Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-42

5-47 (continued –1)

2. The additional business with AS would leave very little unused

capacity(less than 3%) as shown below:

Total Calls

Answered

Avg. No. of

Minutes/

Call

Total Time (minutes)

Inquiries

Autos

Trucks

Total

Inquire re: Rates and

Terms

Autos

96,000

5

480,000

Trucks

32,000

7

224,000

Inquire re: Loan App Status

Autos

37,500

6

225,000

Trucks

6,750

11

74,250

Inquire re: Payment Status

Autos

39,000

3

117,000

Trucks

12,000

4

48,000

Inquire re: Other Matter

Autos

29,000

11

319,000

Trucks

8,500

15

127,500

Total

1,141,000

473,750

1,614,750

Processing Credit Checks

Auto

45,600

10

456,000

Truck

12,500

18

225,000

Total Processing Minutes

456,000

225,000

681,000

Total Minutes for the Combined

Engagement

2,295750

Minutes for other Clients

9,499,421

Total Minutes

11,795,171

Unused Capacity

249,829

Call Center Capacity

12,045,000

The cost of the unused capacity could be determined as follows:

$.78/min × 249,829 minutes = $194,867

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-43

5-48 Personnel Planning; TDABC(30 min)

1. Unlike a manufacturing company, almost all costs for a service company

are indirect in nature. Almost all of these costs are supplied in advance;

short-term spending is generally not affected by fluctuations in demand or

produce/service mix. Thus, traditional accounting practice is to view such

2. As indicated in the text, two items need to be estimated for each

department or process in conjunction with a TDABC model: (1) the unit

cost of supplying capacity for the department or process in question (this

is also referred to as the capacity cost rate), and (2) the consumption of

capacity (i.e., an estimate of how much capacity (measured, generally

speaking, in terms of time) by activities performed. As to item (1), we

3. and 4.

Claim information

Remote

Processing

On-site

Processing

Total

Processing time/claim

0.50

1.00

Customer record maintenance/claim

0.20

0.20

Total time per claim

0.70

1.20

× Number of claims

1,900

2,900

4,800

Total hours needed

1,330

3,480

4,810

× Capacity cost per hour

$ 51

$ 51

Budgeted support costs

$ 67,830

$ 177,480

$ 245,310

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-44

5-48 (continued –1)

5.

Claim information

Remote

Processing

On-site

Processing

Total

Processing time/claim

0.50

1.00

Customer record maintenance/claim

0.20

0.20

Total time per claim

0.70

1.20

× Number of claims

2,700

2,000

4,700

Total hours needed

1,890

2,400

4,290

× Capacity cost per hour

$ 51

$ 51

Budgeted support costs

$ 96,390

$ 122,400

$ 218,790

Note that the capacity cost per hour is unchanged because 3 workers are still needed to handle the

demand. (1 worker has about 1,667 hours of capacity, which is 5,000 hours ÷ 3 workers, so 4,290 hours

needed ÷ 1,667 = 2.6 workers).

6. As noted above in response to Requirement 1, many support costs are

short-term fixed costs, related to the supply of capacity/service. Thus, after

companies institute cost-saving measures or process improvements in

response to ABC-based data, there might not be immediate financial

7. The underlying theory is that when cost-allocation rates are estimated in

conjunction with an ABC system the denominator volume level should be

consistent with the numerator (resource spending). That is, the numerator

represents the dollar amount of resource cost for a given activity (e.g.,

claims processing). The denominator should logically be measured as the

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-45

5-48 (continued –2)

terms of bringing the demand for and supply of resources in each

support area (process).

5-49 Assessing Customer Lifetime Value (45 min)

1. The primary issue addressed in the article is the effort to boost the

total value of each of the firm’s customers.

2. Customer lifetime value is the estimate of how much a customer is

expected to spend on a company’s products and/or services for some

designated time, less the cost of marketing to that customer. Customer

referral value is an estimate of the lifetime value of a customer that

would not otherwise have become a customer if the referral had not

exceed the spending of any one customer that made the referrals.

3. Customer referral value is more difficult to estimate because of the

number of variables involved. In addition to estimating the expected

lifetime value of each referral, the number of successful referrals must

also be estimated. This entails estimating how many new customers

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-46

5-49 (continued –1)

4. The customer value matrix is a method of categorizing the

organization’s customers based on their value to the firm. Since the

authors found that CLV is not a good predictor of CRV, it became

necessary to capture these two different dimensions of a customer’s

5. The determination of CLV and CRV both require the ability to identify the

resources directed toward the acquisition and retention of customers.

This fundamental requirement matches up with the underlying theme of

5-47

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution

in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

5-50 Volume-Based Costing vs. ABC (30 min)

1. Current Costing System – Direct-Labor-Hour Based

Overhead rate = Budgeted overhead ÷ Budgeted direct labor hours

Overhead cost allocation:

Cost per capsule:

Diomycin

Homycin

Addolin

Direct labor-hours

7,200

6,800

2,000

Overhead rate

$12.50

$12.50

$12.50

Total overhead

$90,000

$85,000

$25,000

Diomycin

Homycin

Addolin

Direct Materials

$205,000

$265,000

$258,000

Direct Labor

250,000

234,000

263,000

Overhead:

90,000

85,000

25,000

Total Cost

$545,000

$584,000

$546,000

Packets produced

1,000,000

500,000

300,000

Cost per capsule

$0.545

$1.168

$1.820

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-48

5-50 (continued-1)

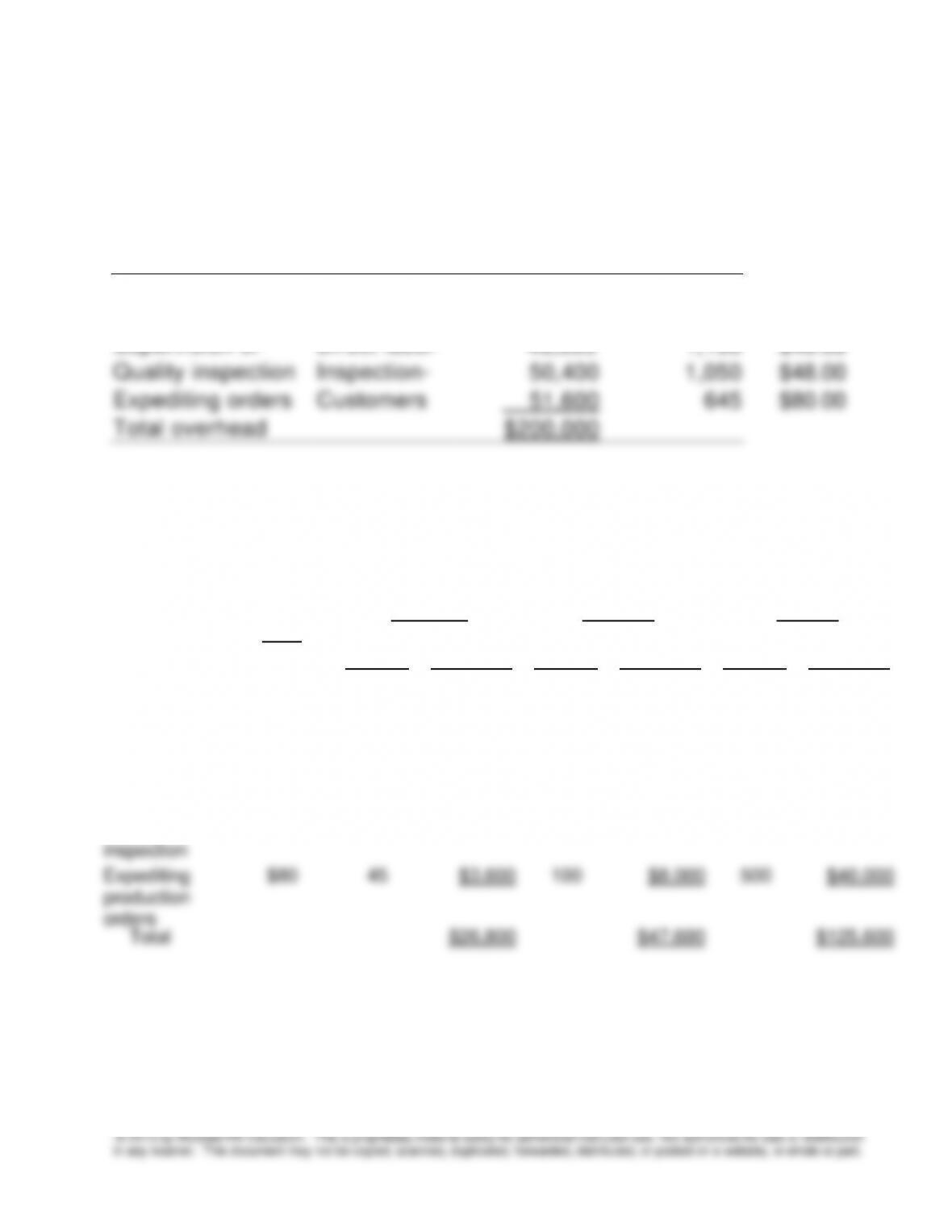

2. Overhead rates for Activity-Based Costing:

Activity

Cost Driver

Budgeted

Overhead

Cost

Budgeted

Cost Driver

Volume

Overhead

Rate

Machine setup

Setup hours

$ 16,000

1,600

$10.00

Plant management

Workers

36,000

1,200

$30.00

Supervision of

Direct labor–

46,000

1,150

$40.00

Quality inspection

Inspection–

50,400

1,050

$48.00

Expediting orders

Customers

51,600

645

$80.00

Total overhead

$200,000

Overhead Costs Assigned to Products Using Activity-Based Costing:

Overhead

Rate

Diomycin

Homycin

Addolin

Driver

Volume

Applied

Overhead

Driver

Volume

Applied

Overhead

Driver

Volume

Applied

Overhead

Machine

setup

$10

200

$2,000

600

$6,000

800

$8,000

Plant

management

$30

200

$6,000

400

$12,000

600

$18,000

Supervision

of direct labor

$40

200

$8,000

300

$12,000

650

$26,000

Quality

inspection

$48

150

$7,200

200

$9,600

700

$33,600

Expediting

production

orders

$80

45

$3,600

100

$8,000

500

$40,000

Total

$26,800

$47,600

$125,600

5-49

5-50 (continued-2)

Cost per capsule under Activity-Based Costing:

Diomycin

Homycin

Addolin

Direct Materials

$205,000

$265,000

$258,000

Direct Labor

250,000

234,000

263,000

Overhead

26,800

47,600

125,600

Total Cost

$481,800

$546,600

$646,600

Packets produced

1,000,000

500,000

300,000

Cost per capsule

$0.4818

$1.0932

$2.1553

3. Comparison of Product Costs Using Current Costing and ABC Costing:

Diomycin

Homycin

Addolin

Current Costing System

Overhead

$90,000

$85,000

$25,000

Cost per capsule

$0.5450

$1.1680

$1.8200

Activity-Based Costing system

Overhead

$26,800

$47,600

$125,600

Cost per capsule

$0.4818

$1.0932

$2.1553

products “subsidize” low-volume products in this case. Because of lack of

detailed costing information, ADA ends up undercosting Addolin ($1.82

under the current costing) and overcosting Diomycin ($0.545 under the

current costing).

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-50

5-50 (continued-3)

Activity-based costing provides ADA with more detailed and better

estimates of product costs. For example by using ABC, ADA becomes

aware that the cost of Diomycin is lower ($0.4818 per capsule compared

to $0.545 under current costing), meaning that it can set the price of

Diomycin lower and be more competitive. Also, ABC revealed how costly

Addolin is ($2.1553 per capsule compared to $1.82 under the current

costing). Thus, this opportunity would allow ADA to properly price Addolin

or if it is not profitable, stop producing.

From the schedule, activity-based costing assigns more overhead to

the lower-volume Addolin because the production of Addolin requires

more setups, inspection, supervision, formulation and management. The

current direct-labor-hours based costing system failed to assign costs of

all activities. As a result, Diomycin and Homycin subsidized Addolin.

The production department at ADA also benefits under ABC. ABC

profits by focusing on the high-volume products.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-51

5-50 (continued-4)

4. Among major uses of ABC in the Pharmaceutical Industry are:

a. Strategic Use of ABC to Reduce Costs

One of the important ways companies develop competitive advantages

is to become a low-cost producer. Many companies in the

pharmaceutical industry have learned to use the information they have

gained from their costing systems to make substantial price cuts to

increase market share.

b. Use of ABC to Eliminate Low-Value-Added Costs

ABC can be used to identify and eliminate activities that add costs but

not value to the products in the pharmaceutical industry. A company

can eliminate low-value added activities and costs without reducing

can be computed and the information used in making informed

decisions. For example, some of the different channels of distribution

in the pharmaceutical industry are: grocery stores, convenience stores,

pharmacy shops, each having different activities. The cost of

alternative channels of distribution is useful to marketing managers

who make decisions about which channel to use.

d. Use of ABC to Make Better Pricing Decisions

ABC enables managers to make better pricing decisions by providing

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-52

5-51 Environmental Costing (30 minutes)

1. Social and customer pressures, along with regulatory requirements have

caused organizations’ environmental costs to rise over the past few decades.

Environmental cost accounting or just environmental accounting addresses

the limitations of conventional accounting methods by incorporating both direct

and less obvious costs associated with environmental sustainability.

2. Some of the obvious environmental costs include:

Materials, equipment, and labor costs that can be readily identified from the

general ledger of an organization.

Some of the “hidden” or less obvious costs include:

investors

3. Both ABC and ABM require a clear understanding of processes. Therefore,

the process analysis step will help managers better understand the scope of

an environmental sustainability initiative. Once the process is understood, the