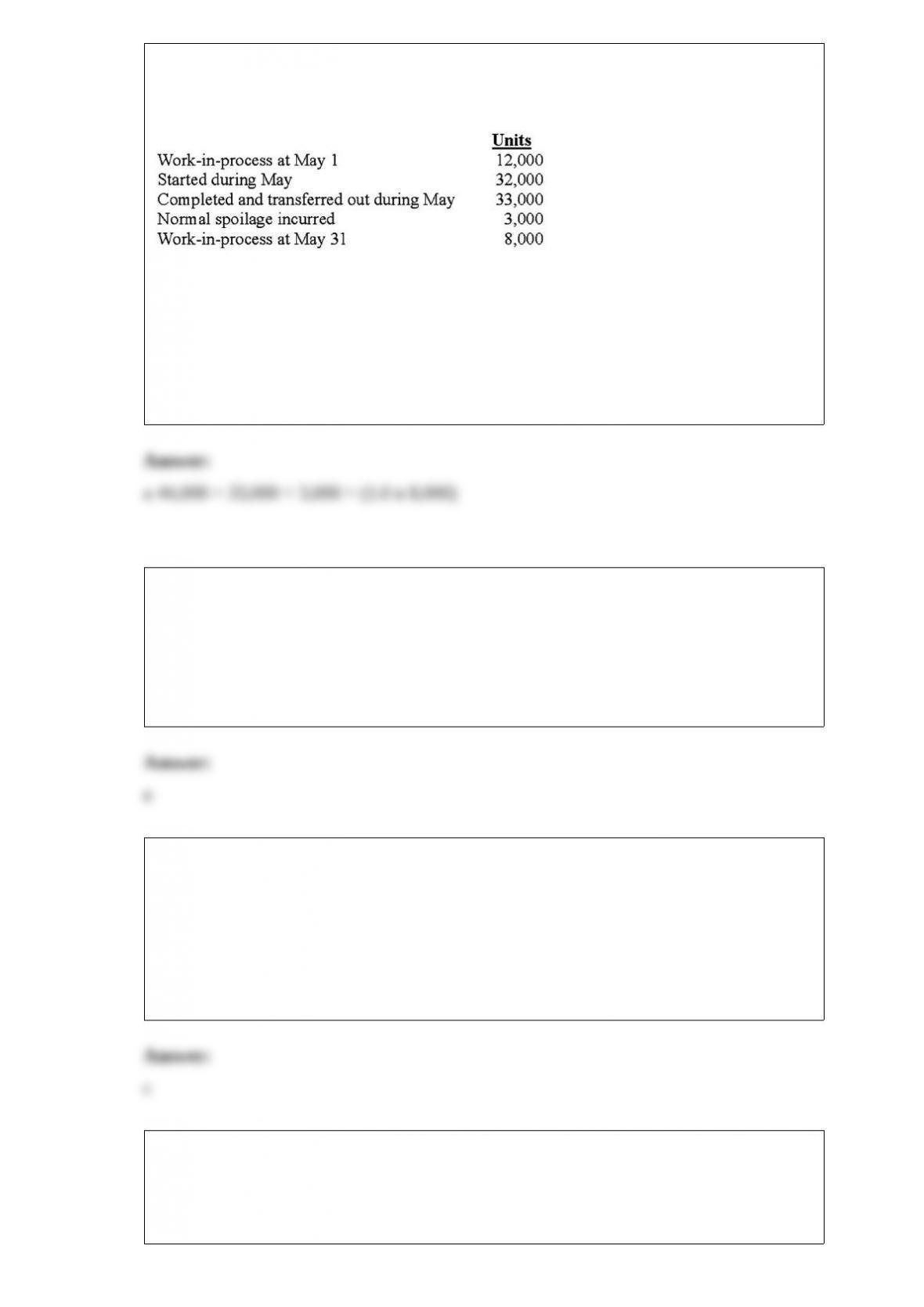

1) larsen company adds materials at the beginning of the process in department 2 . data

concerning the materials used in may production are as follows:

using the weighted-average method, the equivalent units for materials are:

a.44,000

b.41,000

c.36,000

d.33,000

e.32,000

2) in job costing, the job might consist of:

a.a single product

b.a batch of identical products

c.a batch of similar products

d.a single, well-defined project

e.a single product, a batch of products, or a single well-defined project

3) volume-based rates are appropriate in situations where the incurrence of factory

overhead:

a.is related to multiple cost drivers

b.is related to several non-homogeneous cost drivers

c.is related to a single, common cost driver

d.varies considerably from period to period

e.is relatively small in amount

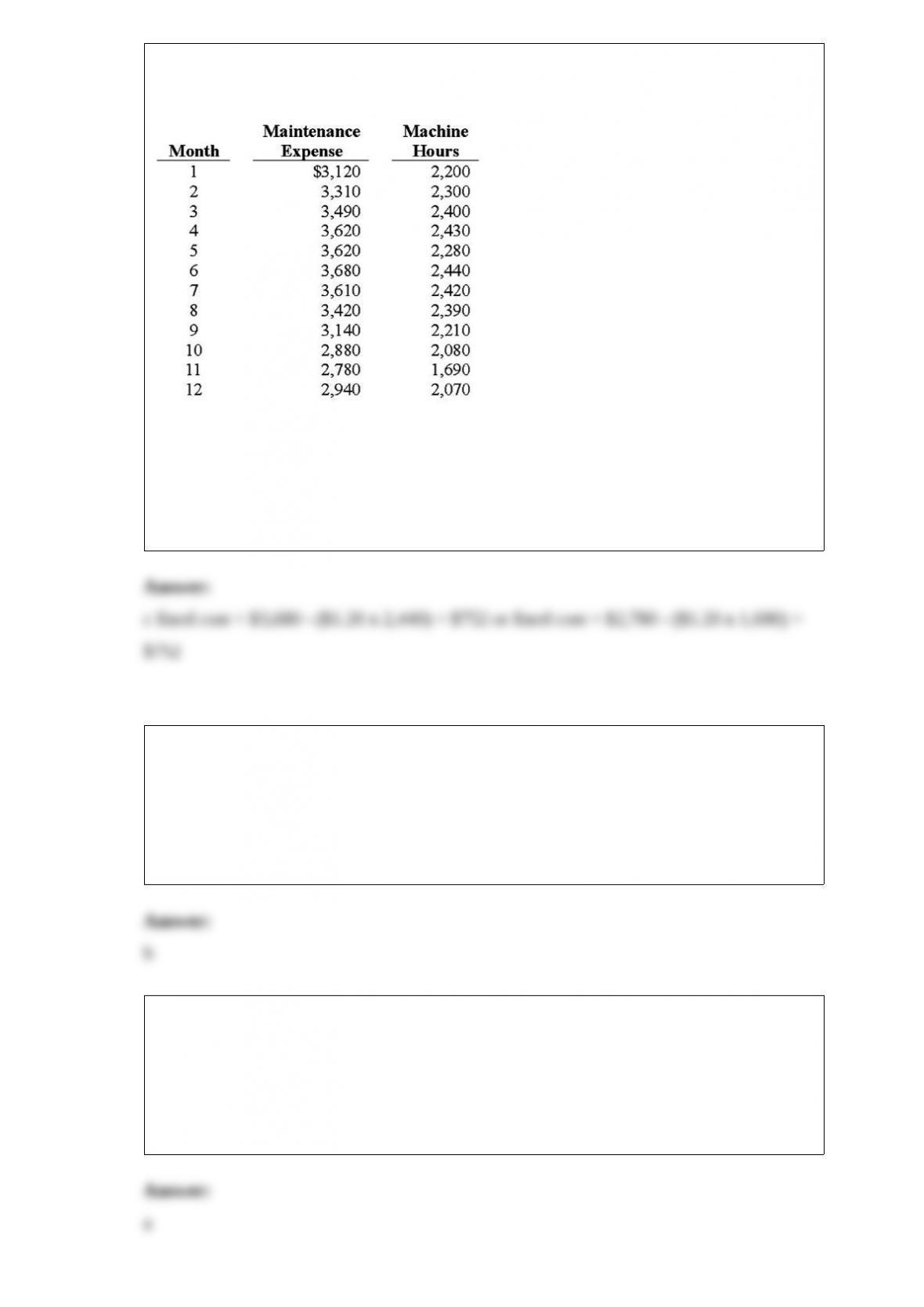

4) felinas inc. produces floor mats for cars and trucks. the owner, kenneth felinas, asked

you to assist him in estimating his maintenance costs. together, mr. felinas and you

determined that the single best cost driver for maintenance costs was machine hours.

below are data from the previous fiscal year for maintenance expense and machine

hours:

using the high-low method, total monthly fixed cost is calculated to be:

a.$484

b.$364

c.$752

d.$259

e.$898

5) a measure of the statistical reliability of each independent variable is:

a.correlation

b.t-value

c.r-squared

d.standard error

e.multicollinearity

6) all of the following items are debited to the work-in-process inventory account

except:

a.cost of the completed goods being transferred out of the plant

b.direct labor cost consumed/incurred

c.direct materials cost consumed/used

d.applied factory overhead cost

7) a retailer, in business for over 50 years, has developed the following regression

model from the past 60 months of operating data:

monthly sales dollars = $50,000 + $4.70a + $30b – $1,000x

where:

a = number of customers

b = advertising dollars per month

x = 1 if a winter month

x = 0 if other months

an appropriate interpretation of this model is that:

a.the business is seasonal, generating higher sales in winter months than other months

b.advertising is not cost effective

c.within the relevant range, each additional customer will make a monthly purchase of

$4.70 on average

d.sales are always expected to be at least $50,000

8) a variable used in regression analysis that represents the presence or absence of a

condition, e.g., seasonality, is called a(n):

a.random variable

b.dummy variable

c.constant term variable

d.correlating variable

e.fixed term variable

9) if the coefficient of correlation between two variables is nearly zero, how might a

graph of these variables appear?

a.random points

b.a least squares line that slopes up to the right

c.a least squares line that slopes down to the right

d.under this condition, a scatter diagram could not be plotted on a graph

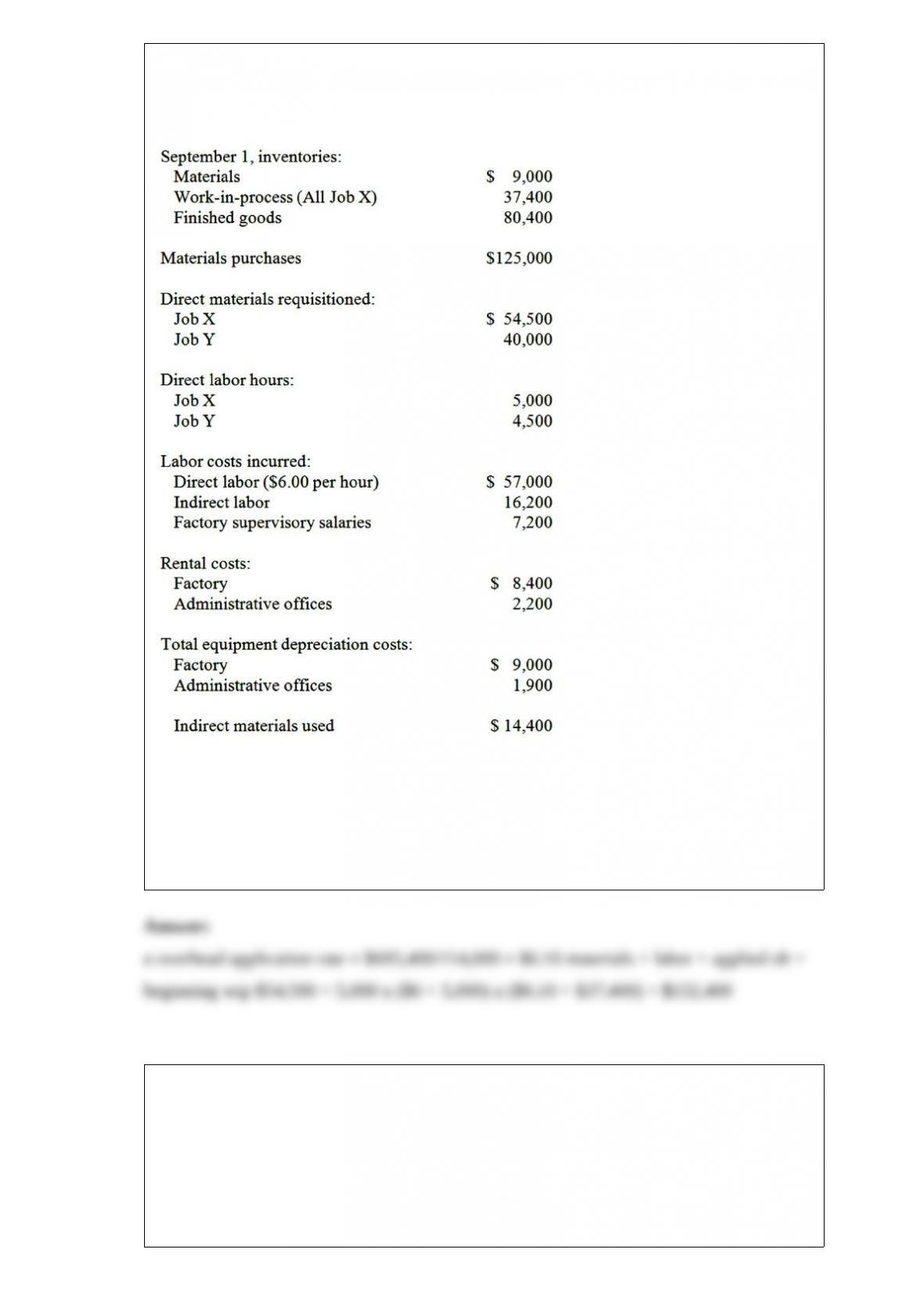

10) badour inc. is a job-order manufacturer. the company uses a predetermined

overhead rate based on direct labor hours to apply overhead to individual jobs. for the

current year, estimated direct labor hours were 114,000 and estimated factory overhead

was $695,400. the following information was for september. job x was completed

during september, while job y was started but not finished.

the total cost of job x is:

a.$152,400

b.$128,200

c.$151,900

d.$129,600

e.$140,800

11) which of the following best describes the type of information that cost management

must provide that is important for the success of the organization?

a.short term information for decision making

b.reported financial information

c.reported nonfinancial information

d.information that addresses the strategic objectives of the organization

e.long-term planning information

12) a company’s management accountant is trying to improve the way costs are

allocated within the company. currently, several corporate expenses are grouped

together and labeled “overhead.” if the accountant wanted to use activity-based costing

(abc) to help solve the problem, what should she do?

a.she should try to trace the departments’ costs to their cost objects, and then charge

each department based on those cost relationships

b.she should research how the company’s competitors are allocating their costs, and

then implement one of those strategies

c.she should look for bottlenecks within the production process, and try to eliminate

them, thus reducing costs

d.she should examine the firm’s value chain and apply target costing before adopting

abc

13) management accountants are frequently asked to analyze various decision situations

including the following:

(1) alternative uses of plant space, to be considered in a make/buy decision.

(2) joint production costs incurred, to be considered in a sell-at-split-off versus a

process-further decision.

(3) research and development costs incurred in prior months, to be considered in a

product-introduction decision.

(4) the cost of a special device that is necessary if a special order is accepted.

(5) the cost of obsolete inventory to be considered in a keep-versus-disposal decision.

the costs described in situations 2, 3, and 5 above are:

a.prime costs

b.sunk costs

c.discretionary costs

d.relevant costs

e.differential costs

14) which of the following are alternatives to traditional budgeting approaches?

a.volume-based budgeting and zero-base budgeting (zbb)

b.activity-based budgeting (abb) and volume-based budgeting

c.kaizen budgeting and volume-based budgeting

d.activity-based budgeting (abb), kaizen budgeting, and zero-base budgeting (zbb)

e.activity-based budgeting (abb), kaizen budgeting, and volume-based budgeting

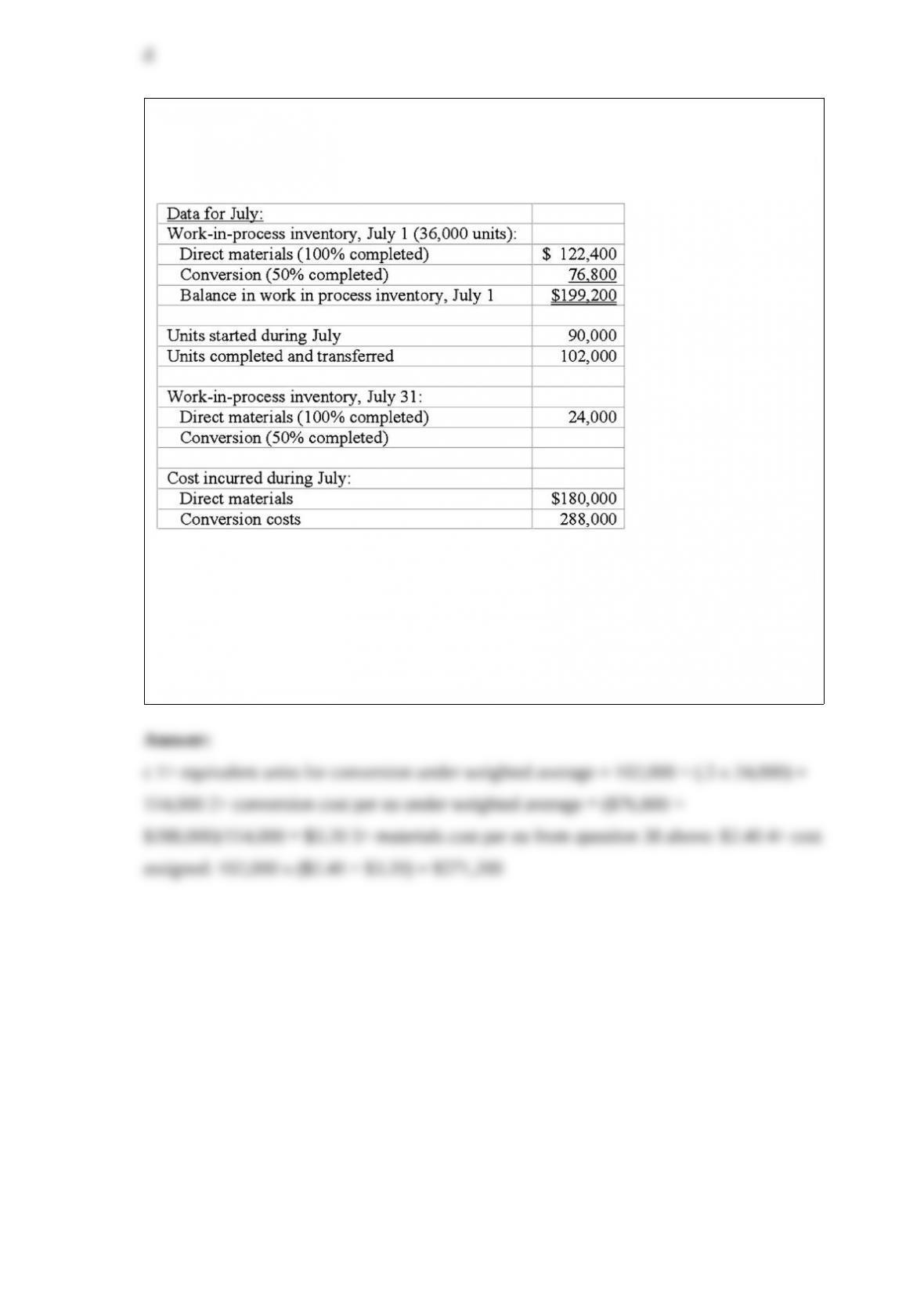

15) matrix inc. calculates cost for an equivalent unit of production using both the

weighted-average and the fifo methods.

the cost of goods completed and transferred out under the weighted-average method is

calculated to be:

a.$96,000

b.$476,400

c.$571,200

d.$484,000

e.$468,200