Chapter 6 – Process Costing

6-1

CHAPTER 6: PROCESS COSTING

QUESTIONS

6-1 A company that should use a process costing system typically has homogenous

products, which pass through a series of similar processes or departments.

6-2 Process costing is likely used in industries such as chemicals, oil refining,

textiles, paints, flour, canneries, rubber, steel, glass, food processing, mining,

6-3 Differences between job and process costing: (1) accumulating costs by job

6-4 Equivalent units are the number of completed units that could have been

produced given the amount of work actually performed on both complete and

6-5 If direct materials are added at the beginning of the process rather than uniformly

throughout the process, we do not need to add any equivalent units of direct

6-6 A production cost report is a report, which summarizes the physical units and

equivalent units of a department, the costs incurred during the period, and costs

assigned to both finished goods and work-in-process inventories. The five key

6-7 The weighted-average method equivalent units include both the units placed into

production in the current period and the units from the prior period that are still in

production at the beginning of this period. FIFO method does not include the

6-8 The weighted–average method would be inappropriate when a firm’s beginning

and ending inventories or manufacturing costs per unit change dramatically from

Chapter 6 – Process Costing

6-2

6-9 The advantage of the weighted-average method is its simplicity.

6-10 From the standpoint of cost control, the FIFO method is superior to weighted-

average because the cost per equivalent unit under FIFO represents the cost for

6-11 Transferred-in costs are costs of work done in the prior department that are

6-12 Work-in-Process Inventory — Second Department $50,000

6-13 Under the FIFO method of handling units transferred out, beginning inventory

6-14 Under the weighted-average method, it makes no difference when a product is

started; all units completed in the same period or in the ending inventory of that

period are treated the same. In computing the equivalent units, this method looks

cost.

6-15 Process costing uses the same manufacturing accounts as job costing. Journal

entries are essentially the same as in job costing. However, instead of tracing

6-16 Backflush costing is a simple costing system that assigns materials and

conversion costs directly to finished goods inventory, by assuming there is little

6-17 Activity-based process costing is an extension of the basic process costing

model in which certain products require significantly more processing costs in

certain activities. Activity-based costing is used together with process costing to

Chapter 6 – Process Costing

6-3

BRIEF EXERCISES

6-18

Work-in–process inventory, 2/1 80,000

Units started 60,000

6-19

Units completed 83,000

Work-in-process inventory, 6/30 55,000

6-20

Units completed 7,300

Work-in-process inventory, 9/30 3,400

6-21

Work-in-process inventory, 11/1 45,000

Units started 57,000

6-22

Weighted Average

Materials: 47,000 = 44,000 + 1.0 x 3,000

Conversion: 45,500 = 44,000 + .5 x 3,000

FIFO

Chapter 6 – Process Costing

6-4

6-23

6-24 Ending WIP must be 2,500 units

6-25

6-26 The number of units transferred in must be 33,000 units

Units

Beginning WIP 5,000

Units started or Trans-in 20,000

Total to account for 25,000

Units Finished or Trans-out 22,000

Normal spoilage 400

Abnormal spoilage 100

Ending WIP 2,500

Total accounted for 25,000

Units

Beginning WIP 6,000

Units started or Trans-in 33,000

Total to account for 39,000

Units Finished or Trans-out 35,000

Normal spoilage 0

Abnormal spoilage 0

Ending WIP 4,000

Total accounted for 39,000

Chapter 6 – Process Costing

6-5

EXERCISES

6-27 Process Costing in Process Industries (10 min)

There are a number of possible answers here. Some examples are given

in the chapter, as well as exercises 4-29 and 4-30 from chapter 4. The

exercise is intended for class discussion. The goals is to have the

students able to identify process-oriented companies in industries such as

chemicals, food processing, beverages, etc. The instructor may choose

to follow up this short question with a more substantive one such as 6-29

which gets into the details of one type of process industry, sugar

manufacturing.

Chapter 6 – Process Costing

6-6

6-28 Equivalent Units; Weighted-Average Method (15 min)

1. Work-in-process inventory, 5/1 1,000

Units started 7,000

Total units to account for 8,000

2. Equivalent units — Weighted-Average Method

Materials:

Units completed 6,000

Work-in-process inventory, 5/31 2,000 x 30% = 600

Total equivalent units 6,600

3. Equivalent units — Weighted-Average Method

Materials:

Units completed 6,000

Work-in-process inventory, 5/31 2,000 x 40% = 800

Total equivalent units 6,800

4. Process costing is a good fit for the fish processing industry because

there is single or a small number of products that are processed through a

6-7

6-29 Process Costing in Sugar Manufacturing (20 min)

1. There are very likely to be transferred in costs in sugar

manufacturing, as there are a number of processes, each of which

could be a separate manufacturing department with its own process

cost report. There are seven steps in the manufacturing process so

there are possibly as many as seven departments, each with its own

much of its volume and weight before the final product (refined sugar)

is produced. The amount of loss, or yield, can be measured as part

of the process costing. The case of sugar manufacturing also

involves joint products (molasses and refined sugar); the costing

methods to measure the cost of joint products are explained in the

next chapter, Chapter 7.

2. As noted in the problem, the raw material for sugar production, sugar

cane, goes through periods of very volatile changes in price. This

means the cost of sugar can fluctuate greatly, and the production

costs may be given greater attention, especially in periods when

prices are low and sugar manufacturers compete on cost leadership

based methods that specifically target operating improvements.

These include activity-based management (chapter 5) the theory of

constraints (chapter 13), lean management and lean accounting

(chapter 17), total quality management (chapter 17), and the flexible

budget (chapters 14-16).

Chapter 6 – Process Costing

6-8

6-29 (continued –1)

3. As in most process industries, sustainability issues arise in the

manufacture of refined sugar. For example, the sugar company

produces a large amount of shredded cane as one of the outputs of

the milling process. The shredded cane is called “bagasse” and is

sustainability issue is to weigh the value of the sugar cane in the

production of refined sugar versus the value of the raw material in

producing fuel in a renewable and environmentally friendly manner.

4. As noted in the problem, the production and consumption of sugar

takes place world-wide, with many of the producing countries (India,

Cuba, Brazil, China, Thailand, and Mexico) somewhat different from

the consuming countries (E.U., U.K., U.S.A., Japan). In addition, the

Sweetener Users Association, an industry group representing sugar

users, has argued for increases in the U.S. quotas.

Source: Alexandra Wexler, “Sugar Runs Into Barriers,” The

Wall Street Journal, March 26, 2012, p C10; Alexandra Wexler,

“Sugar Users Want U.S. to Ease Import Quotas,” The Wall Street

Journal, April 2, 2012,p C11.

Chapter 6 – Process Costing

6-9

6-30 Equivalent Units; Weighted-Average Method (20 min)

Quantity Schedule

Input

Work-in-process inventory, 1/1 30,000

Units started 180,000

Total units to account for 210,000

Output

Units completed (=210,000 – 15,000) 195,000

Work in process inventory (12/31) 15,000

Conversion:

Units completed 195,000

Work-in-process inventory(12/31) 15,000 x 60% = 9,000

Chapter 6 – Process Costing

6-10

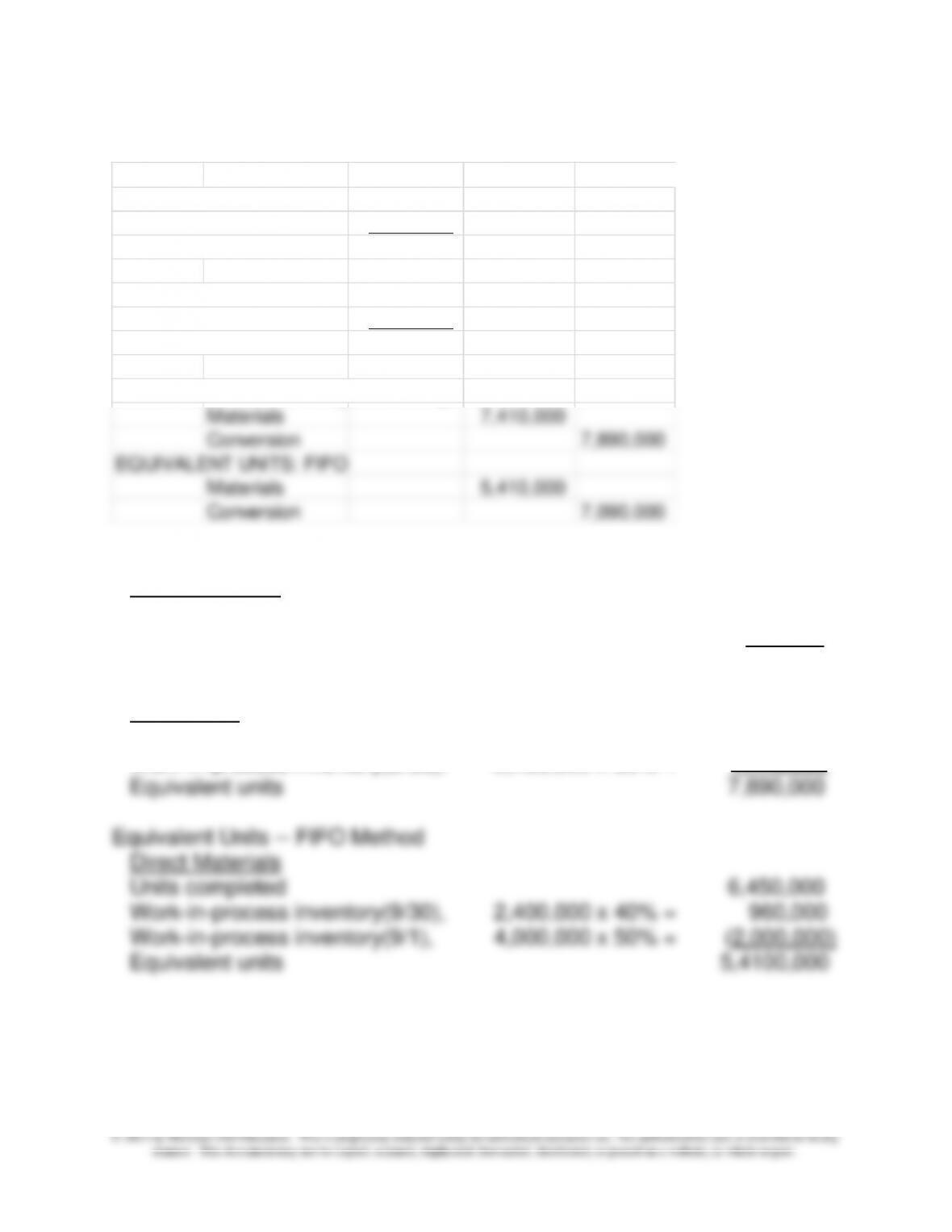

6-31 Equivalent Units; Weighted-Average and FIFO (25 min)

Equivalent Units – Weighted-Average Method

Direct Materials

Units completed 6,450,000

Work-in-process inventory(9/30), 2,400,000 x 40% = 960,000

Equivalent units 7,410,000

Conversion:

Units completed 6,450,000

Work-in-process inventory(9/30), 2,400,000 x 60% = 1,440,000

Units Materials

Conversion

Beginning WIP 4,000,000 50% 20%

Units started or Trans-in 4,850,000

Total to account for 8,850,000

Units Finished or Trans-out 6,450,000

Ending WIP 2,400,000 40% 60%

Total accounted for 8,850,000

EQUIVALENT UNITS: Weighted Average

Materials 7,410,000

Conversion 7,890,000

EQUIVALENT UNITS: FIFO

Materials 5,410,000

Conversion 7,090,000

Chapter 6 – Process Costing

6-11

Conversion:

Units completed 6,450,000

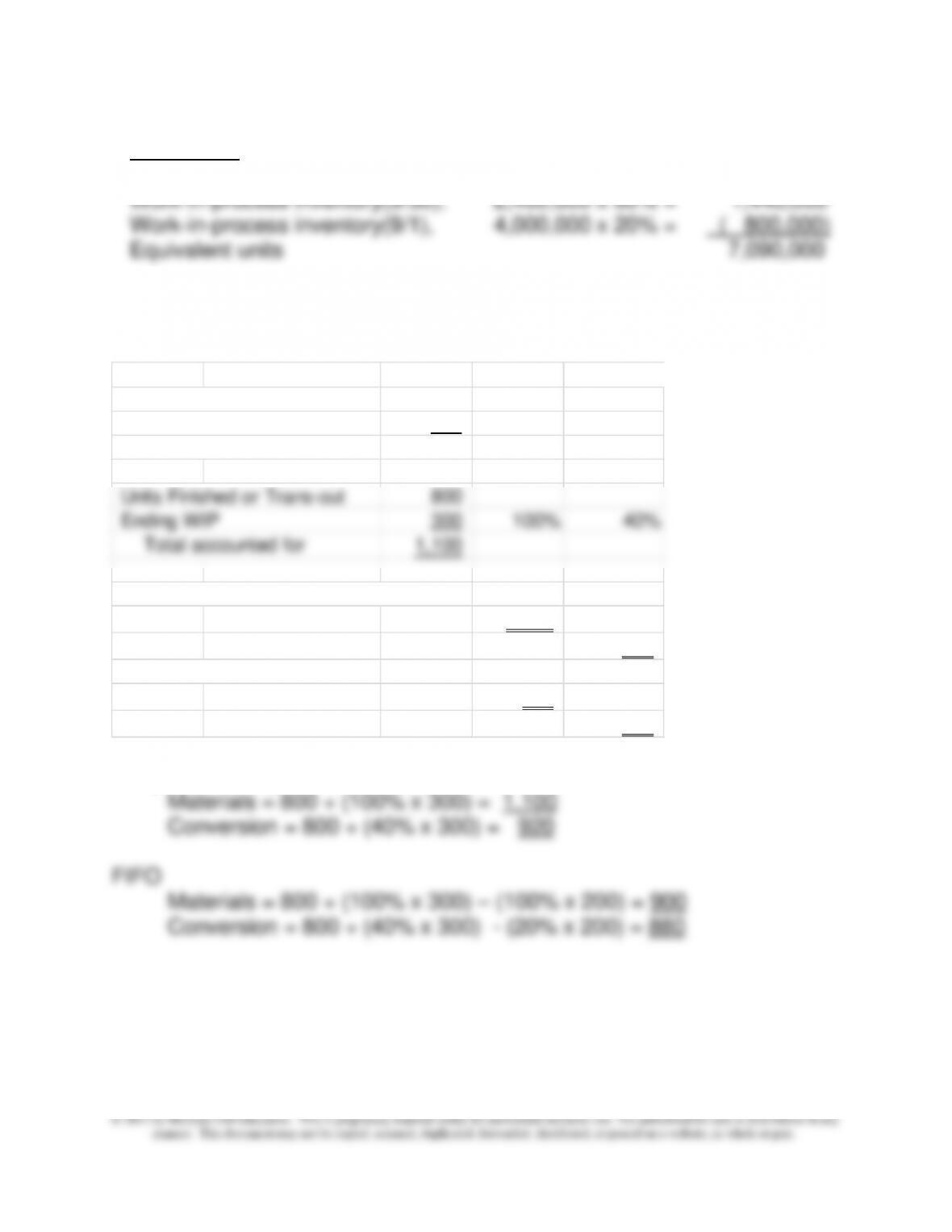

6-32 Equivalent Units; FIFO Method (25 min)

Units started or trans-in = 900 = 800+300-200

Weighted Average:

Units Materials

Conversion

Beginning WIP 200 100% 20%

Units started or Trans-in 900

Total to account for 1,100

Units Finished or Trans-out 800

Ending WIP 300 100% 40%

Total accounted for 1,100

EQUIVALENT UNITS: Weighted Average

Materials 1,100

Conversion 920

EQUIVALENT UNITS: FIFO

Materials 900

Conversion 880

6-33 Equivalent Units: Weighted-Average Unit Cost (20 min)

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 100

Materials 50%

Conversion 50%

Units started 600

Total to account for 700

Units Finished 500 500 500

Ending WIP 200

Materials 50% 100

Conversion – 30% 60

Total accounted for 700 – –

Total Equivalent Units 600 560

DETERMINE TOTAL COSTS Total Materials Conversion

Beginning WIP 110,000$ 50,000$ 60,000$

Current Costs 1,190,000 550,000 640,000

TOTAL 1,300,000$ 600,000$ 700,000$

WTAVG Cost per EU 2,250$ 1,000$ 1,250$

Equivalent Units

Weighted Average

6-13

6-34 Equivalent Units; FIFO Unit Cost (25 min)

1.

Physical Percent

Units Complete Materials Conversion Materials Conversion

Beginning WIP 30,000

Materials 100% 30,000

Conversion 40% 12,000

Units started 70,000

Total to account for 100,000

Units Finished 70,000 70,000 70,000 70,000 70,000

Ending WIP 30,000

Materials 100% 30,000 30,000

Conversion –

80% 24,000 24,000

Total accounted for 100,000 – – – –

Total Equivalent Units 100,000 94,000 70,000 82,000

DETERMINE TOTAL COSTS Total Materials Conversion Materials Conversion

Beginning WIP 84,000$ 60,000$ 24,000$

Current Costs 420,000 120,000 300,000 120,000$ 300,000$

TOTAL 504,000$ 180,000$ 324,000$

WTAVG Cost per EU 5.2468$ 1.800$ 3.4468$

FIFO Cost per EU 5.3728$ 1.7143$ 3.6585$

Equivalent Units

Equivalent Units

Weighted Average

FIFO

Weighted Average:

Materials: $1.80

2. The differences between the cost per equivalent unit (FIFO vs weighted–

average) for materials and conversion are due to differences in the per unit

amounts in beginning WIP and current costs. These differences are

Chapter 6 – Process Costing

6-14

6-35 FIFO Method (25 min)

1. Equivalent units

Returns completed during March 1,500*

Returns in process, 3/31: 200 x 90% = 180

2. Cost per equivalent unit

$173,250 / 1,650 = $105

3. Cost of completed returns

From beginning inventory, 3/1: $2,500

Added to finish the beginning inventory:

4. Cost of returns in process on March 31

Chapter 6 – Process Costing

6-15

PROBLEMS

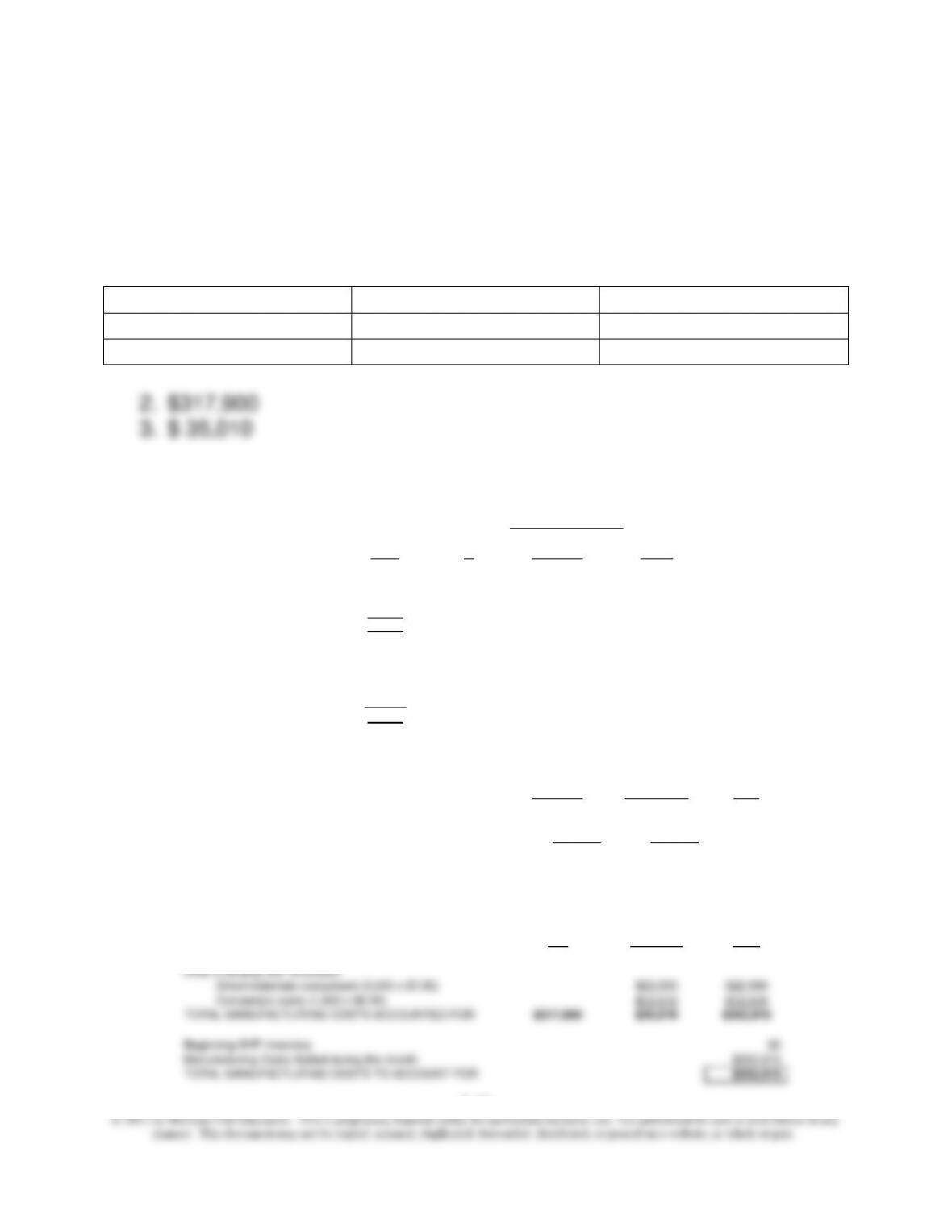

6-36 Weighted Average Method

1.

Materials

Conversion

Equivalent units

25,000

23,800

Cost per Equiv. Unit

$7.50

$6.95

Answers are shown in the process cost report below.

Equivalent Units

Physical Completion Direct Conversion

Units % Materials Costs

Beg. WIP Inventory: 0

DM 0%

Conversion Cost 0%

Units started during May 25,000

Units to Account For 25,000

Units completed 22,000 100% 22,000 22,000

Ending WIP Inventory: 3,000

DM 100% 3,000

Conversion cost 60% 1,800

Units Accounted For 25,000 ________ _______

Equivalent Units Produced 25,000 23,800

Cost Element

Materials Conversion Total

Total Manufacturing Cost (numerator of calculation):

Beginning WIP Inventory $0 $0

Manufacturing Costs Added in Current Month $187,500 $165,410

Total Cost $187,500 $165,410

Number of Equivalent Units Produced 25,000 23,800

Cost per Equivalent Unit $7.500 $6.9500 $14.45

Units Completed Units in Ending

and Transferred WIP

Out Inventory Total

Goods Completed and Transferred Out (22,000 x $14.45) $317,900 N/A $317,900

Units in Ending WIP Inventory:

Direct materials component (3,000 x $7.50) $22,500 $22,500

Conversion costs (1,800 x $6.95) $12,510 $12,510

TOTAL MANUFACTURING COSTS ACCOUNTED FOR $317,900 $35,010 $352,910

Beginning WIP Inventory $0

Manufacturing Costs Added during the month $352,910

TOTAL MANUFACTURING COSTS TO ACCOUNT FOR $352,910