Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 17 - The Management and Control of Quality

17-61

17-53 Cost-of-Quality (COQ) Reporting; Spreadsheet Application (45–60 Minutes)

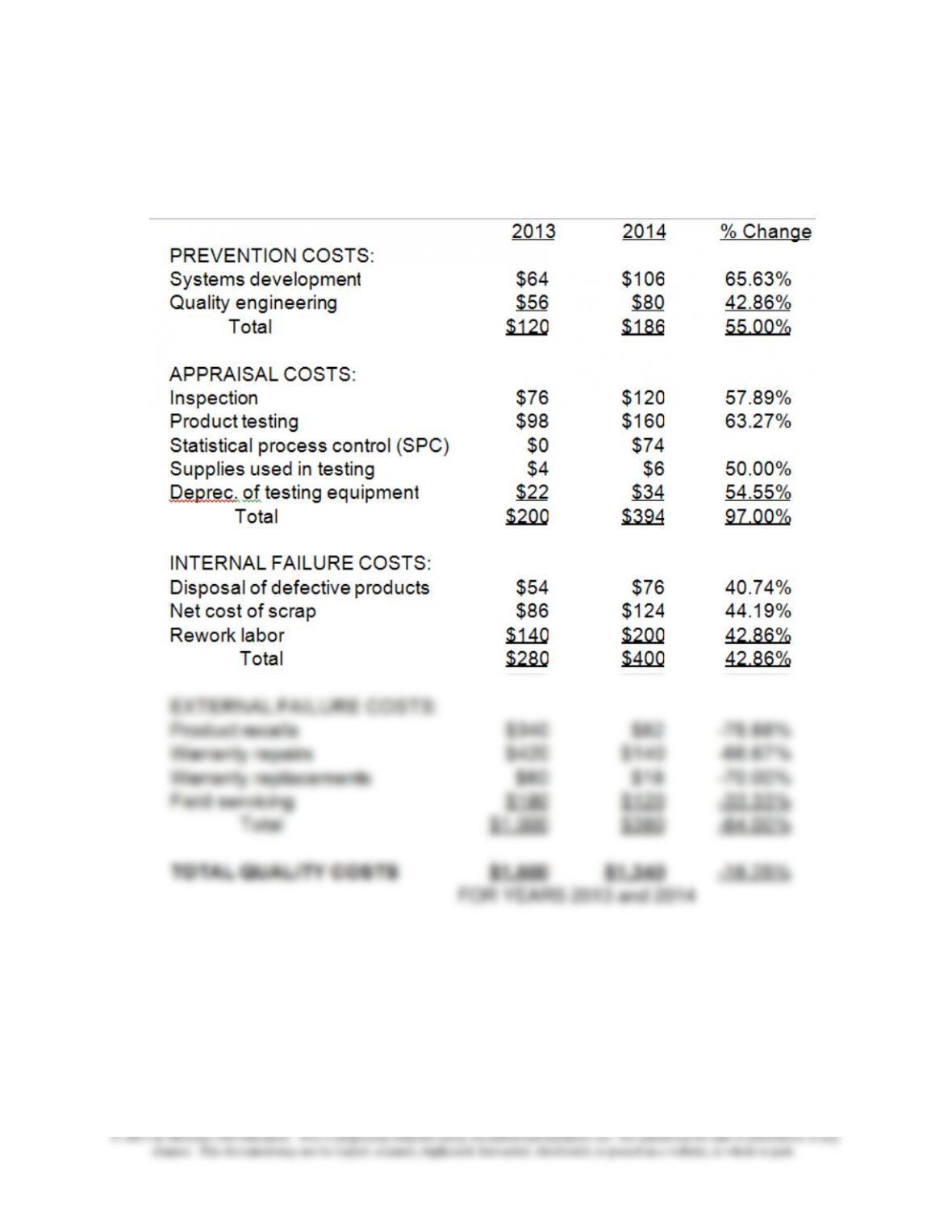

1. LEE ENTERPRISES

COST-OF-QUALITY REPORT

Chapter 17 - The Management and Control of Quality

17-62

17-53(Continued-1)

2.

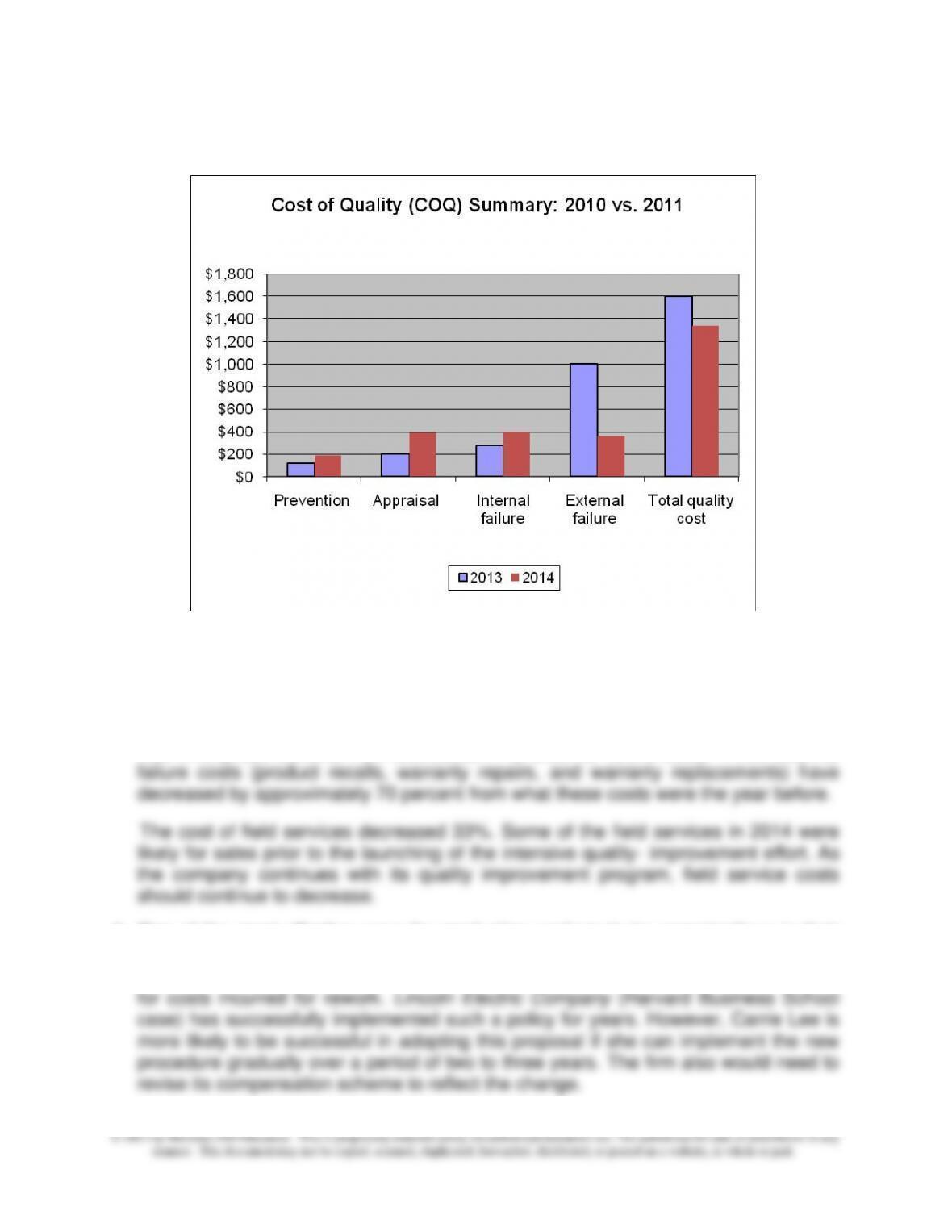

3. The report indicates that prevention, appraisal, and internal failure costs have

increased from 2013 to 2014. The external failure cost category decreased by 64%.

It is likely that the intensive efforts to improve quality has begun to pay off as,

indicated by a decrease of approximately 16% in total COQ from 2013 to 2014.

Lee Enterprises benefits from decreases in its external failure costs. Three external

4. One of the most effective ways for production workers to be conscientious in their

work is to hold them responsible for mistakes. Holding employees responsible for

their work can include a policy for workers to do rework on their own time and to pay

17-63

17-53 (Continued-2)

Note: Two linked Excel spreadsheet solution files for this Problem are embedded

below. You can open each spreadsheet “object” by doing the following:

1. Right click anywhere in the worksheet area.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to...”

while you are in the spreadsheet mode. The screen should return you to this

Word document.

17-54 Relevant Costs and Quality Improvement (20–30 minutes)

1.

Lightening Bulk Company

Cost and Benefit Analysis of the Proposed

Scheduling and Tracking System

Cost of the new system (per year) $ 150,000

Expected benefits each year from the new system:

Contribution margin from sales increase:

(5,000 × 10%) × $200 × 40% = $ 40,000

The new scheduling and tracking system will most likely decrease the firm‘s pre-tax

cash flow per year. Thus, from a purely financial point of view the company cannot

justify the purchase of the new system.

2. Among other factors the manager needs to consider are: reliability and accuracy of

the estimates, including contribution margins, cost of tracking misplaced and lost

items (and their behavior patterns), and the estimated decreases in misplaced and

Pr. 17-53(a).xlsx

Pr. 17-53(b).xlsx

Chapter 17 - The Management and Control of Quality

17-64

3. Cost to handle lost or misplaced items in the country in question:

Misplaced items: 5,000 × 12.0% × 0.8 × $60 = $28,800

Chapter 17 - The Management and Control of Quality

17-65

17-55 Quality Improvement; Relevant Cost Analysis (50-60 Minutes)

1. Cost of new equipment and installation $12,000,000

Training 3,000,000

2. Quality cost if no change is made:

Rework (3,000 × 40%) × $2,000/unit = $ 2,400,000

Repair (3,000 × 15%) × $2,500/unit = 1,125,000

Appraisal 600,000

Inspection 3,000 × $50 = 150,000

Foregone contribution from lost sales:

Contribution margin per unit:

($12,000 × 85%) − $2,500 = $7,700

Lost sales units = (3,000 0.8) − 3,000 = × 750 5,775,000

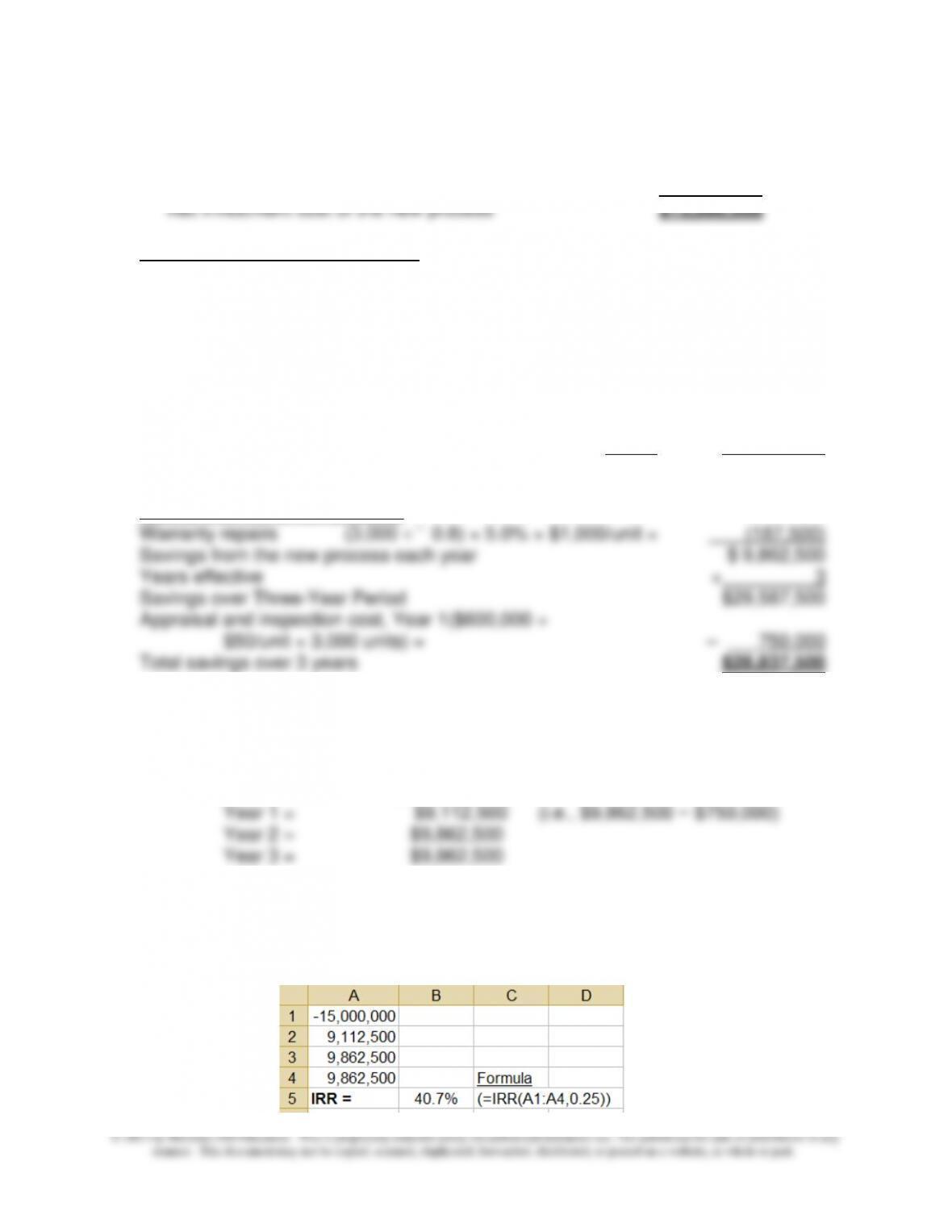

Total current cost of quality per year = $10,050,000

Quality cost of the new process:

3. Yes. The cost of the new process is $15,000,000 and the expected benefits total

$28,837,500 over three years. The pattern of pre-tax cash flows for this investment

opportunity is as follows:

Year 0 = ($15,000,000)

Thus, the payback period for this proposed investment is less than two years. Its

internal rate of return (IRR) is approximately 41%, as shown in the following screen

shot from Excel:

17-66

17-55 (Continued)

4. The following factors should be considered before making the final decision:

a. Accuracy of cost estimates, including:

▪ contribution margin per unit

d. Time-value-of-money factor (discount rate) for capital budgeting decision-

making

5. The member of the board would be right if we ignore the financial payoff of the new

process and if the company is going to be in business for only three years. Having

high-quality products, especially for a high-end product such as the one the

company is selling, is crucial for a long-term success.

Chapter 17 - The Management and Control of Quality

17-67

17-56 Analyzing Cost of Quality (COQ) Reports (60 Minutes)

1. There is an extensive literature in the area of “change management” from which

students can draw in order to respond to this question. Based on this literature, the

following factors might be mentioned as being critical for an organization's

successful quality program:

▪ Evidence of top-management support, including motivational leadership and

to continuous, dynamic improvement; related to this is the need to develop an

effective reward system (i.e., link performance and compensation).

2.

BERGEN, INC

Quality Cost Report

Most Recent and Most-Distant Quarter

6/30/2013 9/30/2014

% of % of % of % of

Quality Amount Quality Prod. Amount Quality Prod

Cost Category (in ‘000) Cost Cost (in ‘000) Cost Cost

Prevention $240 24.90 5.83 $270 45.68 5.99

Appraisal 205 21.27 4.98 116 19.63 2.57

From an analysis of the COQ Report (oldest vs. most recent quarterly results) it would

appear that Bergen Inc.'s program has been successful because:

▪ Total COQ as a percentage of total production cost has declined from 23.4% to

13.1%.

▪ External failure costs, those costs signaling customer dissatisfaction, have

declined from 8.03% of total production cost to 2.28%. These declines in

for testing.

17-68

17-56 (Continued)

▪ Quality costs have shifted to the area of prevention where problems are solved

before the customer becomes involved. Prevention costs, such as maintenance,

3. Tony Reese's current reaction to the quality-improvement program is more favorable

as he is seeing the benefits of having the quality problems investigated and solved

before they reach the production floor. Because of improved designs, quality

last assertion can be tested through the collection of relevant nonfinancial quality

indicators.)

4. To measure the opportunity cost of not implementing the quality program, Bergen

Inc. could assume that:

a. Sales and market share would continue to decline and then estimate the

5. This question is designed to make students think about a proper role of a COQ

reporting system as part of a comprehensive framework for managing and

controlling quality, such as the framework presented in Exhibit 17.3. The main point

is that COQ data can be a valuable attention-director. For example, many

organizations (confirmed by our own in-class discussions with MBA students) are

quantify in financial terms the impact of these failures on profitability. In short,

“diagnostic control” of quality is probably better achieved through the application of

techniques borrowed from operations management (“cause-and-effect diagrams,”

Pareto charts, etc.) applied to nonfinancial measures of quality. This suggests,

therefore, that one characteristic of a comprehensive framework for managing and

controlling quality is the use of both financial and nonfinancial quality indicators.

Chapter 17 - The Management and Control of Quality

17-69

17-57 Benefits of Switching to JIT (50-60 Minutes)

1. A JIT manufacturing approach is considerably different from a conventional

manufacturing system. Under JIT, an output is produced only when

demanded by the customer (internal or external). At the core of JIT is a

strong commitment to quality (i.e., eliminating or reducing processing

kept on-hand as a “cushion” to compensate for error, waste, and

inefficiencies, or for unforeseen circumstances. “Normal” inefficiencies, in

fact, are built into overhead application rates.

2. The response to this question can be crafted around an examination of

Exhibit 17.3. As indicated in this exhibit, the management accountant,

because of expertise in the area of measurement, can supply to

management relevant cost information and relevant nonfinancial

performance indicators associated with a change in manufacturing process,

such as a move to JIT.

Specifically, the management accountant can help estimate the financial

savings associated with inventory reductions and with manufacturing

assess the overall benefits associated with the move to JIT. These

characteristics of the manufacturing process are important to monitor

because they can be leading indicators of future financial performance.

3. Annual benefits associated with the proposed move to JIT—in general,

improvements in quality, such as those associated with the adoption of JIT,

result in two separate benefits: increases in revenues (or, contribution

margin), and decreases in costs.

Chapter 17 - The Management and Control of Quality

17-70

17-57 (Continued-1)

Estimated decrease in inventory carrying costs:

Pre-JIT Inventory Holdings:

Raw materials = 40,000 × $15 × (4 ÷ 12) = $200,000

WIP Inventory = 40,000 × $25 × (3 ÷ 12) = $250,000

Finished Goods = 40,000 × $40 × (2 ÷ 12) = $266,667

Average Inventory Holdings = $716,667

Post-JIT Inventory Holdings:

Raw Materials = 52,000 × $12 × (2 ÷ 12) = $104,000

WIP Inventory = 52,000 × $20 × (1.5 ÷ 12) = $130,000

Finished Goods = 52,000 × $30 × (1 ÷ 12) = $130,000

Average Inventory Holdings = $364,000

Difference in Average Inventory Holdings = $352,667

4. Based solely on the short-term financial effect, ABC should replace the

equipment and move to JIT. The annual pre-tax net benefit of $712,900

break its existing lease.

5. Additional considerations:

▪ This decision is technically a capital budgeting decision; as such, the

future cash flows should be stated on an after-tax basis and discounted

product?

Chapter 17 - The Management and Control of Quality

17-71

17-57 (Continued-2)

▪ JIT places significant pressures on employees and managers alike, to

constantly improve: is there an appropriate change agent in the

organization to lead this effort? Does the change have the full, and

planning efforts regarding the implementation of JIT?

▪ Has the cost of collecting, reporting, and interpreting key nonfinancial

quality indicators been factored into the analysis?

Chapter 17 - The Management and Control of Quality

17-72

17-58 Environmental Performance—Meeting Stakeholder Expectations (60 Minutes)

1. As indicated in the cited HBR piece, the following stakeholders are likely to be

interested in corporate disclosures regarding environmental performance:

2. The environmental performance scorecard created by Climate Counts

(http://www.climatecounts.org/pdf/Climate_Counts_Scorecard.pdf) consists of 22

items, broken down into four areas, as follows:

Review:

(1) GHS emissions inventory completed? (5 points)

(4 points)

Reduce:

(7) Has a clear goal been set? (4 points)

(8) Strength of baseline year used for the reduction goal? (3 points)

(9) Magnitude of reduction goal? (5 points)

(10) Have a measurement plan and organizational structure been established

for climate? (5 points)

(17) Does the company work to educate its employees, trade associations,

and/or customers on how they can reduce individual GHG emissions

(through direct education programs, incentives, or philanthropic projects?

(4 points)

(18) Does the company require suppliers to take climate change action or give

preference to those that do? (2 points)

Chapter 17 - The Management and Control of Quality

17-73

17-58 (Continued-1)

Policy Stance:

(19) Does the company support public policy that could require mandatory

Report:

(21) Is the company publicly reporting on emissions, risks, and actions? How is

information disclosed? Company-based (e.g., on their website or annual

report) or through a credible third-party program (e.g., CDP, GRI, etc.)? (10

points)

(22) Are emissions broken out by facility, business unit, country of operations,

or other meaningful sub-segments? (2 points)

3. As seen at http://www.climatecounts.org/scorecard_score.php?co=28 (accessed 25

November, 2011), IBM’s scorecard total for the current year is 82 (an increase of 3

points over last year’s score). It has scored highly in each of the areas, with the

possible exception of Policy Stance (4 out of 10 points). Its current score places it #2

among the 12 firms from the electronics sector. The website lists IBM as “striding,” as

follows:

Apple, on the other hand, scored last among 12 companies in the electronics industry

category (see http://www.climatecounts.org/scorecard_score.php?co=7, accessed 25

January, 2011). Apple’s current score is 60, a one-point change from last year, but

significantly above the score of three years ago (which score is mentioned in the HBR

article). Apple’s component scores are as follows: Review: 19/22 points. Apple has

resigned from the US Chamber of Commerce over the trade group's opposition to

comprehensive climate and energy legislation. Report: 8/12 points. Apple has made