Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-61

in terms of presenting an estimate of the amount of "capital"

employed during the period.

19-47 (Continued-2)

(2) LIFO Reserve: the entire amount of the LIFO reserve is added as an

adjustment. This adjustment brings the inventory amount from LIFO

to FIFO (i.e., current-cost) basis.

(3) Deferred Income Tax: deferred income tax arises from a difference in

the timing when revenues and expenses are recognized for tax

3. EVA®:

EVA® NOPAT =

$53

Capital Charge:

EVA® Capital =

$925

WACC =

10.70%

$99

EVA® =

($46)

The negative EVA amount suggests that during the most recent period,

the company did not earn a sufficient amount of economic (cash) profit

to fully compensate the suppliers of capital. That is, during the most

recent period, stockholder value was not created.

19-48 EVA®, Shareholder Value Analysis, and Sustainability; Internet-

Based Research (90 Minutes, including search time)

1. Economic Value Added (EVA®) is essentially a measure of economic

profit during a period. EVA® for a given period can be estimated as

follows:

EVA® = NOPAT – Imputed Charge for the Use of Capital (Assets)

During the Period

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-62

= NOPAT – (k × Average Invested Capital)

= After-tax cash operating income, after depreciation – (k ×

Average Invested Capital)

= Revenues – Cash Operating Costs – Depreciation – Cash

Taxes on Operating Income

where: k = cost of capital (e.g., weighted-average cost of capital), and

Capital = Economic Capital = Cash Contributed by Suppliers of

Funds to the Business Unit (or firm as a whole)

Notice that relative to an accounting-based approach to income

determination (which is based on accrual concepts), EVA® is attempts

to measure economic profit for a period (i.e., the amount of value

added to the firm during a period). On the surface, the EVA® formula

looks similar to residual income (RI). However, RI relies on accounting-

based estimates of both income and capital, while EVA® is based on

economic concepts for these variables. Put another way, the EVA®

calculation begins with accounting-based measures, then adjusts

these to better approximate the amount of economic earnings (or,

value added) during a period.

2. The key here is to view the constituent parts of EVA® as a guide for

evaluating the contribution of sustainability-related initiatives (programs,

projects, etc.) to shareholder value, as follows:

EVA® = Shareholder Value Added = NOPAT – Capital Charge

19-48 (Continued-1)

Thus, shareholder value can be increased either by increasing NOPAT

or by decreasing the imputed capital charge. In turn, NOPAT can be

increased in essentially two ways, each of which provides a basis for

assessing the contribution of an investment project (such as a

sustainability initiative):

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-63

• growth initiatives that increase revenues (e.g., product/process

The imputed capital charge is a function of both the amount of capital

employed and the cost of capital (risk, or discount rate). Thus, the

charge for capital employed can be reduced (thereby increasing EVA®,

everything else held constant) either through better/more efficient

utilization of assets (e.g., through process simplification or through

supply chain streaming) or by reducing the discount rate (investments in

social and/or environmental projects tend to reduce social and/or

political risk, thereby reducing the discount rate).

3. Student responses to this requirement will differ. In his book Making

Sustainability Work: Best Practices in Managing and Measuring

Corporate Social, Environmental, and Economic Impacts (San

Francisco, CA: Berrett-Koehler Publishers, Inc.), Marc Epstein offers (p.

141) the following two examples:

a. DuPont uses a metric called “shareholder value added per pound of

production” or SVA/lb. SVA is defined as “shareholder value created

above the cost of capital. A company increases SVA by adding

material, knowledge, or both. SVA/lb. emphasizes the addition of

knowledge, rather than material. DuPont has used this metric to

evaluate its business units and set goals to increase its SVA/lb.

based on those evaluations.

19-48 (Continued-2)

b. Georgia-Pacific used shareholder value analysis to align the

company’s goals of creating shareholder value and environmental

responsibility (critically important for a forest-products company).

The EH&S department at Georgia-Pacific, as well as individual

environmental projects, has been evaluated using shareholder value

analysis. Included in each environmental project evaluation is an

assessment of the project’s impact on revenues, operating costs (such

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-64

as consulting fees, fines, and administrative costs), and capital costs.

Using shareholder analysis, Georgia-Pacific has been able to identify

environmental investments that create financial and stakeholder value

for the company.

4. The purpose of this question is to motivate students to think more

broadly (e.g., in terms of strategic performance measurement systems)

that could be used to support corporate sustainability initiatives. Implicit

in the discussion is the role of the management accountant in the design

of such systems.

Students will likely already have been exposed to the Balanced

Scorecard (BSC) as one example of a strategic management system

(or, a strategic performance measurement system). Thus, they might

metrics. Alternatively, students may recommend that a fifth performance

perspective/dimension be added to an organization’s BSC:

sustainability. This new dimension would include social and

environmental performance indicators that link with the other four

dimensions of the BSC. This alternative approach would highlight the

importance of social and environmental responsibility as a core

corporate objective.

In Making Sustainability Work: Best Practices in Managing and

Measuring Corporate Social, Environmental, and Economic Impacts

19-48 (Continued-3)

(San Francisco, CA: Berrett-Koehler Publishers, Inc.), Marc Epstein

suggests (p. 138) the following reasons why companies would choose to

establish a separate BSC perspective for sustainability:

1. Social and environmental responsibility is seen as a core to the

strategy of the organization, creating competitive advantage (through

factors such as corporate image, reputation, and product

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-65

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

differentiation), as opposed to being seen as a means to improve

operational efficiency.

2. The fifth perspective becomes a tool to focus the attention of

managers on social and environmental responsibility as a core

about these issues and objectives.

3. When a company has high-profile or high-impact social and

environmental issues, a fifth perspective on the BSC helps to highlight

4. When the resource allocation to social and environmental

responsibilities is relatively large, companies may want to highlight

the link between the use of those resources and company strategy.

In the course of their information search, students may have encountered

reference to the BSC that Nike developed to help identify the reason for

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-66

19-49 General Transfer-Pricing Rule; Goal Congruence (30-40 Minutes)

1. Using the general guideline presented in the chapter, the minimum price

at which the Transmission Division (i.e., the producer) would sell

standard transmissions to the Auto Division (i.e., the buyer) is $900 per

unit, the incremental costs. The Transmission Division currently has idle

sense that it induces the correct decision from the standpoint of the

company as a whole.

2. Transferring products internally at incremental cost has the following

properties:

a. Achieves goal congruence? Yes, as described in requirement 1

above.

b. Useful for evaluating division performance? No, because this transfer

price does not cover or exceed full costs. By transferring at

Transmission Division has little incentive to control costs.

d. Preserves division autonomy? No. Because it is rule-based, the

Transmission Division has no say in the setting of the transfer price.

3. If the two divisions were to negotiate a transfer price, the range of

possible transfer prices will be between $900 and $1,250 per unit. The

Transmission Division has excess capacity that it can use to supply

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-67

19-49 (Continued)

transmission. The Auto Division will be willing to buy units from the

Transmission Division only if the price does not exceed the external

$900 and $1,250 will depend on the bargaining strengths of the two

divisions. The negotiated transfer price has the following properties.

a. Achieves goal congruence? Yes, as described above.

b. Useful for evaluating division performance? Yes, because the transfer

price is the result of direct negotiations between the two divisions. Of

specified by headquarters on the basis of some rule (such as the

producing division’s incremental costs).

4. Neither method is perfect, but negotiated transfer pricing (requirement 3)

has more favorable properties than the cost-based transfer pricing

(requirement 2). Both transfer-pricing methods achieve goal

congruence, but negotiated transfer pricing facilitates the evaluation of

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-68

19-50 Transfer-Pricing Methods (45-60 minutes)

1. a. The positive and negative motivational implications arising from

employing a negotiated transfer price system for goods exchanged

between divisions include the following:

Positive:

• Both the buying and selling divisions have participated in the

autonomy/independence of the divisions.

Negative:

• The result of a negotiated transfer price between divisions may not

b. The motivational problems which can arise from using actual full

(absorption) manufacturing costs as a transfer price include the

following.

• Full-cost transfer pricing is not suitable for a decentralized

structure where the autonomous divisions are measured on

fixed costs. This price reduction would optimize overall company

performance.

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-69

19-50 (continued-1)

2. The motivational problems that could arise if Mylar Corporation decides

to change its transfer pricing policy to one that would apply uniformly to

all divisions, include the following:

• A change in policy may be interpreted by the divisional managers as

and bonuses.

3. The likely behavior of both buying and selling divisional managers, for

each of the following transfer pricing methods being considered by Mylar

Corporation, include the following:

a. Standard full manufacturing costs plus a markup.

• The selling divisions will be motivated to control costs because any

divisions will be unhappy.

b. Market selling price of the product being transferred.

• Creates a fair and equal chance for the buying and selling divisions

to make the most profit they can and should promote cost control,

willing to enter into the transaction.

19-70

19-50 (continued-2)

c. Outlay (out-of-pocket) costs incurred to the point of transfer plus

opportunity cost per unit.

• This method is the same as market price when there is an

established market price and the seller is at full capacity. At any

level below full capacity, the transfer price is the outlay cost only

realize for the product under the circumstances. This method

should promote overall goal congruence between managers and

the firm, should motivate managers, and should optimize overall

company profits.

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-71

19-51 Transfer Pricing; Decision Making (30-45 minutes)

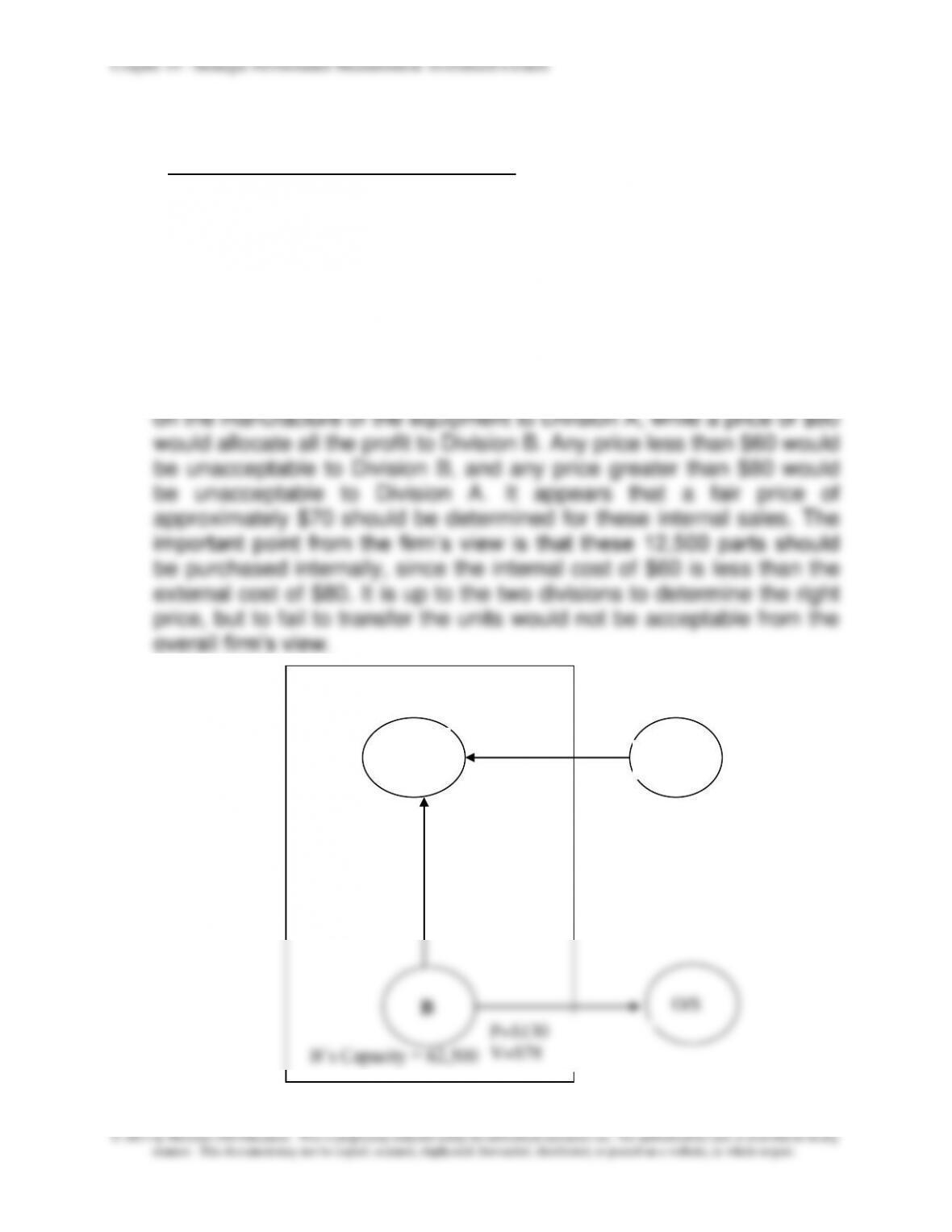

1. Division B has capacity to produce 62,500 units (50,000 ÷ 0.80).

Division A will require 25,000 units, which will limit B’s outside sales

to 37,500 units, a loss in outside sales of 12,500 units (50,000 −

37,500).

The contribution for each type of sale by Division B is:

To Division A Outside

Selling Price $ 75 $130

Determining the Best Decision (assuming Division A requires all

25,000 units):

The best decision in the interest of Division B is to not sell all 25,000

units to Division A:

Contribution for selling 25,000 units to Division A:

The Division B manager should reject the proposal because it

reduces Division B’s operating income by $275,000.

Also, the decision of Division B to not sell inside is in the best interest

of the firm as a whole. The savings to the firm of Division A buying

19-72

19-51 (continued)

If Partial Sales to Division A are OK:

Division B should sell as many units as possible (in this case 50,000

of total demand) to outside consumers. The remaining capacity (20%,

or 12,500 units) should be used to provide Division A with equipment.

2. Assuming that Division B limits its sales to Division A to the excess

capacity of 12,500 units, the best transfer price should fall in the range

of $60 (Division B’s variable cost) and $80 (the outside purchase cost

to Division A). The two divisions should negotiate to determine the

desired price in this range. A price of $60 would allocate all the profit

A

B

O/S

O/S

P=$75 (what division A

wants)

V=$60

P=$130

V=$78

P=$80

B’s Capacity = 62,500

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-73

19-52 Transfer Pricing; Strategy (30-45 minutes)

1. There are three options for the commercial division: buy from the

internal supplier (the industrial division), buy from Admiral Electric, or

buy from Advanced Micro. The analysis follows, from the perspective

of FMI:

Buy inside from the industrial division:

Cost to FMI (assuming the Industrial Division is at full capacity):

Ind. Div.’s variable cost: $155 × 5,000 $775,000

Buy from Admiral Electric: Cost to FMI is $210. The contribution on

sales to Admiral by the industrial division is ignored because these

sales are not contingent on the commercial division’s decision.

Buy from Advanced Micro:Cost to FMI: $200

Best decision for FMI: have the commercial division buy from

Advanced Micro, presuming the parts sold by Advanced Micro and

Admiral Electric are of equivalent quality and service. The cost is the

lowest, at $200.

The best transfer price, which would cause the buying division to

autonomously make the correct decision, would be to use the selling

division’s market price of $205.

2. If the sales to Admiral Electric by the industrial division were

contingent on the commercial division’s decision, the relevant cost to

FMI would be the price of $210 × 5,000 units (amount needed over

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-74

19-52 (continued)

3. The decision to have the commercial division buy outside to reduce

overall costs is also consistent with a strategy of decreasing the

reliance of the commercial division on products from the industrial

division. If top management is unsure about the growth potential of the

industrial division and has declined any new investments there,

perhaps the future holds capacity reduction or divestment of the

division’s decision. This is a positive statement about the quality of the

industrial division’s product and the quality of its relationship with

Admiral. Perhaps top management should rethink its long-term

strategy for the industrial division.

Chapter 19 - Strategic Performance Measurement: Investment Centers

19-75

19-53 Strategy; Strategic Performance Measurement; Transfer Pricing

(45-50 minutes)

1. Transfer prices based on cost are not appropriate as a divisional

performance measure, and among the reasons are because they:

• provide little incentive for the selling division to control manufacturing

2.Using the market price as the transfer price the contribution margin for

both the Mining Division and the Metals Division for the year ended May

31, 2013 is as calculated below.

Ajax Consolidated Calculation of

Divisional Contribution Margin

For the Year Ended May 31, 2013

Mining Division

Metals Division

Selling Price

$90

$150

Less: Variable costs

Direct materials

12

6

Direct labor

16

20

Manufacturing overhead (1)

24

10

Transfer price

0

90

Unit contribution margin

$38

24

× Volume

× 400,000

× 400,000

Total contribution margin

$15,200,000

$9,600,000

Notes:

(1) Variable overhead = $32 × 75% = $24 for mining division;

Variable overhead = $25 × 40% = $10 for metals division

(2) The $5 variable selling cost that the Mining Division would incur for

sales on the open market should not be included as this is an

internal transfer.