Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-61

9-47 CVP Analysis, Activity-Based Costing (ABC) (30 min)

1. Total fixed overhead cost, including setup cost, is equal to $6,000,000 (i.e.,

$40/unit × 150,000 units).

Setup costs are $300 per setup (given). Under the current production plan

there are 3,000 setups, so total setup costs must be $900,000 (3,000 ×

$300).

Thus, the total fixed manufacturing costs for the current plan, other than

Therefore, under the current production plan, total variable costs per unit

are $59.50 (including setup costs), while under the proposed

manufacturing plan the variable cost per unit is $74.75 (including setup

costs), as follows:

Current Proposed

Materials and purchased parts $6.00 $15.00

Direct labor $12.50 $13.75

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-62

9-47 (Continued-1)

The ABC breakeven points can be determined as follows:

Current Plan

Proposed Plan

Contribution

Margin

$100 − $59.50 = $40.50

$100 − $74.75 = $25.25

Breakeven

points

($5,100,000 + $1,250,000) ÷

$40.50 = 156,790 units

($2,100,000+$1,250,000) ÷

$25.25 = 132,673 units

Breakeven

points,

exact

($5,100,000 + $1,250,000 +

[3,136 batches ×

$300/batch]) ÷ $46.50/unit =

$7,290,800 ÷ $46.50/unit =

156,792 units

($2,100,000 + $1,250,000

+ [2,654 batches ×

$300/batch]) ÷ $31.25/unit

= $4,146,200÷ $31.25/unit

=132,679 units

Notes:

1. In the “breakeven, exact” calculations above, total batch-level costs

are added to the numerator (at the rate of $300 per batch), while being

excluded from the denominator (i.e., $6/unit).

2. For the current plan, all batches but the last batch (#3,136) are of 50

units. Thus, under the current plan we would produce 3,135 batches @

50 units/batch = 156,750 units. Batch #3,136 would consist of 42 units,

3. Note that the breakeven point for the current manufacturing plan is

above the current operating level of 150,000 units. Also, since the

operating level of 150,000 is based on the assumption of 50 batches of

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-63

9-47 (Continued-2)

2. Contribution Income Statements, Exact Breakeven Points:

Current Proposed

Sales volume (in units) 156,792 132,679

Sales (at $100/unit) $15,679,200 $13,267,900

Less: Variable Costs(@ $53.50 and $68.75)

$8,388,372 $9,121,681

Contribution margin $7,290,828 $4,146,219

Less: Fixed costs

Manufacturing (other than batch-related) $5,100,000 $2,100,000

Batch-related fixed costs $940,800 $796,200

SG&A $1,250,000 $1,250,000

Total fixed costs $7,290,800 $4,146,200

Operating Income $28 $19

Note: the differences between the above-listed operating figures and $0

(breakeven point) are attributable to rounding up the exact breakeven

point to a whole number.

3. The ABC costing breakeven calculations do not differ much from that for

the volume-based calculations in Problem 9–46, and they both point to

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-64

9-48 Multiple-Product CVP Analysis; Sensitivity Analysis (75-90 min)

1. Contribution margin per unit = subscription price − variable costs

Weekly Subscriptions:

Mailing $0.60 per issue × 52 = $ 31.20 per subscription

Commission $ 3.00 per subscription

Administrative $ 1.50 per subscription

Monthly Subscriptions:

Mailing $0.60 per issue× 12 = $ 7.20 per subscription

Commission $ 3.00 per subscription

Administrative $ 1.50 per subscription

Total Variable Cost $11.70

cm per subscription = subscription price − variable cost

2. Contribution Margin Ratio (CMR) = cm per unit ÷ subscription price

Weekly: $11.30 ÷ $47.00 = 24.0%

Monthly: $ 7.30 ÷ $19.00 = 38.4%

3. Breakeven in total sales units (# of subscriptions)

Weighted-average cm per unit = ∑ (cm/unit)(weight)i, i = 1,2

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-48 (Continued-1)

Overall breakeven point = F ÷ weighted-average contribution margin/unit

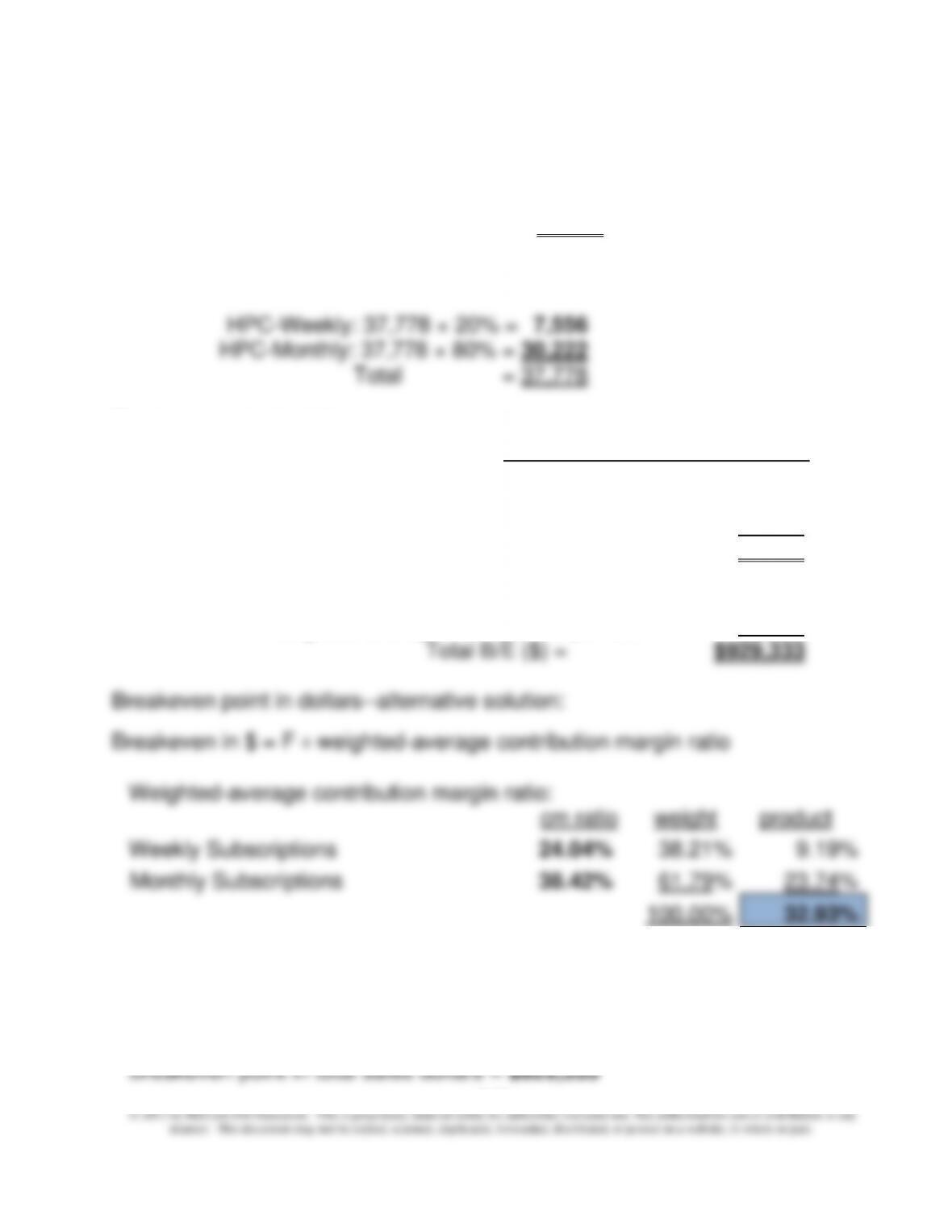

= $306,000 ÷ $8.10/subscription = 37,778 subscriptions

Breakdown into individual products:

Breakeven point in dollars:

Weight Selling Price Product

Wtd.-avg. selling price/unit:

Weekly Subscriptions 20% $47.00 $9.40

Monthly Subscriptions 80% $19.00 $15.20

100% $24.60

Breakeven ($):

Total breakeven units (subscriptions) 37,778

× weighted-average selling price per unit $24.60

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-66

9-48 (Continued-2)

Breakdown of sales, by product:

Sales mix, in terms of dollars: Sales Price Units Dollars

Weekly Subscriptions $47.00 7,556 $355,111

Monthly Subscriptions $19.00 30,222 $574,222

37,778 929,333

4. “For the multiproduct (or multiservice) firm, there is no breakeven point

independent of the sales mix assumption.”

One option for multiproduct CVP analysis is to trace and/or allocate total

fixed costs across the products and then prepare a separate CVP model for

each product. Regardless of the ability to allocate such costs across

products, this approach fails to capture demand interdependencies among

for the firm. In fact, there is an infinite number of breakeven points. As the

assumed sales mix changes, so too will the breakeven point for the firm.

The breakeven point moves in response to shifts in the sales mix: as the

mix shifts to more profitable products, the breakeven point decreases, and

vice versa. Thus, “for the multiproduct firm, there is no breakeven point

independent of the sales mix assumption.” The only exception to this rule is

when each product has the same contribution margin per unit, which is

considered a trivial case.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-67

9-48 (Continued-3)

5. Sensitivity analysis table: what happens to the breakeven point as the sales

mix changes (in increments of 1%), from 15% to 25% for HPC Weekly? Of

what value to management is this type of analysis?

Weighted-

Average

Contribution

Margin/Unit

B/E (units)

B/E %

Change from

Base Case

% Change in

Weighted-

Avg. CM/Unit

(from base)

$7.90

38,734

2.53%

-2.47%

$7.94

38,539

2.02%

-1.98%

$7.98

38,346

1.50%

-1.48%

$8.02

38,155

1.00%

-0.99%

$8.06

37,965

0.50%

-0.49%

$8.10

37,778

0.00%

0.00%

$8.14

37,592

-0.49%

0.49%

$8.18

37,408

-0.98%

0.99%

$8.22

37,226

-1.46%

1.48%

$8.26

37,046

-1.94%

1.98%

$8.30

36,867

-2.41%

2.47%

Sales Mix (based on units sold)

Weighted-

HPC Weekly

HPC Monthly

Avg. CM/Unit

15%

85%

$7.90

16%

84%

$7.94

17%

83%

$7.98

18%

82%

$8.02

19%

81%

$8.06

Base Case

20%

80%

$8.10

21%

79%

$8.14

22%

78%

$8.18

23%

77%

$8.22

24%

76%

$8.26

25%

75%

$8.30

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-68

9-48 (Continued-4)

The above data table provides the results of a sensitivity analysis.

Specifically, we are looking at the sensitivity of the breakeven point to the

assumption regarding sales mix for the two products. Based on the above

results management will form a judgment as to the sensitivity of the B/E

6. Given the assumed sales mix (20%:80%), the required sales volume (in total

units) to generate a before-tax profit, πB, of $ 75,000 is 47,037 units:

Targeted before-tax profit target, πB =

$75,000

Fixed Costs (F) =

$306,000

F + πB =

$381,000

Weighted-average cm/unit =

$8.10

Breakeven point in sales units =

47,037

Although not required in the problem, the breakdown by product is:

1) 20% × 47,037 = 9,407

2) 80% × 47,037 = 37,630

7. Given the assumed sales mix, what is the required sales volume (in total

units) to generate an after-tax profit, πA, equal to 10% of sales dollars?

Let Q = the required sales volume (in units) to achieve the profit objective

πB= Total sales − Total variable cost − Total fixed cost (F)

πB = πA ÷ (1 − t), where t = tax rate

πA ÷ (1 − t) = Total sales − Total variable cost − F

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-69

9-48 (Continued-5)

(0.10 × (sp/unit × Q)) ÷ (1 − t) = Total contribution margin − F

(0.10 × (sp/unit × Q)) ÷ (1 − t) = (cm per unit × Q) − F

(0.10 × $24.60/unit × Q) ÷ (1 − 0.30) = ($8.10 × Q) − $306,000

$3.5142857 × Q = ($8.10 × Q) − $306,000

$4.5857143 × Q = $306,000

Q = $306,000 ÷ $4.5857143/unit = 66,729 units

8. The point of this question is to get the students started thinking about the

competitive context in which the firm operates. There are many different

relevant points that could be made. If the discussion is slow to start, ask

them to think about what a firm like HPC must do to be competitive.

There are a number of critical success factors that are likely to be important

for both domestic and foreign subscriptions. These would include quality of

in different countries.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-70

9-49 CVP Analysis; Strategy; Sensitivity Analysis (75-90 min)

1.

Selling price per unit

$600

$600

Less: variable cost per unit:

Materials and purchased parts

180

195

Direct labor

55

63

Variable overhead

70

80

Variable GSA per unit

25

25

Total variable cost per unit

$330

$363

Contribution margin per unit (CM)

$270.00

$237.50

Total fixed cost per year:

Fixed manufacturing overhead

per unit

$90

$55

Fixed manufacturing overhead

$34,200,000

$20,900,000

Plus: Fixed GSA costs

$2,050,000

$2,050,000

Total fixed costs per year (F)

$36,250,000

$22,950,000

Breakeven in units (= F ÷ CM)

134,260

96,632

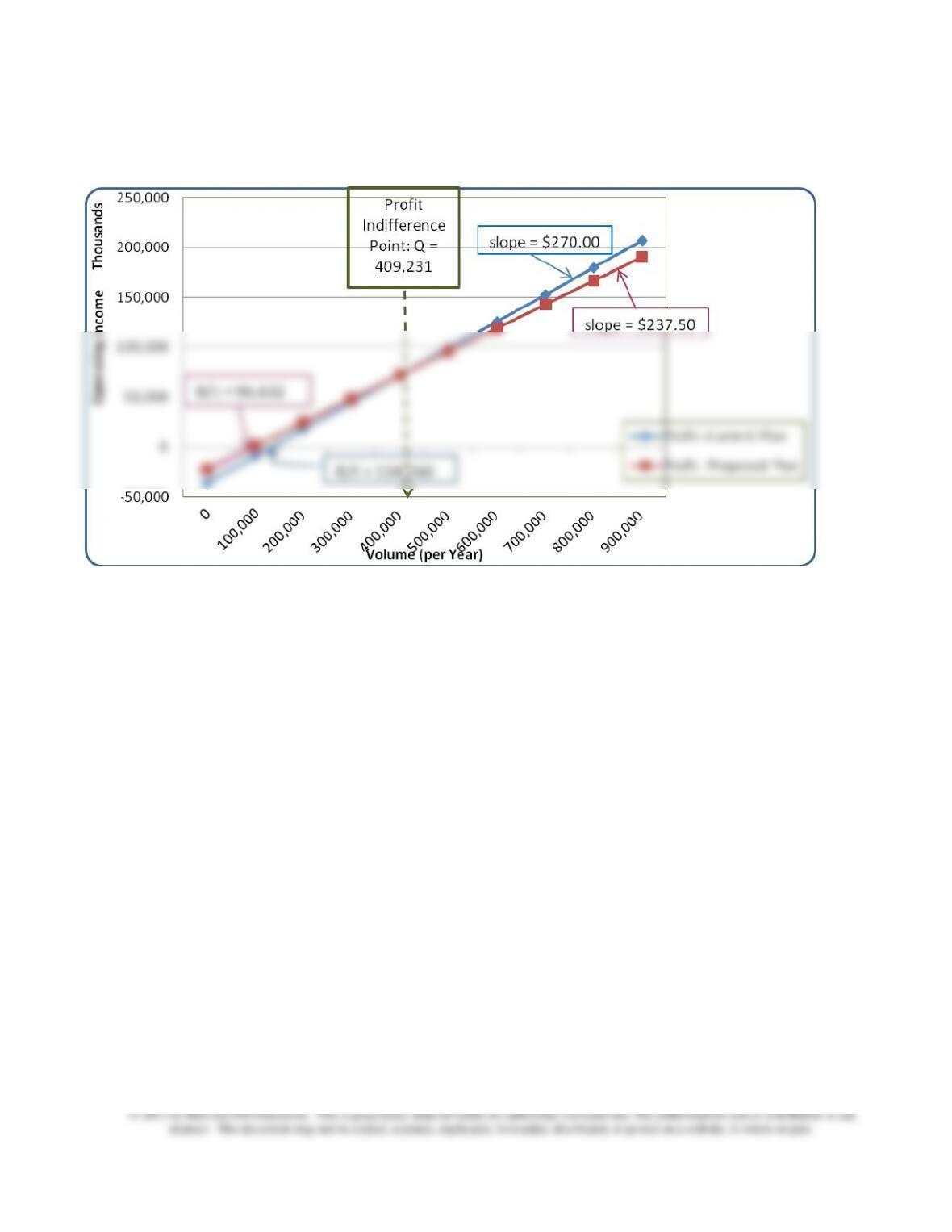

2. Indifference Point Calculation: the indifference point, in terms of cost, is

defined as the volume level (Q) in which total cost is the same for both

production options, as follows:

Cost Function for Current Plan:

($330 × Q) + $36,250,000

Cost Function for Proposed Plan:

($362.50 × Q) + $22,950,000

Cost Indifference Point, Q

($330.50 × Q) + $36,250,000 = ($362.50 × Q) + $22,950,000

$32.50 × Q = $13,300,000

Q = $13,300,000

$330 =

409,231 units

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-71

The above calculation shows that at the current level of 380,000 units, the

firm would prefer the low-fixed-cost strategy (i.e., the proposed plan)

9-49 (continued-1)

3. a) SolarFlex’s strategy is best described as differentiation, since the firm has

succeeded by innovation in product design. Further, the firm operates in

an industry in which innovation and product design are critical to success.

An important element of the firm’s strategy is also the fact that the

technology, as for many firms in the industry, is not proven. That is, there

with the possibility that the technology might fail.

b) The calculations in part 2 above support a decision to go to the new plan;

at the current level of 380,000 units, costs are lower for the new plan, and

will continue to be lower for the new plan as long as volume stays below

409,231 units.

Strategically, the new plan is preferred since it is an appropriate

failure of the innovation and then drop-off in sales. The reduction in fixed

costs also helps the firm to manage cash flows. Thus, the new plan is

more consistent with the firm’s strategy of developing an innovative

product and also dealing with the risk of potential loss because of a

possible failure of the technology in the market place. Also, one could

look at the proposal as consistent with the firm’s core strength, which

appears to be product innovation. There is no evidence that the firm is

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-72

9-49 (continued-3)

Current

Proposed

Difference

CM

$270.00

$237.50

$32.50

Fixed Cost

$36,250,000

$22,950,000

$13,300,000

Indifference Point = ($13,300,000 ÷ $32.50) = 409,231 units

Assumed Levels of

Demand

Profit-Current

Profit-Proposed

0 -36,250,000 -22,950,000

100,000 -9,250,000 800,000

200,000 17,750,000 24,550,000

300,000

44,750,000

48,300,000

400,000

71,750,000

72,050,000

500,000

98,750,000

95,800,000

600,000

125,750,000

119,550,000

700,000

152,750,000

143,300,000

800,000

179,750,000

167,050,000

900,000

206,750,000

190,800,000

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-73

4. Excel Charts (P-V function for each of the two decision alternatives)