Chapter 19 – Strategic Performance Measurement: Investment Centers

19-1

Chapter 19

Strategic Performance Measurement: Investment Centers

Teaching Notes for Cases

Case 19-1: Investment Centers

1. The prior performance measurement system was called “performance income,” and is best described as

a profit center method. The focus was on divisional profits.

2. The new system called “asset management,” is best described as an investment-center method. The

system is focused on return on investment (ROI), as described in the case, where it is called “return on

capital.” The advantage of the investment-center approach is that it focuses managers’ attention on the

management of assets. Also, it brings managers’ incentives in line with that of the entire firm, to increase

the ROI of the firm.

The change to an investment center is consistent with Polymer’s new strategy, which is to

withdraw from activities, which do not fit the overall firm’s competitive advantage. The investment-

center approach is useful here to identify those units where the profitability is marginal, since the firm

wishes to focus on the most profitable units, and divest or consolidate the others. ROI provides a useful

basis to make this analysis. Thus, choosing investment centers is consistent with the present competitive

strategy.

ROI is often the desired performance measure in firms such as Polymer, where the activities are

diverse and complex, and comparison among the activities is difficult.

3. A common view is that foreign exchange gains and losses are a non-controllable element that should be

excluded from the manager’s evaluation. In contrast, many now view the manager’s responsibility more

broadly and urge that foreign exchange can be managed. The potential for exchange rate losses can be

managed by hedging, that is, purchasing financial instruments, which protect the firm from significant

swings in currencies. A common argument is that the firm is in the business of making and selling

products and services, and the management of foreign exchange can be delegated to financial service

firms, banks, etc., which will provide the desired hedging. The cost of hedging is small relative to the

potential losses.

Also, managers can adapt to foreign exchange changes by relocating manufacturing and other

activities over the longer term. Overall, the firm should be watchful of what individual managers are

doing to adapt to foreign exchange changes, both favorable and unfavorable. For this reason, it is

desirable to include foreign exchange gains and losses in the manager’s performance evaluation, as

Polymer Products is doing.

Income taxes, like foreign exchange, are often viewed as uncontrollable to the manager.

However, this overlooks the fact that the manager can often take steps to reduce taxes, by relocating

operations and changing sources of supply, etc. Thus, in a manner similar to that of foreign exchange

noted above, it is desirable for income taxes to be also included in the manager’s performance evaluation.

This places the appropriate incentive for the manager to reduce taxes for the benefit of the firm as a

whole.

A common problem with both profit centers and investment centers is that the performance

measures promote short-term decision making. In this case, Polymer Products has adopted a

“performance shares” approach. This is described in the next to last paragraph of the case: “...stock which

is accessible only after 3 years…” Performance shares are a type of deferred income in which the

compensation to the manager depends on the success of certain critical financial and non-financial

measures over a period of time (see Chapter 20 for a discussion of this method). In effect, Polymer

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-2

Products has recognized the inherent bias to the short-term in the ROI measure, and is using performance

shares to provide an incentive for longer term thinking and action by the managers.

Case 19-2: Transfer Pricing

1. In order to maximize short-run contribution margin, the Cole Division should accept the contract from

Wales Company. This conclusion is supported by the following calculations ($000‘s omitted throughout

the calculations.). See graphic below which shows product flows, prices and variable costs to assist in

understanding the analysis.

From the Cole Division Point of view

a. Cole transfers to Diamond

Transfer price: Cole to Diamond

(3,000 units @ $1,500 each) $4,500

Variable cost:

Purchase from Bayside

(3,000 units @ $600 each) $1,800

Processing by Cole

(3,000 units @ $500 each) 1,500

Total variable cost 3,300

Contribution margin $1,200

b. Cole accepts Wales contract

Selling Price (3,500 units @ $1,250 each) $4,375

Variable cost:

Purchase from Bayside

(3,500 units @ $500 each) $1,750

Processing by Cole

(3,500 units @ $400 each) 1,400

Total variable cost 3,150

Contribution margin $1,225

Conclusion for the Cole Division

Contribution margin from Wales contract $1,225

Contribution margin from Diamond sale 1,200

Difference in favor of Wales contract $ 25

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-3

From the point of view of the cost to the entire company:

a. Cole transfers to Diamond

Variable cost

Bayside

(3,000 units @ $300 each) $900

Cole

(3,000 units @ $500 each) 1,500

Total variable cost $2,400

b. Cole accepts Wales contract; then the following shows the three parts to the calculation, including

the opportunity cost of lost contribution to Bayside and Cole:

1. Contribution of Wales Contract to Cole

Selling Price (3,500 units @ $1,250 each) $4,375

Variable cost:

Purchase from Bayside

(3,500 units @ $250 each) $875

Processing by Cole

(3,500 units @ $400 each) 1,400

Total variable cost 2,275

Contribution to Cole $2,100

2. Plus: Contribution of London Contract to Bayside

Selling Price (3,000 × $400) $1,200

Variable Cost (3,000 × $200) 600

Contribution to Bayside $600

3. Less: Cost of outside purchase to Diamond

Selling price to Diamond: (3,000 × $1,500) $4,500

Net Cost to the company of the Wales contract to Cole

= $4,500 – $600 – $2,100 $1,800

Conclusion for the Entire Company; Relevant Costs

Cole Transfers to Diamond $2,400

Cole Sells to Wales 1,800

Difference favoring the Wales Contract $ 600

It appears that the solution is to have Cole Division accept the Wales contract, either from the division’s

or the company’s point of view, though the calculations differ considerably. From the firm’s point of

view, the Wales contract is a lot more attractive than it is to the Cole Division ($600 versus $25).

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-4

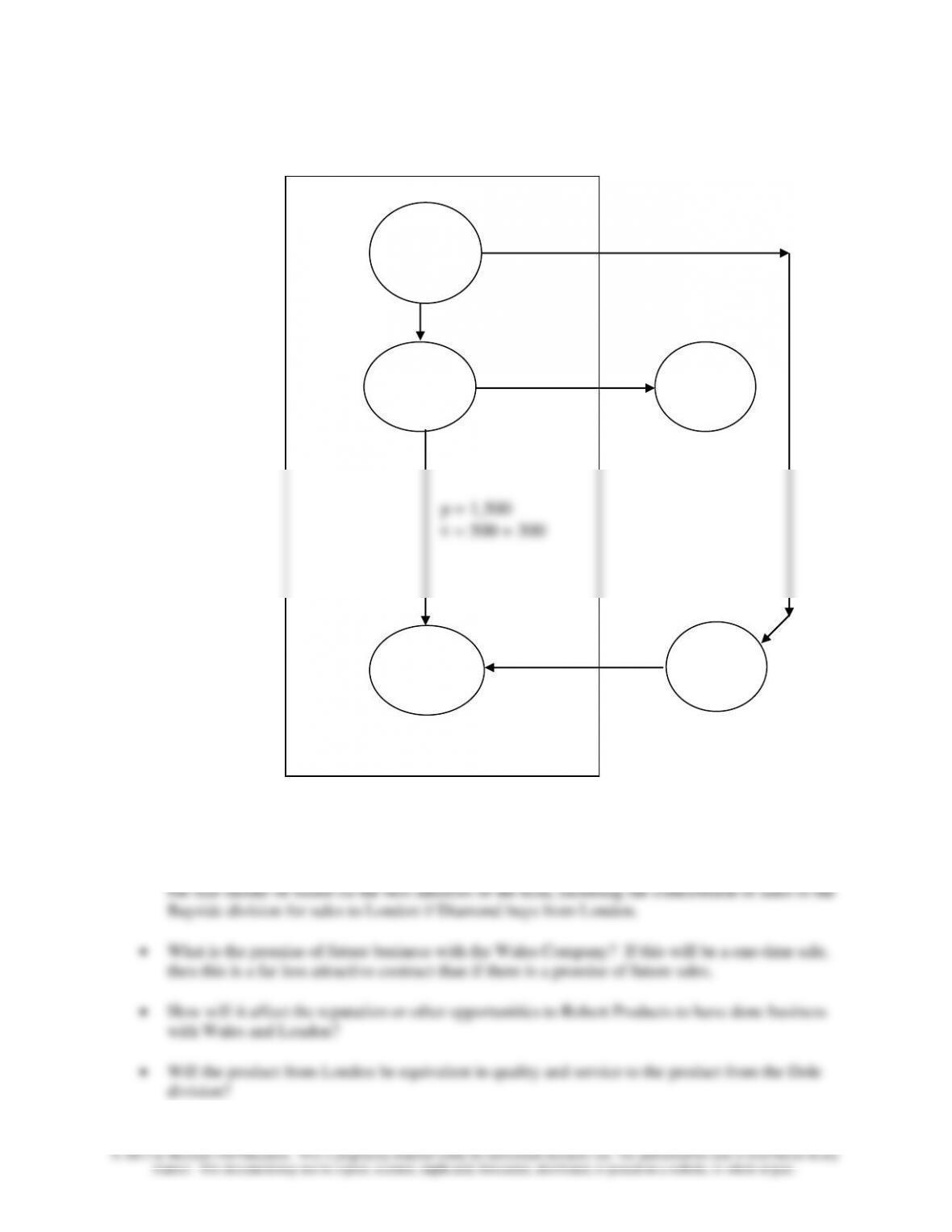

2. The strategic issues Robert Products should consider include:

• Is the structure of the transfer pricing system set properly so that division managers choose what

is in the best interests of the firm? In this case, Cole Division should choose the Wales contract,

London

p = 1,500

Cole

Diamond

Bayside

Wales

p = 400

v = 200

p = 1,250

v = 250 + 400

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-5

Case 19-3: Transfer Pricing (Foreign Sales Corporations)

1. A wide variety of responses are likely for this case exercise, depending on the depth of the student’s

research. There are a number of useful references on Foreign Sales Corporations (FSCs), one of which is

noted in the case assignment. Also, two recent articles in Business Week are useful: “This Tax Break

Could Trigger a War,” by Paul Magnusson, September 4, 2000, p.103 and “U.S. Exporters Get the Word:

Guilty,” by Paul Magnusson, August 16, 1999, p. 42.

Note: The status of FSCs was under active consideration within the U.S. Congress at the time

(April 2001) this case was written, it is possible that the matter might have been settled by the

time the case is assigned. If the matter has been settled, then the nature of the assignment should

shift to an understanding and critique of the nature of the settlement or legal change that was

enacted, including the expected effects on U.S. exporters and the firms with which they compete

globally.

2. We would expect students to address at least a number of the following issues (in no particular order):

a) The ethical issue: should U.S. exporters have what appears to be an unfair advantage in

international trade?

b) The legal issue: are FSCs in conflict with international law?

c) Have FSCs accomplished the goal set in 1971 when the law establishing FSCs was enacted?

Some say the law was enacted to narrow the U.S. trade gap at the time, but the trade gap has

continued to grow.

d) Who most benefits from FSCs and who is most adversely affected, and why? The group most

helped by FSCs are the U.S. exporters such as Boeing and Kodak while competitors in the

EU (European Union) are hurt because they do not have access to the favorable tax treatment.

e) What are the impacts of FSCs in monetary terms? Business Week reports tax savings to U.S.

corporations of approximately $2.3 billion in 1992.

f) What is the outlook for FSCs in the future?

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-6

Case 19-4: Interior Systems, Inc.

The purpose of this case is to introduce and critique the use of “residual income” measures for decision

making, performance evaluation and incentive compensation. As indicated in the case, Stern Stewart’s

version of residual income is referred to as Economic Value Added (EVA®). EVA® has received

favorable press coverage and adoptions from major corporations including Briggs & Stratton Corp.,

Coca-Cola Co., and Eli Lilly and Co (see Tully 1993, 1998; Fisher 1995). The case has been used

successfully at the undergraduate level, in M.B.A. programs and in executive programs. At the M.B.A.

level, the authors have used the case with both traditional full-time students as well as Executive M.B.A.

students. As indicated by our dedication on the title page, the case was inspired by our interaction with

Professor Bill Alberts. Although the case materials are fictitious, they benefited greatly from discussions

with Bill and a number of executives at companies that considered or adopted EVA®. For example, the

situation in Airline Interiors division (discussed below) is loosely based on the Boeing Company.

The Setting

Each division of Interior Systems (the Company) has a different market and different key drivers for

success; e.g, Airline Interiors’ (AI) key drivers are innovation, new orders (leading to a backlog) and,

probably, productivity improvements (though this latter item is not discussed in the case). Since sales lag

orders (potentially by years), accounting numbers are slow in reporting performance and are likely to be

poorly correlated with stock price movements (once the Company is publicly traded). In contrast, Office

Solutions (OS) is selling in the intensely price-competitive office furniture market. Current period sales

and expenses are key indicators of success. The division shows earnings and sales growth, but ROA is

declining. (ROA is not explicitly provided but can be easily calculated.) OS has excess capacity and

proposes to add a “profitable” new product to its line of office furniture, the E-chair.

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-7

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-8

Suggested Solution to Case Questions in the Engagement Letter (Exhibit 7)

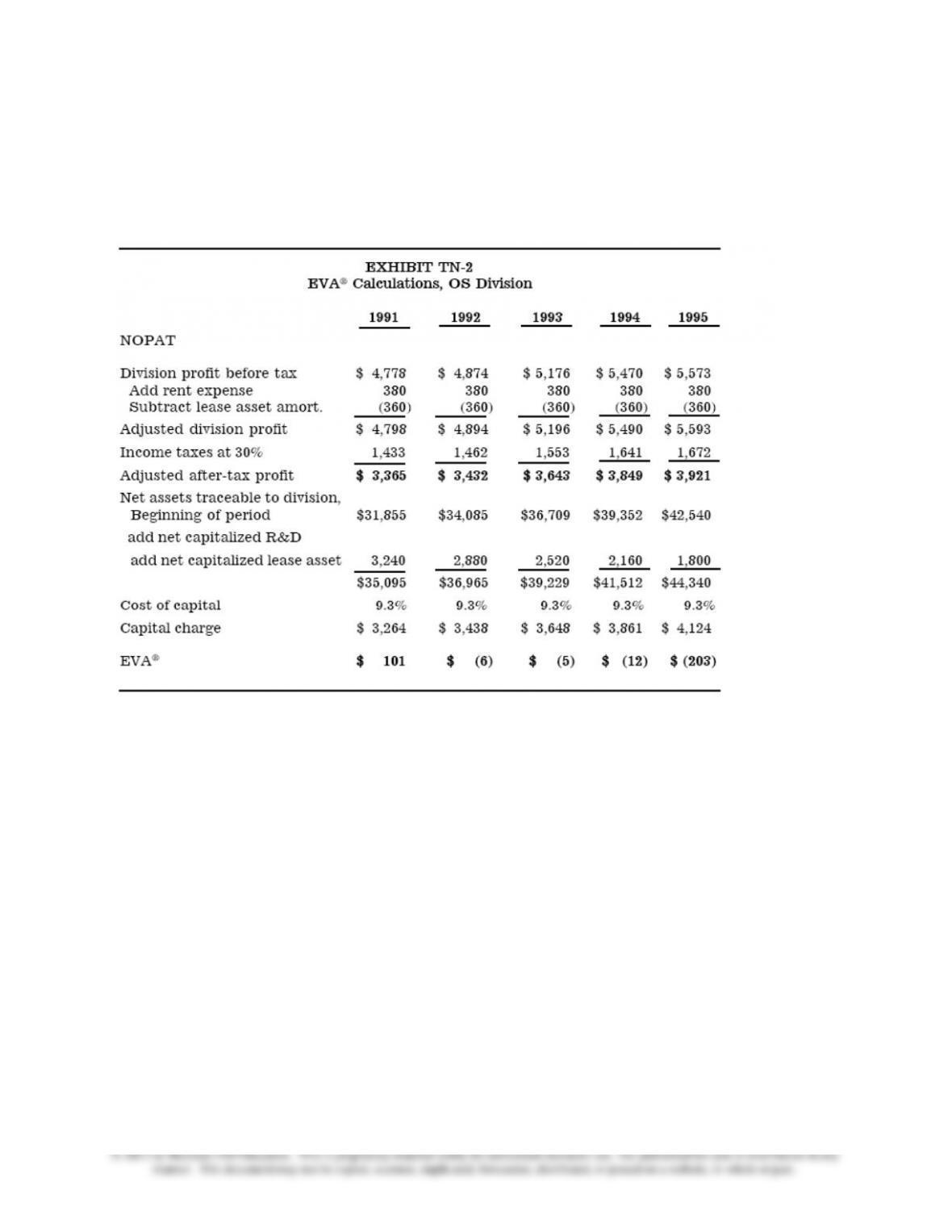

1. EVA® calculations are included in exhibit TN-1 (for Airline Interiors) and exhibit TN-2 (for Office

Solutions).Major points include:

AI division EVA® performance:

• Strong in 1991 and 1992; EVA® is positive, consistent with creating increased shareholder value.

• Very negative during downturn of 1993 and 1994 (consistent with destroying shareholder value)—but

recovery in 1995.

• Over the past five years, the three positive EVA® years have not overcome the two negative EVA®

years. Not surprisingly, EVA® appears to fluctuate with cycles in the industry. To get a picture of AI’s

long-term profitability, one would have to observe a complete business cycle.

OS division EVA® performance:

• Positive in 1991, somewhat negative in 1992–1994 and increasingly negative in 1995.

• Trend suggests that OS division is destroying shareholder value and therefore has not yet met the goal of

stabilizing the cycles experienced by the AI division.

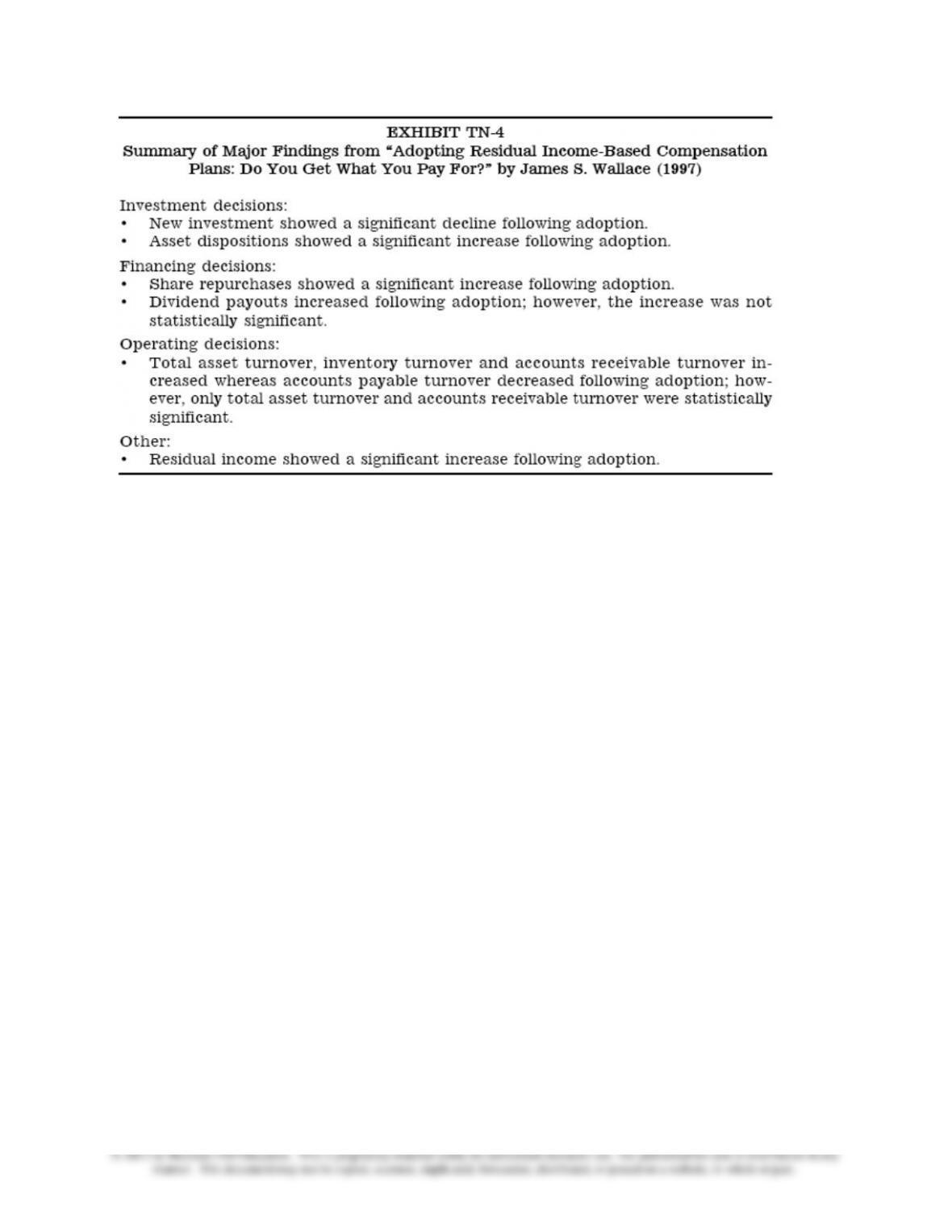

2. EVA® is likely to affect managerial decisions. (See exhibit TN-4 for elaboration and summary of

results from Wallace [1997], a study on firms’ adoption of EVA®-like incentive plans.)

2a. Other things equal, management should find that fewer projects are viewed as acceptable since each

project must now earn greater than the overall, after-tax, weighted cost of capital. (With profits as a

performance measure, any project that earns more than the imbedded cost of debt increases earnings.)

Profitable projects (such as the E-chair proposal) will be rejected if they are not predicted to cover the

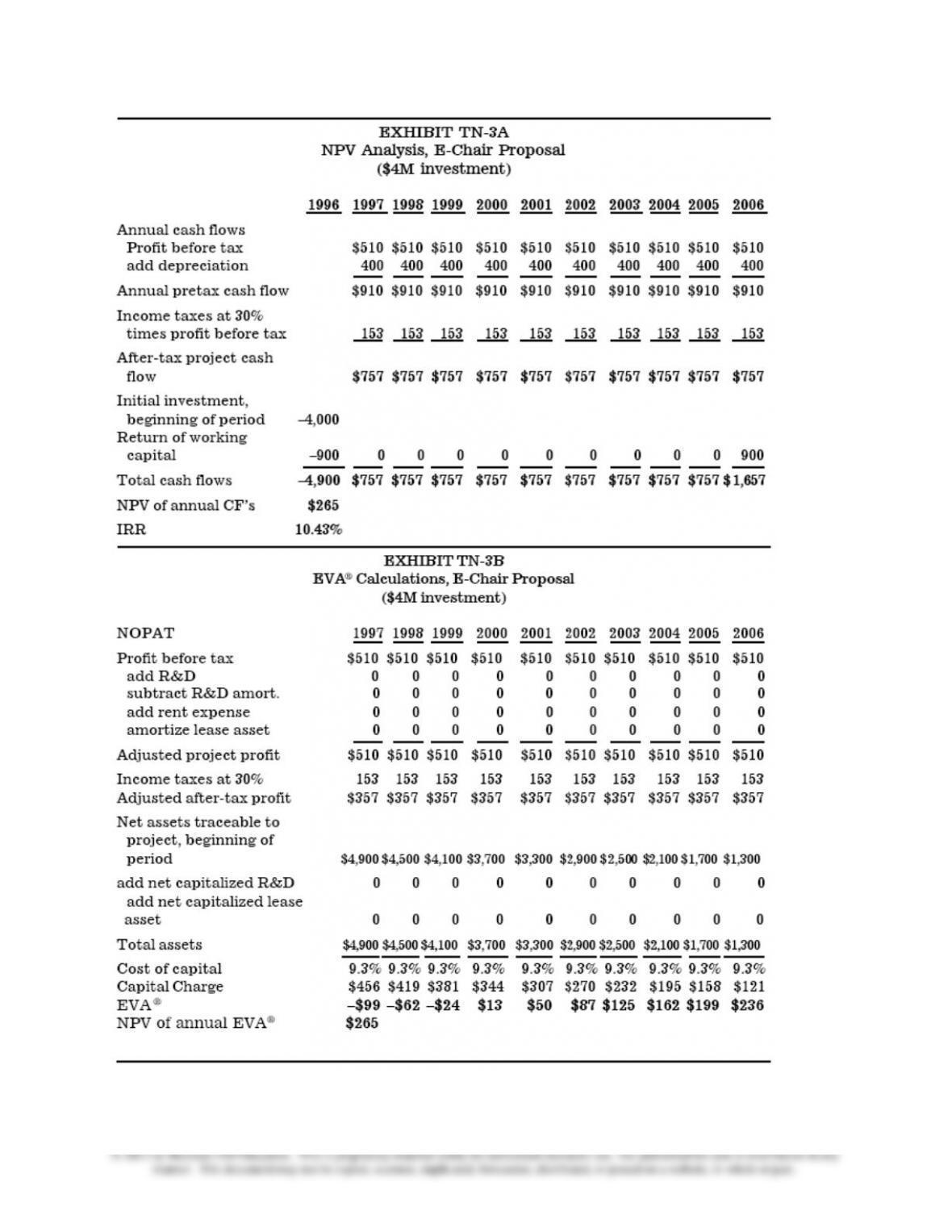

cost of capital. Exhibit TN-3A includes a traditional discounted expected cash flow analysis and exhibit

TN-3B presents a discounted expected EVA® analysis of the E-chair proposal using the assumption that

the necessary capital investment is $4 million. Note that, given the same set of assumptions (discussed

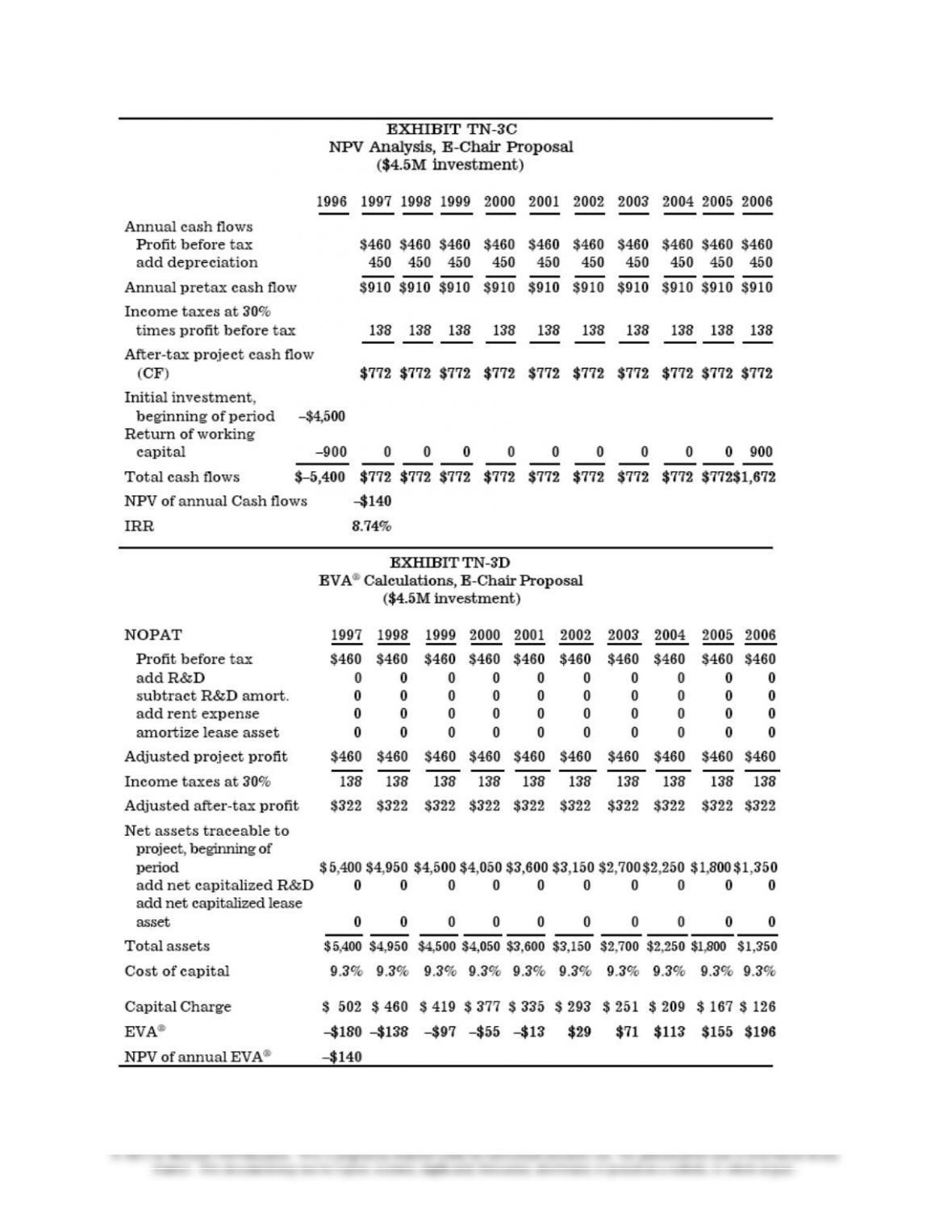

next), both approaches arrive at the same NPV. Exhibits TN-3C and 3D repeat the calculations using the

assumption that the necessary capital investment is $4.5 million.

Assumptions (not made explicit in the case) include:

• The single year of cash flows provided in exhibit 4 is representative of all years of the project’s

life. This suggests that there is no learning curve and no decay in performance throughout the

project’s life. Constant performance throughout the project’s life is consistent with no

competitive entry and thus is a particularly strong assumption.

• Tax treatment is based on income before EVA® adjustments.

• The appropriate hurdle rate for this project is OS division’s 1995 cost of capital (from exhibit

3).

• No inflation throughout the life of the project. (A close approximation would be to assume the

division’s cost of capital is a “real” [vs. nominal] rate of return and is appropriately matched

against “real” [vs. nominal] cash flows in exhibit 4. This is not precisely correct because, for

example, tax savings related to depreciation deductions are nominal cash flows.)

Given the above assumptions, the quantitative attractiveness of the E-chair proposal hinges on the size of

the initial investment in depreciable assets.

At $4 million (provided in exhibits TN-3A and 3B), the project has:

• a payback of 6.5 years

• positive incremental earnings in each year

• negative EVA® for 1997 through 1999

• a positive NPV of $265,000

At $4.5 million (provided in 10C and D), the project has:

Chapter 19 – Strategic Performance Measurement: Investment Centers

19-9

• a payback of 7 years

• positive incremental earnings in each year

• negative EVA® for 1997 through 2001

• a negative NPV of $140,000

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–10

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–11

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–12

Discussion of Non-NPV Criteria for Evaluating the Proposal

• Payback and earnings fail to alert the decision maker about the sensitivity of the decision to the level of

the investment in depreciable assets.

• Focusing on the level of EVA® in the early years can lead to the “wrong” decision. Even managers with

a three-year horizon might reject a positive NPV project (as it is when the investment in depreciable

assets is $4 million). Interestingly, focusing on incremental division profits in the early years can

inadvertently lead to the “correct” decision (when the investment in depreciable assets is $4 million).

Qualitative Factors

• What is likely to be the effect of the E-chair proposal on sales of other Company products? The case

suggests that the E-chair might cross-sell the AI version of the seat. While it strikes us that it is a stretch

to argue that airline seating could sell high-end office chairs, other OS products might benefit from

introducing the E-chair. (This is in contrast to many situations where new products cannibalize sales of

existing products.)

• Are some of the assumptions listed above likely to be violated? If so, how might it affect the decision?

2b. Other things equal, since fewer projects will be viewed as acceptable, more cash will be returned to

owners in the form of share repurchases (most likely\) or cash dividends (less likely). Ex ante, the

predicted effect on capital structure is less clear. Empirical evidence in Wallace (1997) suggests that firms

will reduce both debt and equity capital. (We have not included the data necessary to calculate financial

leverage.)

2c. Managers also have an increased incentive to efficiently run day–to-day operations because they have

to consider both earnings and the investment necessary to generate those earnings. This suggests that,

other things equal, we expect to see increases in total asset turnover, inventory turnover, AR turnover, etc.

(We have not included the data necessary to calculate these ratios.)

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–13

3. EVA® should mitigate but not eliminate incentives to emphasize short-run performance. Annual

EVA® is still based on a one–period historical model. However, accounting “distortions” such as the

requirement to expense R&D are “corrected” in calculating EVA®. In practice, EVA® compensation

plans are often implemented as rolling three-year targets in order to lengthen the managers’ planning

horizon.

For example, without lengthening the time horizon, a proposal might be rejected because it produces

negative EVA® in the early years despite having large positive EVA® in future years. This could be the

case with the E-chair proposal if the initial investment in depreciable assets is at the low end of the range,

e.g., $4 million. See discussion of case question 1 above. An alternative means of mitigating manager’s

rejecting positive NPV projects with early losses is to use a form of economic depreciation where lesser

amounts of depreciation is taken in the early years (i.e., decelerated depreciation).

4a. If EVA® is deemed to be cost effective (and management is sure it is not the “fad of the year”),

telling shareholders about it is probably a good (but bold?) idea. Given the capital charge, EVA® will

generally be (considerably) lower than the earnings numbers shareholders are accustomed to seeing. Note

that most firms appear to start slowly with EVA®. They tend to adopt it for performance measurement

some years before explicitly incorporating the measure into management incentive compensation plans.

(Of course it is possible that all the accolades for EVA® are due to self–selection, i.e., of those firms that

consider EVA®, the only ones that adopt it are successful firms that can “afford” to take a charge for

equity capital.) Many firms now include disclosure about their use of an EVA® performance measure;

however, they do not report actual EVA® performance.

4b. Asking a CPA firm to audit the numbers could potentially represent a high cost to the firm because of

the deviations from GAAP accounting resulting from adjusting for “accounting distortions” and providing

a deduction for the cost of equity capital. These additional costs include the direct costs of the additional

work that the CPA firm must perform in order to substantiate the accounting adjustments and the

calculation of the firm’s cost of capital. In addition to the direct costs, potential indirect costs include

possible litigation costs resulting from the deviations from GAAP accounting. Zimmerman (1997) in the

Journal of Applied Corporate Finance discusses these costs. Zimmerman (1997) gives the example of a

firm that capitalizes a large amount of R&D expense, leading to high and growing EVA® and high

EVA®-based bonuses. In his example, the stock price is also rising because the market looks beyond the

GAAP numbers to the EVA® results, believing the R&D will pay off. Unfortunately in this example a

new scientific discovery destroys the usefulness of the firm’s R&D expenditures, leading to a sharp drop

in the stock price. The R&D must be written off, leading to a sharp drop in EVA®. (No adjustment is

needed for GAAP earnings since R&D is already expensed.) In retrospect, the managers received large

EVA®-based bonuses that now appear unwarranted. A potential shareholder lawsuit could result because

the large EVA®-based bonuses may appear self-serving, given that GAAP earnings were much lower all

along. Some CPA firms might relish the opportunity to work with firms that adopt EVA®. Several of the

large accounting firms currently market versions of similar shareholder value measures.

Supplemental Questions

5. Note that this question does not directly deal with the merits of EVA®. Instead it addresses the more

general topic of accounting-based vs. stock-based compensation. No, it is probably a good idea to

continue to tie at least some of the managers’ incentive compensation to accounting (or EVA®)

performance even after the stock is publicly traded (Lambert 1993, 101). A reason to have an incentive

compensation plan is to align incentives (induce effort in the interests of the owner). Use of accounting–

based compensation allows more direct monitoring of that effort. Since managers are generally less

diversified than investors, without monitoring managers will tend to adopt more conservative projects

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–14

than investors would prefer. To the extent that accounting performance is correlated with management

effort (that is not captured in stock prices), incentives between managers and owners will be better

aligned by basing a portion of managers’ incentive compensation on accounting performance. Further,

because stock price is often affected by many events outside of the managers’ control, basing all incentive

compensation on stock price would subject managers to increased risk that could require higher than

optimal compensation.

6. Note that this question is closely related to question 2b above. The CFO’s arguments are theoretically

correct, i.e., pay out excess cash flow when positive NPV projects cannot be identified. However, the

Marketing VP’s position is common and understandable, given that managers generally are not

diversified (especially when one considers the amount of human capital tied up in the firm and frictions

in the managerial labor market). Thus, it is rational for managers to want to reduce their personal risk by

retaining excess cash in the business. The question is: “To what degree can changing to an EVA®-based

compensation scheme align the incentives of managers and owners?” Other reasons to retain cash (instead

of paying out “excess” cash via share repurchases or special dividends) include:

• Management can take actions (e.g., invest in new projects) without seeking funds and incurring

additional scrutiny from the impartial capital markets

• Empire building

> larger firms tend to pay higher salaries

> firms that are growing in scale (if not in EVA®) provide more opportunities for managerial

promotions (and most salary increases are associated with promotions)

> prestige and perks are associated with larger firms

Summary of Benefits and Costs of Switching to EVA®

Benefits include:

• Better aligns incentives with owners’ interests

• Like other investment-center performance metrics, forces managers to explicitly consider

balance sheet investment along with income statement performance.

• Reduces incentive to adopt profitable (but negative NPV) projects

• Increases the incentive to dispose of currently profitable (but negative NPV) projects.

• Increases incentive to pay out free cash flow (cash flow in excess of what can be used to fund

positive NPV projects)

• Better aligns performance evaluation with project selection based on NPV

Costs of switching to EVA® include:

• Installation and education of managers, e.g., it may be difficult to compute division-level cost of

capital or determine asset base attributable to each division.

• Difference from the metric that gets public attention—earnings.

• Accounting-based performance metrics that take into account the investment base (e.g., ROA)

may be “good enough.”

• Correlation between EVA® and stock price performance that may not be high for some firms

and may be no higher than for earnings or cash from operations. See Biddle et al. (1997).

Other issues:

• EVA® does not solve short–run incentive to show positive results early in a project’s life.

• EVA® does not help in situations where underlying operating profits are a poor measure of the

key success factors of the business (e.g., Boeing, biotech and AI!)

On balance, EVA® is probably a good idea for OS and, perhaps, for AI and the Company as a whole. (No

historical measure of performance, e.g., earnings, cash flow or EVA®, gets around the fundamental issue

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–15

that the key driver for success at AI is obtaining a new order.) We believe performance measurement and

incentive compensation should be based on more than accounting numbers alone (whether they be

earnings, cash flow, ROI or EVA®). One approach is to identify key drivers of shareholder value for each

level of the organization and be incorporated in a balanced scorecard. For example, at AI new orders are

obviously a key driver. Other key measures might include: quality (e.g., defects, durability, customer

complaints), cycle time, operating up-times, inventory levels, on-time delivery, parts simplification, new

product development, etc.