Chapter 12 – Strategy and the Analysis of Capital Investments

12–91

12–58 MACRS Depreciation and Capital-Budgeting Analysis; Sensitivity Analysis;

Spreadsheet Application (60 minutes)

1. The estimated after-tax NPV of this proposed investment is ($66,917), as follows:

Net investment outlay, time 0:

Purchase cost $500,000

Remodeling cost (25 units × $20,000 per unit) $500,000

Net investment outlay $1,000,000

After-tax cash inflow per year:

Pre-tax rental revenue, $500 units = 15 units × $500 × 12 = $90,000

Pre-tax rental revenue, $650 units = 10 units × $650 × 12 = $78,000

$168,000

Less: Income taxes (@ 40%) = $67,200

After-tax rental revenue = $100,800

After-tax Cash Operating Expenses per Year:

Pre-tax expenses, $500 units ($90,000 × 0.16) = $14,400

Pre-tax expenses, $650 units ($78,000 × 0.16) = $12,480

NPV = ($66,917)

Note: the PV factor of 0.3372for 27.5-year residential rental property is given in the

problem, but can be calculated as follows:

PV27YR = [ (t * Dep%i)÷(1+r)i]÷100, where t = tax rate, Dep% = MACRS

depreciation rate (e.g., Exhibit 12.4), r = WACC (discount rate), and i = 1,

28.The MACRS depreciation rates for 27.5-year property must be

obtained outside the text (they are not disclosed in Exhibit 12.4.)

2. Sensitivity analysis:

a. If the discount rate were 8% (rather than 10%), the estimated NPV of the project is

now positive, as follows:

MACRS depreciation rates÷12-month period=100% ÷ 27.5 periods = 3.636%

MACRS depreciation per year, first 27 years = 3.636%

12–92

12–58 (Continued-1)

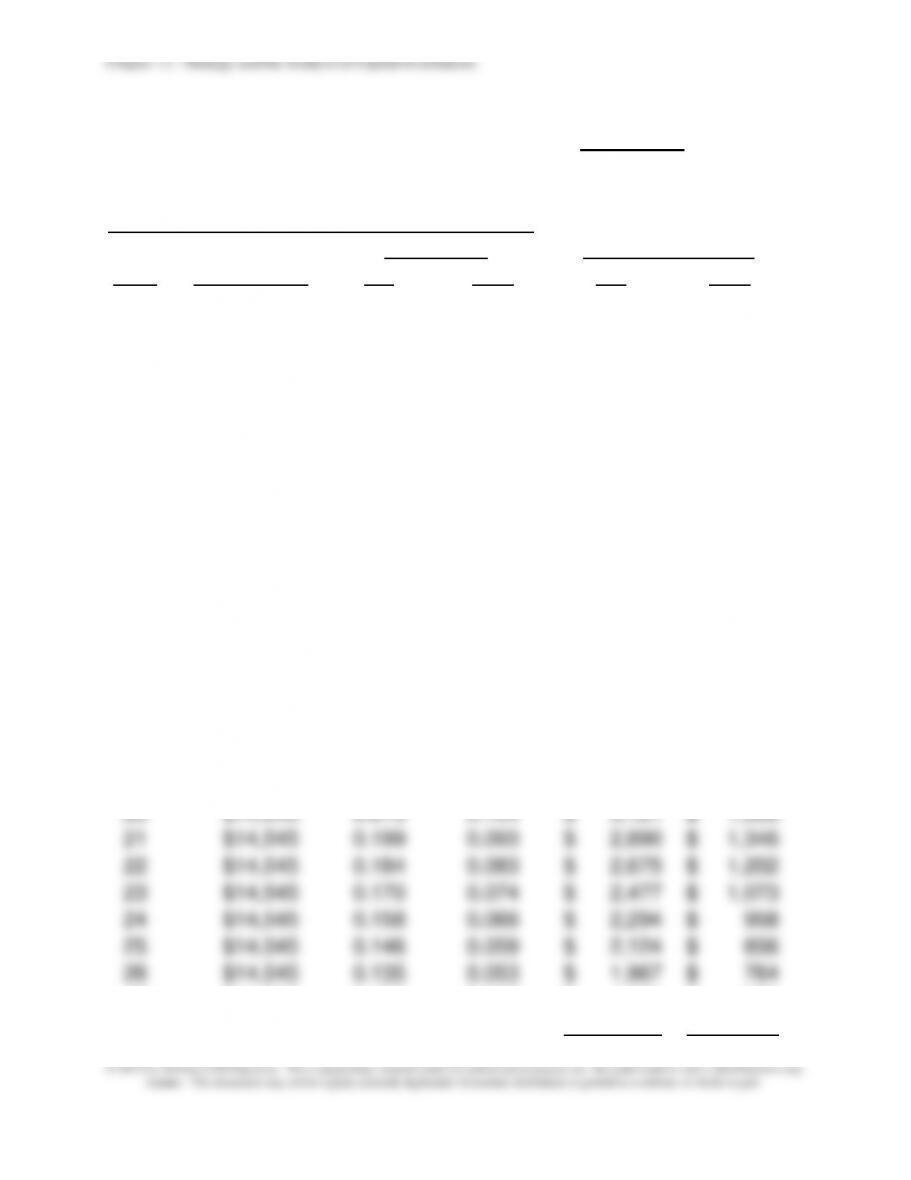

Tax Savings

MACRS annual depreciation, first 27 years = $36,364 $14,545

MACRS depreciation deduction, year 28 = $18,182 $7,273

Present Value of MACRS Depreciation Deductions

PV Factors

PV of Tax Savings

Year

Tax Savings

8%

12%

8%

12%

1

$14,545

0.926

0.893

$ 13,468

$ 12,987

2

$14,545

0.857

0.797

$ 12,470

$ 11,596

3

$14,545

0.794

0.712

$ 11,547

$ 10,353

4

$14,545

0.735

0.636

$ 10,691

$ 9,244

5

$14,545

0.681

0.567

$ 9,899

$ 8,253

6

$14,545

0.630

0.507

$ 9,166

$ 7,369

7

$14,545

0.583

0.452

$ 8,487

$ 6,580

8

$14,545

0.540

0.404

$ 7,858

$ 5,875

9

$14,545

0.500

0.361

$ 7,276

$ 5,245

10

$14,545

0.463

0.322

$ 6,737

$ 4,683

11

$14,545

0.429

0.287

$ 6,238

$ 4,181

12

$14,545

0.397

0.257

$ 5,776

$ 3,733

13

$14,545

0.368

0.229

$ 5,348

$ 3,333

14

$14,545

0.340

0.205

$ 4,952

$ 2,976

15

$14,545

0.315

0.183

$ 4,585

$ 2,657

16

$14,545

0.292

0.163

$ 4,246

$ 2,373

17

$14,545

0.270

0.146

$ 3,931

$ 2,118

18

$14,545

0.250

0.130

$ 3,640

$ 1,891

19

$14,545

0.232

0.116

$ 3,370

$ 1,689

20

$14,545

0.215

0.104

$ 3,121

$ 1,508

21

$14,545

0.199

0.093

$ 2,890

$ 1,346

22

$14,545

0.184

0.083

$ 2,675

$ 1,202

23

$14,545

0.170

0.074

$ 2,477

$ 1,073

24

$14,545

0.158

0.066

$ 2,294

$ 958

25

$14,545

0.146

0.059

$ 2,124

$ 856

26

$14,545

0.135

0.053

$ 1,967

$ 764

27

$14,545

0.125

0.047

$ 1,821

$ 682

28

$7,273

0.116

0.042

$ 843

$ 305

12–93

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

SUM = $ 159,900 $ 115,833

12–58 (Continued-2)

Alternatively:

a) For 8%: ($14,545 × 10.935) + (0.116 × $7,273) = $159,900

b) For 12%: ($14,545 × 7.943) + (0.042 × $7,273) = $115,833

Estimated NPV of Proposed Investment (@ 8% discount rate):

Net initial investment outlay, time 0 = ($1,000,000)

Plus: PV of after-tax rental revenues (11.258 × $100,800) = $1,134,806

Plus: PV of MACRS depreciation tax savings (see above) = $159,900

Less: PV of after-tax cash operating expenses

Summary:

Discount Rate NPV

8.00% $113,137

10.00% ($66,917)

12.00% ($202,134)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–94

3. Additional factors to be considered before investing in the apartment complex:

• Alternative investment opportunities (rather than the proposed investment)?

• Sensitivity of investment decision (i.e., accept or reject) with respect to:

o Volume (occupancy) assumption?

12–95

12-59 Environmental Cost Management (60 minutes)

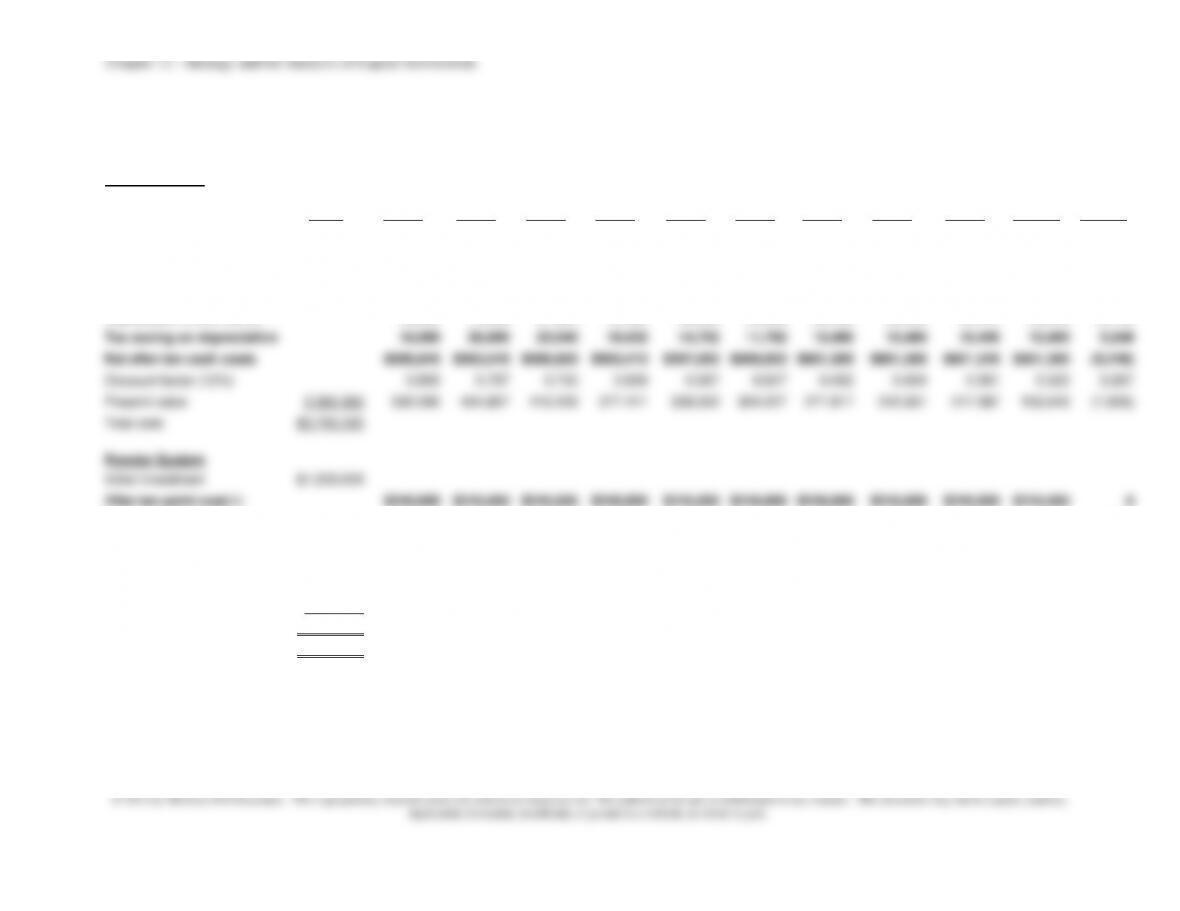

1.

Solvent System

Present

Value

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Year 11

Initial investment

$400,000

After-tax paint cost (1)

$228,000

$228,000

$228,000

$228,000

$228,000

$228,000

$228,000

$228,000

$228,000

$228,000

0

After-tax environ. costs (3)

$383,845

$383,845

$383,845

$383,845

$383,845

$383,845

$383,845

$383,845

$383,845

$383,845

Total after-tax cash costs

$611,845

$611,845

$611,845

$611,845

$611,845

$611,845

$611,845

$611,845

$611,845

$611,845

Depreciation (MACRS) (2)

40,000

72,000

57,600

46,080

36,880

29,480

26,200

26,200

26,240

26,200

13,120

Tax saving on depreciation

16,000

28,800

23,040

18,432

14,752

11,792

10,480

10,480

10,496

10,480

5,248

Net after-tax cash costs

$595,845

$583,045

$588,805

$593,413

$597,093

$600,053

$601,365

$601,365

$601,349

$601,365

(5,248)

Discount factor (12%)

0.893

0.797

0.712

0.636

0.567

0.507

0.452

0.404

0.361

0.322

0.287

Present value

3,360,365

532,090

464,867

419,229

377,411

338,552

304,227

271,817

242,951

217,087

193,640

(1,506)

Total cost

$3,760,365

Powder System

Initial investment

$1,200,000

After-tax paint cost(4)

$240,000

$240,000

$240,000

$240,000

$240,000

$240,000

$240,000

$240,000

$240,000

$240,000

0

Depreciation (MACRS)

120,000

216,000

172,800

138,240

110,640

88,440

78,600

78,600

78,720

78,600

39,360

Tax saving on depreciation

48,000

86,400

69,120

55,296

44,256

35,376

31,440

31,440

31,488

31,440

15,744

Net after-tax cash costs

192,000

153,600

170,880

184,704

195,744

204,624

208,560

208,560

208,512

208,560

(15,744)

Discount factor (12%)

0.893

0.797

0.712

0.636

0.567

0.507

0.452

0.404

0.361

0.322

0.287

PV

1,064,182

171,456

122,419

121,667

117,472

110,987

103,744

94,269

84,258

75,273

67,156

(4,519)

Total cost

$2,264,182

Difference in total cost

$1,496,183

Chapter 12 – Strategy and the Analysis of Capital Investments

12–96

12–59 (Continued)

Notes:

(1) Annual after-tax paint cost, solvent system = $0.19/unit × 2,000,000 units/year

× (1 − 0.40) = $228,000.

(2) MACRS depreciation rates, 10-year property (from text Exhibit 12.4):

Year

Rate

1

10.00%

2

18.00%

3

14.40%

4

11.52%

5

9.22%

* First year switching to SL method

(3) Additional environmental costs, Solvent Paint System:

Wastewater treatment

50,000

Pre-tax Total

After-tax environmental costs

(4) Annual after-tax paint cost, Powder Paint System = $0.20/unit × 2,000,000

units/year × (1 − 0.40) = $240,000.

2. Based solely on financial considerations, the maximum the company should spend

on the Powder-Based System = original estimate + difference in PVs of costs (from

Year

Rate

6

7.37%

7

6.55%*

8

6.55%

9

6.56%

10

6.55%

11

3.28%

Item

Annual Cost

Pit cleaning

$12,000

Waste disposal

549,000

Superfund Fee

3,177

Worker training

3,000

Insurance

10,000

Amortization of air-emission permit

200

Air-emission fee

1,115

Recordkeeping

11,250

Chapter 12 – Strategy and the Analysis of Capital Investments

12–97

12-60 Research Assignment, Strategy (50-60 Minutes)

This assignment pertains to the following article: Clayton M. Christensen, Stephen P.

Kaufman, and Willy C. Shih, “Innovation Killers: How Financial Tools Destroy Your

Capacity to Do New Things,” Harvard Business Review (January 2008), pp. 98-105.

The article focuses on bias against innovation that is attributable to the misuse of

certain financial tools. In fact, they conclude (p. 104) that “managers in established

corporations use analytical methods that make innovation investments extremely

difficult to justify.” The authors point to the following three “misguided applications” of

financial tools: (1) discounted cash flow (DCF) and net present value (NPV) to evaluate

away from investments whose payoff lies beyond the immediate horizon.

1. According to the authors of the article, how does the use of DCF tools by

managers in practice bias against innovation? What solution do the authors

propose to counter this problem?

While not disputing the underlying mathematics of the discounting process that lies at

the heart of DCF methods such as NPV, the authors assert two implementation errors

on the part of decision-makers:

(1) The “DCF Trap:” some analysts (erroneously) assume a status quo competitive

position in their analysis of an investment project. That is, they extrapolate the

current market share and profitability of the company, without recognizing the

potential for erosion of both over time as competitors invest. As the authors state,

“In most situations, competitors’ sustaining and disruptive investments over time

Answering this question entails assessing the projected value of the innovation

against a range of scenarios, the most realistic of which is often a deteriorating

competitive and financial future.

Chapter 12 – Strategy and the Analysis of Capital Investments

12–98

12–60 (Continued-1)

(2) Errors of estimation. The authors assert that in practice many managers, as a

way to recognize the inherent uncertainties associated with distant cash flows,

simply assume a terminal value at a certain point in the project’s life. That is, all

cash flows beyond this (near-term) point in a project’s life is embodied in a single

amount, called the project’s “terminal value.” (This terminal value is often

estimated as the present value, at the terminal point, of the stream of future cash

cash inflows (because the future stream, to infinity, is a function of the assumed

near-term cash inflows), and (2) the method fails to incorporate the declining

competitive situation discussed above in point #1.

2. Define the terms “fixed costs” and “sunk costs.” According to the authors of

this article, what is the bias against innovation that is created by how some

decision-makers view such costs? What remedies do the authors recommend

for dealing with this problem?

(a) “Fixed costs” are defined as those costs that in the short run do not vary in

response to an underlying activity variable or cost driver. These costs are also

referred to as “capacity–related” costs, since they provide a certain amount of

(b) In terms of assessing “innovation projects,” the authors suggest that in practice

some managers err by assuming that the current levels of fixed costs are adequate to

support the new investment. In their words, these managers assume that “capabilities

required for yesterday’s success are adequate for tomorrow’s as well.” The example

of Nucor and USX steel companies can be used here to more forcefully illustrate the

underlying error of logic regarding the adequacy of current levels of investment in