1) in the current year, becker sofa company expected to sell 12,000 leather sofas. fixed

costs for the year were expected to be $8,400,000; unit sales price was budgeted at

$4,600; and unit variable costs were expected to be $2,200.

becker sofa company’s margin of safety (mos) in sales dollars is:

a.$36,200,000

b.$42,600,000

c.$33,300,000

d.$46,700,000

e.$39,100,000

2) management accountants are frequently asked to analyze various decision situations

including the following:

(1) alternative uses of plant space, to be considered in a make/buy decision.

(2) joint production costs incurred, to be considered in a sell-at-split-off versus a

process-further decision.

(3) research and development costs incurred in prior months, to be considered in a

product-introduction decision.

(4) the cost of a special device that is necessary if a special order is accepted.

(5) the cost of obsolete inventory to be considered in a keep-versus-disposal decision.

the costs described in situations 1 and 4 above are:

a.prime costs

b.sunk costs

c.discretionary costs

d.relevant costs

e.fully-absorbed costs

3) the focal point in budgeting for a service organization is likely to be:

a.capital assets acquisition

b.raw material utilization

c.human resource (i.e., personnel) planning

d.cost minimization

e.the process of mission development and goal specification

4) critics (e.g., the beyond budgeting roundtable) of traditional budgeting assert that the

budgeting process:

a.reflects too much of a “bottom-up” process, which is costly and inefficient

b.puts too much pressure on individuals to attain the budget, at whatever cost

c.makes too much use of so-called linear compensation plans

d.unnecessarily incorporates excessive detail

5) prime cost and conversion cost share what common element of total cost?

a.direct labor

b.direct materials

c.variable overhead

d.fixed overhead

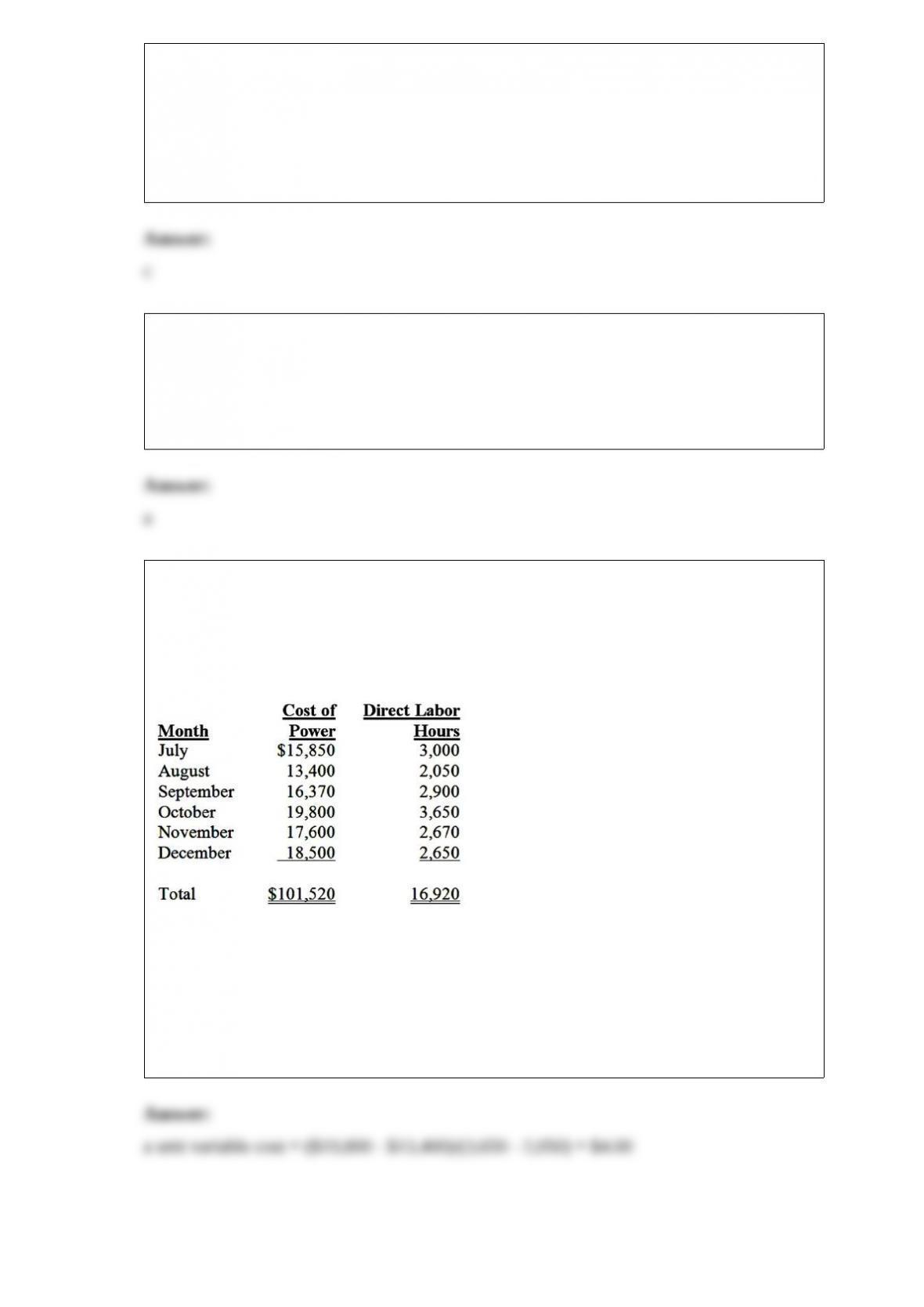

6) jackson, inc. is preparing a budget for the coming year and requires a breakdown of

the cost of electrical power used in its factory into the fixed and variable elements. the

following data on the cost of power used and direct labor hours worked are available for

the last six months of this year:

assuming that jackson uses the high-low method of analysis, the estimated variable cost

of steam per direct labor hour is:

a.$4.00

b.$5.42

c.$5.82

d.$6.00

7) the key difference between weighted-average and fifo process costing methods is the

handling of the partially completed:

a.beginning direct materials inventory

b.ending direct materials inventory

c.beginning work-in-process inventory

d.ending work-in-process inventory

e.beginning finished goods inventory

8) the general sales manager’s salary is an example of a:

a.customer unit-level cost

b.customer batch-level cost

c.customer-sustaining cost

d.distribution-channel cost

e.sales-level cost

9) brownsville novelty store prepared the following budget information for the month

of may:

sales are budgeted at $360,000. all sales are on account and a provision for bad debts is

made

monthly at three percent of sales.

inventory was $84,000 on april 30 and an increase of $12,000 is planned for may 31 .

all inventory is marked to sell at cost plus fifty percent.

estimated cash disbursements for selling and administrative expenses for the month are

$48,000.

depreciation for may is projected at $6,000.

brownsville’s budgeted operating income for may is:

a.$72,000

b.$66,000

c.$55,200

d.$61,200

e.$43,200

10) costs relevant to a make-versus-buy decision include variable manufacturing costs

as well as:

a.avoidable fixed costs

b.factory depreciation

c.unavoidable costs

d.property taxes on the manufacturing facility

e.factory administrative costs

11) when production levels are expected to decline within a relevant range, what effects

would be anticipated with respect to each of the following?

a.option a

b.option b

c.option c

d.option d

12) freight charges based on number of units shipped to customers is a:

a.customer unit-level cost

b.customer batch-level cost

c.customer-sustaining cost

d.distribution-channel cost

e.sales-level cost

13) a strategy map is:

a.a detailed flowchart outlining which firm managers are responsible for each

implementation of a firm’s strategy and when these implementations are to take place

b.a cause and effect diagram of the relationships among the balanced scorecard

perspectives to show how the achievement of critical success factors in each perspective

affects the achievement of goals in other perspectives and the overall financial

performance of the firm

c.a framework for the firm to achieve a desired organizational change in strategy while

mapping the successes of other firms within the industry

d.none of the above

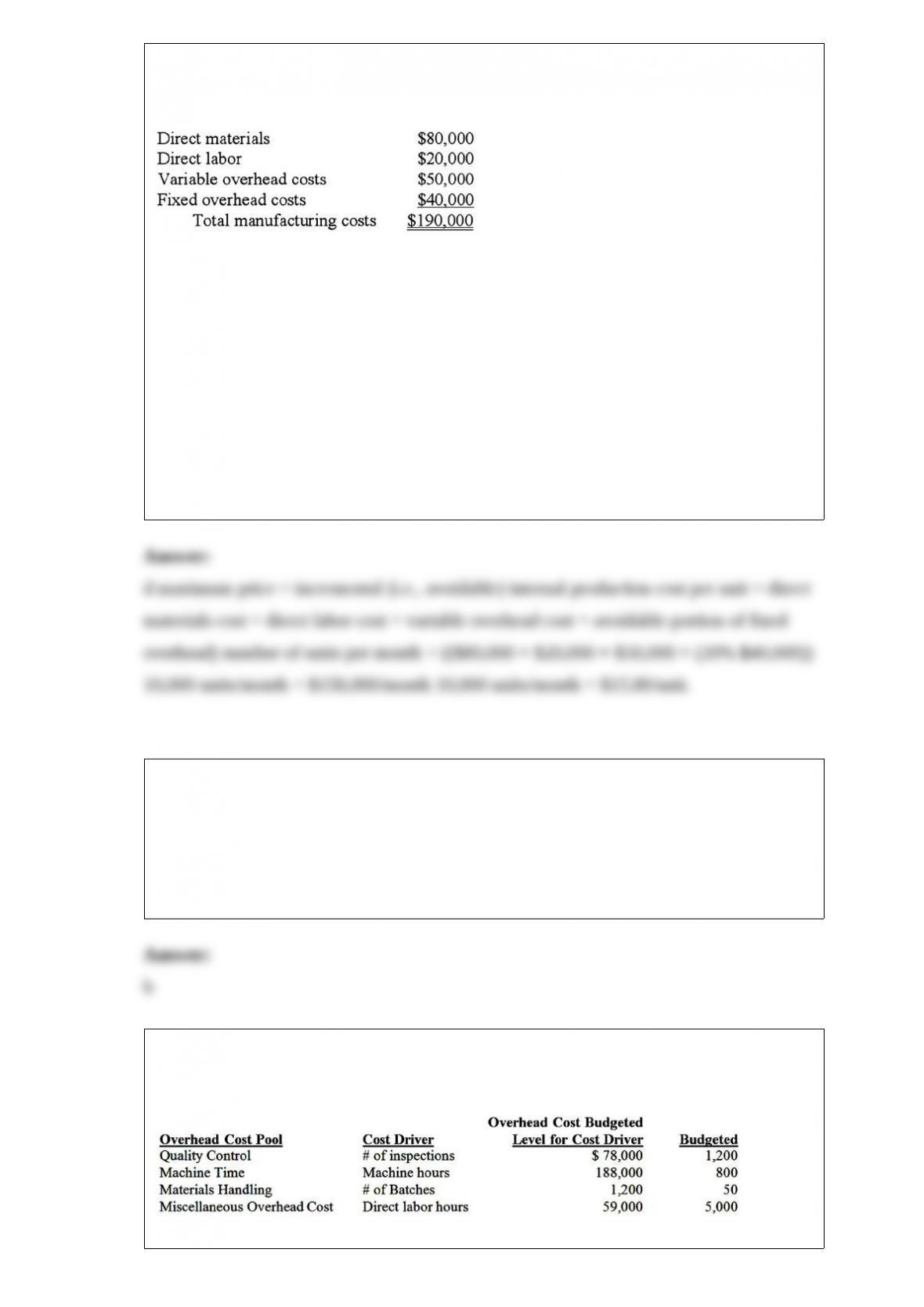

14) preston industries, inc. currently manufactures part qx100, which is used in several

products it produces. monthly production costs for 10,000 units of qx100 are as follows:

accounting has estimated that 20% of the fixed overhead costs assigned to qx100 would

not be needed if the company chose to purchase the part from an outside supplier.

preston has the option of purchasing the part from an outside supplier at $16.00 per

unit.

the maximum price that preston should be willing to pay the outside vendor for each

unit of qx100 is:

a.$10.00

b.$11.00

c.$15.00

d.$15.80

e.$16.00

15) if the usage of project activities is not proportional to the number of units produced,

then some managers will be overcharged and others undercharged under the:

a.activity-based costing

b.volume-based costing

c.overhead costing

d.process costing

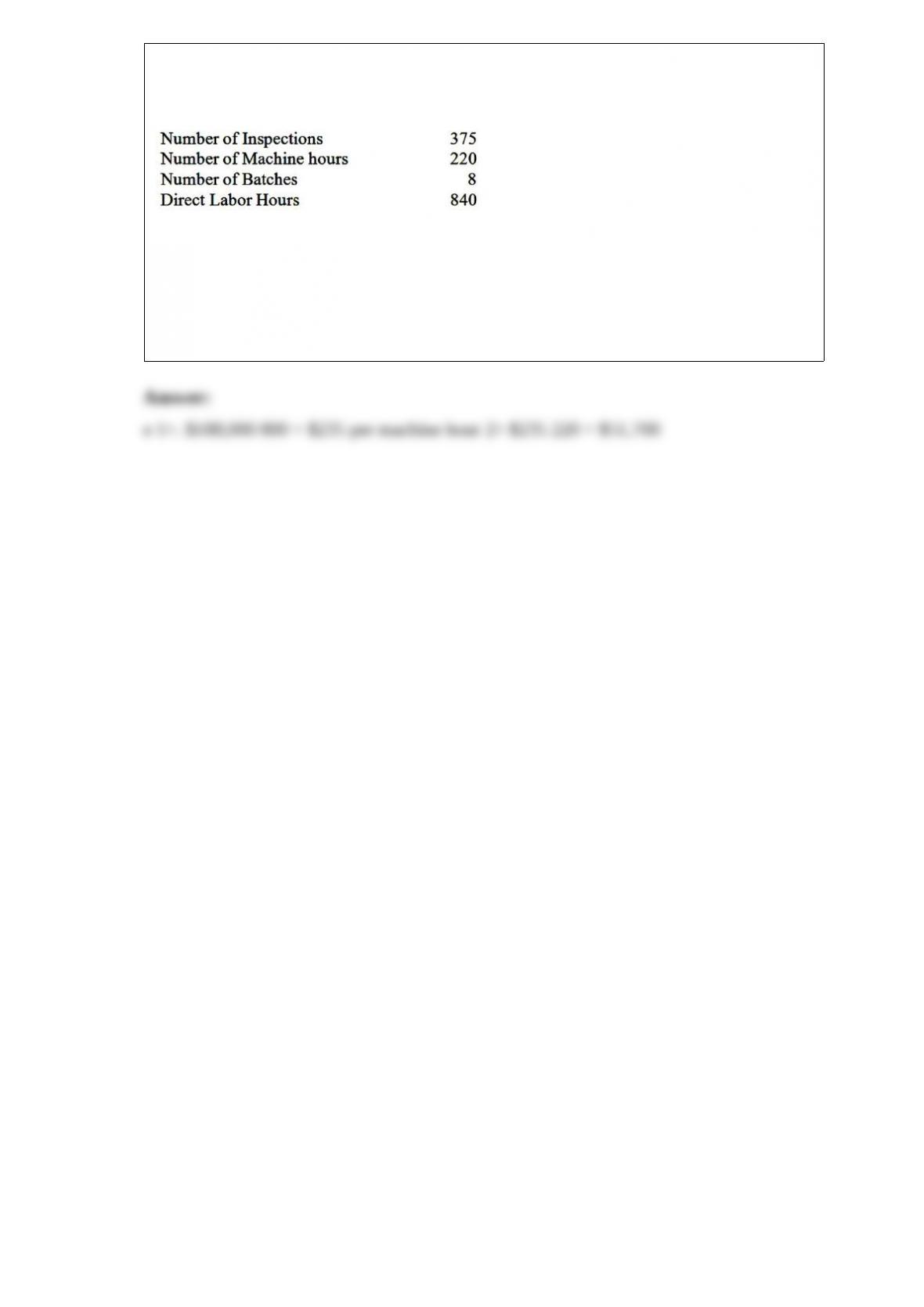

16) diamond cleats co. manufactures cleats for baseball shoes. it has outlined the

following overhead cost drivers:

diamond cleats co. has an order for cleats that has the following production

requirements:

using activity-based costing, applied machine overhead for the baseball cleat order is:

a.$47,800

b.$55,300

c.$40,500

d.$59,150

e.$51,700