Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–46

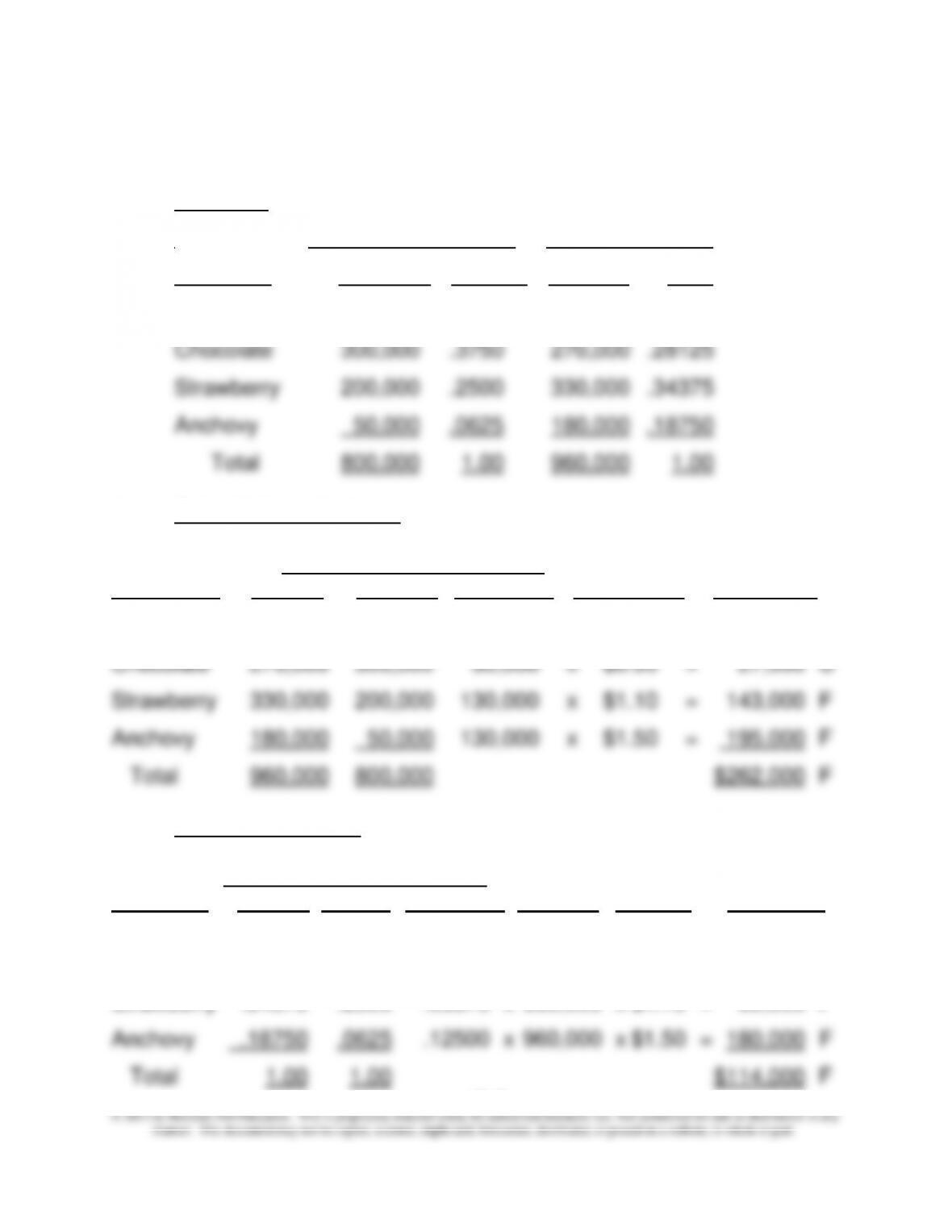

16–52 Sales Volume, Sales Quantity, and Sales Mix Variances (20 min)

Sales Mix

Budget Actual

Flavor Quantity Mix Quantity Mix

Vanilla 250,000 .3125 180,000 .18750

1. a. Sales Volume Variance

Budgeted Sales

Sales Quantity Contribution Volume

Flavor Actual Budget Difference Margin/Unit Variance

Vanilla 180,000 250,000 70,000 x $0.70 = $ 49,000 U

1. b. Sales Mix Variance

Total Budgeted Sales

Sales Mix Actual CM Mix

Flavor Actual Budget Difference Quantity per Unit Variance

Vanilla .18750 .3125 – .12500 x 960,000 x $ .70 = 84,000 U

Chocolate .28125 .3750 – .09375 x 960,000 x $ .90 = 81,000 U

Strawberry .34375 .2500 .09375 x 960,000 x $1.10 = 99,000 F

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–47

16-52 (continued –1)

1. c. Sales Quantity Variance

Budget Budgeted Sales

Sales Mix Sales CM Quantity

Flavor Actual Budget Difference Mix per Unit Variance

Vanilla 960,000 800,000 160,000 x .3125 x $0.70 = $35,000 F

Chocolate 960,000 800,000 160,000 x .3750 x $0.90 = 54,000 F

Recap

Sales Mix Sales Quantity Sales Volume

Flavor Variance Variance Variance

Vanilla $ 84,000 U + $ 35,000 F = $ 49,000 U

Chocolate 81,000 U + 54,000 F = 27,000 U

2. Overall, the firm has enjoyed a good year. The total sales

substantially exceed the budgeted amount (20%). The increases in

sales could have been a result of the increase of the entire market

size for ice cream and other competing merchandises. In any event,

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–48

16–52 (continued –2)

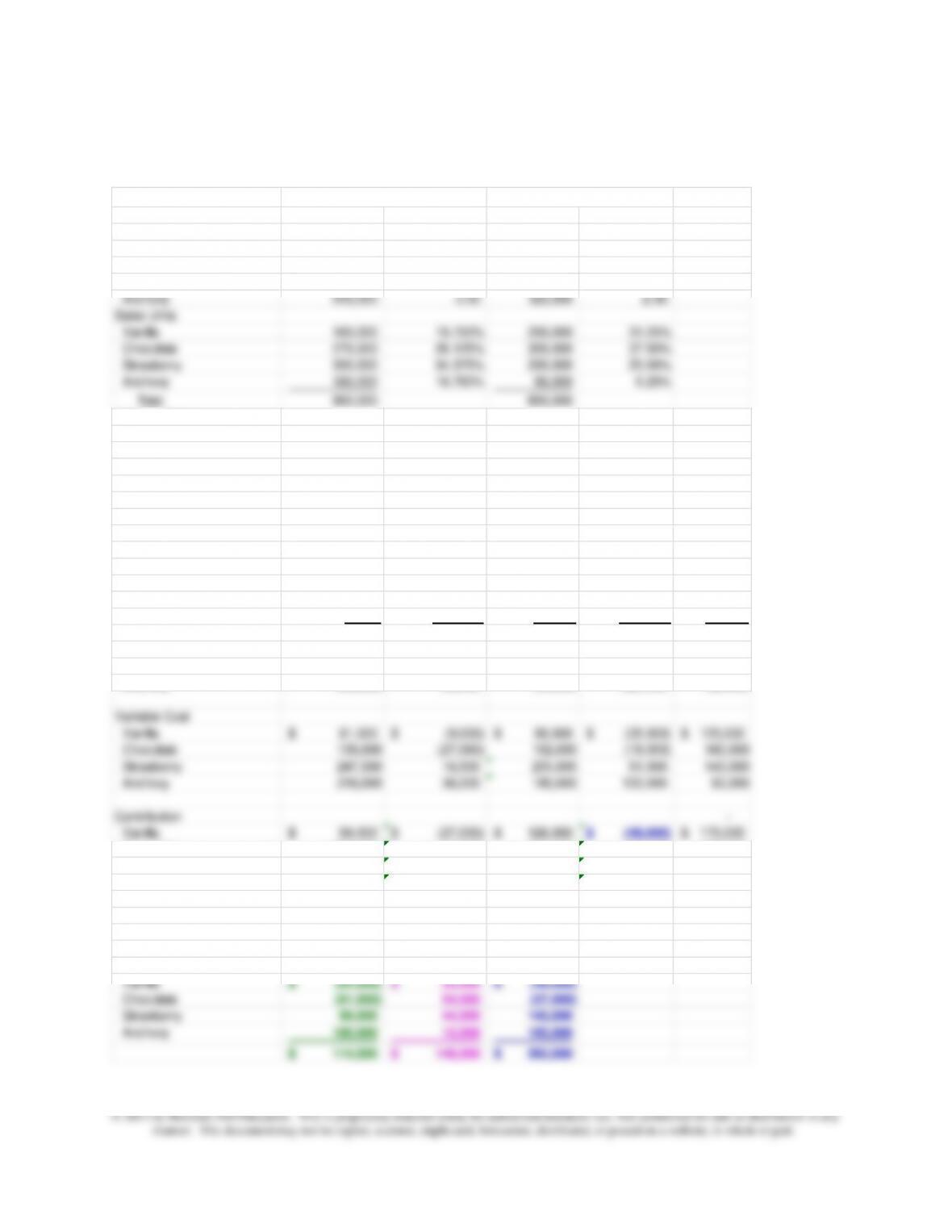

The spreadsheet solution for 16-52 is provided below:

Total per unit or % Total per unit or %

Sales

Vanilla 180,000$ 1.00$ 300,000$ 1.20$

Chocolate 364,500 1.35 450,000 1.50

Strawberry 660,000 2.00 360,000 1.80

Anchovy 540,000 3.00 125,000 2.50

Sales Units

Vanilla 180,000 18.750% 250,000 31.25%

Chocolate 270,000 28.125% 300,000 37.50%

Strawberry 330,000 34.375% 200,000 25.00%

Anchovy 180,000 18.750% 50,000 6.25%

Total 960,000 800,000

Variable Cost

Vanilla 81,000$ 0.45$ 125,000$ 0.50$

Chocolate 135,000 0.50 180,000 0.60

Sales Price Flexible Sales Volume

Sales Actual Variance Budget Variance Budget

Vanilla 180,000$ (36,000) $216,000 (84,000) 300,000$

Chocolate 364,500 (40,500) 405,000 (45,000) 450,000

Strawberry 660,000 66,000 594,000 234,000 360,000

Anchovy 540,000 90,000 450,000 325,000 125,000

Variable Cost

Vanilla 81,000$ (9,000)$ 90,000$ (35,000)$ 125,000$

Chocolate 135,000 (27,000) 162,000 (18,000) 180,000

Strawberry 247,500 16,500 231,000 91,000 140,000

Anchovy 216,000 36,000 180,000 130,000 50,000

Contribution –

Vanilla 99,000$ (27,000)$ 126,000$ (49,000)$ 175,000$

Chocolate 229,500 (13,500) 243,000 (27,000) 270,000

Strawberry 412,500 49,500 363,000 143,000 220,000

Strawberry 99,000 44,000 143,000

Anchovy 180,000 15,000 195,000

114,000$ 148,000$ 262,000$

Actual

Budget

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–49

16–53 Market Size and Market Share Variances (20 min)

1.

Selling price variance: ($.48 – $.52) x 69,120,000 =$2,764,800 U

Sales volume variance:

(69,120,000 – 80,000,000) x $.40 = 4,352,000 U

Total operating income variance $7,116,800 U

Total market size

Market size variance:

(1,440,000,000 – 1,600,000,000) x .05 x $.40 = 3,200,000 U

Total $4,352,000 U

2. The global risks for an airline include weather events, foreign currency

fluctuations, disruptions in political environments, terrorist activities (as in

the case in this problem), and changes in regulations from country to

country, among others. The airlines manage these risks by hedging

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–50

16–54 Market Size and Market Share Variances (15 min)

WS= Welcome Signs; BH= Birdhouses

1. Budget Actual (per month)____

Diane’s Designs Industry Share Diane’s Designs Industry Share

WS 50 3,000 1.6667% 45 3,000 1.5%

BH 25 200 12.5% 35 175 20%

2. Weighted Average Budgeted Contribution Margin Per Unit:

Budgeted contribution margin per unit for both products:

$240 75 = $3.20

3. Market size variance

Welcome Signs: (3,000 – 3,000) X 0.1 X $3.20 = $ 0

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–51

16–54 (continued –1)

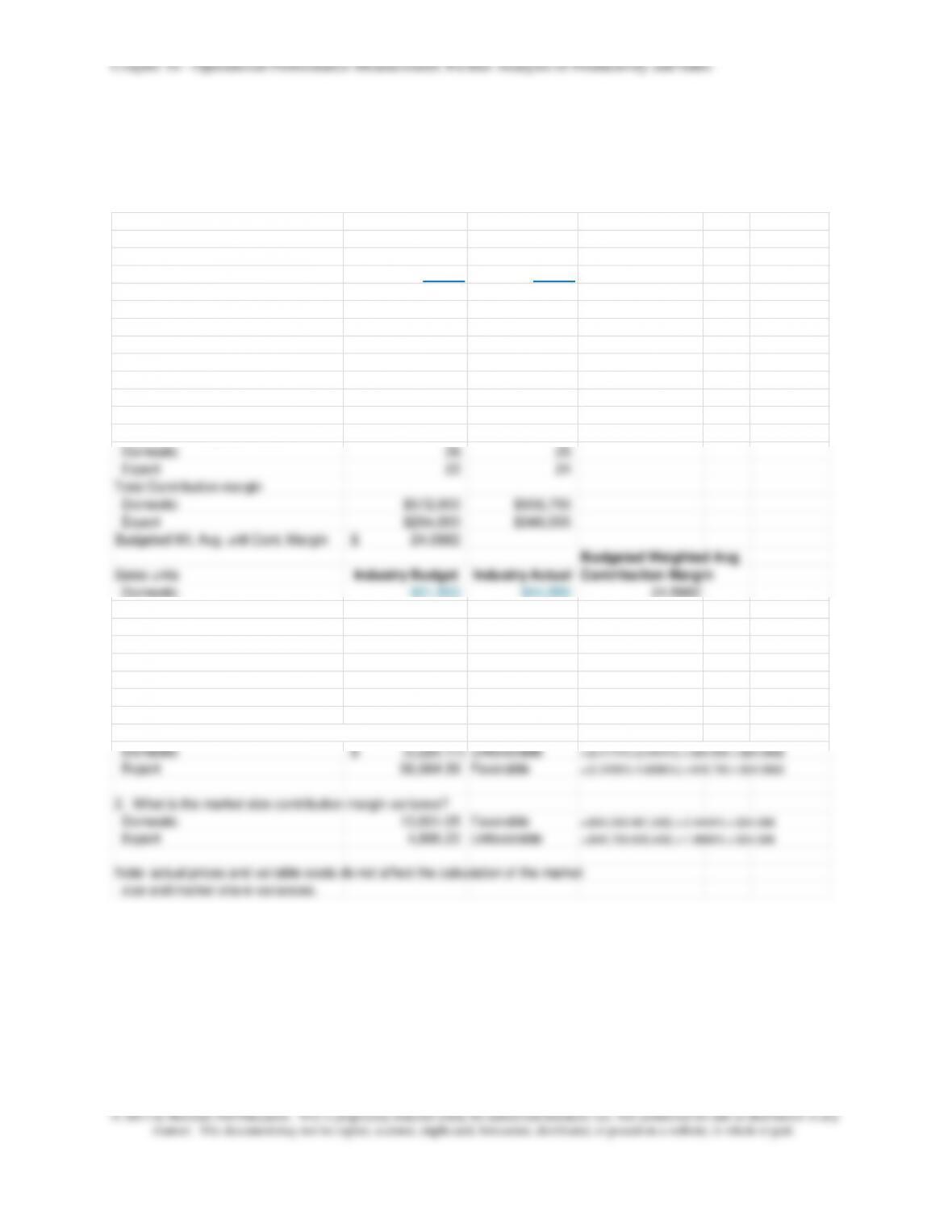

The spreadsheet solution for 16-54 is shown below

Budgeted

Budget Actual Wt Avg CM

Sales units

Welcome Signs 50 45

Birdhouses 25 35

Total 75 80

Total Contribution margin

Welcome Signs $110.00 $95.00 3.20$

Birdhouses 130.00 150.00

Sales units Industry Budget Industry Actual

Signs 3,000 3,000 per six month period

Birdhouses 200 175 per month

1. Market Share Budgeted Actual

Signs 1.6667% 1.50%

Birdhouses 12.50% 20.00%

2. What is the market share contribution margin variance?

Signs (16.00)$ Unfavorable

Birdhouses 42.00 Favorable

3. What is the market size contribution margin variance?

Signs –

Birdhouses (10.00) Unfavorable

16–52

16-55 Market Size and Market Share Variances; Foreign Currency

Fluctuations (20 min)

1.,2.

Budget Actual

Sales units (cases)

Domestic 22,000 22,350

Export 12,000 14,500

Total 34,000 36,850

Price per case

Domestic 88$ 87$

Export 90 92

Variable Cost per case

Domestic 62 62

Export 68 68

Contribution Margin per case

Domestic 26 25

Export 22 24

Total Contribution margin

Domestic $572,000 $558,750

Export $264,000 $348,000

Budgeted Wt. Avg. unit Cont. Margin 24.5882$

Budgeted Weighted Avg

Sales units Industry Budget Industry Actual Contribution Margin

Domestic 901,500 924,550 24.5882

Export 635,400 645,750

Currency: $/Euro 1.29$ 1.42$

Market Share Budgeted Actual

Domestic 2.4404% 2.4174%

Export 1.8886% 2.2455%

1. What is the market share contribution margin variance?

Domestic (5,225.17)$ Unfavorable =(2.4174%-2.4404%) x 924,550 x $24.5882

Export 56,664.39 Favorable =(2.2455%-1.8886%) x 645,750 x $24.5882

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–53

16–55 (continued –1)

3.

The unfavorable market share for the domestic market reflects the decline in

the company’s sales as the market increased; the unfavorable domestic

market share variance of $5,225 is more than offset by the favorable market

size variance of $13,831.

The very large favorable market share variance of $56,664 for the export

market reflects the large increase in exports due at least in part to the falling

able to retain some of its new foreign customers.

16–54

16-56 Comparative Income Statements and Sales Performance

Variances; Current to Prior Year (35 min)

1. Comparative Income Statement for 2013 based on the flexible

budget (Exhibit 16.15)

2013 2012

Sales Units 7,200 6,500

Sales Mix for each Product

Half Inch 50% 30%

One Inch 50% 70%

Price

Half Inch 12.00$ 14.00$

One Inch 36.00$ 32.00$

Variable Cost per Unit

Half Inch 6.00$ 6.00$

One Inch 8.00$ 8.00$

Fixed cost 35,000$ 35,000$

Sales Price Flexible Sales Volume

Sales January 2013 Variance Budget Variance December 2012

Half Inch 43,200$ (7,200)$ 50,400$ 23,100$ 27,300$

One Inch 129,600 14,400 115,200 (30,400) 145,600

Total Sales 172,800$ 7,200$ 165,600$ (7,300)$ 172,900

Less Variable Costs

Half Inch 21,600$ 21,600$ 9,900 11,700$

One Inch 28,800$ 28,800$ (7,600) 36,400$

Total Variable Costs 50,400$ 50,400$ 2,300 48,100$

Contribution

Half Inch 21,600 (7,200) 28,800 13,200 15,600

One Inch 100,800 14,400 86,400 (22,800) 109,200

Total Contribution 122,400 7,200 115,200 (9,600)$ 124,800

Less Fixed Costs 35,000 35,000

Operating Income 87,400$ 89,800$

Sales Mix Sales Quantity Volume

Variance Variance Variance

Half Inch 11,520.00$ 1,680.00$ 13,200.00$

One Inch (34,560.00) 11,760.00 (22,800.00)

(23,040.00)$ 13,440.00$ (9,600.00)$