Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-1

CHAPTER 7:

COST ALLOCATION: DEPARTMENTS, JOINT PRODUCTS,

AND BY-PRODUCTS

QUESTIONS

7-1 The four objectives in the strategic role of cost allocation are to achieve effective

cost management through methods which:

1. Determine accurate departmental and product costs as a basis for evaluation

the performance of the department or profitability of the product.

2. Motivate managers to exert a high level of effort to achieve the goals of top

7-2 Joint products and by-products are derived from processing a single input or a

common set of inputs. Joint products are products from the same production

classified as by-products.

7-3 Reciprocal service flows are the service flows between service departments in

departmental allocation. These flows are ignored in the direct method, they are

7-4 There are three methods for departmental cost allocation: the direct method, the

step method, and the reciprocal method.

The direct method of cost allocation is done by taking the service

department flows to production departments only and determining each

production department’s share of that service.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-2

7-5 The three phases of departmental cost allocation, which apply for each of the

three methods (Question 7-4) are:

1. The initial allocation of all production and service costs to departments

2. The allocation of service department costs to production departments

3. The allocation of costs of production departments to products

The first phase in departmental cost allocation has two parts: to trace the direct

manufacturing costs in the plant to each service and production department that

service departments. These are often called reciprocal flows.

The third phase is to take the costs accumulated in the producing departments

and to allocate these costs to the final cost objects⎯the products or services.

7-6 There are a number of possible answers here. The chapter gives an example of

the use of departmental cost allocation in the banking industry. Other examples

would include cost allocation in an electric utility company to provide a basis for

use cost allocation to allocate the cost of the bank’s various internal departments

to the services provided by the bank, as a basis for setting fees and for

assessing the profitability of the services.

7-7 There are four methods for by-product costing:

The two asset recognition methods are:

Method 1 – Net Realizable Value Method. This method shows the net

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-3

The two revenue methods are:

Method 3 – Other Income at Selling Point Method. The net sales revenue

from a by-product sold at time of sale is shown in the income statement as an

other income or other sales revenue item.

Method 4 – Manufacturing Cost Reduction at Selling Point Method. The

Asset recognition methods are based on the financial accounting concepts of

asset recognition, matching, and materiality. By-products are recognized as

assets with probable future economic benefits since there is a market for them.

Asset recognition methods also have the preferred effect of matching the value of

the by-product with its manufacturing cost.

7-8 and,

7-9 There are a number of limitations and implementation issues to consider when

using either joint cost allocation or departmental cost allocation.

One issue is that it is often difficult to determine an appropriate allocation

the allocation, can help to reduce the effects in (a) and (b). Also, regarding (c),

to motivate managers to be efficient, and to make the right decisions, the

allocation in this case should be based on the cost to each department if it were

to obtain the service from outside the firm.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-4

7-10 A number of ethical issues are important when implementing cost allocation

methods. First, there are ethical issues when cost allocation is used in a situation

where the products or services are produced for both a competitive market and

for a public agency or government which is paying on a cost-plus basis. There is

an incentive for the provider to allocate an unfairly high portion of joint costs to

the cost-plus customer.

A second issue is the equity or “fair share” issue that arises when a

of taxes paid in the U.S. and the foreign country. Firms can reduce their world–

wide tax liability by increasing the costs of products purchased in high tax

countries, or countries where the firm does not have favorable tax treatment. For

this reason, international tax authorities watch closely the cost allocation

methods used by multinational firms.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-5

BRIEF EXERCISES

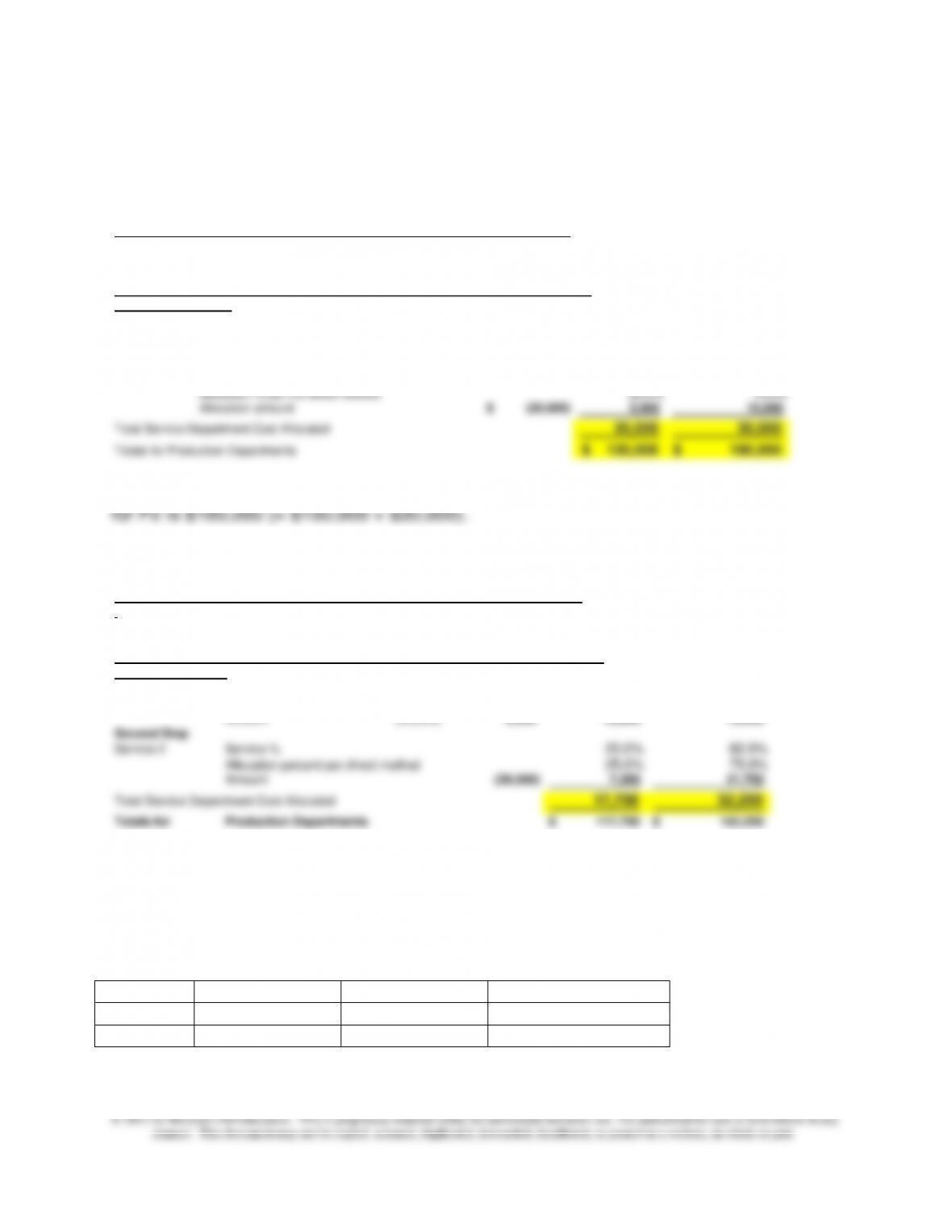

7-11

Total cost allocated to P1 is $20,000 and to P2 is $30,000

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

30,000$ 20,000$ 100,000$ 150,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Service 1 Service % to producing departments 35.0% 35.0%

Allocation % per the direct method 50.0% 50.0%

Allocation amount

(30,000)$ 15,000$ 15,000$

Service 2 Service % to producing departments 20.0% 60.0%

Allocation % per the direct method 25.0% 75.0%

Allocation amount (20,000)$ 5,000 15,000

Total Service Department Cost Allocated

20,000 30,000

Totals for Production Departments

120,000$ 180,000$

7-12 See 7-11 above, the total for P1 is $120,000 (= $100,000+$20,000), and the total

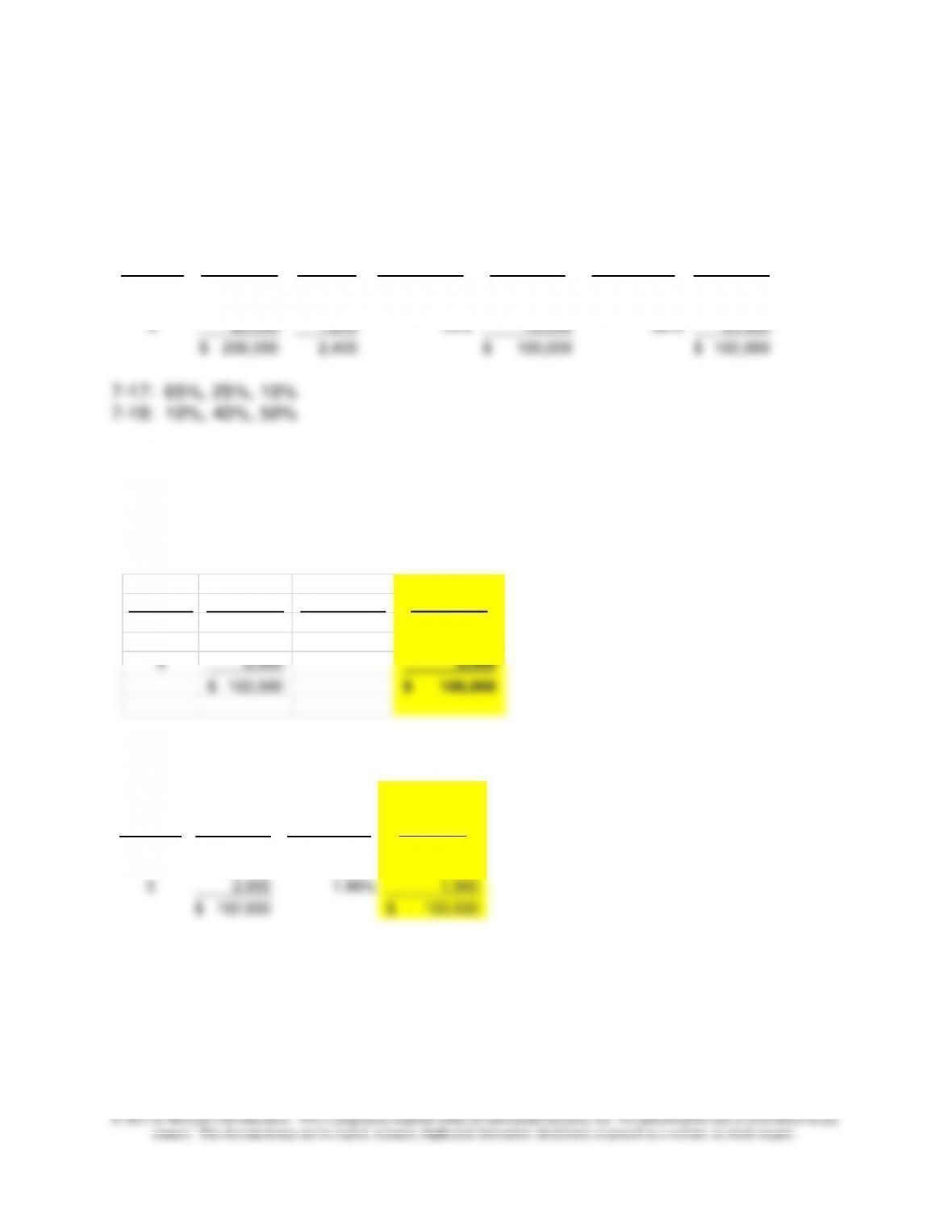

7-13

Total cost allocated to P1 is $17,750 and to P2 is $32,250

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

30,000 20,000 100,000 150,000

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Service 1 Service % 30.0% 35.0% 35.0%

Amount (30,000)

9,000 10,500 10,500

Second Step

Service 2 Service %

20.0% 60.0%

Allocation percent per direct method

25.0% 75.0%

Amount (29,000) 7,250 21,750

Total Service Department Cost Allocated

17,750 32,250

Totals for Production Departments 117,750$ 182,250$

7-14 There will be no change. The cost allocation is for service department cost (for S1

and S2); these costs are allocated to the production departments.

7-15, 16

Non Service %

P1

P2

S1

60%

40%/60% = 2/3

20%/60% = 1/3

S2

80%

40%/80% = 1/2

40%/80% = 1/2

for 7-15; 2/3 for P1 and 1/3 for P2

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-6

for 7-16 ½ for P1 and ½ for P2

7-17,18

The cost allocations are shown below.

7-19

First, the net realizable value of the by-product, $2,000 is reduced from the total joint

product cost; the by-product is inventoried at $2,000, and the remaining joint cost of

$98,000 is allocated to products 2 and 3 using the net realizable value method, as

follows:

7-20

Sales Value:

Sales Value Percent of Allocated

Product at Split-off Sales Value Joint Cost

1 50,000$ 49.02% 49,020$

2 50,000 49.02% 49,020

3 2,000 1.96% 1,960

102,000$ 100,000$

Sales Value: Units:

Sales Value Units at Percent of Allocated Percent of Allocated

Product at Split-off Split-off Sales Value Joint Cost Sales Units Joint Cost

1 130,000$ 240 65% 65,000$ 10% 10,000$

2 50,000 960 25% 25,000 40% 40,000

3 20,000 1,200 10% 10,000 50% 50,000

200,000$ 2,400 100,000$ 100,000$

Sales Value Percent of Allocated

Product at Split-off Sales Value Joint Cost

1 50,000$ 50.00% 49,000$

2 50,000 50.00% 49,000

3 2,000 2,000

102,000$ 100,000$

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-7

EXERCISES

7-21 Cost Allocation, General (15 min)

1. Service and administrative costs are costs that are incurred by

headquarters’ staffs or other central units. In order to maintain the

as administrative costs.

2. Homogeneous cost pools are collections of costs that are similar in

nature and have a presumed causal connection. Examples of

homogeneous pools include personnel-related costs, payroll-related

costs, space-related costs, and energy-related costs. A cost object

benefit from particular costs should share responsibility for these

costs. The “cause” criterion focuses on the cost objects that

precipitated the costs involved. The cause criterion is often applied to

service costs and allocates these costs to those units or cost objects

that gave rise to these costs.

b. The “ability to bear” criterion, which is similar in objective to

the benefit criterion, is based on the ability of the cost objects to cover

or absorb costs and allocates costs based on the profits of the cost

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-8

7-22 By-products and Decision Making (15 min)

Joe is considering a fruit-liquid, which is a by-product of the

processing for his jams and jellies, to produce a new product – a

coffee flavoring to complement his line of gourmet coffees. Joe is

correct in understanding that the production cost of jams and jellies is

selling costs.

The more critical consideration is the strategic issue: will the

new product line enhance the sales of coffees and the overall image

of Joe’s business as a high-end, quality gourmet business? Joe might

consider some form of consumer survey or marketing research to

determine whether the new product line would contribute as he

expects to the strategic competitive position of the firm.

7-9

7-23 Federal Reserve Banks; Cost Allocation (10 min)

By using an allocation method that resulted in lower costs being assigned

to the price-sensitive services, the FED was able to lower the full cost and,

therefore, the price of its most price-competitive services. As

demonstrated throughout this chapter, there are a number of alternative

see which one provides the best for their purposes; this is the approach

which should be considered unethical and inconsistent with the

management accountant’s code of ethics (see chapter 1).

Based on information in Ken S. Cavalluzzo, Christopher D. Ittner, and

David F. Larcker, “Competition, Efficiency, and Cost Allocation in

Government Agencies: Evidence on the Federal Reserve System,” Journal

of Accounting Research, Spring 1998, pp. 1–32;

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-10

7-24 Cost Allocation and Taxation at Nonprofit Organizations (10 min)

The nonprofit has an incentive to allocate a relatively large portion of the

common costs to the business activity to reduce taxes, but current

Treasury regulations require that the cost allocation be reasonable. This

has led some to argue that common costs should not be allocated in these

Treasury stance, which allows “reasonable” cost allocations.

Based on an article by Richard Sansing, “The Unrelated Business Income

Tax, Cost Allocation, and Productive Efficiency,” National Tax Journal,

June 1998, pp. 291–302.

7-11

7-25 Fuel Surcharges: Allocating the Increased Cost of Fuel (20

min)

1.,2.

The rising cost of fuel has affected many industries, but particularly

those in the transportation industries. In air freight, trucking, and

railroads, the surcharges can be as high as 35% of average charges.

The surcharges can be a substantial portion of total revenues for

these firms. The practice of fuel surcharges has grown widely to

include many service firms, involving most types of deliveries of

products or services (florists, retailers, appliance repair, and many

others). Unfortunately, many of these surcharges do not seem to be

reduced or removed when fuel prices fall, as they did during fall of

2008.

The issue of surcharges for railroads has been a contentious

one for the shippers and railroads. There have been several law

suits regarding the conflicts and currently several of the largest U.S.

railroads are subject to a suit charging price fixing regarding their use

of surcharges. The railroads’ attempt to have the suit dismissed

recently failed in U.S. courts (https://ecf.dcd.uscourts.gov/cgi-

bin/show_public_doc?2007mc0489-138). Apparently the STB ruling in

January 2007 was ineffective in resolving the surcharge issue for the

railroads and shippers. One reason it may have failed is that it

did not provide clear guidance regarding what would be an

acceptable method for cost allocation. The shippers’ suggestion for

miles traveled is probably closer to a basis that would recover actual

fuel cost increases. Also, one might consider an allocation that is

based on both miles and weight of product shipped. The goal is to

find the causal link between the use of fuel and the railroads’ service

to the shipper.

The litigation is on-going, as of December 2011.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-12

7-25 (continued –1)

3. The sustainability issue arises in the case of rail transport because

rail transport is more efficient than truck transport. A shipper that

has the option between the two methods of transport should

Based on: Christine Hauser, “Shippers May Raise Fuel Fees,” The

New York Times, April 26, 2011; Mina Kimes, “Railroads: Cartel or

Free Market Success Story?” Fortune, September 26, 2011; John D.

Schultz, “Fuel Surcharge Lawsuits: Antitrust Fines Growing,” Logistics

Management, July 1, 2008;Gargi Chakrabarty, “Many Businesses in

no Hurry to Pass on Savings,” Rocky Mountain News, October 31,

2008.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-13

7-26 Cost Allocation and Legal Disputes (30 Min)

The actual case is based on a dispute between the Department of Health

and Family Services (DHFS) of the State of Wisconsin and St. Francis

Home in the Park (the nursing home). The judgments shown below are by

the State of Wisconsin Court of Appeals, dated March 23, 1999. The full

explanation of the case is at the following site:

http://caselaw.lp.findlaw.com/scripts/getcase.pl?court=wi&vol=wisctapp2%5C1q99%5C

98-0986&invol=1

1. The court determined that further documentation was not required,

but that the stated reason for charging these items to the nursing

home is persuasive, and that further, DHFS had not shown that it had

asked NCI for the documentation. The specific assignment of these

costs to the nursing home was therefore allowed.

2. The court determined that DHFS had “no substantial basis” for

disallowing the direct assignment of the nourishment costs to the

meal production.” The court concluded that DHFS had no

substantial basis to disallow the method used by NCI.

5. The argument that NCI competes in the same manner (cost

leadership) for both the nursing home and the apartment-retirement

home is arguable. Is there evidence that the retirement home is a

cost competitive business? Also, it is not clear how the argument has

anything to do with the issue of cost allocation.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-14

7-27 Cost Allocation; Cost Shifting (15 min)

1. The cost-shifting in this case is from the airlines (that experience

lower costs of baggage handling) to TSA (that experience a larger

number of “carry–on” bags to examine) and to the airline passengers

(who experience the discomfort of increased time in going through

survive in a difficult competitive and economic environment.

Passengers’ views are likely to be mixed, with many frustrated by the

new charges and delays, and others seeking low air fares.

3. Given the emphasis airline customers place on price, air travel has

become somewhat of a commodity. It is hard to differentiate the

different carriers. The “fees for services” approach is consistent with

this strategy as it keeps ticket prices low for those who want to avoid

the fees, and it effectively shifts some of the airlines costs to TSA.

Source: See Real World Focus “Commodities, Globalization and Cost

Leadership,” in Chapter 1. Also, Christine Negroni, “More Fees, More

Carry-Ons,” The New York Times, March 29, 2011, p B4; Michelle Higgins,

“Elite for a Day, In Coach for a Fee,” The New York Times, September 4,

2011.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-15

7-28 Departmental Cost Allocation (25 min)

1. The Direct Method

Net service to both Production Departments (Advertising and Sales)

for the Actuarial Service Dept:

100% – 80% = 20%

Advertising Department share: 10%/20% = .5

Sales Department share: 10%/20% = .5

Net Service to both Production Departments for Premium

Department:

Advertising

Department

Sales Department

Actuarial Department

cost allocation

$80,000 x .5 = $40,000

$80,000 x .5 = $40,000

Premium Department

cost allocation

$15,000 x .25 = $3,750

$15,000 x .75 =

$11,250

Add: Initial Production

Dept. Costs

$60,000

$40,000

Total Cost for Each

Production Dept.

$103,750

$91,250

2. Step Method