Chapter 10 – Strategy and the Master Budget

10–46

10–47 (Continued-5)

7. Budgeted selling and administrative expenses:

Spring Manufacturing Company

Selling and Administrative Expense Budget

2013

Selling Expenses:

Advertising $60,000

Sales salaries 200,000

Travel and entertainment 60,000

Depreciation 5,000 $325,000

Administrative expenses:

Offices salaries $60,000

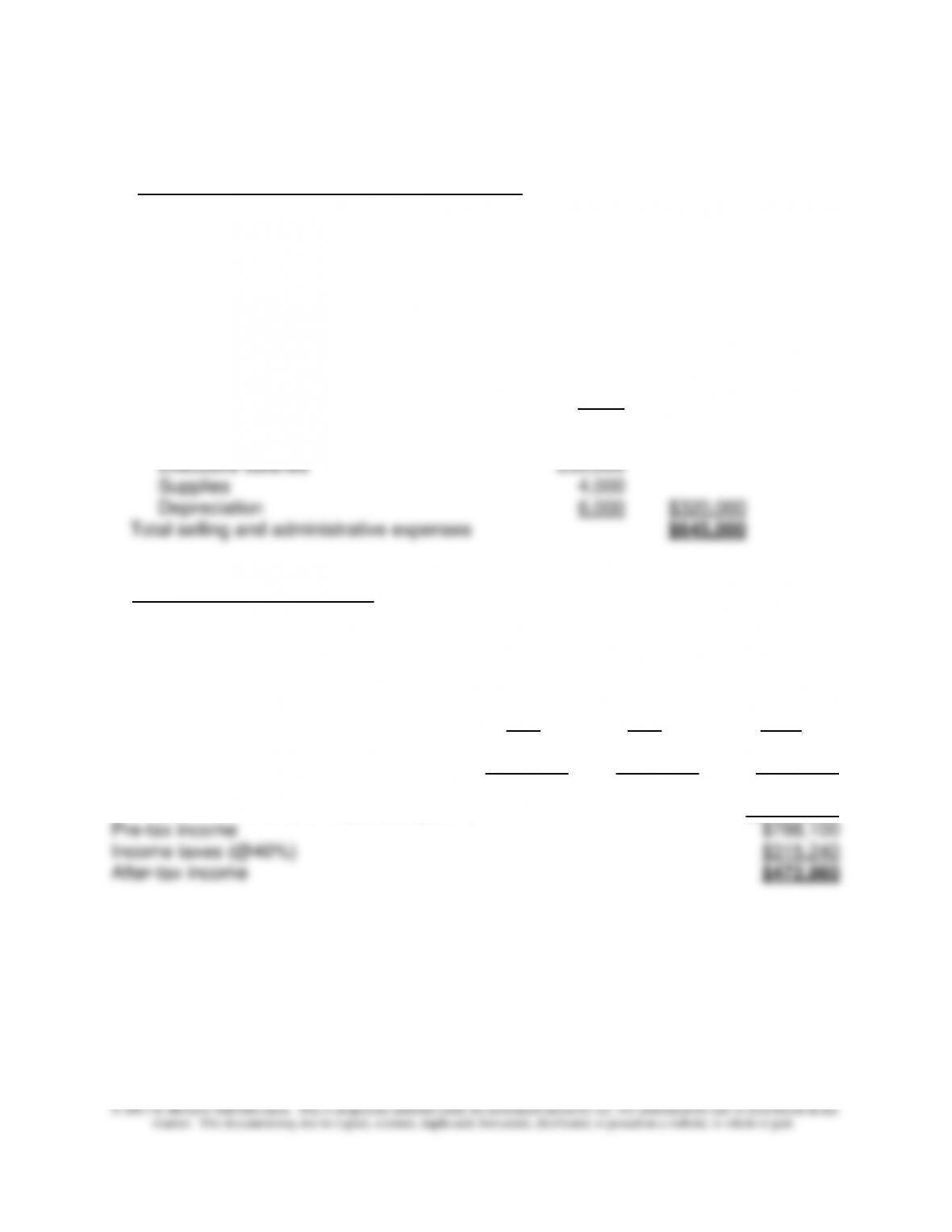

8. Budgeted Income Statement:

Spring Manufacturing Company

Budget Income Statement

For the Year 2013

C12 D57 Total

Sales (part 1) $1,800,000 $1,980,000 $3,780,000

Cost of goods sold (part 6) 1,125,600 1,221,300 2,346,900

Gross profit $674,400 $758,700 $1,433,100

Selling and administrative expenses (part 7) $645,000

Chapter 10 – Strategy and the Master Budget

10–47

10–47 (Continued-6)

Note to Instructor: An Excel spreadsheet solution file is embedded in this document.

You can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet icon below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode.

Pr 10-47.xlsx

Chapter 10 – Strategy and the Master Budget

10–48

10-48 Spring Manufacturing Company—Comprehensive Profit Plan (90 Minutes, but

much less if used in conjunction with 10-47 and completed with an Excel

spreadsheet)

1. Sales Budget

2013

C12 D57 Total

2. Production Budget

Spring Manufacturing Company

Production Budget

2013

C12 D57

Budgeted Sales (in units) 12,000 18,000

Plus: Desired finished goods ending inventory 300 200

Total units needed 12,300 18,200

Chapter 10 – Strategy and the Master Budget

10–49

10–48 (Continued-1)

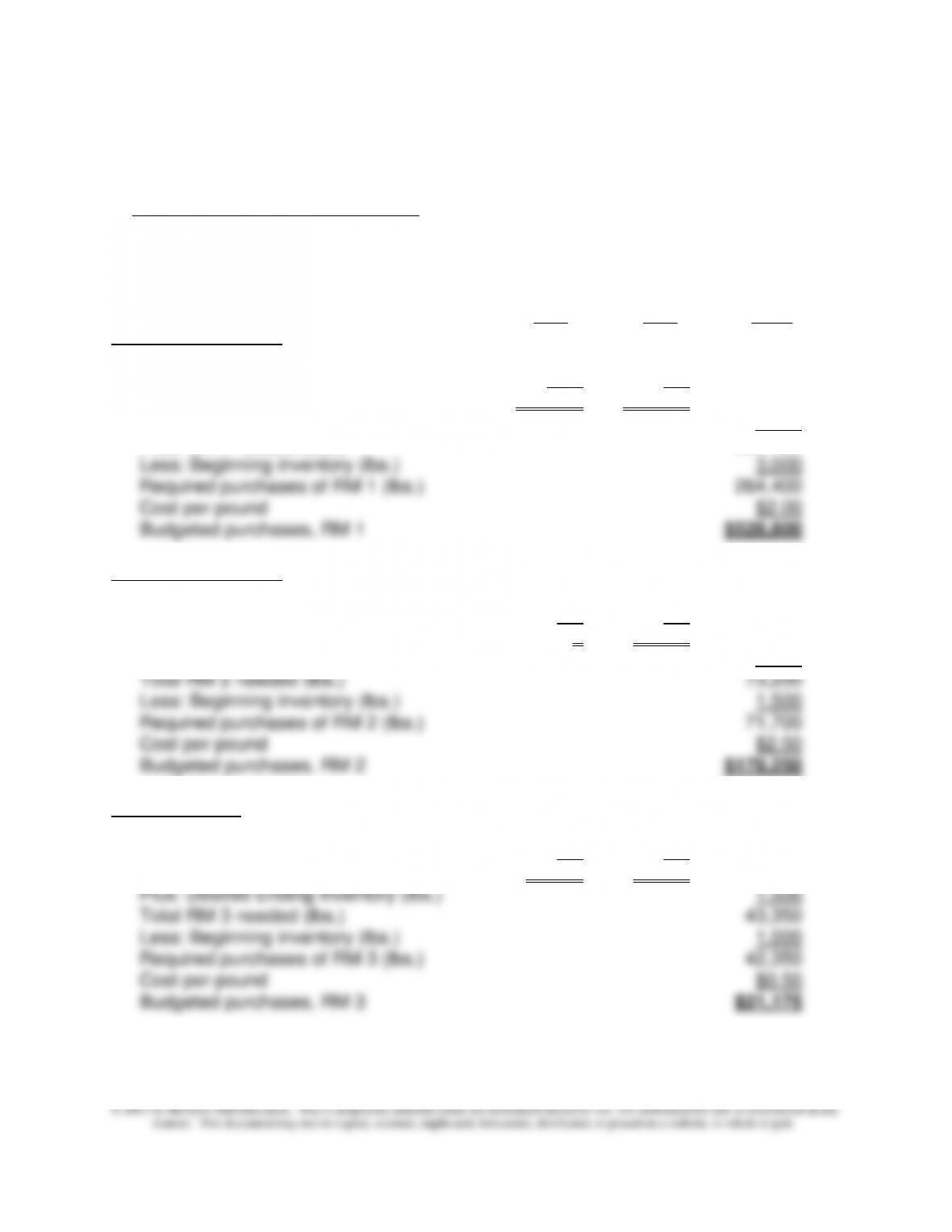

3. Direct Materials Purchases Budget (units and dollars)

Spring Manufacturing Company

Direct Materials Purchases Budget (units and dollars)

2013

C12 D57 Total

Raw Material (RM) 1:

Budgeted Production 11,900 18,050

Pounds per Unit × 10 × 8

RM 1 needed for production 119,000 144,400 263,400

Plus: Desired Ending Inventory (lbs.) 4,000

Total RM 1 needed (lbs.) 267,400

Raw Material (RM) 2:

Budgeted Production 11,900 18,050

Pounds per Unit × 0 × 4

RM 2 needed for production 0 72,200 72,200

Plus: Desired Ending Inventory (lbs.) 1,000

Raw Material 3:

Budgeted Production 11,900 18,050

Pounds per Unit × 2 × 1

RM 3 needed for production 23,800 18,050 41,850

Chapter 10 – Strategy and the Master Budget

10–50

10–48 (Continued-2)

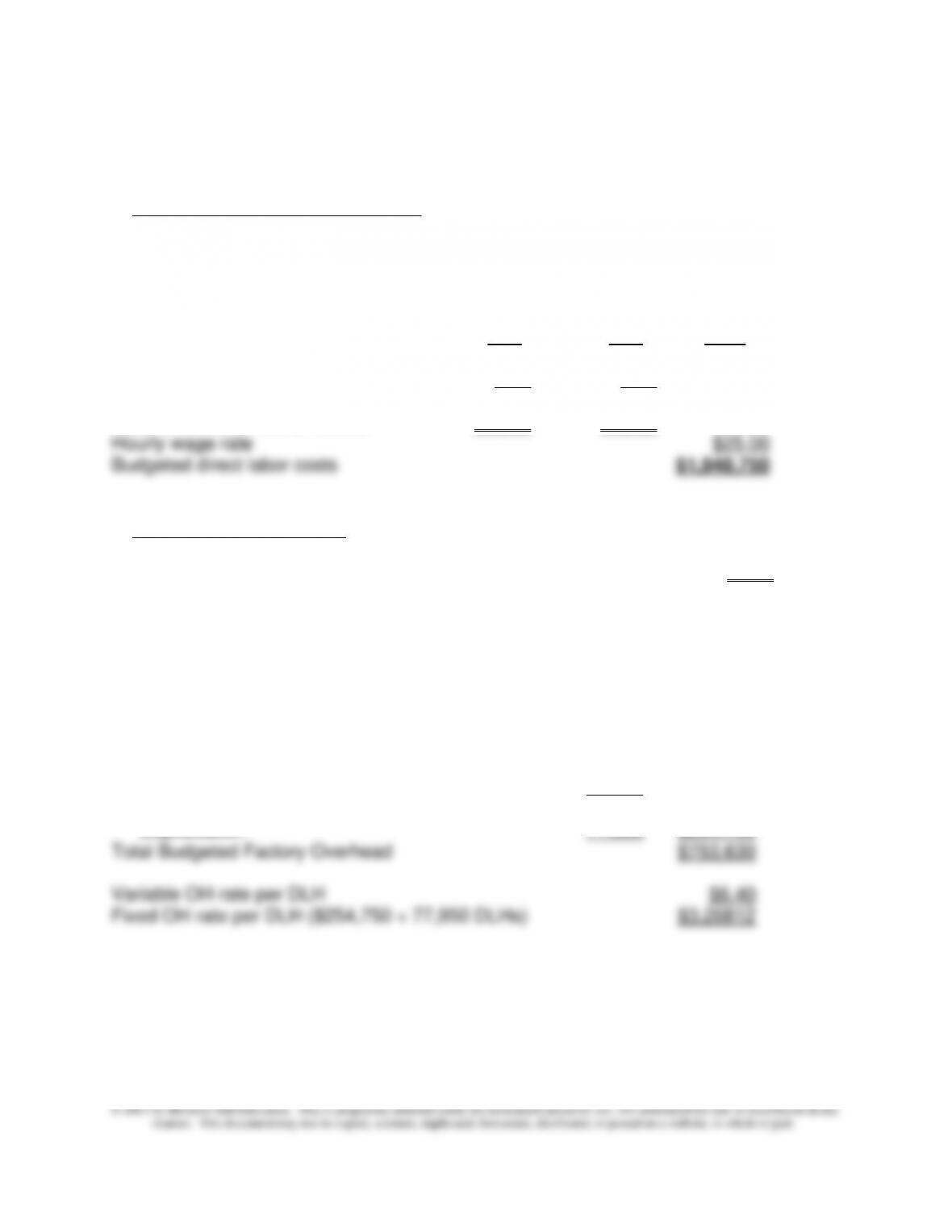

4. Direct Manufacturing Labor Budget

Spring Manufacturing Company

Direct Labor Budget

2013

C12 D57 Total

Budgeted production 11,900 18,050

Direct labor hours (DLH) per unit × 2 × 3

Total direct labor hours needed 23,800 54,150 77,950

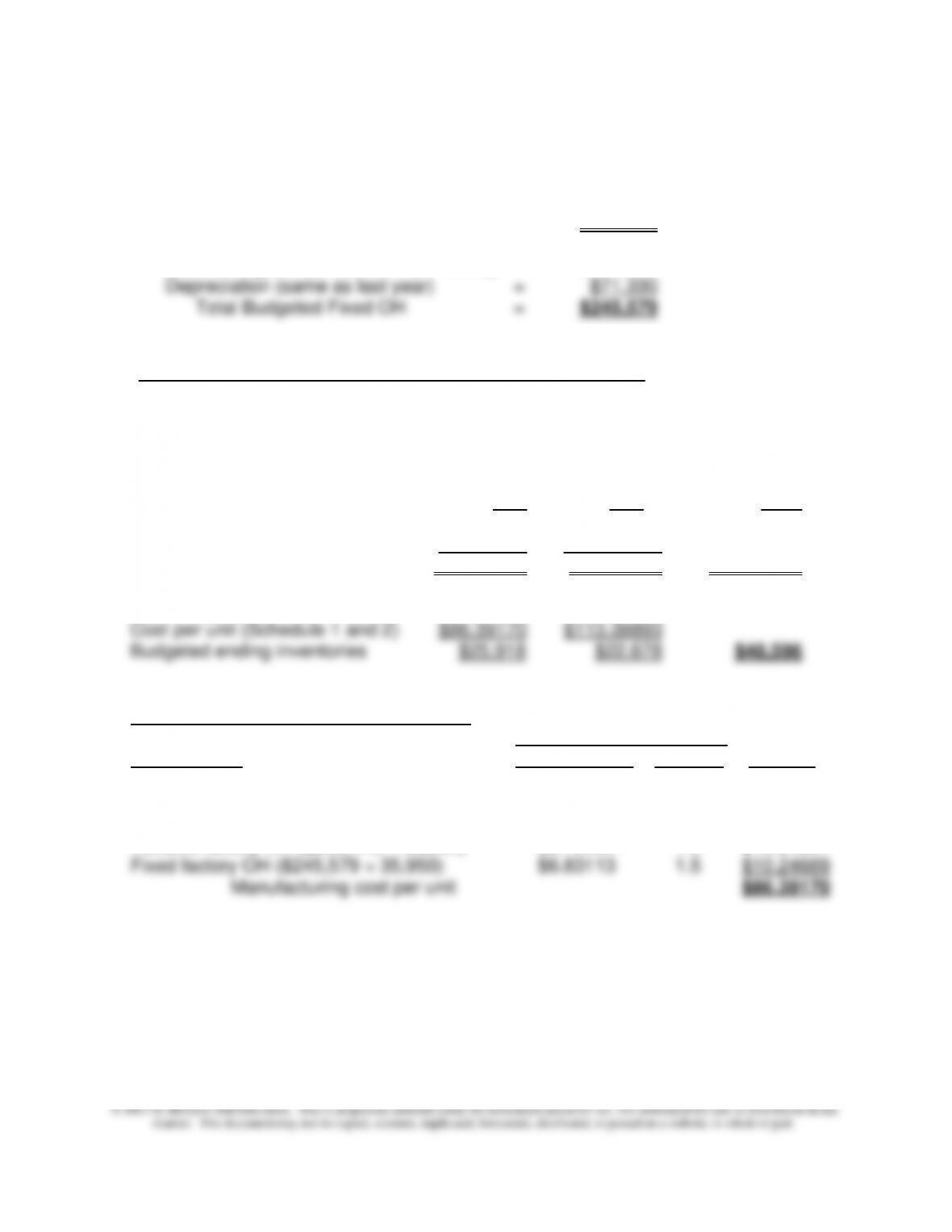

5. Factory Overhead Budget

Variable OH per DLH (fromProb. 10-47): $6.40

Spring Manufacturing Company

Factory Overhead Budget

2013

Variable Factory Overhead ($6.40/DLH × 77,950 DLHs) $498,880

Fixed Factory Overhead:

Supervision $120,000

Maintenance costs 20,000

Heat, light, and power 43,420

Total Cash Fixed Factory Overhead $183,420

Depreciation 71,330 $254,750

Chapter 10 – Strategy and the Master Budget

10–51

10–48 (Continued-3)

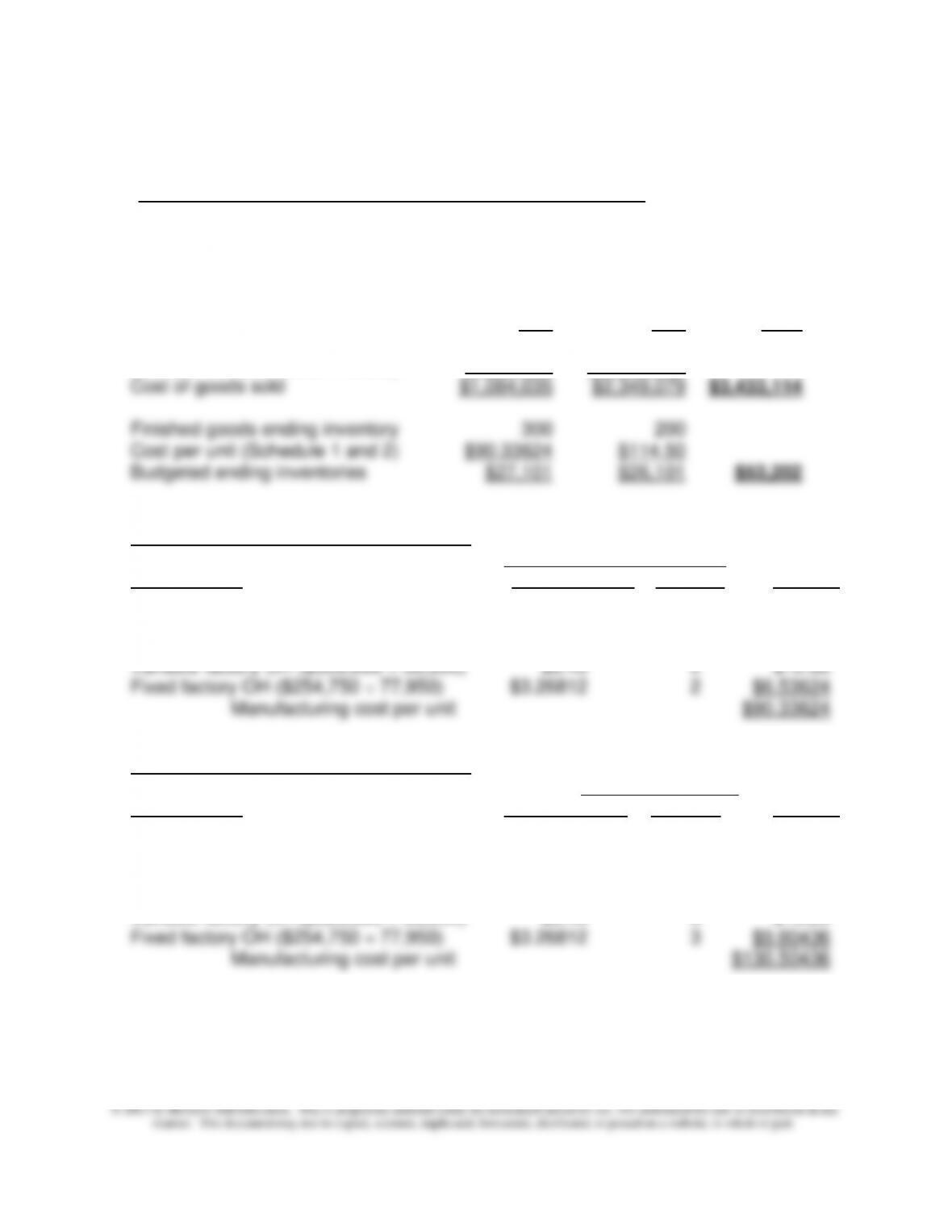

6. Budgeted CGS and Ending Finished Goods Inventory Budget

Spring Manufacturing Company

Ending Finished Goods Inventory and Budgeted CGS

2013

C12 D57 Total

Sales volume 12,000 18,000 30,000

Cost per unit (Schedule 1 and 2) $90.33624 $130.50436

Schedule 1: Cost per Unit—Product C12:

Inputs Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 10 $20.00

RM-3 $0.50 2 $1.00

Direct labor $25.00 2 $50.00

Schedule 2: Cost per Unit—Product D57:

_______ Inputs___ Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 8 $16.00

RM-2 $2.50 4 $10.00

RM-3 $0.50 1 $0.50

Direct labor $25.00 3 $75.00

Variable factory OH ($326,080 ÷ 50,950) $6.40 3 $19.20

10–52

10–48 (Continued-4)

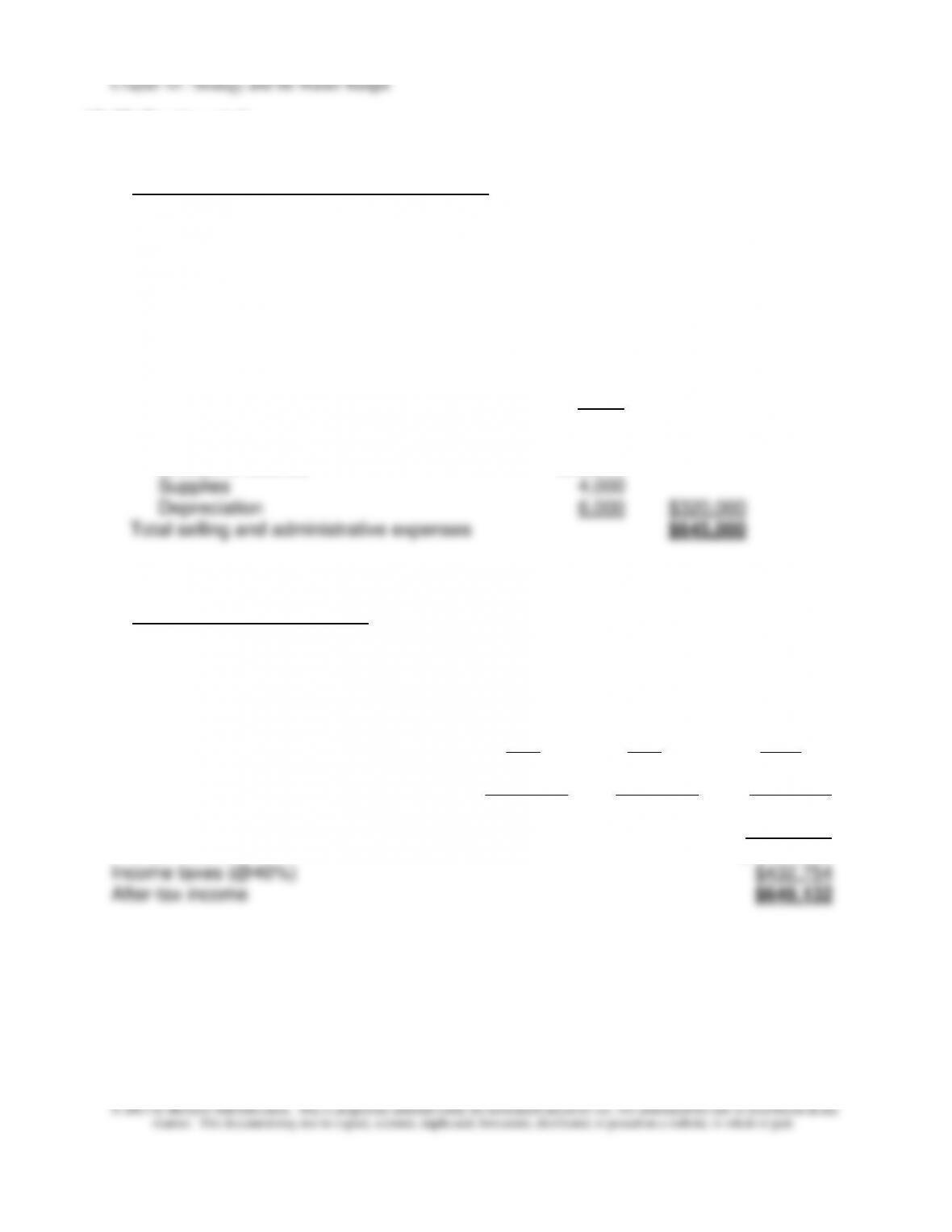

7. Selling and Administrative Expense Budget

Spring Manufacturing Company

Selling and Administrative Expense Budget

2013

Selling Expenses:

Advertising $60,000

Sales salaries 200,000

Travel and entertainment 60,000

Depreciation 5,000 $325,000

Administrative expenses:

Offices salaries $60,000

Executive salaries 250,000

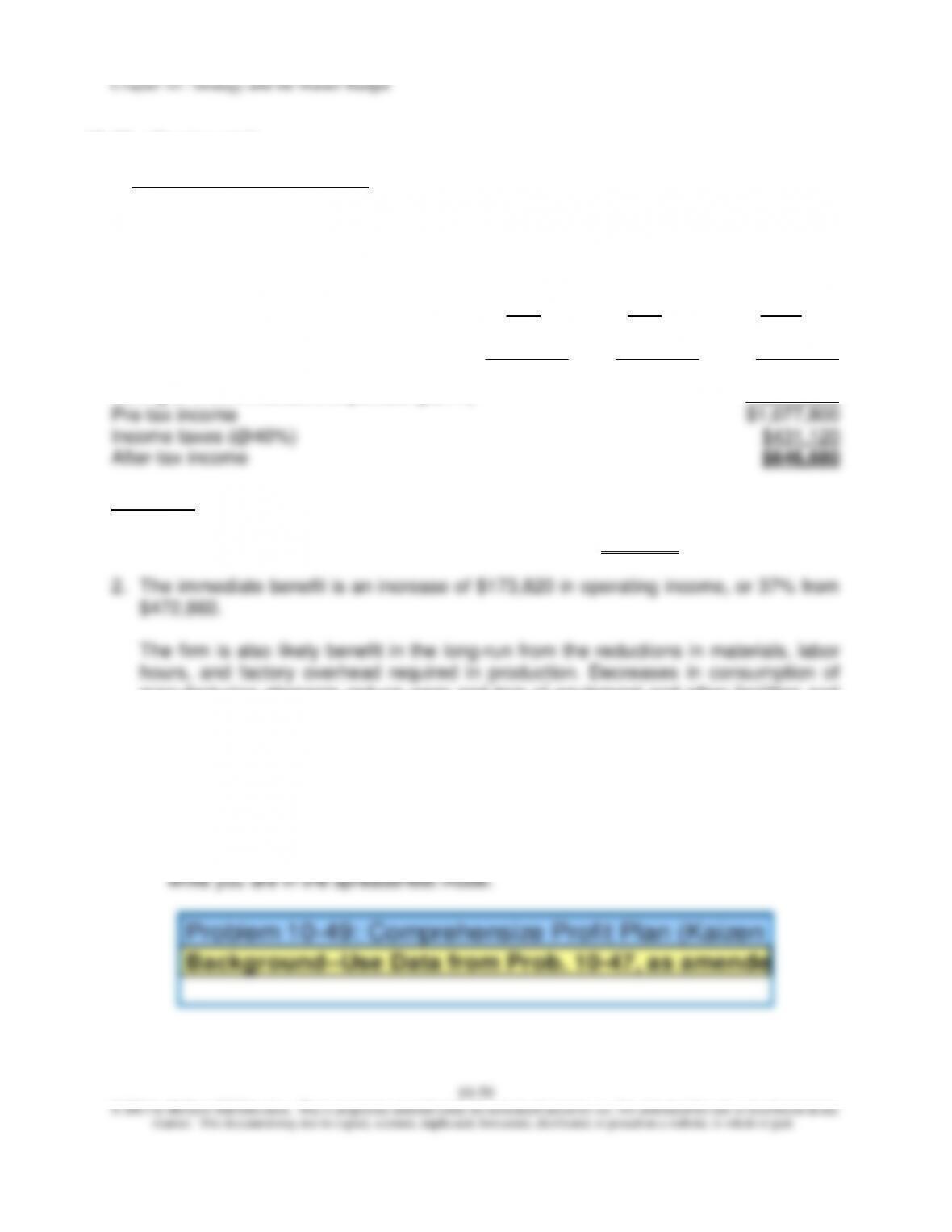

8. Budgeted Income Statement

Spring Manufacturing Company

Budget Income Statement

For the Year 2013

C12 D57 Total

Sales (part 1) $1,920,000 $3,240,000 $5,160,000

Cost of goods sold (part 6) 1,084,035 2,349,079 3,433,114

Gross profit $835,965 $890,921 $1,726,886

Selling and administrative expenses (part 7) $645,000

Pre-tax income $1,081,886

Chapter 10 – Strategy and the Master Budget

10–53

10–48 (Continued-5)

Answers:

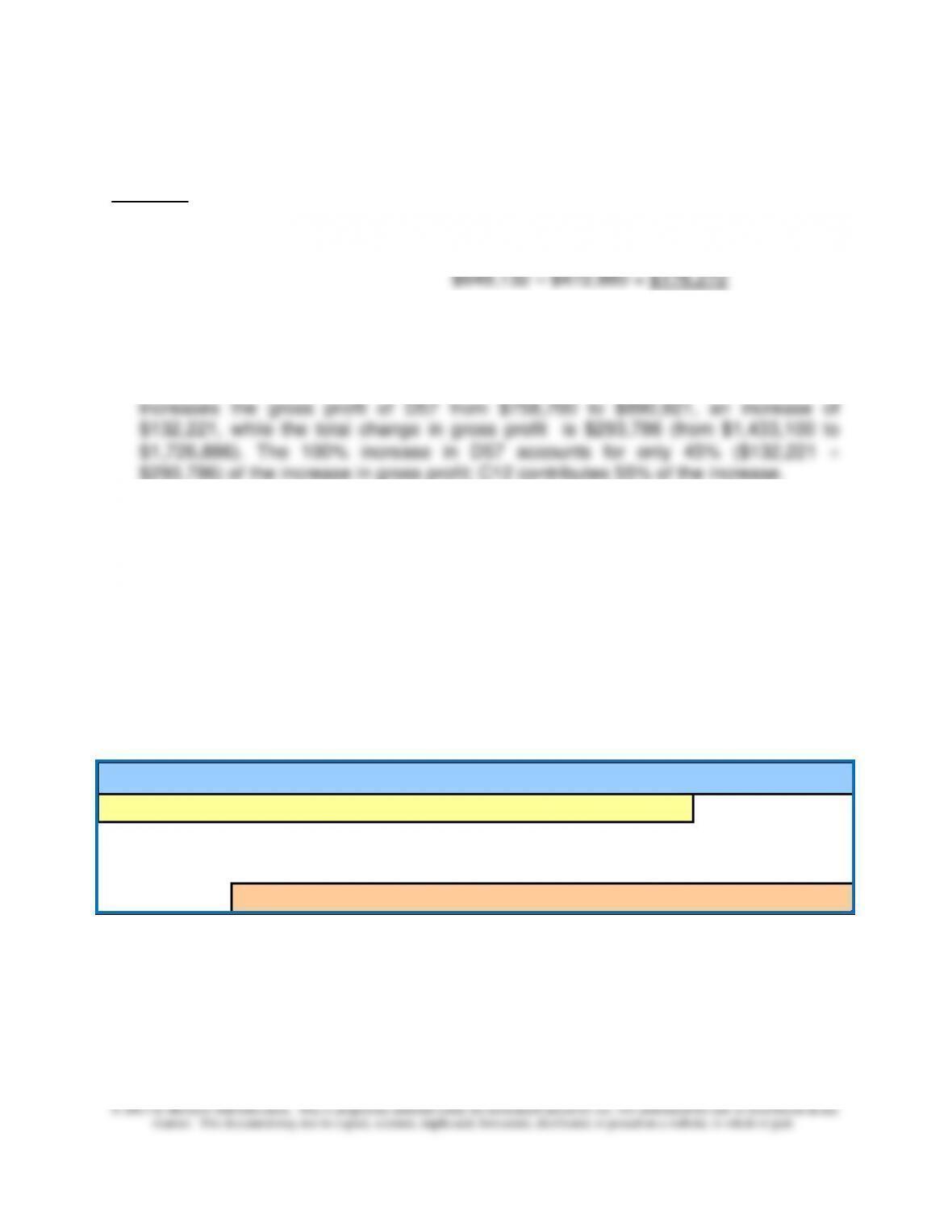

1. The projected increase in after-tax operating income =

$649,132 – $472,860 = $176,272

2. While the changes are projected to increase after-tax operating income, the

company should examine the decision more closely. Although the company

increases its after-tax operating income by 37% ($176,272 ÷ $472,860), it requires a

doubling of units of D57 to achieve this. In fact, a 100% increase in units sold of D57

Further, the price increase in C12 has no effect on the units sold. This may be an

indication that C12 may have a higher potential than the firm perceived.

Note to Instructor: An Excel spreadsheet solution file is embedded in this document.

You can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and

return to…” while you are in the spreadsheet mode.

(Use information in Prob. 10-47 for Spring Manufacturing Company, amen

Problem 10-48: Comprehensize Profit Plan

Background

Chapter 10 – Strategy and the Master Budget

10–54

10-49 Comprehensive Profit Plan with Kaizen (90 minutes, but much less if assigned

in conjunction with 10-47 and completed with an Excel spreadsheet)

1. Sales Budget

Spring Manufacturing Company

Sales Budget

2013

C12 D57 Total

Sales (in units) 12,000 9,000 21,000

2. Production Budget

Spring Manufacturing Company

Production Budget

2013

C12 D57

Budgeted Sales (in units) 12,000 9,000

Plus: Desired finished goods ending inventory 300 200

Total units needed

12,300 9,200

Chapter 10 – Strategy and the Master Budget

10–55

10–49 (Continued-1)

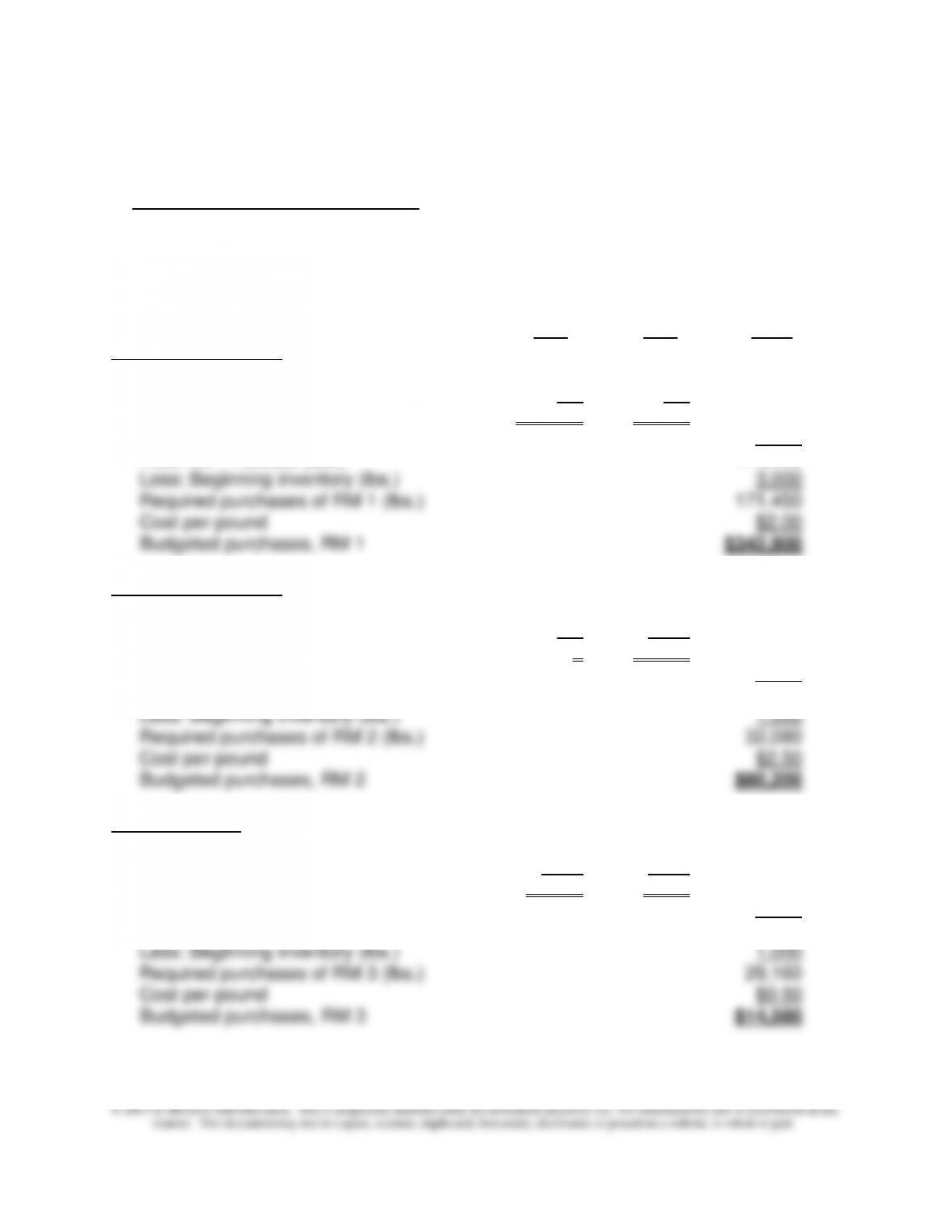

3. Direct Materials Purchases Budget (units and dollars)

Spring Manufacturing Company

Direct Materials Purchases Budget (units and dollars)

2013

C12 D57 Total

Raw Material (RM) 1:

Budgeted Production 11,900 9,050

Pounds per Unit × 9 × 7

RM 1 needed for production 107,100 63,350 170,450

Plus: Desired Ending Inventory (lbs.) 4,000

Total RM 1 needed (lbs.) 174,450

Raw Material (RM) 2:

Budgeted Production 11,900 9,050

Pounds per Unit × 0 × 3.6

RM 2 needed for production 0 32,580 32,580

Plus: Desired Ending Inventory (lbs.) 1,000

Total RM 2 needed (lbs.) 33,580

Raw Material 3:

Budgeted Production 11,900 9,050

Pounds per Unit × 1.8 × 0.8

RM 3 needed for production 21,420 7,240 28,660

Plus: Desired Ending Inventory (lbs.) 1,500

Total RM 3 needed (lbs.) 30,160

10–56

10–49 (Continued-2)

4. Direct Manufacturing Labor Budget

2013

C12 D57 Total

5. Factory Overhead Budget

Spring Manufacturing Company

Factory Overhead Budget

2013

Original Variable OH Budget:

Indirect materials $10,000

Miscellaneous supplies and tools 5,000

Indirect labor 40,000

Payroll taxes and fringe benefits 250,000

Reduction Rate for Variable OH Costs 10.00%

Original Fixed OH, Excluding Depreciation:

Supervision $120,000

Maintenance costs 20,000

Heat, light, and power 43,420

Total Cash Fixed Factory Overhead $183,420

Chapter 10 – Strategy and the Master Budget

10–57

10–49 (Continued-3)

Budgeted Variable OH:

($326,080 × (1 − 0.10)) = $293,472

Budgeted Fixed OH:

Cash Charges = ($183,420 × (1 − 0.05)) = $174,249

6. Budgeted CGS and Ending Finished Goods Inventory Budget

Spring Manufacturing Company

Ending Finished Goods Inventory and Budgeted CGS

2013

C12 D57 Total

Sales volume 12,000 9,000 21,000

Cost per unit (Schedule 1 and 2) $86.39170 $113.38893

Cost of goods sold $1,036,700 $1,020,500 $2,057,200

Finished goods ending inventory 300 200

Schedule 1: Cost per Unit—Product C12:

Inputs __ Cost

Cost Element Unit Input Cos Quantity Per Unit

RM-1 $2.00 9 $18.00

RM-3 $0.50 1.8 $0.90

Direct labor $30.00 1.5 $45.00

Variable factory OH ($293,472 ÷ 35,950) $8.16334 1.5 $12.24501

Chapter 10 – Strategy and the Master Budget

10–58

10–49 (Continued-4)

Schedule 2: Cost per Unit—Product D57:

Inputs Cost

Cost Element Unit Input Cost Quantity Per Unit

RM-1 $2.00 7 $14.00

RM-2 $2.50 3.6 $9.00

RM-3 $0.50 0.8 $0.40

Direct labor $30.00 2 $60.00

Variable factory OH ($293,472 ÷ 35,950) $8.16334 2 $16.32668

7. Selling and Administrative Expense Budget

Spring Manufacturing Company

Selling and Administrative Expense Budget

2013

Selling Expenses:

Advertising $60,000

Sales salaries 200,000

Travel and entertainment 60,000

Depreciation 5,000 $325,000

Administrative expenses:

Offices salaries $60,000

10-49 (Continued-5)

8. Budgeted Income Statement

Spring Manufacturing Company

Budget Income Statement

For the Year 2013

C12 D57 Total

Sales (part 1) $1,800,000 $1,980,000 $3,780,000

Cost of goods sold (part 6) 1,036,700 1,020,500 2,057,200

Gross profit $763,300 $959,500 $1,722,800

Selling and administrative expenses (part 7) $645,000

Answers:

1. The budgeted after-tax operating income with Kaizen is $646,680.

manufacturing elements reduce wear and tear of equipment and other facilities and

lessens the need for additional capital investments/replacements.

Note to Instructor: An Excel spreadsheet solution file is embedded in this document.

You can open this spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

Chapter 10 – Strategy and the Master Budget

10–60

10-50 Budgeting for a Merchandising Firm (40-50 minutes)

1. Budgeted cash collections—December:

From November’s sales = net A/R, November 30th = $ 76,000

From December’s sales = $220,000 × 60% × 99% = 130,680

2. Net accounts receivable—December 31st:

Budgeted sales in December (given) $220,000

Allowance for doubtful accounts $220,000 × 2% = 4,400

Net A/R from sales in December $215,600

3. Budgeted pre-tax operating income—December:

Total sales $220,000

Gross margin ratio × 25%

Gross margin $ 55,000

Operating expenses:

Monthly cash operating expenses $22,600

4. Budgeted Inventory—December 31st:

5. Budgeted Purchases—December:

Inventory, December 1st (given) = $132,000

Inventory, December 31st (part 4 above) = $120,000

6. Budgeted Accounts Payable—December 31st:

Accounts Payable, December 1st (given) $162,000

Plus: Budgeted Purchases, December (part 5 above) $153,000