. Ref. 1

be left without the control check which the Audit Committee is expected to provide.” (The quote comes from Ref. 4,

pp. 55-56.) Without proper oversight, objectivity may become compromised.

Ref. 2

ANSWER to 6: D. Such an extended delay of scheduled audits without the Board of Directors’ explicit approval

Supporting documentation ensures objectivity; fairness requires

the financials to reflect actual operations and not just

budgeted targets. Ref. 1

ANSWER to 9: E. Periodic rent provides current period benefits but no future economic benefits owned or

controlled by the company despite the fact that its payment may be fixed for an extended future period of time.

sentenced to 25 years in jail. Ref. 1

ANSWER to 13: E. It is clearly fraudulent to book a

gain contingency. Ref. 1

Chapter 1 - Cost Management and Strategy

1-14

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

ANSWER to 14: D. While simple filing errors occur

even in well-run organizations, a filing room in complete disarray indicates a serious problem with record keeping.

When this situation continues, the accounting records become virtually unauditable, and the integrity of the

accounting system is in question.

2 When do accountants usually face ethical dilemmas and what is the best way to deal with these

issues?

As accountants, we typically don’t face ethical dilemmas on a daily basis. Instead, the dilemmas tend

3 What effect did the WorldCom incident in 2001 have on our world?

Fraud at WorldCom—along with Enron and others—brought our stock market prices down, tarnished

the reputations of all accountants, felled a global accounting firm that was once known as the “gold