1) moss manufacturing has just completed a major change in its quality control (qc)

process. previously, products had been reviewed by qc inspectors at the end of each

major process, and the company’s ten qc inspectors were charged as direct labor to the

operation or job. in an effort to improve efficiency and quality, a computerized video qc

system was purchased for $250,000. the system consists of a minicomputer, 15 video

cameras, other peripheral hardware, and software.

the new system used cameras stationed by qc engineers at key points in the production

process. each time an operation changes or there is a new operation, the cameras are

moved, and a new master picture is loaded into the computer by a qc engineer. the

camera takes pictures of the units in process, and the computer compares them to the

picture of a “good” unit. any differences are sent to a qc engineer who removes the bad

units and discusses the flaws with the production supervisors. the new system has

replaced the ten qc inspectors with two qc engineers.

the operating costs of the new qc system, including the salaries of the qc engineers,

have been included as factory overhead in calculating the company’s volume-based

factory overhead rate which is based on direct labor dollars.

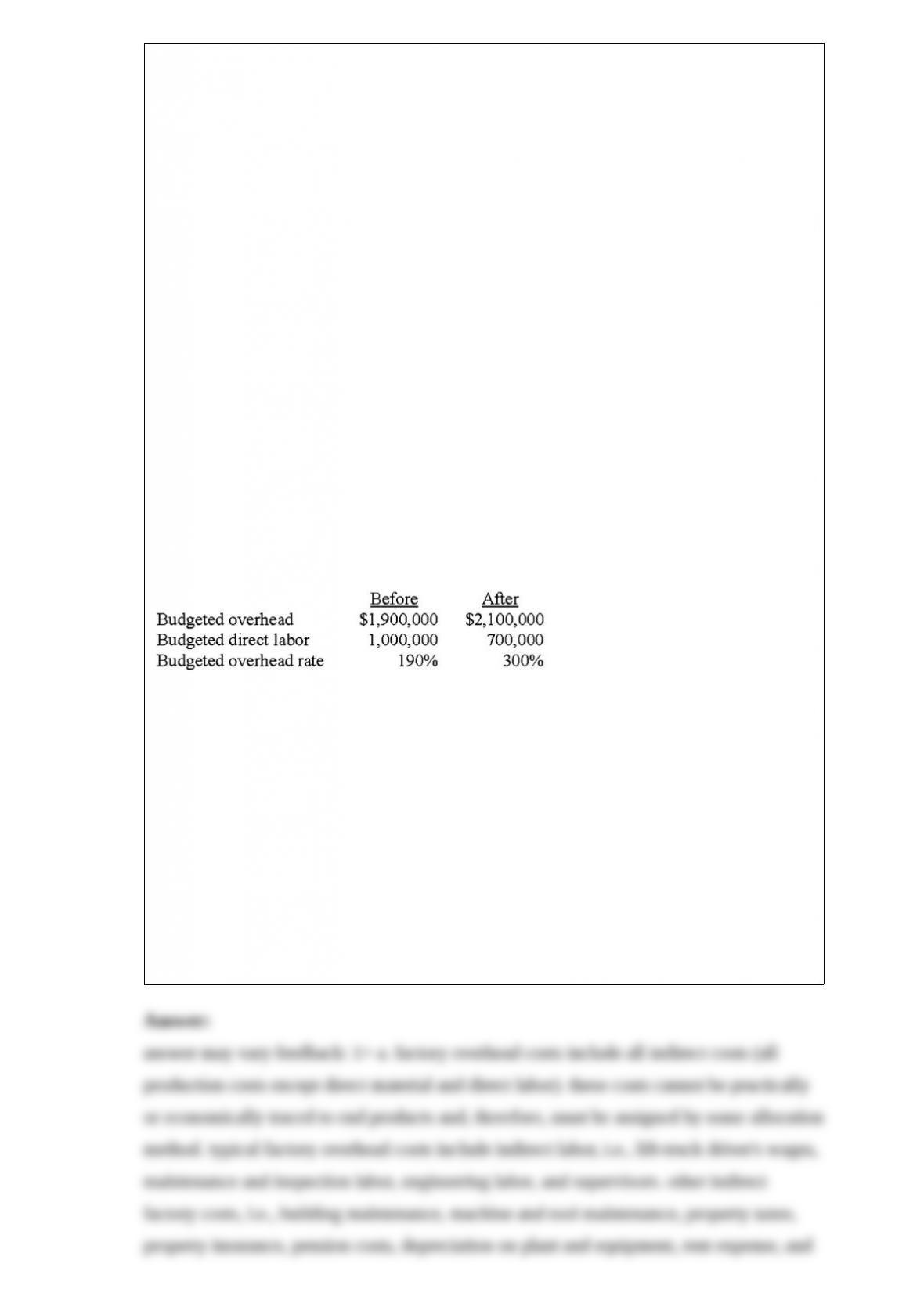

the company’s president is confused. his vice president of production has told him how

efficient the new system is, yet there is a large increase in the factory overhead rate. the

computation of the rate before and after automation is shown below.

“three hundred percent,” lamented the president, “how can we compete with such a high

factory overhead rate?”

required:

1> a. define factory overhead, and cite three examples of typical costs that would be

included in factory overhead.

b. explain why companies develop factory overhead rates.

2> explain why the increase in the overhead rate should not have a negative financial

impact on moss manufacturing.

3> explain, in the greatest detail possible, how moss manufacturing could change its

overhead accounting system to eliminate confusion over product costs.

2) a final step in the swot analysis is to identify quantitative measures for the:

a.value propositions

b.competitor analyses

c.critical success factors

d.both a and c

e.both b and c

3) midgettco.has accumulated data to use in preparing its annual profit plan for the

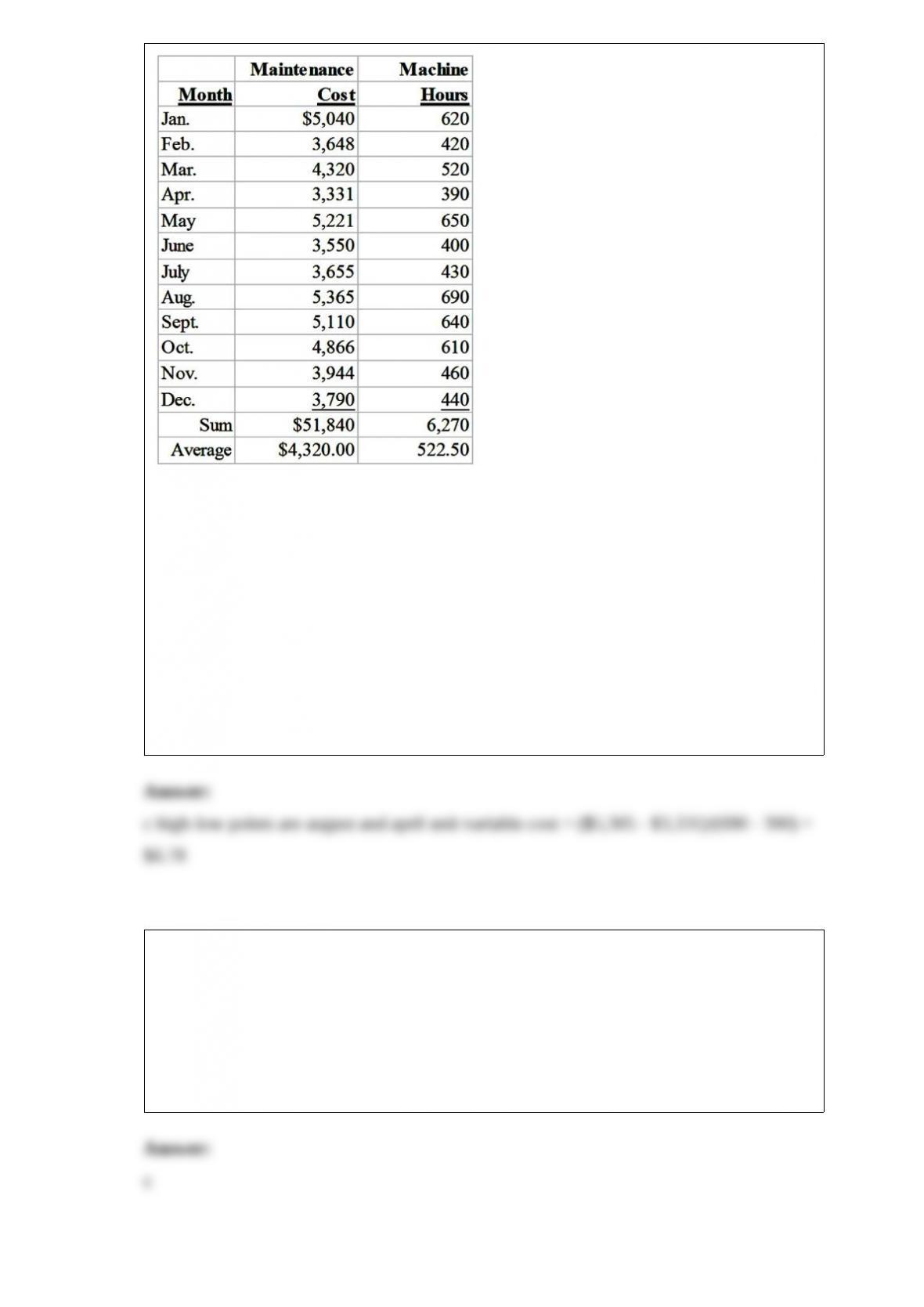

upcoming year. the cost behavior pattern of the maintenance costs must be determined.

the accounting staff suggested that linear regression be employed to derive an equation

for maintenance hours and costs. data regarding the maintenance hours and costs for the

last year and the results of the regression analysis are as follows:

average cost per hour ($51,840 6,270) = $8.27 (rounded to the nearest cent)

r = .99821

r2 = .99780

using the high-low method, unit variable cost is calculated to be(round to the nearest

cent):

a.$6.83

b.$8.67

c.$6.78

d.$7.88

e.$6.48

4) the competitive strategy of cost leadership allows a firm to outperform competitors

by producing products or services:

a.with reduced quality standards, thus reducing overall costs

b.in smaller operational units

c.at lower cost achieved by increased productivity

d.with attractive added features making the product more expensive, or “the cost leader”

e.that are heavily promoted and heavily warranted

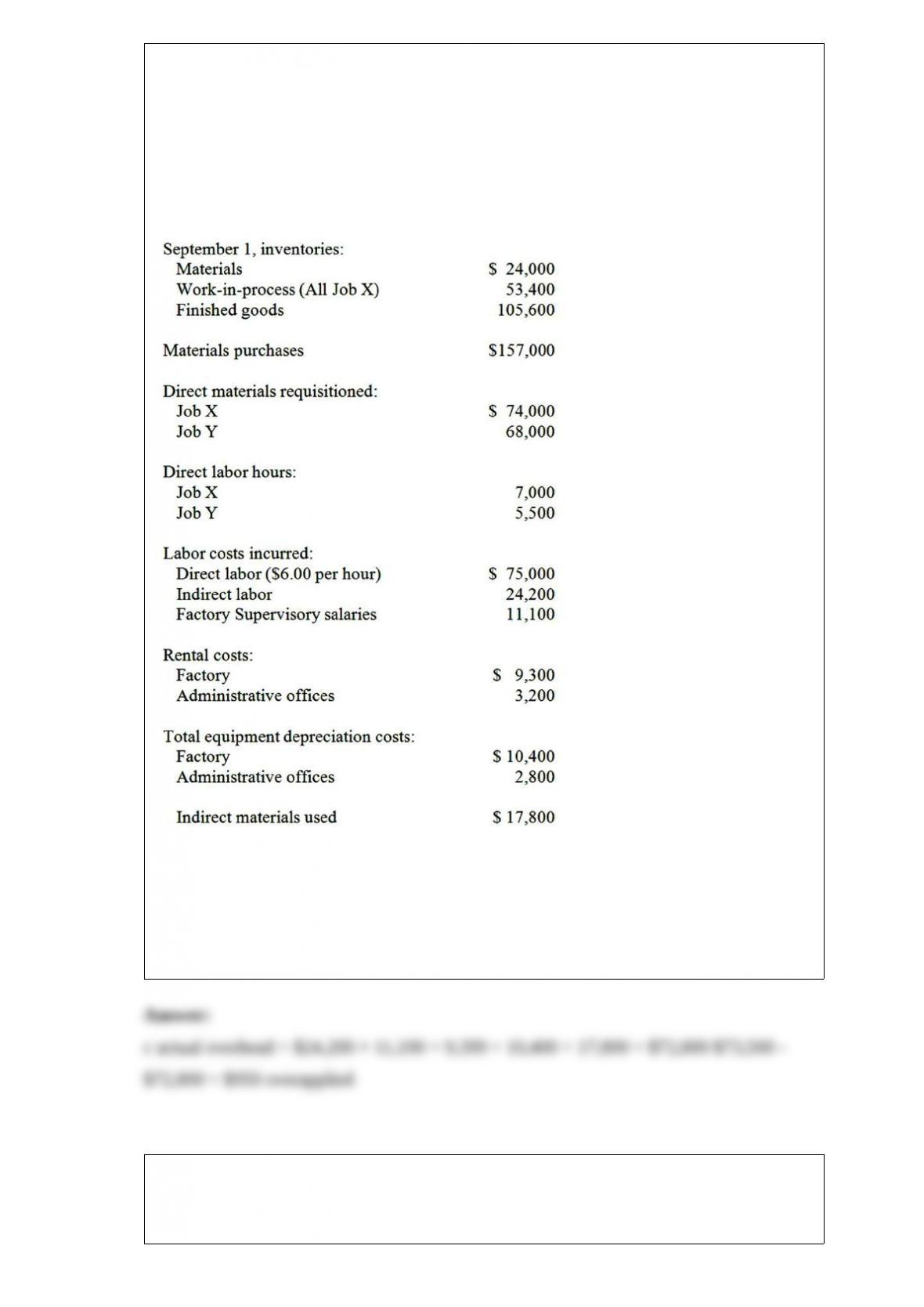

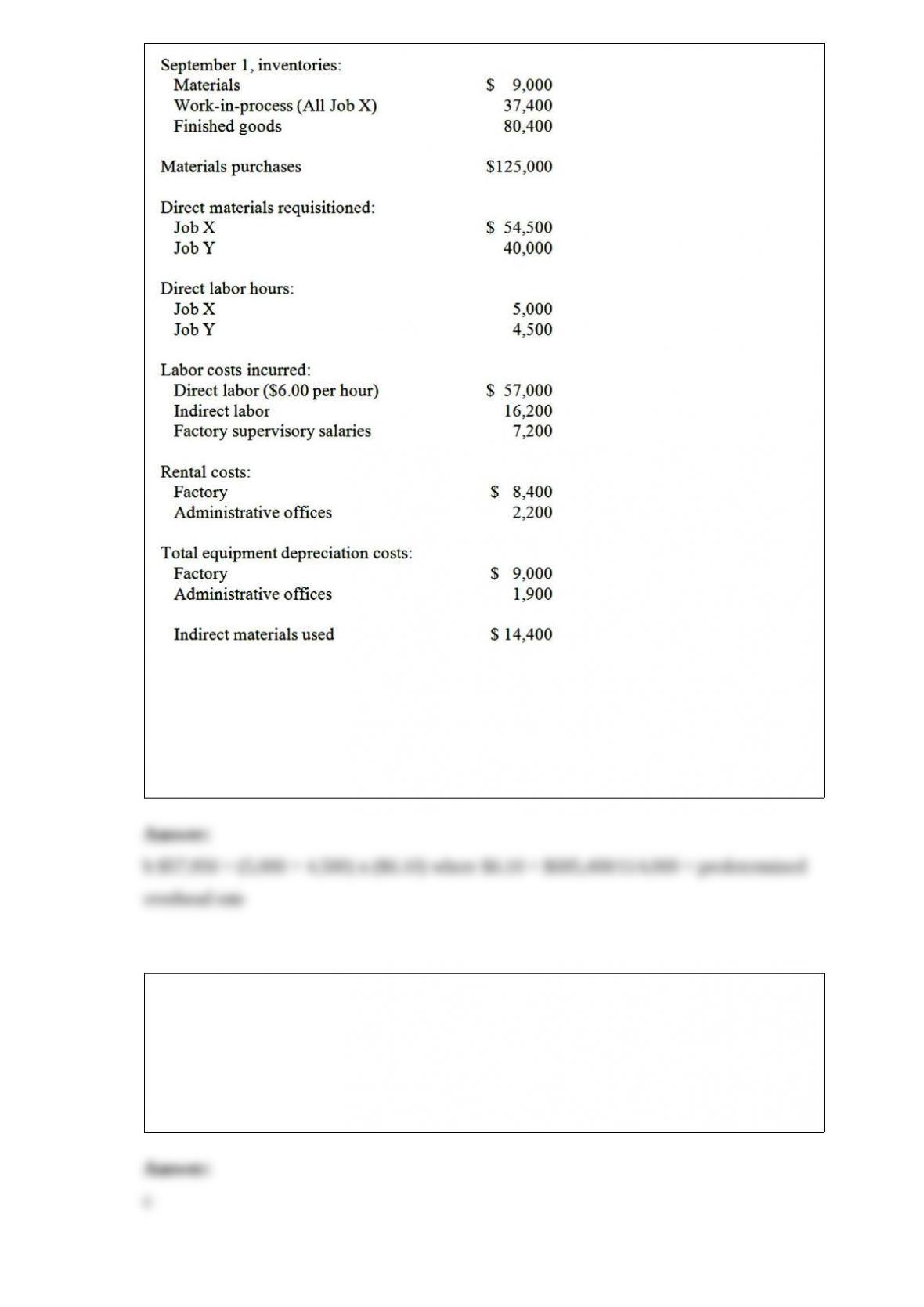

5) beckner inc. is a job-order manufacturer. the company uses a predetermined

overhead rate based on direct labor hours to apply overhead to individual jobs. for the

current year, estimated direct labor hours are 133,000 and estimated factory overhead is

$784,700. the following information is for september. job x was completed during

september, while job y was started but not finished.

the underapplied or overapplied overhead for september is:

a.$2,350 underapplied

b.$2,350 overapplied

c.$950 overapplied

d.$950 underapplied

e.$1,450 underapplied

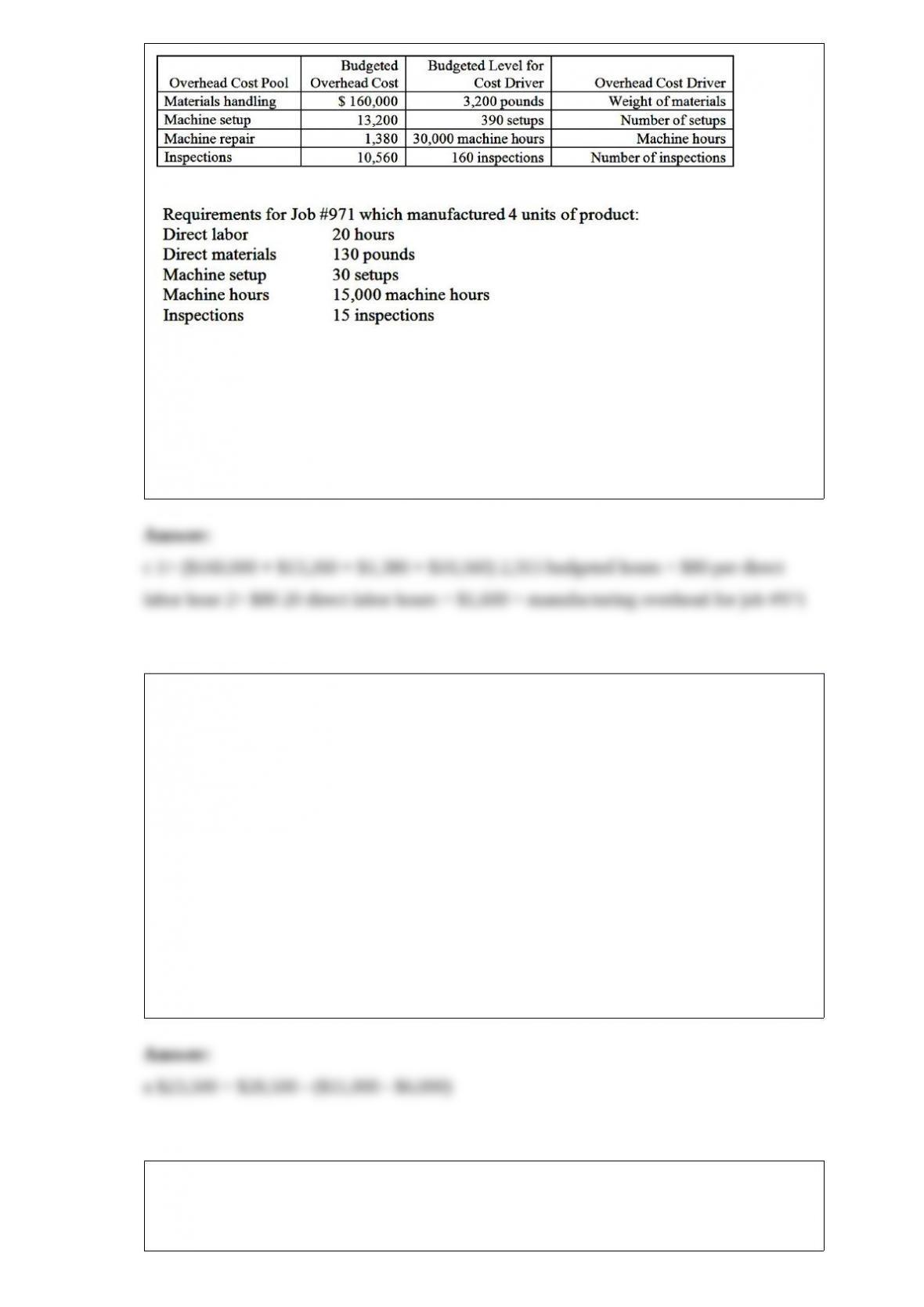

6) wings co. budgeted $555,600 manufacturing direct wages, 2,315 direct labor hours,

and had the following manufacturing overhead:

if wings uses a volume-based overhead rate based on direct labor hours, the

manufacturing overhead for job #971 is:

a.$990

b.$1,020

c.$1,600

d.$3,460

e.$6,400

7) conrad, inc. recently lost a portion of its records in an office fire. the following

information was salvaged from the accounting records.

direct labor cost incurred during the period amounted to 1.5 times the factory overhead.

the cfo of fisher, inc. has asked you to recalculate the following accounts and to report

to him by the end of the day.

what is the amount of direct materials purchased?

a.$23,500

b.$28,500

c.$31,000

d.$36,000

8) when significant differences exist in costs allocated to production departments, cost

management should use what method to find a more accurate cost allocation?

a.reciprocal method

b.step method

c.direct method

d.none of the above

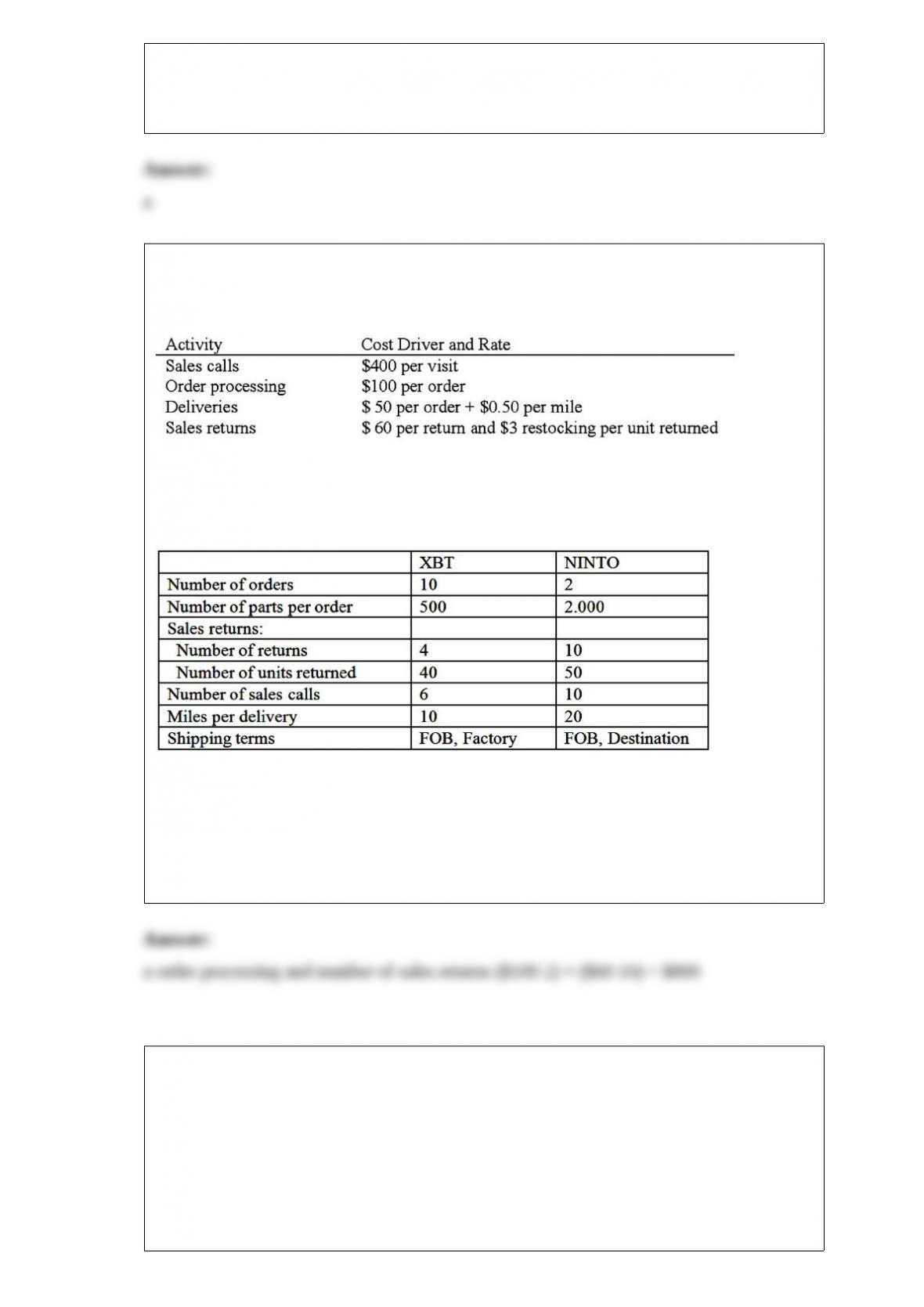

9) nerrod company sells its products at $500 per unit, net 30 . the firm’s gross margin

ratio is 40 percent. the firm has estimated the following operating costs:

nerrod company has gathered the following data pertaining to activities it performed for

two of its customers:

what is nerrod’s total customer batch-level cost applicable to ninto?

a.$800

b.$920

c.$2,300

d.$2,420

e.$6,300

10) the national sales manager for your company has pulled you aside and asked you to

prepare a sales document (bill) for one of the company’s largest clients before the end of

the fiscal year which ends this month. this sales document will include items that have

not yet been shipped and are not planned for shipment until after this fiscal year. what

should you do in this situation?

a.bill the client as asked by the national sales manager

b.bill the client since this is consistent with past transactions near fiscal year-end

c.contact the client and notify them that credit terms are being extended on this invoice

since the goods have not been shipped

d.discuss this situation with your supervisor

e.bring up the matter with the external auditor

11) when a firm is determining its opportunities and threats, which of the following

would not be mentioned?

a.an intense rivalry with a local competitor was beginning to start a price war

b.the firm just received a patent on its main product

c.the success of the firm’s latest marketing campaign

d.in spite of its patent, there are several substitute products consumers could use

e.increased competition in some of its key product lines

12) which one of the following is one of the key steps in determining process costs?

a.assigning the total manufacturing costs to the units completed and transferred out and

the units of work in process at the end of the period

b.analyzing the physical flow of production units

c.computing the cost per equivalent unit for each manufacturing cost element

d.calculating equivalent units of production for all manufacturing cost elements

e.all of the above are correct

13) the time ticket shows which amount for an employee?

a.the pay rate

b.number of hours a manager assigns

c.check-in times and check-out times

d.overtime costs

14) badour inc. is a job-order manufacturer. the company uses a predetermined

overhead rate based on direct labor hours to apply overhead to individual jobs. for the

current year, estimated direct labor hours were 114,000 and estimated factory overhead

was $695,400. the following information was for september. job x was completed

during september, while job y was started but not finished.

the total factory overhead applied during september is:

a.$59,300

b.$57,950

c.$57,848

d.$56,120

e.$57,710

15) fixed costs will often be irrelevant for decision making because they:

a.do not vary on a per-unit-of-output basis

b.are the same each time period

c.typically do not differ between and among decision alternatives

d.are not committed

e.cannot be estimated with precision

16) a group of related products may be referenced as:

a.cost objects

b.cost drivers

c.value streams

d.cost pools

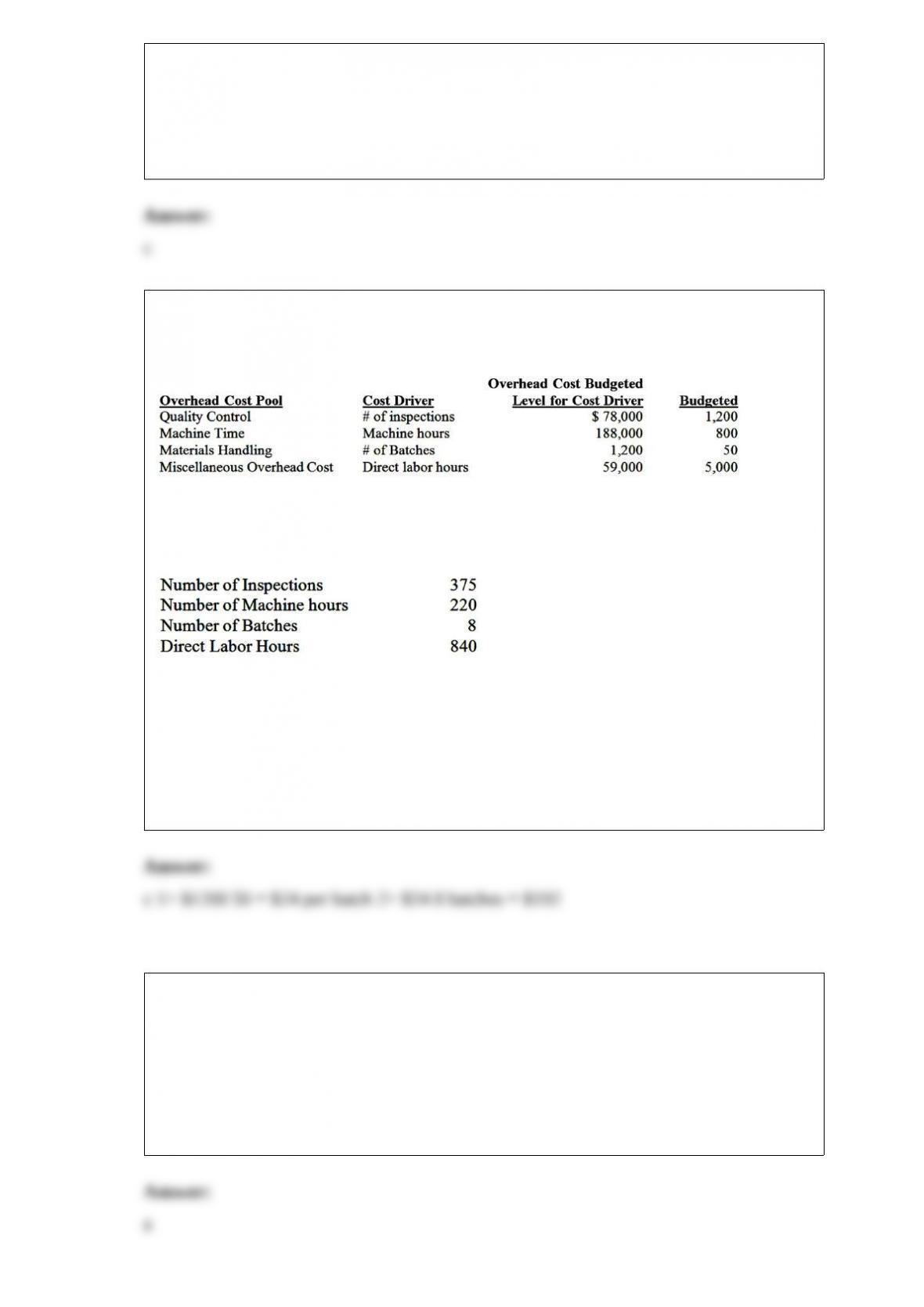

17) diamond cleats co. manufactures cleats for baseball shoes. it has outlined the

following overhead cost drivers:

diamond cleats co. has an order for cleats that has the following production

requirements:

using activity-based costing, applied materials handling factory overhead for the

baseball cleat order is:

a.$338

b.$584

c.$192

d.$353

e.$686

18) cost allocation is an important strategic issue for u.s. manufacturing firms is with

foreign subsidiaries because of:

a.the tax implications

b.quality concerns

c.import restrictions

d.cultural differences

e.the company’s desire to grow

19) brownsville novelty store prepared the following budget information for the month

of may:

sales are budgeted at $360,000. all sales are on account and a provision for bad debts is

made

monthly at three percent of sales.

inventory was $84,000 on april 30 and an increase of $12,000 is planned for may 31 .

all inventory is marked to sell at cost plus fifty percent.

estimated cash disbursements for selling and administrative expenses for the month are

$48,000.

depreciation for may is projected at $6,000.

brownsville’s budgeted cost of inventory purchased in may is:

a.$120,000

b.$180,000

c.$198,000

d.$252,000

e.$240,000

20) which of the following does not represent a main focus of cost management

information?

a.strategic management

b.performance measurement

c.planning and decision making

d.preparation of financial statements

e.internal audit and control

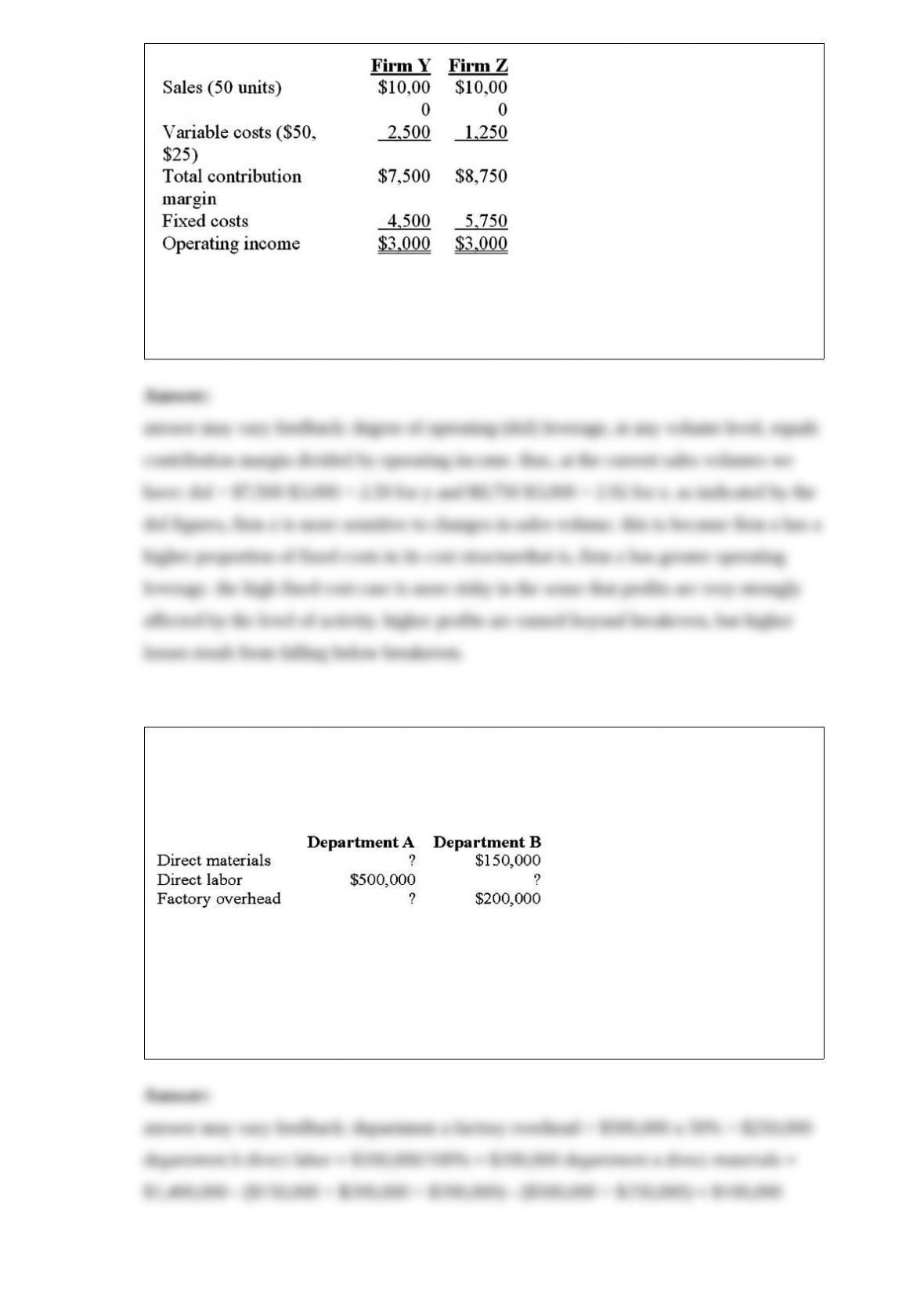

21) firms y and z both produce and sell small gasoline engines. the sales price is $200

per engine. data for both firms at a sales volume of 50 units are as follows:

required: from the existing level of sales, which firm’s operating income is more

sensitive to changes in sales volume? show calculations and round your answers to 2

decimal places.

22) harrison allocates factory overhead on the basis of direct labor cost. the overhead

rates for the year are 50% for department a and 100% for department b. harrison started

and completed job m15 during may. the costs of job m15 are summarized below.

the total manufacturing costs assigned to job m15 during may were $1,400,000.

required:

calculate the missing (?) costs (department a direct materials and factory overhead and

department b direct labor).

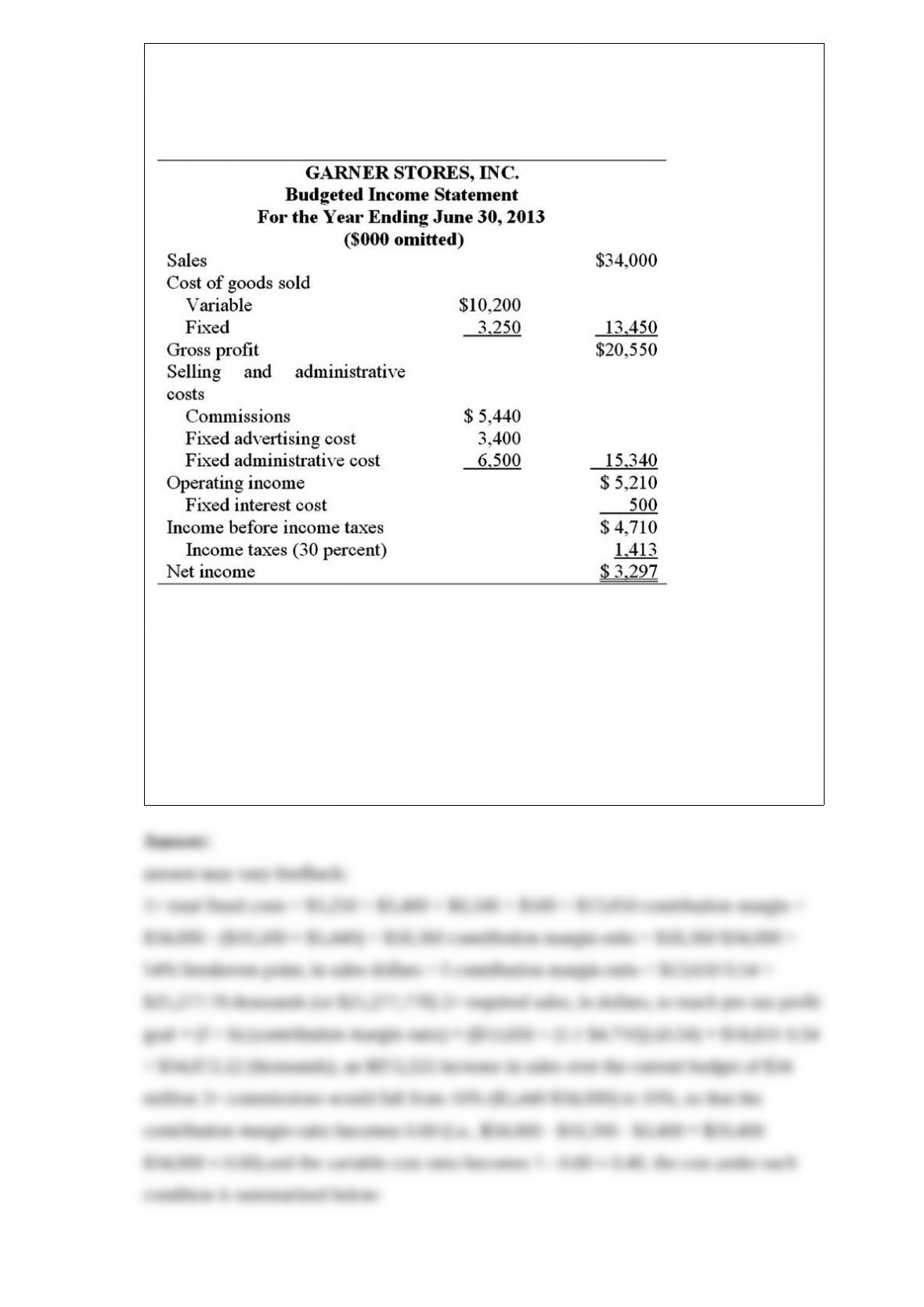

23) garner stores, inc. is a multiple-store chain retailer of women’s clothing. you are

provided with the following budgeted income statement for the coming year.

required:

1> determine the breakeven point in dollars for 2013 .

2> what is the required sales dollars if desired profit is to increase by 10% over the

budgeted pre-tax profit?

3> what is the indifference point between reducing the commissions to 10% of sales

dollars, and at the same time increasing sales salaries by $2.4 million, relative to the

current budget?

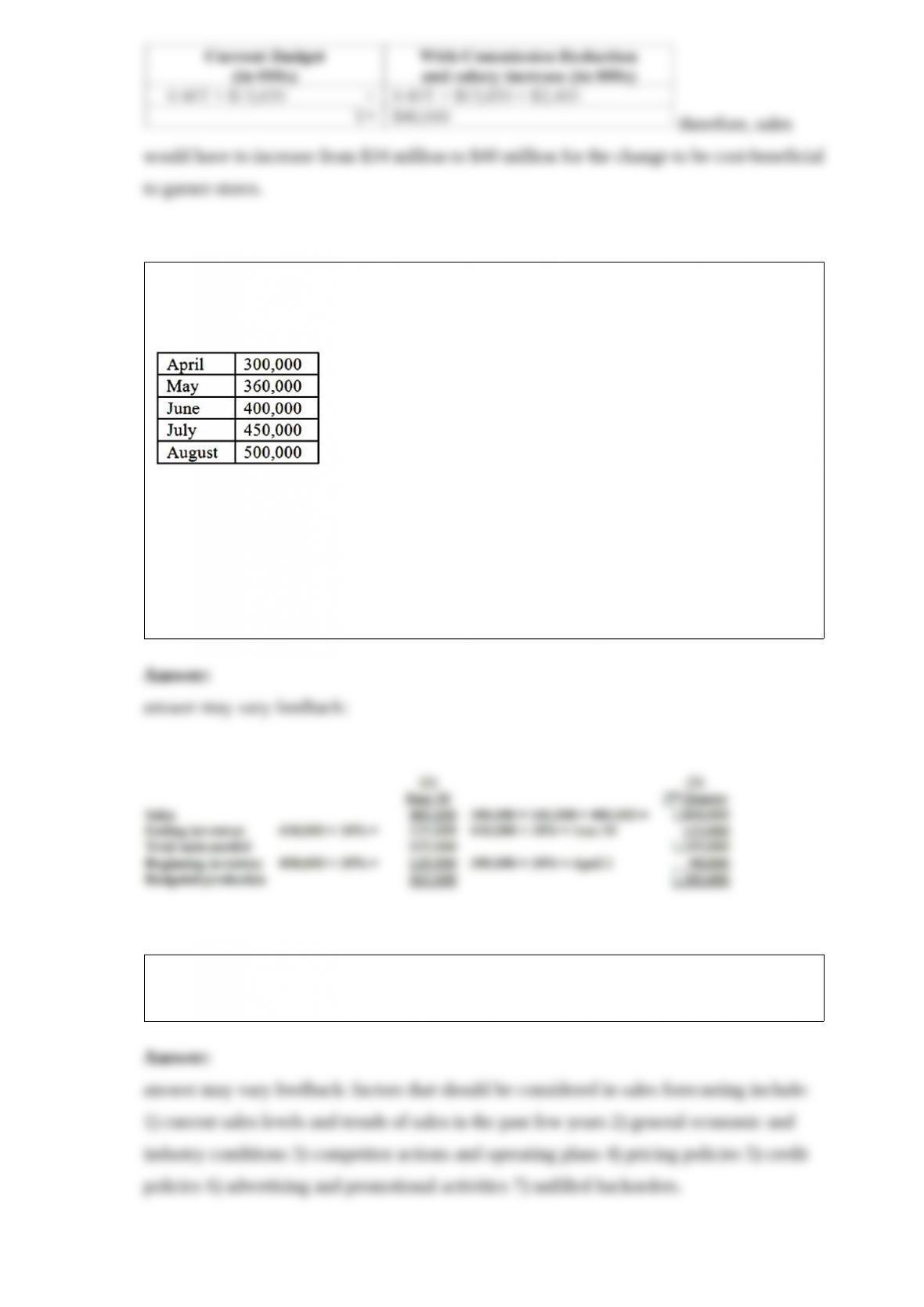

24) papa joe, inc., is preparing its budget for the second quarter of the calendar year. the

following unit sales data have been forecasted:

desired ending inventory each month: 30% of next month’s estimated sales (in units)

required:

1> how many units should be budgeted for production in june?

2> how many units should be budgeted for production in the second quarter?

25) list factors that should be considered in developing a sales forecast for an upcoming

budget period.

26) andrews & henderson inc. is a manufacturer of mining equipment in colorado. eric

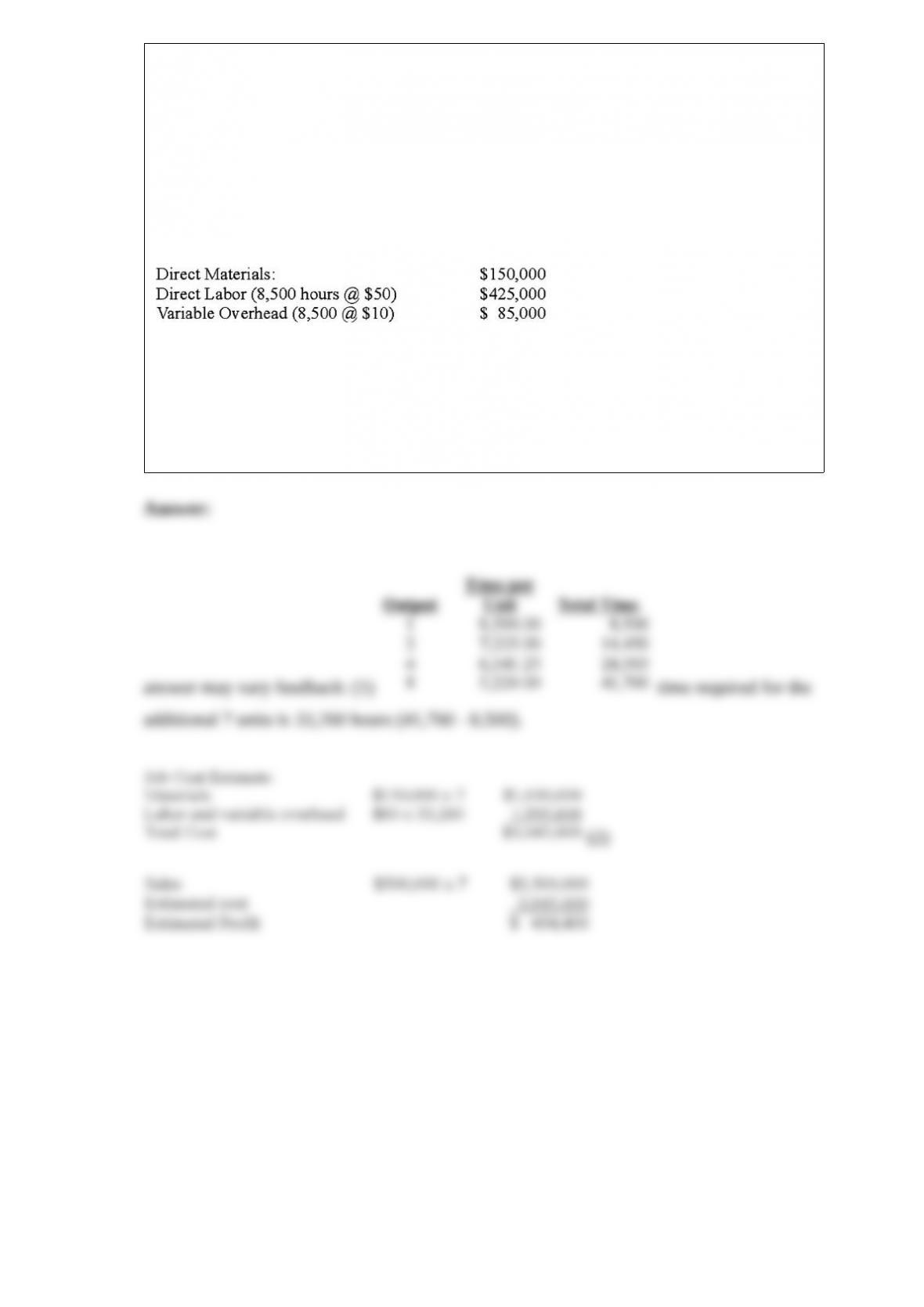

andrews, the founder of the corporation, has just won a new contract from shakley inc.

to build seven new tunneling machines for a price of $500,000 each. the machines are

to be delivered in the next seven months. the costs associated with the production of the

first machine are listed below. eric estimates that an 85% cumulative average learning

rate exists for these types of projects.

following is the cost information for the first tunneling machine:

required:

(1) prepare an estimate of the total hours for producing the second through eighth

machines.

(2) determine the expected profit from this project.