Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–31

Reference: Pierce, L. and J. Snyder. (2008). “Ethical Spillovers in Firms:

Evidence from Vehicle Emissions Testing.” Management Science 54 (11):

pp 1891-1903.

18–39 Allocation of Central Costs; Profit Centers (30 min)

1. Allocation based on revenue

Allocation Base Pine Valley Oak Glen Mimosa Birch Glen Total

Revenue $5,350 $7,995 $8,857 $6,550 $28,752

Percentage 18.6074% 27.8068% 30.8048% 22.7810%

Alocated Cost $3,522 $5,264 $5,831 $4,312 18,930$

Operating Margin $1,828 $2,731 $3,026 $2,238

Operating Margin % 34.2% 34.2% 34.2% 34.2%

Note that the allocation based on revenue shown above means that

the operating margin (operating margin/revenue) is the same for all

administrative and executive salaries are closely related to revenue.

Also, the cost of front office personnel is likely to be related to same

measure of the number of customers of the resort. Perhaps the

number of rooms is a better measure of the usage of the cost of front

office personnel.

2. There are a number of possible answers. A useful starting point for

class discussion might be the following solution:

The four allocation bases are revenues, square feet, number of

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–32

18-39 (continued -1)

Square Feet: carpet cleaning, contract to repaint rooms; it could be

argued that these costs are driven by the size of the areas to be

cleaned and painted

Total cost: $450 = $50 + $400

Number of rooms: front office personnel, housekeeping, room

maintenance; the number of guests drives these costs, and the

number of rooms is used as a surrogate

Revenue cost pool: advertising, depreciation on reservations

computer system, administrative and executive salaries. These are

the office costs that cannot be traced to one of the above costs

drivers (square feet, number of rooms, assets), but using the ability to

3. Cost Allocation

This part can be compared to the application of ABC costing in

chapter 5; the goal is to allocate costs in a manner that most nearly

reflects the consumption of the costs.

The allocation using the multiple cost pools is preferred because it

allocates costs in a manner more closely related to the cause-effect

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18-39 (continued –2)

Allocation Based on Cost Pools

Allocation Base Pine Valley Oak Glen Mimosa Birch Glen Total

Revenue $5,350 $7,995 $8,857 $6,550 $28,752

Percentage 18.6074% 27.8068% 30.8048% 22.7810%

Square feet 55,475 76,599 41,774 83,664 257,512

Percentage 21.5427% 29.7458% 16.2222% 32.4894%

Number of Rooms 86 122 66 174 448

Percentage 19.1964% 27.2321% 14.7321% 38.8393%

Assets $92,345 $136,745 $72,355 $57,499 $358,944

Percentage 25.727% 38.096% 20.158% 16.019%

Cost Allocation

Allocated Base Pine Valley Oak Glen Mimosa Birch Glen Total

Revenue $871 $1,301 $1,442 $1,066 $4,680

Square feet 97 134 73 146 $450

Number of Rooms 2,073 2,941 1,591 4,195 $10,800

Assets 772

1,143

605

481

$3,000

Total Cost Allocated $3,813 $5,519 $3,710 $5,888 $18,930

Operating Margin $1,537 $2,476 $5,147 $662

Operating Marigin % 28.73% 30.97% 58.11% 10.11%

Comparison of Allocation Methods

Allocation Pool–Based 3,813$ 5,519$ 3,710$ 5,888$ 18,930$

Revenue-Based 3,522 5,264 5,831 4,312 18,930$

Difference 290$ 255$ (2,121)$ 1,575$

The allocation rates for each of the four cost drivers are determined above.

Note the large differences between the rates for revenue and for the

number of rooms; relative to Oak Glen, Pine Valley is a smaller resort with

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–34

18–39 (continued –3)

Based on the relationship between revenue and number of rooms,

the result is that Pine Valley and Oak Glen’s cost allocation and operating

margin are similar under the revenue-only and the multiple-driver

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–35

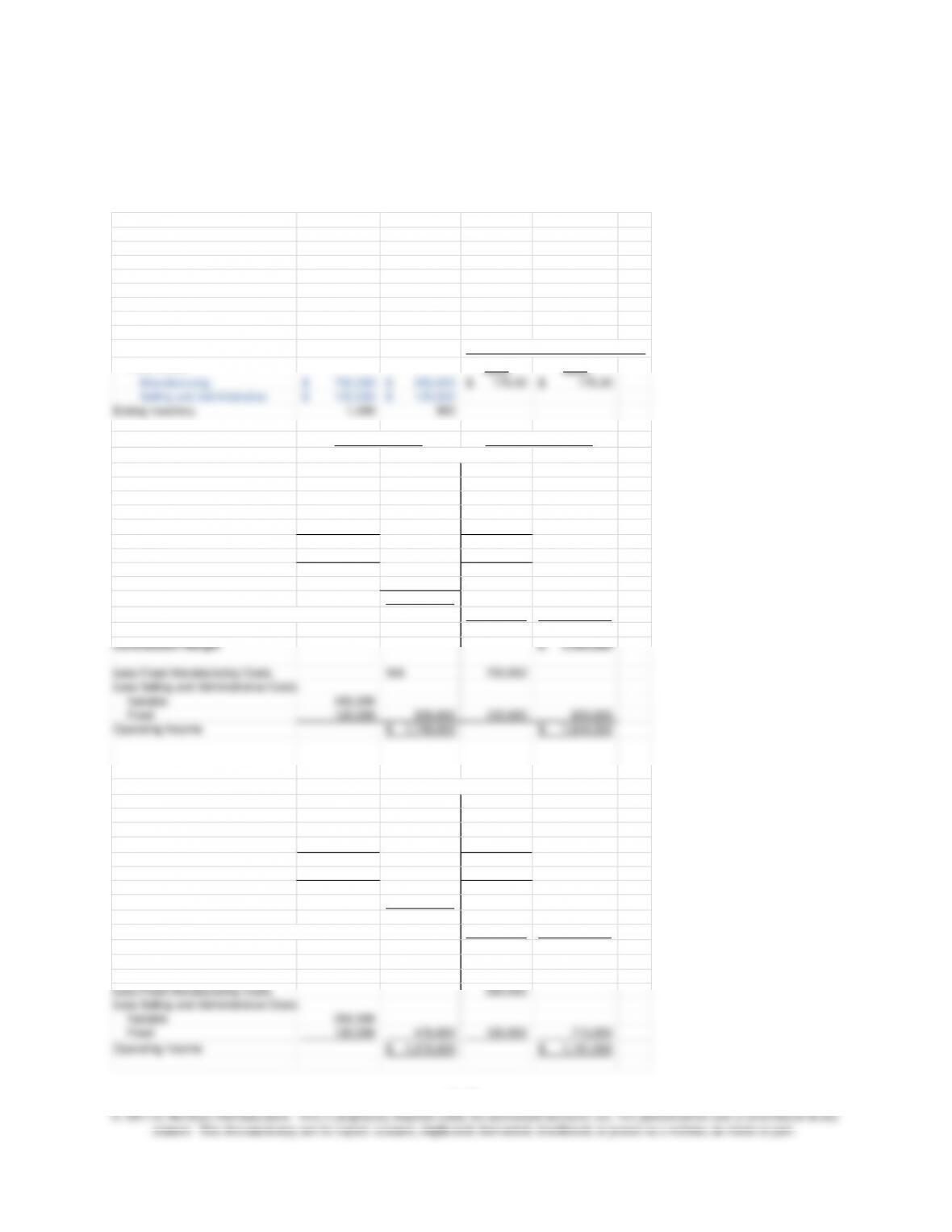

18-40 Profit Centers: Comparison of Variable and Full Costing (20

min)

1.

DATA SUMMARY 2012 2013

Units

Beginning Inventory 0200

Price 3.00$ 3.00$

Sold 1,800 2,200

Produced 2,000 2,000

Unit Variable Costs

Manufacturing 0.60$ 0.60$

Selling and Administrative 0.40$ 0.40$

Fixed Costs

Selling and Administrative 500$ 500$

Manufacturing – Total 1,000$ 1,000$

– Per unit 0.50$ 0.50$

Full Manufacturing Cost per unit 1.10$ 1.10$

PART TWO

Income Statement for 2012

Sales (1,800 x $3) 5,400$ 5,400$

Less: Cost of Goods Sold

Beginning Inventory – –

Cost of Production (2,000 x $1.10; 2,000x$.6) 2,200$ 1,200$

Contribution Margin 3,600$

Less Fixed Manufacturing Costs 1,000

Less Selling and Administrative Costs

Variable (1800x$.40) 720

Fixed 500 1,220 500 1,500

Operating Income 2,200$ 2,100$

Income Statement for 2013

Sales 6,600$ 6,600$

Less: Cost of Goods Sold

Beginning Inventory 220$ 120$

Less Selling and Administrative Costs

Variable 880

Fixed 500 1,380 500 1,500

Operating Income 2,800$ 2,900$

Full Costing

Variable Costing

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–36

18-40 (continued -1)

Reconciling Difference in Operating Income between Full and Variable Costing

2012 2013

Change in Inventory in Units 200 (200)

Multiply times Fixed Overhead Rate 0.50$ 0.50$

=Difference in Operating Income 100$ (100)$

(A negative number means variable costing net income is higher)

An increase in inventory units means full costing operating income is

higher than variable costing operating income.

A decrease in inventory units means variable costing operating income is

higher than full costing operating income.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–37

18-41 Full versus Variable Costing (25 min)

1.

DATA SUMMARY 2012 2013

Units

Beginning Inventory 0 1,000

Price 55.00$ 55.00$

Sold 24,000 26,000

Produced 25,000 25,000

Unit Variable Costs

Manufacturing 16.00$ 16.00$

Selling and Administrative 0.50$ 0.50$

Fixed Costs

Selling and Administrative 500$ 500$

Manufacturing – Total 200,000$ 200,000$

– Per unit 8.00$ 8.00$

Full Manufacturing Cost per unit 24.00$ 24.00$

PART TWO

Income Statement for 2012

Sales (24,000 x $55) 1,320,000$ 1,320,000$

Less: Cost of Goods Sold

Beginning Inventory – –

Cost of Production (25,000x$24;25,000x$16) 600,000$ 400,000$

Available for Sale 600,000 400,000

Less Ending Inventory (1,000x$24;1,000x$16) 24,000 16,000

Cost of Goods Sold 576,000 384,000

Less Fixed Manufacturing Costs 200,000

Less Selling and Administrative Costs

Variable (24,000x$0.50) 12,000

Fixed 500 12,500 500 200,500

Operating Income 731,500$ 723,500$

Income Statement for 2013

Sales 1,430,000$ 1,430,000$

Less: Cost of Goods Sold

Beginning Inventory 24,000$ 16,000$

Cost of Goods Produced 600,000 400,000

Available for Sale 624,000 416,000

Less Ending Inventory – –

Cost of Goods Sold 624,000 416,000

Plus Variable Selling and Administrative 13,000 429,000

Operating Income 792,500$ 800,500$

Full Costing

Variable Costing

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–38

18-41 (continued –1)

Reconciling Difference in Operating Income between Full and Variable Costing

2012 2013

Change in Inventory in Units 1,000 (1,000)

Multiply times Fixed Overhead Rate 8.00$ 8.00$

=Difference in Operating Income 8,000$ (8,000)$

(A negative number means variable costing income is higher)

An increase in inventory units means full costing operating income is higher

than variable costing operating income.

A decrease in inventory units means variable costing operating income is

higher than full costing operating income.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–39

18-42 Profit Centers: Comparison of Variable and Full Costing

(Underapplied Overhead) (30 min)

1., 2.

DATA SUMMARY 2012 2013

Units

Beginning Inventory 800 1,400

Price 2,095$ 1,995$

Sold 3,200 2,800

Actual Production 3,800 2,300

Budgeted Production 4,000 3,400

Unit Variable Costs

Manufacturing 1,200$ 1,200$

Selling and Administrative 125$ 125$

Fixed Costs 2012 2013

Manufacturing 700,000$ 595,000$ 175.00$ 175.00$

Selling and Administrative 120,000$ 120,000$

Ending Inventory 1,400 900

PART TWO

Income Statement for 2012

Sales 6,704,000$ 6,704,000$

Cost of Goods Sold:

Beginning Inventory 1,100,000 960,000

Cost of Goods Produced 5,225,000 4,560,000

Adjust: Production Volume Variance 35,000

Adjusted Cost of Goods Sold 4,435,000

Plus Variable Selling and Administrative 400,000 4,240,000

Gross Margin 2,269,000$

Contribution Margin 2,464,000$

Less Fixed Manufacturing Costs N/A 700,000

Less Selling and Administrative Costs

Variable 400,000

Fixed 120,000 520,000 120,000 820,000

Operating Income 1,749,000$ 1,644,000$

Income Statement for 2013

Adjust: Production Volume Variance 192,500

Adjusted Cost of Goods Sold 4,042,500

Plus: Variable Selling and Administrative 350,000 3,710,000

Gross Margin 1,543,500$

Contribution Margin 1,876,000$

Less Fixed Manufacturing Costs 595,000

Less Selling and Administrative Costs

Variable 350,000

Fixed 120,000 470,000 120,000 715,000

Operating Income 1,073,500$ 1,161,000$

Fixed Manufacturing Cost Per Unit

Full Costing

Variable Costing

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–40

18–42 (continued -1)

2. (continued)

Reconciling Difference in Net Income betwee Absoprtion and Variable Costing

2012 2013

Change in Inventory in Units 600 (500)

Multiply times Fixed Overhead Rate 175$ 175$

=Difference in Net Income 105,000$ (87,500)$

(A negative number means variable costing net income is higher)

An increase in inventory units means full costing operating income is higher

than variable costing operating income.

A decrease in inventory units means variable costing operating income is

higher than full costing operating income.

Additional Note on the Production Volume Variance: A recent CFO

magazine item notes how the use of full cost accounting in the auto

industry has biased profit reporting in that industry. See, Marielle Segarra,

“Accounting: Lots of Trouble,” CFO, March 2012, pp. 29-30.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–41

3.

Memo

TO: Mr. Mark Hancock

FROM:

DATE:

The difference in operating income between variable costing

and full costing is due to the fact that the level of units in finished

goods inventory increased by 600 units (from 800 to 1,400) in 2012

and decreased by 500 units (from 1,400 to 900) in 2013. The

variable cost income statements do not include fixed manufacturing

costs in inventory, but treat these costs instead as a cost of the

current period. Thus, variable costing income statements are not

affected by changes in inventory levels.

You may use the variable cost income statements as a more

reliable measure of operating income when fixed manufacturing costs

are high and inventory changes significantly, as in this case. The

income figures for the full costing method, in contrast, do include

fixed cost in inventory, and thus are biased by the changes in

variable cost statements.

Note that the production volume variance does not affect the

difference between variable and full costing income. The difference in

income is fully explained by the change in inventory multiplied times

the fixed overhead rate, as illustrated in the end of part 2 above.

18–42

18-43 Balanced Scorecard (15 min)

Solution for problem 2-35

1. Medical University’s strategy should encompass a focus on the

quality of its clinical care, education, and research. The relative size

of the healthcare system is important as a way to attract third party

payers, providers, and patients. A large hospital system tends to

offer a greater breadth of services, which often increases the

clinician’s level of expertise. A physician at a larger institution will

and public relations departments are very crucial to its success. It is

also essential that the healthcare system stay within its budget in

order to continue operations.

2. Yes. The balanced scorecard goes beyond simply monitoring

financial performance. Because the four areas: financial

performance, customer satisfaction, internal processes, and learning

3.

• Financial: operating margin, cost per discharge, days in accounts

receivable

• Customer: patient satisfaction, employee satisfaction, referring

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–43

18-43 (continued -1)

4. One of the hardest challenges is convincing employees that the

balanced scorecard is not simply a management tool. The reluctance

of employees to implement the balanced scorecard may prevent the

organization from achieving its strategic goals. In order to increase

their personal and professional goals. Organizations must explain

what the balanced scorecard means to its employees in order to

prevent them from dismissing the initiative as the latest strategic

management tool.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–44

18-44 Balanced Scorecard (15 min)

Solution for problem 2-39; Balanced Scorecard for Fowler’s Farm

There are a number of possibilities for determining both the number

and types of perspectives for the balanced scorecard, and for

determining the critical success factors which belong under each

perspective. The answer below is representative of a balanced

scorecard that would be a good fit for the Fowler farm. This

scorecard puts the operations and financial perspectives first, to

and performance – it requires a quantitative measure.

Operations

crop rotation; number of fields in rotation

inventory of supplies and parts, by type of equipment, cost and

date purchased

weather forecast, days missed, important weather changes

cost of materials; fertilizer, fuel, etc.

cost of labor; by type of employee

prices received for each major product

interest cost

Employees

turnover (number and percent)

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–45

18-44 (continued –1)

Regulatory Compliance and Environmental

compliance with local, state and federal laws on tobacco

farming

compliance with FDA regulations regarding handling raw milk

usage of restricted chemicals known to have negative

environmental effects (amount, percent)

Customer

orders shipped on time (number and percent)

quality complaints (number, percent)