Chapter 1 – Cost Management and Strategy

1-1

CHAPTER 1: COST MANAGEMENT AND STRATEGY

QUESTIONS

1-1 Firms Using Cost Management. Here are some examples; there are many

possible answers.

1. Wal-Mart: to keep costs low by streamlining restocking and sales

2. Dell: to keep costs low by improving manufacturing performance and by using

to be able to analyze the relative profitability of its different products, using cost

management

7. A small machine shop: which needs cost management to determine whether it

should repair or replace a machine

8. A dance studio: to analyze and choose between different compensation plans

for its teachers; and to determine whether it should open a new studio

1-2 Firms not expected to be significant users of cost management information:

1. Microsoft: here the focus is on forming strategic alliances, innovation and

competition; cost management is more important for other firms in the

4. Major league sports: dependent primarily on the development of fan support,

good coaching and player acquisition

1-3 Cost management information is a broad concept. It is the information the

manager needs to effectively manage the firm or not-for-profit organization —

Chapter 1 – Cost Management and Strategy

1-2

1-4 In the private sector, the Financial Accounting Standards Board, an independent

organization, and the American Institute of Certified Public Accountants (AICPA)

supply guidance regarding financial reporting practices. The Sarbanes-Oxley Act

of 2002 also created the Public Company Accounting Oversight Board which

reports to the SEC to oversee auditing standards and practices. The AICPA also

around the world. The Financial Executives International (FEI) organization

provides services much like the IMA for financial managers, including controllers

and treasurers. Because of the nature of its membership, the FEI tends to focus

on management and operational control issues, and less on the product costing,

planning, and decision-making functions.

1-5 The Certificate in Management Accounting (CMA) is the most relevant

certification program for management accountants since it focuses on the types

of skills that are most in demand for management accountants: economics,

1-6 The four functions of management are:

1. Strategic Management — information is needed by management to make

sound strategic decisions regarding choice of products, manufacturing methods,

marketing techniques and channels, and other long term issues.

2. Planning and Decision Making — information is needed to support recurring

requirements, for the preparation of financial reports and for use in the three

other management functions.

1-3

1-7 Strategic management is the most important management function since it most

goals drives all other activities in the firm.

1-8 Merchandising firms purchase goods for resale. Merchandisers that sell to other

merchandisers are called wholesalers, while those selling directly to consumers

are called retailers. Examples of merchandising firms include the large retailers,

such as Sears, Wal-Mart, and Radio Shack. Merchandisers use cost

Governmental and not-for-profit organizations provide services, much like the

firms in service industries. However, the service provided by these organizations

is such that there is often no direct relationship between the amount paid and the

services provided. Instead, both the nature of the services to be provided and

the customers who receive the service are determined by government or

philanthropic organizations. These organizations use cost management

information to determine and control the costs of the services they provide.

1-9 The answers here can vary from large manufacturers such as Hewlett-Packard

(HP) to small retail stores. If the class has trouble getting started, the instructor

in a given industry, etc.

1-10 As firms move to the Internet for sales and customer service it is likely that

strategies will change. For some firms, a popular web site can be an important

differentiating factor. Firms such as Amazon.com, Etrade and eBay have

Chapter 1 – Cost Management and Strategy

1-4

1-11 As firms move to the Internet for sales and customer service it is likely that their

demand for cost management information will change. For example, order

response and reliability which can be achieved through the web-site. Whether

and how soon the firm can achieve these benefits is a critical question.

1-12 The factors in the contemporary business environment that affect business firms

and cost management are:

1. Increased global competition, which means an increasingly competitive

environment for all firms and thus the need for cost management information

to become more competitive; the need for competitive non-financial

information in addition to financial information in cost management reports;

2. Lean manufacturing, in which companies reduce costs by using flexible

the firm work together to make the firm successful;

6. Changes in the social, political, and cultural environment of business, which

requires an expansion of cost management reporting to include critical

success factors related to the expectations of those beyond the ownership of

the firm including employees, local government officials, and community

leaders.

Chapter 1 – Cost Management and Strategy

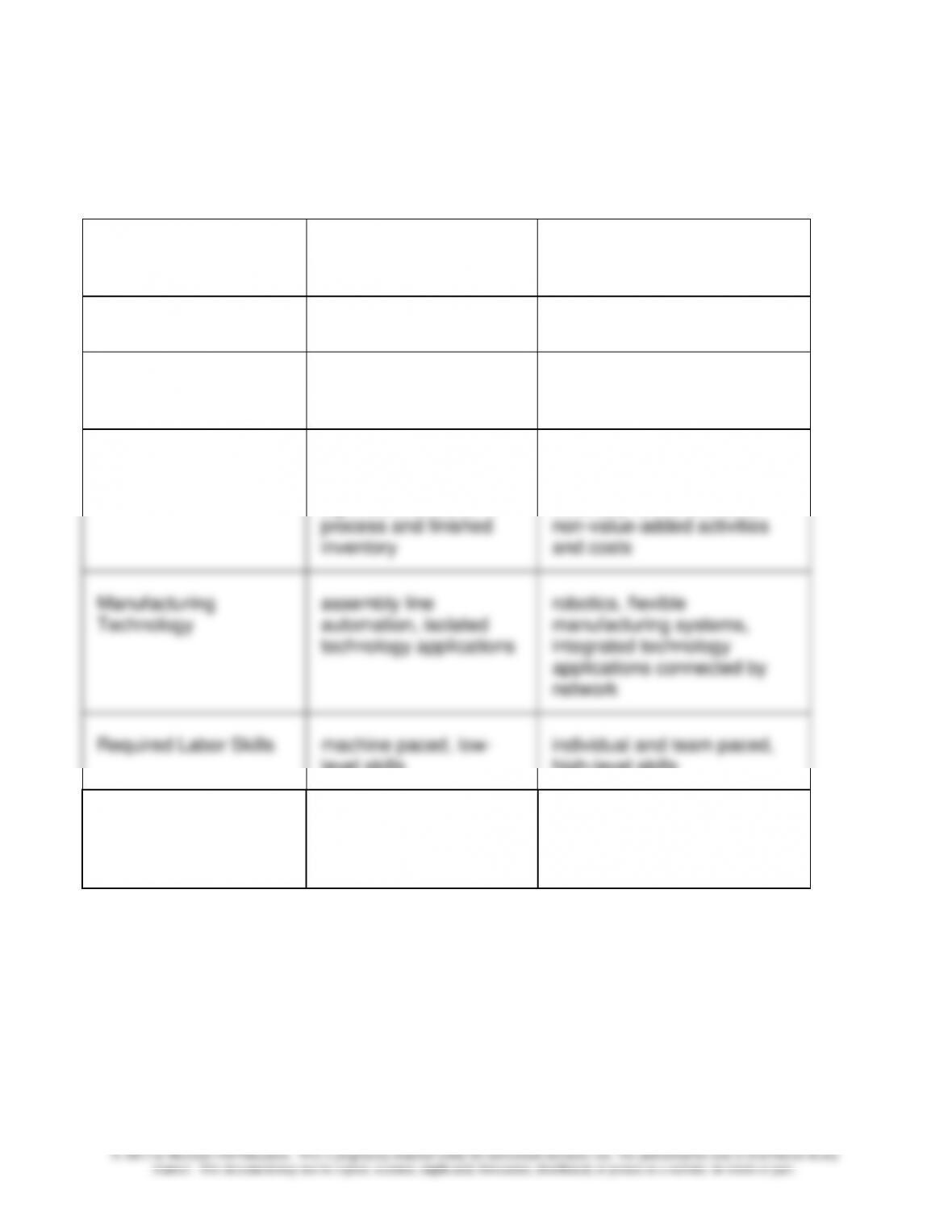

1-13 Refer to Exhibit 1-3 in the text, reproduced here.

Comparison of Prior and Contemporary Business Environments

The Prior Business

Environment

The Contemporary

Business Environment

MANUFACTURING

Basis of Competition

economies of scale,

standardization

quality, functionality,

customer satisfaction

Manufacturing Process

high volume, long

production runs,

significant levels of in-

process and finished

inventory

low volume, short production

run, focus on reducing

inventory levels and other

non-value-added activities

and costs

Manufacturing

Technology

assembly line

automation, isolated

technology applications

robotics, flexible

manufacturing systems,

integrated technology

applications connected by

network

Required Labor Skills

machine paced, low-

level skills

individual and team paced,

high-level skills

Emphasis on Quality

acceptance of a normal

or usual amount of

waste

strive for zero defects

Chapter 1 – Cost Management and Strategy

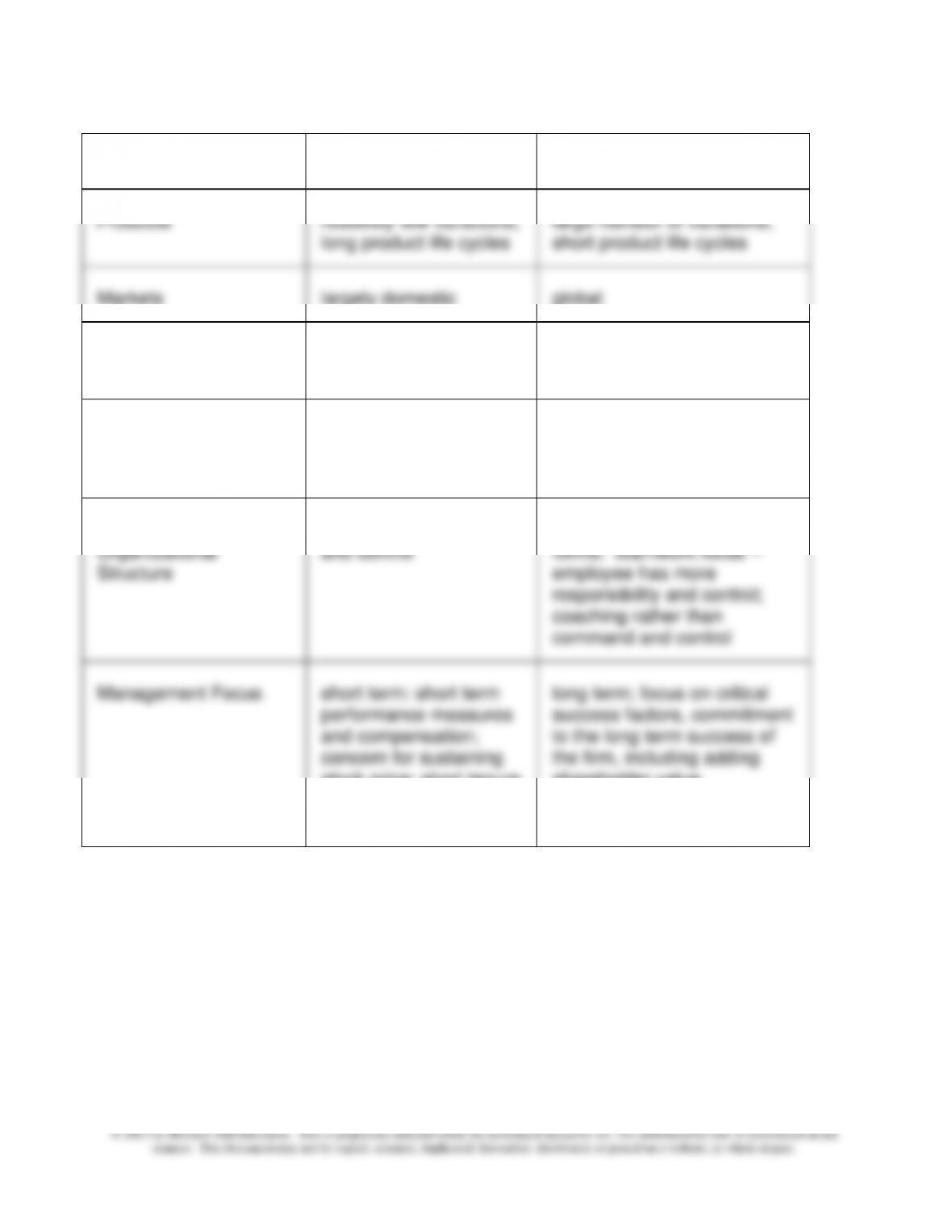

Question 1-13 (continued)

MARKETING

Products

relatively few variations,

long product life cycles

large number of variations,

short product life cycles

Markets

largely domestic

global

MANAGEMENT

ORGANIZATION

Types of Cost

Management

Information Needed

almost exclusively

financial data

financial and operating data,

the firm’s strategic success

factors

Management

Organizational

Structure

hierarchical; command

and control

network-based organization

forms; teamwork focus —

employee has more

responsibility and control;

coaching rather than

command and control

Management Focus

short term: short term

performance measures

and compensation;

concern for sustaining

stock price; short tenure

and high mobility of top

managers

long term; focus on critical

success factors, commitment

to the long term success of

the firm, including adding

shareholder value

1-7

1-14 The thirteen contemporary management techniques are:

1. The Balanced Scorecard (BSC) and the Strategy Map. The BSC is an

accounting report that includes the firm’s critical success factors in four areas:

financial performance, customer satisfaction, internal processes, and learning

and growth (human resources). The Strategy Map is a method, based on the

balanced scorecard, which links the four perspectives in a cause-and-effect

diagram.

2. Value-Chain Analysis is a tool that helps the firm identify the specific steps

required to provide a product or service.

3. Activity-based Costing and Management: Activity-based costing is used to

processes to match or beat the performance of its competitors.

8. Business Process Improvement is a management technique in which

managers and workers commit to a program of continuous improvement in

quality and other critical success factors.

Chapter 1 – Cost Management and Strategy

1-8

9. Total Quality Management is a technique in which management develops

policies and practices to ensure that the firm’s products and services exceed the

11. The Theory of Constraints is a strategic technique to help firms effectively

improve the rate at which raw materials are converted to finished product.

1-14 (continued)

12. Enterprise Sustainability means the balancing of the company’s short– and

13. Enterprise Risk Management is a framework and process that firms use to

manage the risks that could negatively or positively affect the company’s

competitiveness and success.

Chapter 1 – Cost Management and Strategy

1-9

BRIEF EXERCISES

1-15 Many students will answer Wal-Mart or Target since these are mentioned in the

text. A variety of answers are possible and sometimes students will disagree , as

for example, in discussing a fast food restaurant such as McDonald’s. Some will

and price only, and I will get a few examples there, but not many.

1-16 (a) This question is set to get a positive response and that is usually what I get.

Then I try to spend some time getting some examples of why a strong ethical

climate would be beneficial, and note the increasing importance of an ethical

social and environmental values affect financial performance in the short run.

The article notes, as do many other surveys, that the firm Johnson& Johnson is

perhaps the best known example of a company that has high corporate values.

1-17 Again this question is posed for a positive response, and the main goal I have for

the question is to have the class think through the decision as both a business

and an ethical issue. According to a Wall Street Journal article at the time of this

media companies that were counting on Merck’s spending for VIOXX advertising.

1-18 Like most beverage companies, there is a strong differentiation. Refer the

students to the information in Problem 1–41 which shows Coke as having the

1-19 A commodity is a product or service that is difficult to differentiate from

competitors: gasoline and paper products are some examples. You can ask the

Chapter 1 – Cost Management and Strategy

1-10

1-20 Most students will argue that they chose their bank because of service and

location, thus differentiation. Others will say the rates are better, and then

perhaps cost leadership. It is useful to distinguish the banking needs of say, a

student, versus a small business like a car dealership which will rely more

heavily on a variety of customer services and will likely see banks as more

boast that they can afford to offer more personal service than the industry

behemoths.” The large banks are not ignoring customer service, however; at

that time, Wachovia was the fourth largest bank in the U.S. (acquired by Wells

Fargo in 2008) and number one in customer service (for larger banks).

1-21 There are a number of possible answers here. The main point of the question is

that the cost leadership or differentiation classification applies across different

consider the automobile industry and to identify cost leaders and differentiators.

1-22 It is certainly likely that a new product, with technologically advanced features,

may begin as a differentiator and then as the market for the product matures and

1-23 Often people think of strategy as simply planning, or “long term” planning. In the

broadest sense, this is correct, though the planning in strategy formulation and

Chapter 1 – Cost Management and Strategy

1-11

EXERCISES

1-24 Strategy; Real Estate Services (15 min)

This exercise can be used to provide a good perspective for the

students to see the role of cost management in solving business

issues, and in placing the management accountant in more of a

leadership role in the firm. It also provides an early motivation for the

cost behavior issues to be discussed later in chapter 3 and chapter 8.

The management accountant has a hunch that the company is

about to take on a potentially damaging strategic initiative. This is a

Here’s how the case might be used in a class discussion. First,

ask the class to identify the types of costs likely to be incurred by this

company in providing its service. The answers are likely to include

labor costs and materials for cleaning and maintenance, in addition to

costs for maintaining the firm’s office. As these examples are given,

put them on the chalkboard and collect 6 or 8 of them. Then, ask

how each of these costs might differ between large and small

customers. For example, the cost of cleaning labor and materials will

likely be somewhat proportional to the square feet of space each

customer occupies, so that cost projections based on current

space) means the smaller customers will be more costly, per unit of

floor space, than the larger customers. This should be taken into

account in pricing the smaller jobs and in projecting profits from the

smaller customers.

1-12

1-24 (continued-1)

An important issue this case brings out is the need for the

management accountant to take a proactive role in business decision

proposed.

1-25 Impact of the Recession on the Role of Cost Management (15

min)

This question is intended for a brief class discussion, with a number

of possible answers. Some students will note that the financial crisis

has increased the importance of finance generally, as companies

(especially smaller ones) work hard to manage cash flow and to

reduce costs in the face of declining revenues. Others will argue that

the financial crisis has turned management’s focus to operational

skills required of management accountants, and the second is the

increased importance of the management accountant’s role in

strategy.

The impact of the recession on finance and cost management, as for

other areas of business, is to motivate a drive for efficiency. Many

finance staffs have reduced their numbers significantly. On the

other hand, the important development is that the demand for

finance skills has shifted. Automation of the finance function and

economic times.

Chapter 1 – Cost Management and Strategy

1-13

For example, cost management can also be used in target costing

and strategic planning to identify opportunities for success in the

currently weak economic conditions in the U.S. and Europe. To

1-25 (continued -1)

Another important finding, based on a survey of CFOs, shows:

o 46% of the CFOs surveyed report that the crisis has enhanced

beyond finance, including corporate strategy.”

A broad take-away of the discussion should be the enhanced role of

the finance function, the management accountant, and particularly

Source: Alix Stuart, “The Incredible Shrinking Finance Department,”

CFO, November 2010, pp 46-52; “Recession Impressions,” CFO,

November 2009, pp 42-43; John Helyar and Phil Kuntz, “A Mini–

Revival for the Rust Belt,” Bloomberg Businessweek, August 29,

2011, pp 20-21.

1-14

1-15

1-27 Contemporary Management Techniques (30 min)

1. For an article on target costing, Tim should consider the types of

firms which would demand this type of strategic costing. These would

be firms that are in very competitive industries, where cost/price

competition is critical, such as consumer products. Examples of firms

that might use target costing also include those that have short

product life cycles (the time from introduction of the product into the

cycle.

2. For an article on life-cycle costing, Tim’s search for appropriate

firms would lead him to many of the same types of firms as for target

costing in (1) above. Intense competition on price/cost and short

product life cycles are indicators of firms that are likely to use life–

through continuous improvement efforts, the product will become

profitable later in its life cycle.

3. For an article on the theory of constraints, a wide variety of firms,

including both manufacturing firms and service firms, would be

appropriate. Manufacturing firms would be good examples to use for

production process.