Chapter 12 – Strategy and the Analysis of Capital Investments

12–31

12–39 (Continued)

5. NPV Calculations under different assumptions regarding the discount rate

(required rate of return) and annual after-tax net cash inflows. Assume a ten-year

life and an initial investment outlay of $6,000.

15%

5.019

($3,491)

($981)

$4,038

Note to instructor: While this is not required in the present exercise, the above

two-variable “data table” could be generated by using the “Data Table” option under

“What–If Analysis” in Excel 2010. See Problem 12–62 and footnote #17 in Chapter

12.

Discount

PV Annuity

Annual Net After-Tax Cash Flow

Rate

Factor

$500

$1,000

$2,000

10%

6.145

($2,928)

$145

$6,290

20%

4.192

($3,904)

($1,808)

$2,384

Chapter 12 – Strategy and the Analysis of Capital Investments

12–32

12–40 NPV, Sensitivity Analysis (30 minutes)

1. NPV of proposed investment,15-year project life:

PV of after-tax cash inflows = $600,000 × 6.142 = $3,685,200

Initial investment outlay = 3,500,000

NPV of proposed investment, 12-year project life:

PV of after-tax cash inflows = $600,000 × 5.660 = $3,396,000

Initial investment outlay = 3,500,000

Since NPV = ($104,000), the investment should not be undertaken.

2. We are given annual after-tax cash inflows of $600,000 and an initial

investment outlay of $3,500,000. To generate an IRR of exactly 14.00%, the

following must hold:

PV of Future Cash Inflows = Initial Investment Outlay

$600,000 × An,14% = $3,500,000

is approximately 13 years.

Though not discussed in the text, we can solve exactly for the number of years,

n, once we know the formula to calculate the PV of an ordinary annuity (i.e., the

formula for the factors included in Chapter 12, Appendix C, Table 2). This

formula is:

Annuity Factor = [(1 ÷ r) × [1 – [1 ÷ rn]], where n = the number of periods and

r = the discount rate (defined in terms of n, e.g., in years)

In the present case, the annuity factor = 5.83333 and r = 0.14. Thus, we have

Chapter 12 – Strategy and the Analysis of Capital Investments

12–33

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

-0.1833338 = – 1 ÷ (1.14)n

12–40 (Continued)

(3) Multiply both sides by –1:

0.1833338 = 1 ÷ (1.14)n

(4) By rule of exponents (i.e., 1 ÷ xn = x-n), the right-hand side of the above

can be expressed as:

1 ÷ (1.14)n= 1.14–n

(5) This gives us:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–34

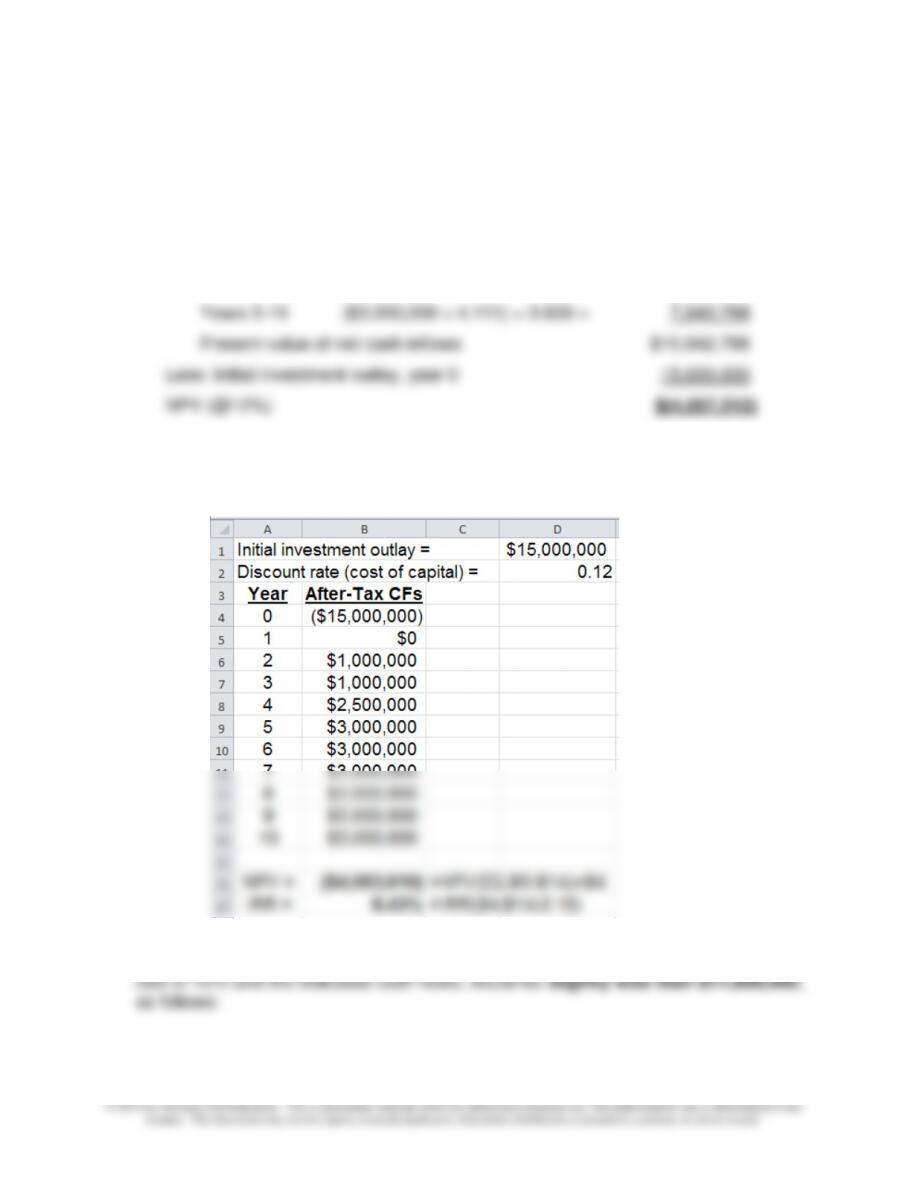

12–41 Uneven Cash Flows, NPV, Sensitivity Analysis (30-40 minutes)

1. Present value of net cash inflows:

Year 1 -0-

Year 2 $1,000,000 × 0.797 = $ 797,000

Year 3 $1,000,000 × 0.712 = 712,000

Year 4 $2,500,000 × 0.636 = 1,590,000

Alternatively, the built-in functions in Excel can be used to estimate the NPV and

the IRR of this project, as follows (Note: the slight difference in answers is due to

rounding—that is, the PV factors in the Tables have been rounded):

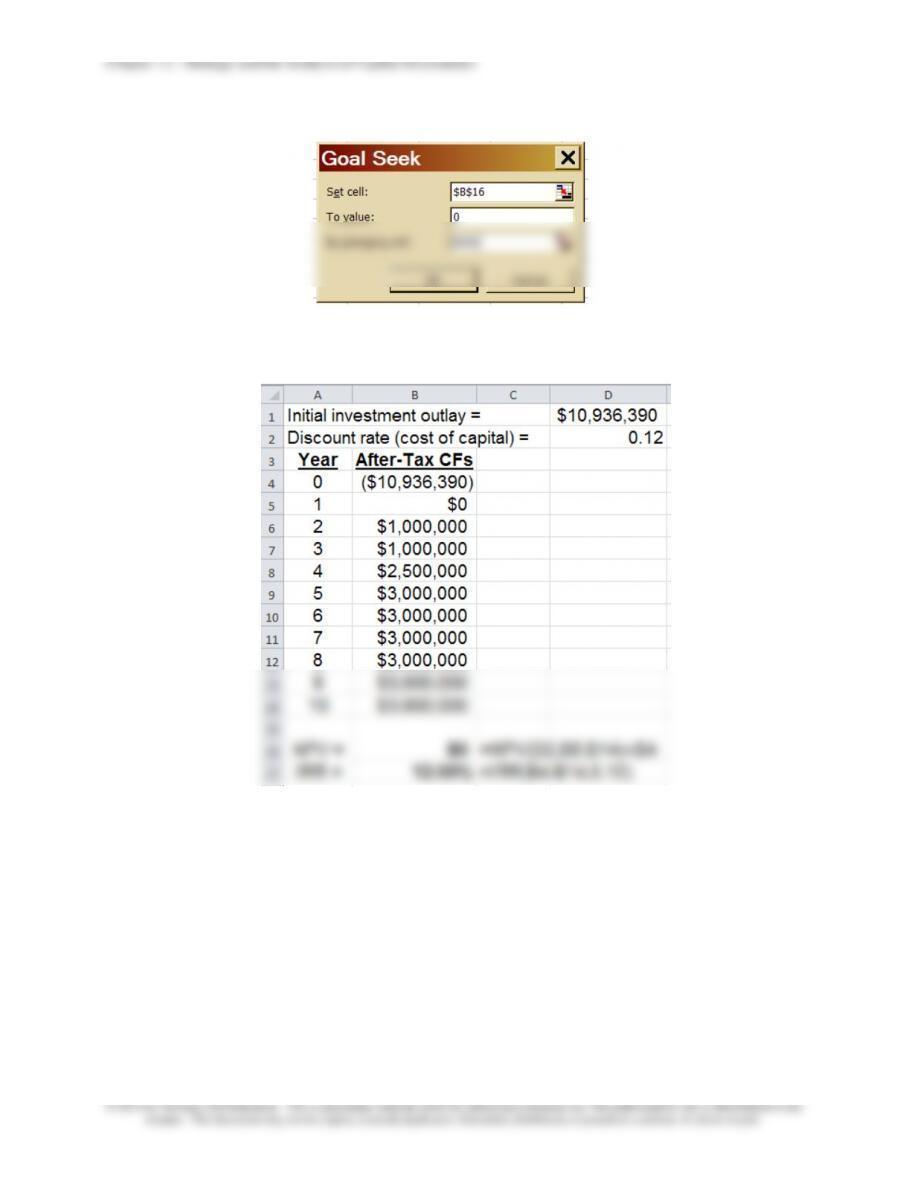

2. The maximum purchase price the seller would be willing to offer, given a discount

12–35

12–41 (Continued)

After executing Goal Seek, the following result is obtained for cell D1:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–36

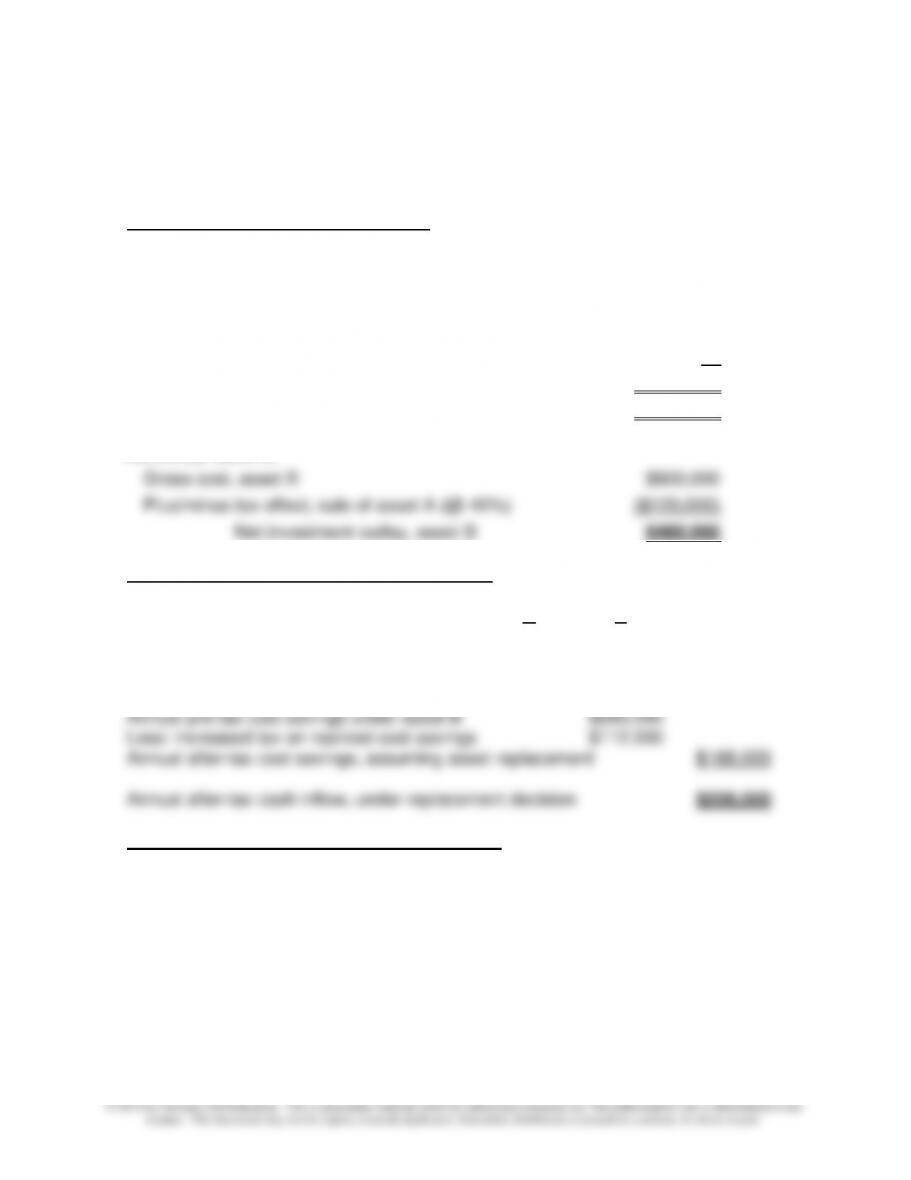

12–42 Asset-Replacement Decision; NPV Analysis (45 Minutes)

1. Relevant (i.e., differential) cash flows (after tax) at:

Project Initiation (i.e., time period 0)

If asset B is purchased, the net investment outlay would be $480,000 (i.e., $600,000

− $120,000).

NBV of existing asset, A

$300,000

Less: Current disposal value of asset A

$0

Gain (Loss) on disposal

($300,000)

Tax effect of sale of existing asset (@ 40%)

($120,000)

Net outlay, asset B:

Gross cost, asset B

$600,000

Plus/minus tax effect, sale of asset A (@ 40%)

($120,000)

Net investment outlay, asset B

$480,000

Project Operation (i.e., years 1-3, inclusive)

A B

Annual depreciation deduction $100,000 $200,000

Annual tax benefit/savings (@40%) $40,000 $80,000

Differential annual tax savings, assuming asset replacement $40,000

Project Termination/Disposal (end of year 3)

N/R—the estimated disposal value of each asset at the end of year 3 is the same, $0,

and therefore not relevant to this asset-replacement decision.

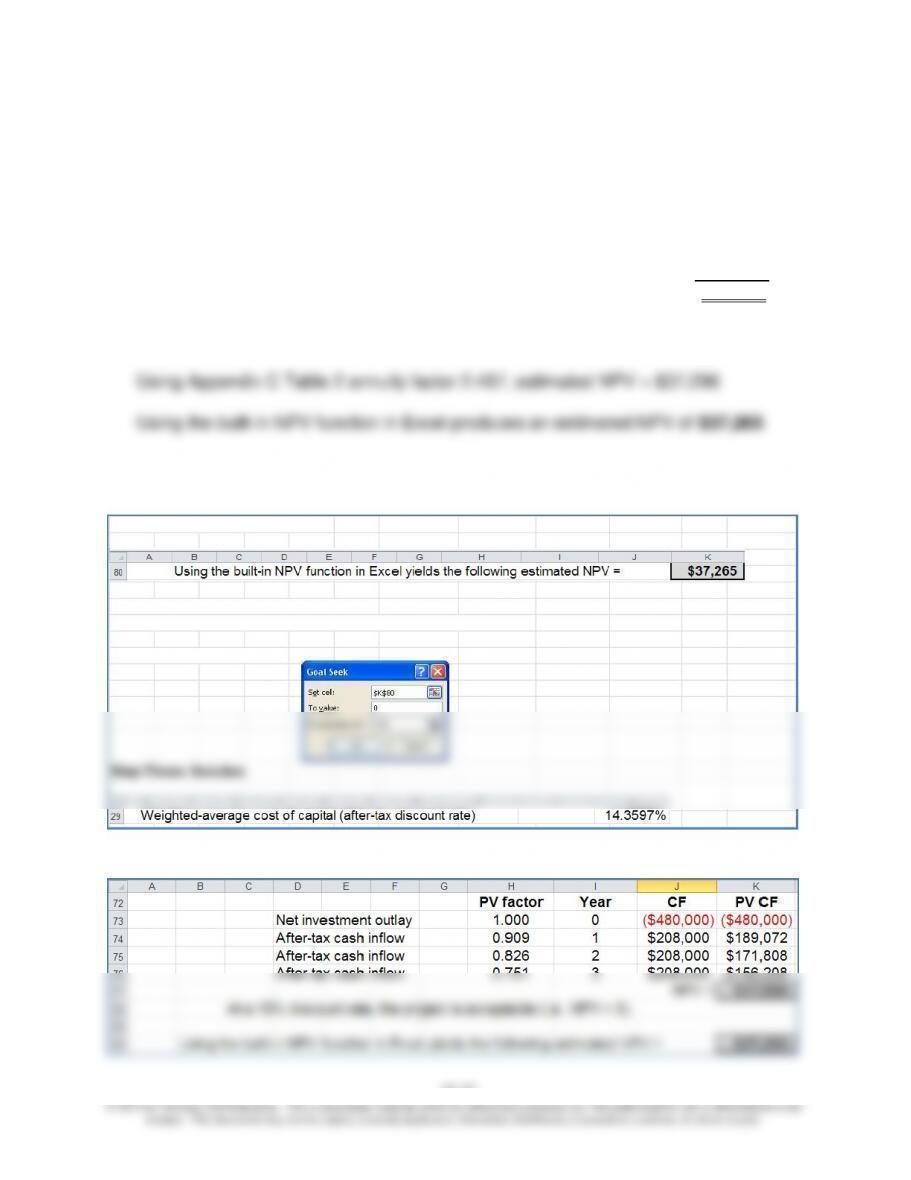

2. Estimated NPV of decision to replace asset A:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–37

12-42 (Continued-1)

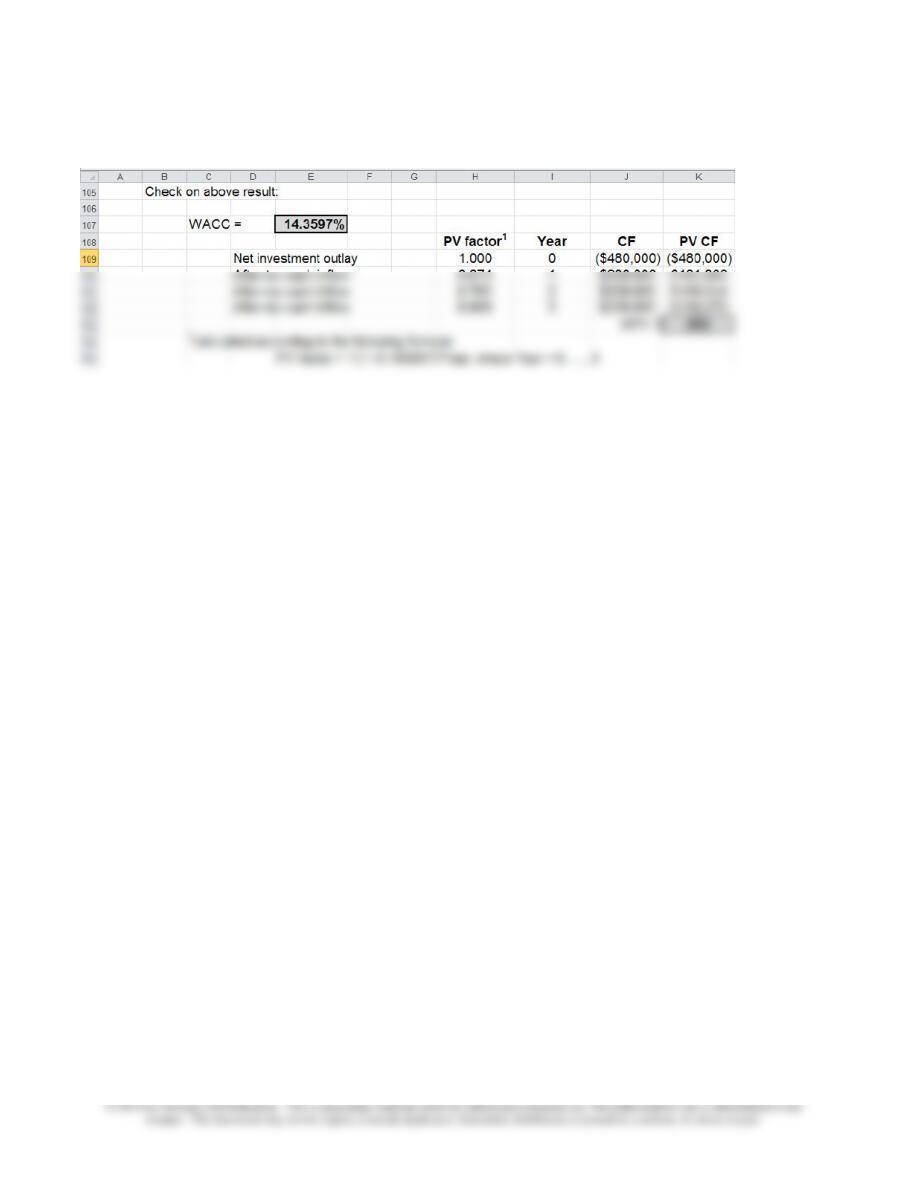

PV factor Year CF PV CF

Net investment outlay

1.000

0

($480,000)

($480,000)

After-tax cash inflow

0.909

1

$208,000

$189,072

After-tax cash inflow

0.826

2

$208,000

$171,808

After-tax cash inflow

0.751

3

$208,000

$156,208

NPV =$37,088

At a 10% discount rate, the project is acceptable (i.e., estimated NPV > 0).

3. The weighted-average cost of capital (WACC) that would make the company

indifferent between keeping or replacing asset A is 14.3597%, as follows:

Step One: Set-up the Problem

Note: the WACC is contained in cell J29

Note: cell K80 contains the formula “=J73+NPV(J29,J74:J76)”

Step Two:Run Goal Seek

Step Three: Solution

The following excerpt is helpful in understanding the above three steps:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–38

12-42 (Continued-2)

12–39

12–43 Cash Flow Analysis; NPV; Spreadsheet Analysis (45 minutes)

1.

PV CASH FLOWS IN YEAR (in ‘000) )

Item & Description Factor PV 0 1 2 3 4 5

a. After-tax rent foregone

($5,000/mo. × 12 × 0.6) N/A ($128,931)1 (36) (36) (36) (36) (36)

b. All are irrelevant

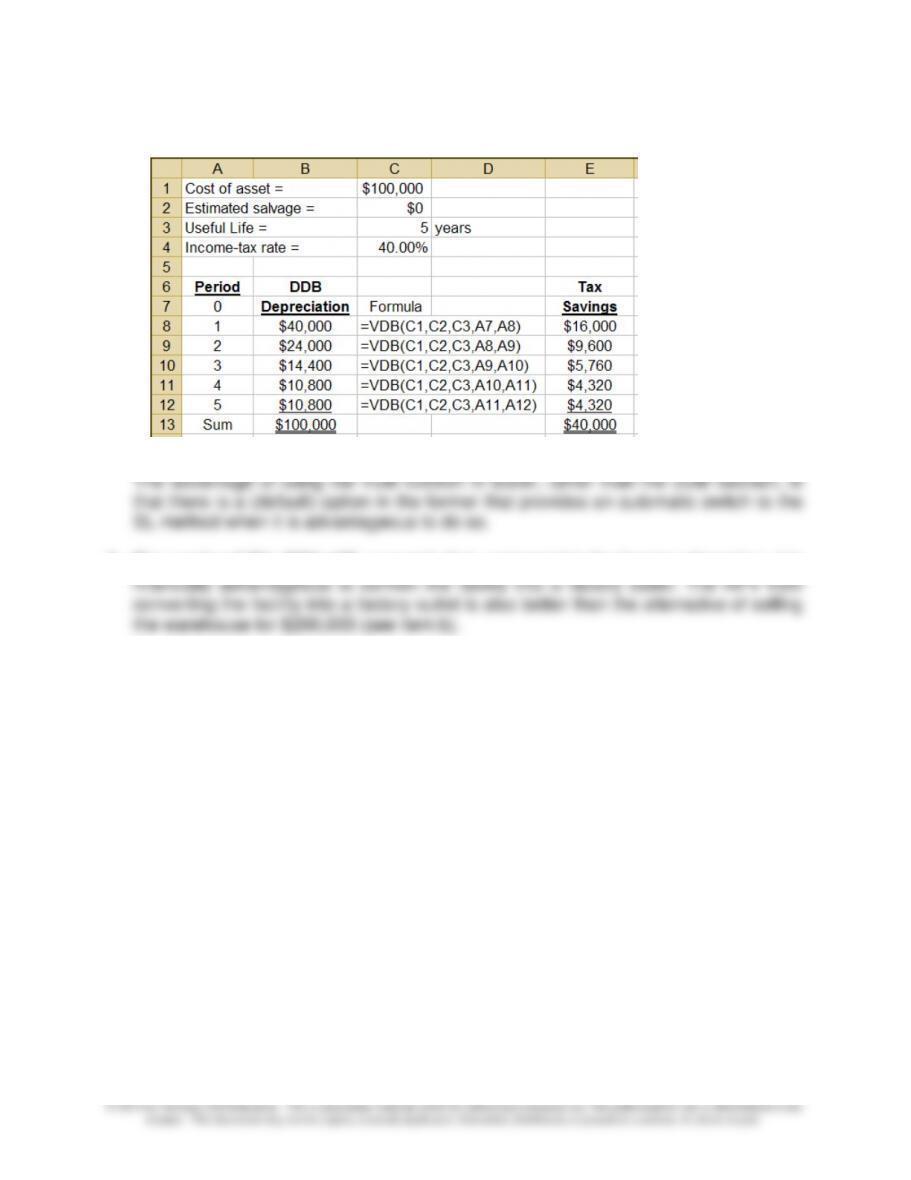

c. Remodeling cost ($100,000) (100)

Depreciation tax savings2 0.877193 $14,035.09 16

0.7694675 $7,386.89 9.6

0.6749715 $3,887.84 5.76

0.5920803 $2,557.79 4.32

0.5193687 $2,243.67 4.32

$30,111 (rounded down)

d. Investment in net working capital ($600,000) (600)

Recovery 0.5193687 $311,621 600

e. Irrelevant

f. Sales ($900 × 0.6) 3.433081 $1,853,864 540 540 540 540 540

Operating expenses

1Use the PV function in Excel to determine the PV of a stream of 60 monthly cash receipts ($3,000 per month, after–

tax). The appropriate formula is: =PV(0.14/12,60,3000).

2Depreciation deductions found using the VDB function in Excel, as follows:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–40

12–43 (Continued)

2. The positive NPV, $261,160, suggests that, compared to the leasing alternative, it is

12–41

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

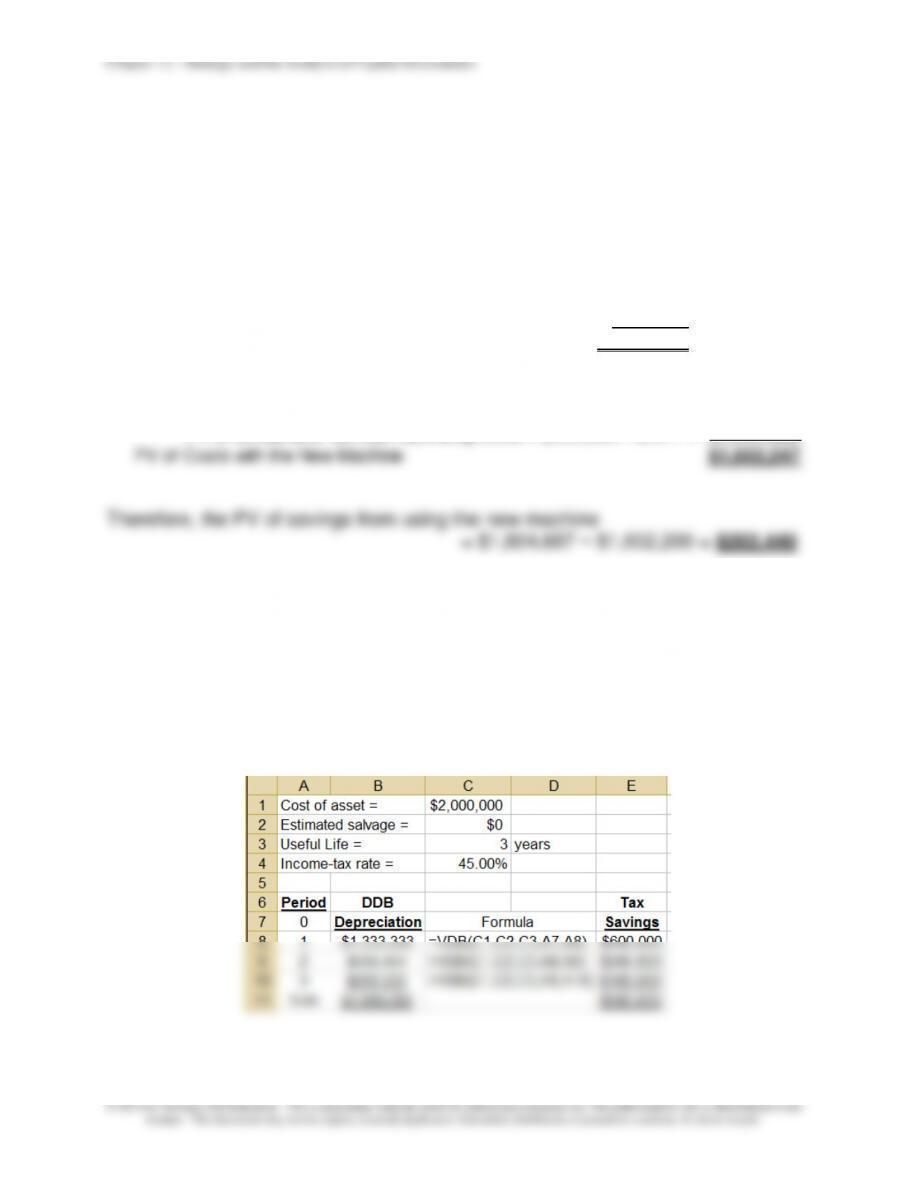

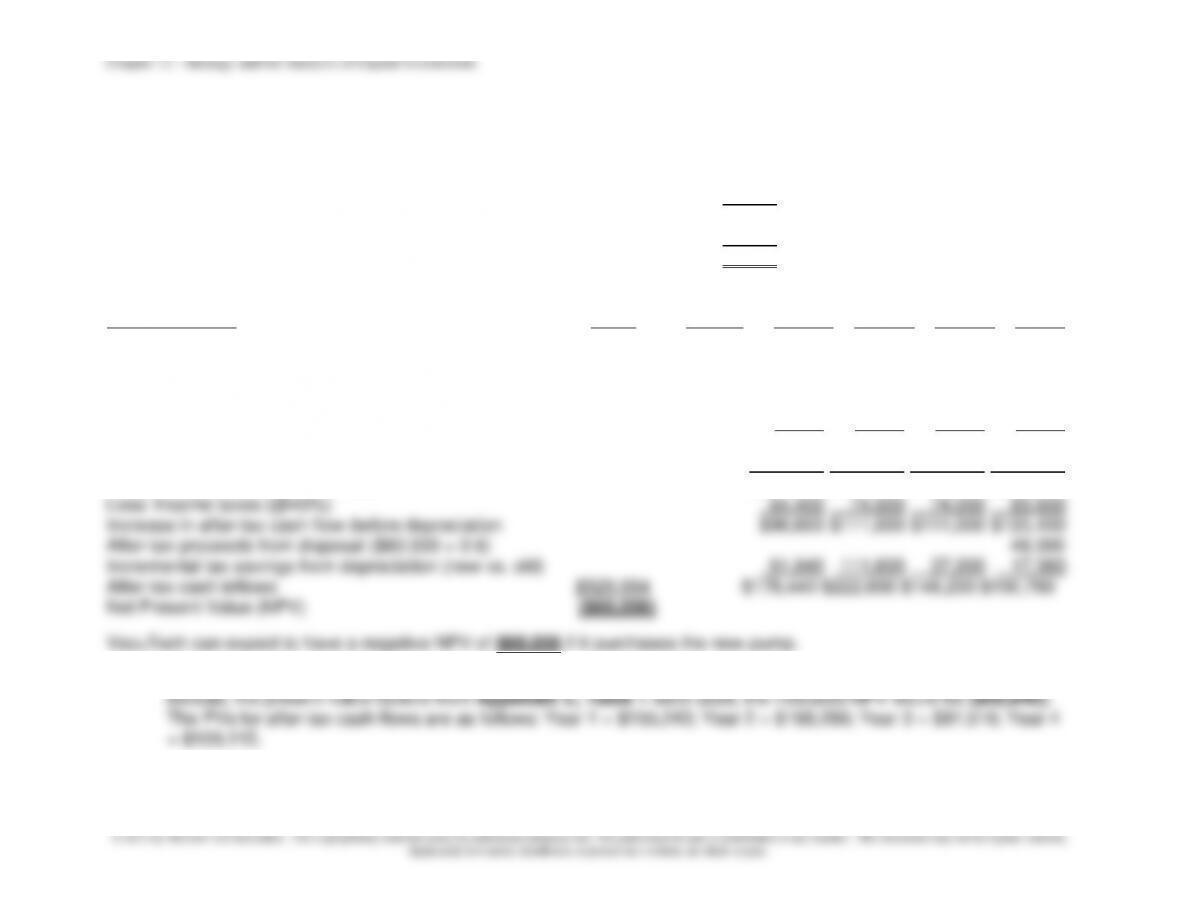

12–44 Machine Replacement with Tax Considerations; Spreadsheet (45 minutes)

and 2 in the text. The solution below is based on the use of PV and NPV functions in Excel.)

Present values of Costs with the Original Equipment:

PV of tax savings from depreciation deductions:

($2,500,000 ÷ 4) × 0.45 × 2.577 = ($724,809) (rounded up)

PV of after-tax cash operating costs:

[$1,800,000 × (1 − 0.45)] × 2.577 = $2,551,326

PV of salvage value, after tax:

[$50,000 × (1 − 0.45)] × 0.794 = ($21,830)

$1,804,687

(NOTE: The present value factors listed above are taken from text Tables 1 and

2 and, as such, have been rounded to three decimal places. However, the actual

calculations above are done using the NPV and PV built-in functions in Excel,

and as such are not rounded.)

PV of Costs with the New Machine

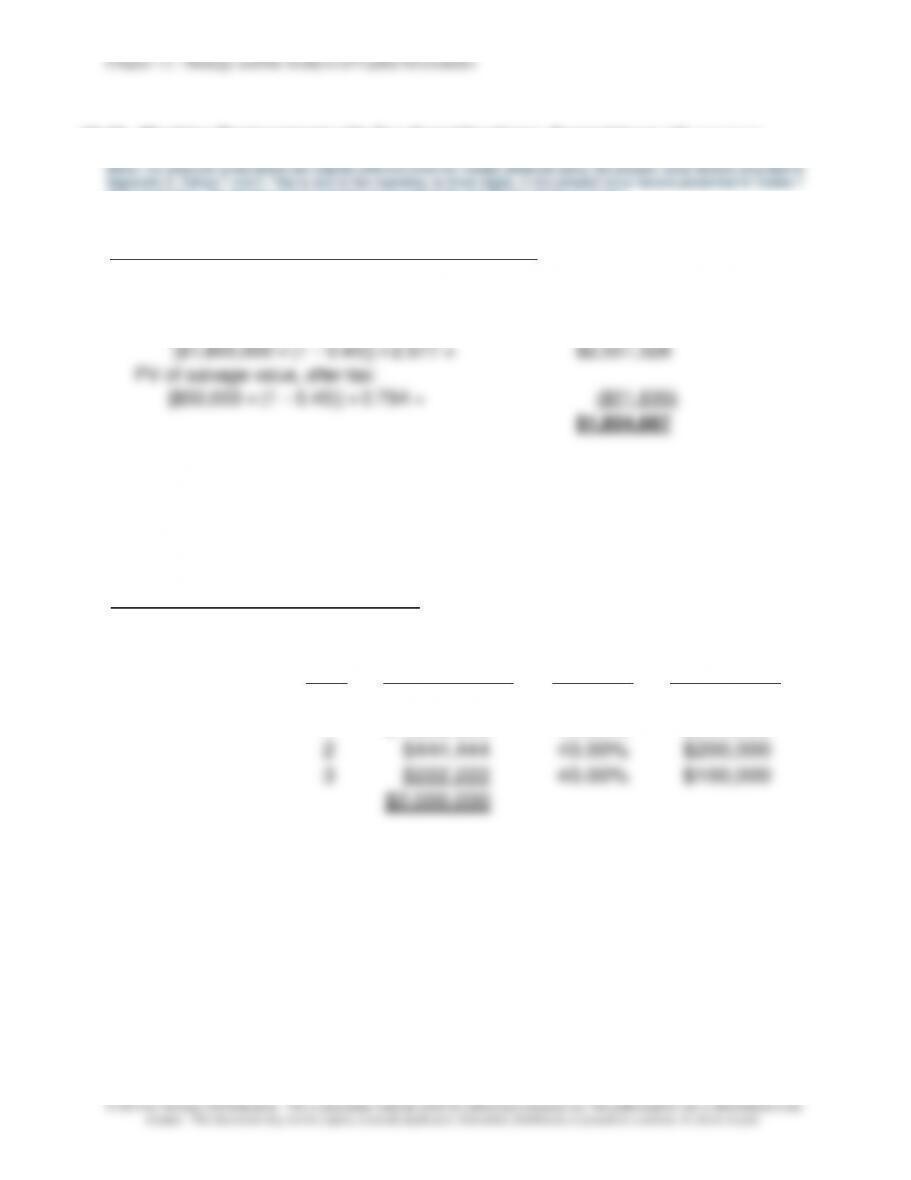

Present value of tax savings from depreciation deduction:

Year Deprec Expse Tax Rate Tax Savings

0

1 $1,333,333 45.00% $600,000

2 $444,444 45.00% $200,000

3 $222,222 45.00% $100,000

$2,000,000

12–42

12-44 (Continued)

Initial outlay cost, new machine = $2,000,000

PV of tax savings from DDB depreciation (see above) = ($806,407)

Cash proceeds from sale of the old machine = ($300,000)

Tax savings related to loss on disposal of old machine:

($1,875,000 − $300,000) × 0.45 = ($708,750)

Book value of old asset at time of sale:

Original cost of asset (1 year ago) = $2,500,000

Less: accumulated depreciation (1 year) = $625,000

Book value, end of one year = $1,875,000

PV of cash operating costs:

Annual after-tax cash operating costs =

= [$1,000,000 x (1 – 0.45)] = $550,000

PV of annual after-tax cash operating costs = $550,000 × 2.577 =

$1,417,403

PV of Costs with the New Machine $1,602,247

Therefore, the PV of savings from using the new machine

= $1,804,687 − $1,602,200 = $202,440

The total cost of the new machine, including the purchase cost and the cash

operating cost in each of the three years is, in PV terms, $202,440 below the

total cost of continuing with the original equipment. Therefore, from a purely

financial standpoint, the purchase of the new machine is a good investment.

Depreciation Calculations for Replacement Machine: Using VDB Function in

Excel

12–43

12–45 Equipment Replacement; MACRS (50 minutes)

1. Per-unit pre-tax cash flow per unit, additional unit sales:

Sales price per unit $3,500

Current variable (cash) manufacturing cost per unit − 2,450

Current cash contribution margin per unit $1,050

Cash-based cost savings per unit with the new machine + 150

Pre-tax cash flow per unit for the additional units $1,200

After-Tax Cash Flow Analysis Present Discount

Item Description Value Factor1 2016 2017 2018 2019

Purchase cost of the new asset ($608,000)

Capitalized installation cost of the new asset ($12,000)

After-tax proceeds from disposing old ($50,000 × (1 − t)) $30,000

Pre-tax cash flow per unit, sale of add’l units (above) $1,200 $1,200 $1,200 $1,200

Additional units (given) 30 50 50 70

Pre-tax cash flow from additional units $ 36,000 $ 60,000 $ 60,000 $ 84,000

Efficiency savings, pretax 125,000 125,000 125,000 125,000

Total increase in pre-tax cash flow $161,000 $185,000 $185,000 $209,000

1Note: The above PV of after-tax cash inflows ($529,994) was determined using the NPV built-in function in Excel. If,

Chapter 12 – Strategy and the Analysis of Capital Investments

12–44

12–45 (Continued)

2. Other factors the firm needs to consider include:

▪ Maintenance costs of the machines

▪ Reliability of the machines

Chapter 12 – Strategy and the Analysis of Capital Investments

12–45

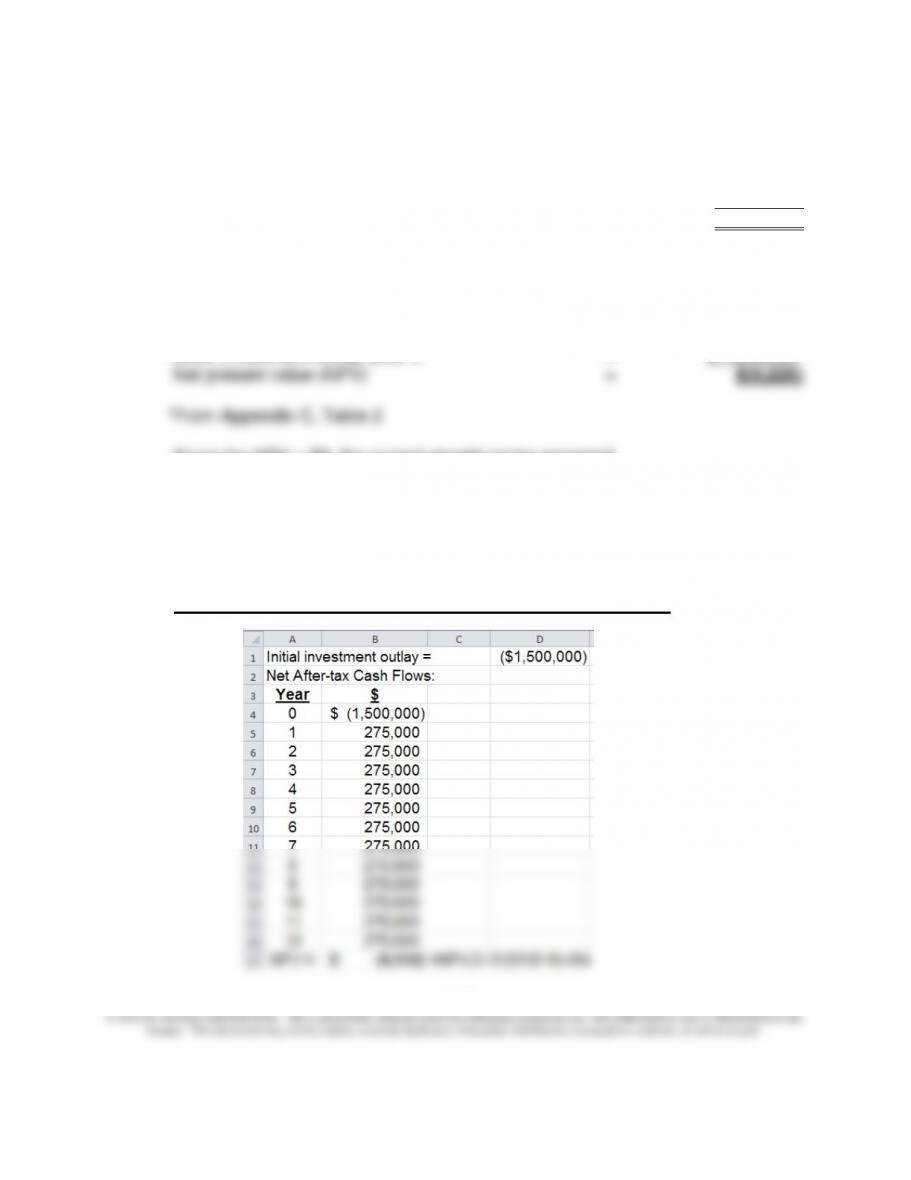

12–46 Risk and NPV; Sensitivity Analysis (40-45 minutes)

1. PV of future cash inflows: 12 years @ 12% = $275,000 × 6.194* = $1,703,350

Less: Initial investment outlay, year 0 = $1,500,000

Net present value (NPV) = $ 203,350

*From Appendix C, Table 2

Since the NPV > $0, the project should be accepted.

2. PV of future cash inflows @ 15% = $275,000 × 5.421* = $1,490,775

Less: Investment outlay, year 0 = $1,500,000

Since the NPV < $0, the project should not be accepted.

3. The “break–even” initial investment outlay is the amount that would produce a

NPV = $0, given the annual after-tax flows of $275,000 and a discount rate of

15.00%. We can use Excel to solve, in two steps, for this “break–even” amount

(viz., $1,490,670), as follows:

Step 1: Estimate the Project’s NPV (compare with 2 above)