Chapter 4 – Job Costing

4-16

4-37 Application of Overhead (15 min)

1.

Budgeted total overhead $360,125

Budgeted direct labor hours

33,500

Overhead rate $10.75 =$360,125/33,500

Job

Direct

Materials

Gallons of

Paint

Direct

Labor

Hours

Direct

Labor Cost

Applied

Overhead at

$10.75 per

hour

Total Job Cost =

Direct Materials

+Direct Labor

+Overhead

Prevette $3,800 24 42 $855 $451.50 $5,106.50

Harmon 4,600 38 66 1,366 $709.50 $6,675.50

2. The oil-based paint, because it required more clean-up time and

materials (harmful chemicals), increased direct labor hours and

increased materials costs (due to the purchase of the clean–up

chemicals), both of which are included in job cost. The disposal of the

based paints should be separately calculated, so the company can track

the “full” cost of using oil–based paints. The company’s practice of

disposing of the waste clean-up materials in an environmentally

appropriate manner is commendable.

Chapter 4 – Job Costing

4-17

4-38 Spoilage and Scrap (20 Min)

Background Information:

Job X12 (specific normal spoilage for a particular job)

Cost of spoiled units $600

Disposal value of spoiled unit 300

Sale value of scrap 80

Sale of scrap common to all jobs 120

1. Journal entries to record spoilage costs:

a. To record the normal spoilage attributable to Job X12

Materials Inventory (disposal price of the spoiled goods) 300

Loss from Abnormal Spoilage 200

Work-in-Process Inventory: Job Y34 600

2. Journal entries to record scrap sold:

a. To record the scrap sold attributable to a specific job

Cash 80

Chapter 4 – Job Costing

4-18

PROBLEMS

4-39 Overhead Rates Used for Each Machine in a Printing Plant

(Note: See also the Comments on Cost Management in Action at the end

of the chapter regarding a similar costing situation)

This short case is intended as a basis for class discussion that could initiate

the following topics and questions: application of job costing in the printing

industry; what are the factors driving the accuracy of product costing; how

does the choice of job costing method affect pricing; what is the effect of

cost allocation methods on management behavior, performance evaluation,

and how does a chosen cost method advance or hinder the firm’s progress

to its strategic goals? Some observations that I would bring out in this

discussion include:

EFS uses a job costing system in which materials and direct labor are

traced to the job, and overhead is traced to each machine and then applied

to the jobs based on machine usage

A strength would be that EFS has put a lot of effort into tracing the printing

costs accurately and using an overhead allocation approach that attempts

to trace the costs of the machinery to the jobs that used that machinery

I would begin a discussion of the EFS approach to allocating other

overhead costs – insurance, supervision, and office salaries – to the jobs

based on the capacity of the machines. That is, machines with more

printing capacity (where capacity is the number of feet of forms produced

per minute of machine time) will receive a larger portion of this portion of

overhead. This is very much like a volume based rate, which is OK, but

does not reflect the actual behavior of these costs. Suppose the total of

other overhead is significant. Then small jobs on high capacity (fast)

machines will be charged a relatively high rate. Conversely, large jobs on

low-capacity machines will be charged a relatively low rate. How this

would affect pricing and the allocation of jobs to machines is not easy to

predict.

Chapter 4 – Job Costing

4-19

4-39 (continued –1)

The strategic issue is the unknown impact of cost calculations on

competitive pricing, and therefore on the company’s competitiveness. The

business) in some periods of the year.

Source: Lisa Cross, “Benefiting from Costing and Pricing Tools,” Graphic

Arts Monthly, July 2004, pp 32-34.

4-40 Plantwide vs. Departmental Overhead Rate (30 Min)

1. Empco Inc. is currently using a plantwide overhead rate that is

applied on the basis of direct labor dollars. In general, a

plantwide factory overhead rate is acceptable only if a similar

relationship between overhead and direct labor exists in all

departments, or the company manufactures products, which

receive proportional services from each department.

In most cases, departmental overhead rates are

preferable to plantwide overhead rates because plantwide

overhead rates do not provide:

• a framework for reviewing overhead costs on a

Chapter 4 – Job Costing

4-20

2. Because Empco uses a plantwide overhead rate applied on the

basis of direct labor dollars, the elimination of direct labor in the

Drilling Department through the introduction of robots may

expenses because of increased depreciation expense. Under

Empco’s current method of allocating overhead costs, the

remaining departments will merely absorb these costs.

4-40 (continued –1)

3. In order to improve the allocation of overhead costs ,Empco should:

• establish separate overhead accounts (pools) and rates

for the Drilling Department.

4-21

4-41 Plantwide vs. Departmental Overhead Rate (30 min)

1. Budgeted Overhead = ($146,000 + $94,000) + ($77,000 + $163,000)

= $480,000

= $24 per direct labor-hour

2. Budgeted Machine-hours = 1,000 units x (5 + 15) hours = 20,000 hours

Predetermined Overhead Rate = $480,000 / 20,000

3. Using Direct Labor-hours:

Department A Department B Total

DL-hours 1,000 x 12 1,000 x 8

Using Machine-hours:

Department A Department B Total

Machine-hours 1,000 x 5 1,000 x 15

= 5,000 hours = 15,000 hours 20,000 hours

Overhead applied

5,000 x $24 15,000 x $24

= $120,000 = $360,000 $480,000

4. If direct labor-hours are used to apply factory overhead, Department A

is overcharged and Department B is undercharged. If machine hours are

used, Department A is undercharged and Department B is overcharged.

Chapter 4 – Job Costing

4-22

4-41 (continued –1)

5. Using direct labor-hours for Department A:

Predetermined Overhead Rate = $240,000 / 12,000

= $20 per direct labor-hour

Applied Overhead = 1,000 units x 12 hours x $20 = $240,000

4-23

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

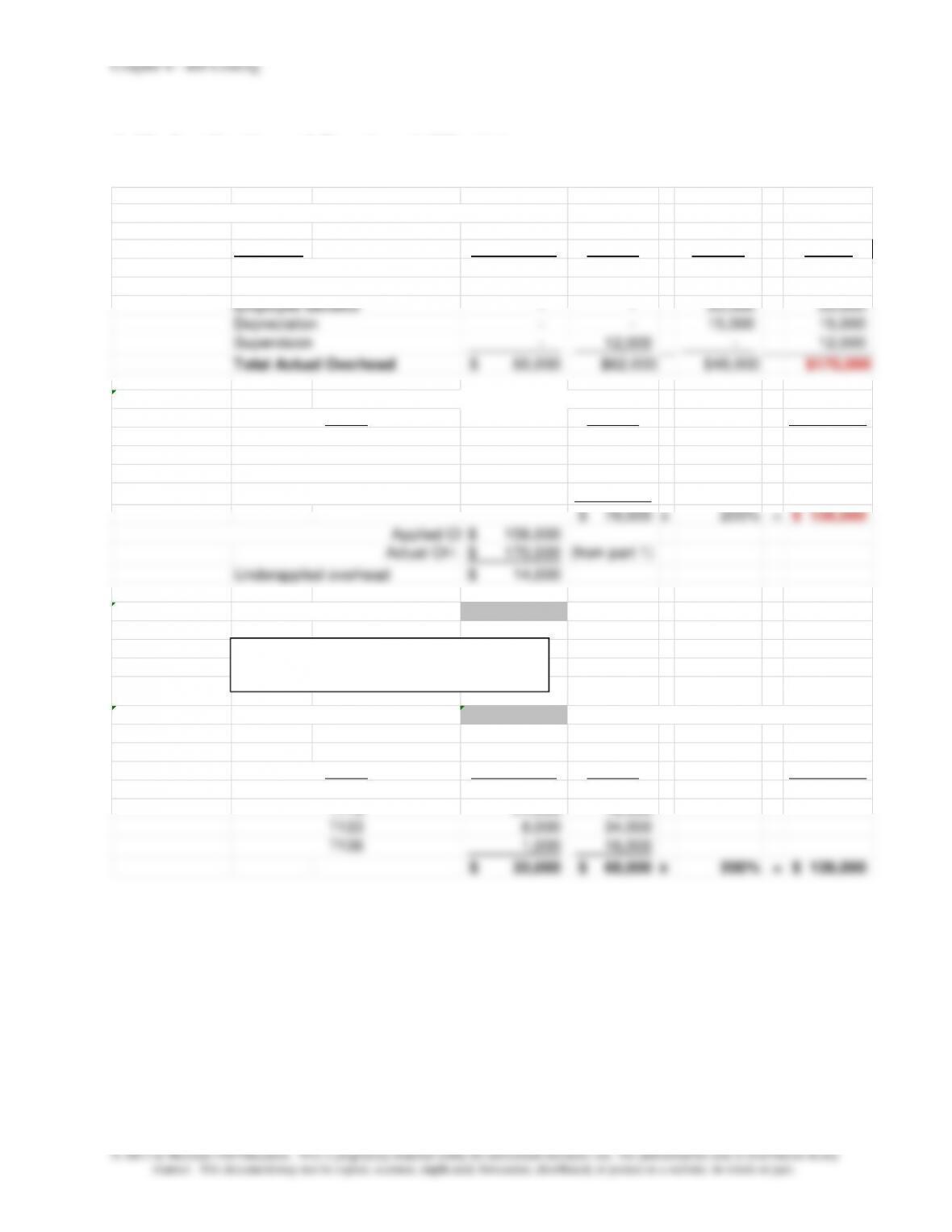

4-42 Application of Overhead (25 min)

1. Total actual overhead: $170,000; see calculations below

Overhead MATERIALS LABOR OTHER TOTAL

60,000$ –$ –$ 60,000$

– 50,000 – 50,000

– – 33,000 33,000

– – 15,000 15,000

– 12,000 – 12,000

Total Actual Overhead 60,000$ $62,000 $48,000 $170,000

2.

LABOR Applied OH

10,000$

18,000

34,000

16,000

78,000$

x

200% =156,000$

Applied OH

156,000$

Actual OH =

170,000$ (from part 1)

Underapplied overhead 14,000$

3. Cost of Goods Sold for Job T114: $108,500

MATERIALS LABOR Applied OH

–$ –$

24,000 18,000

8,000 34,000

1,000 16,000

T119

Indirect Materials and Supplies

Indirect Labor

Employee Benefits

Depreciation

Supervision

JOB #

T114

T136

T133

T136

JOB #

T114

T119

T133

Cost of Goods Sold for Job No. T114:

Chapter 4 – Job Costing

4-24

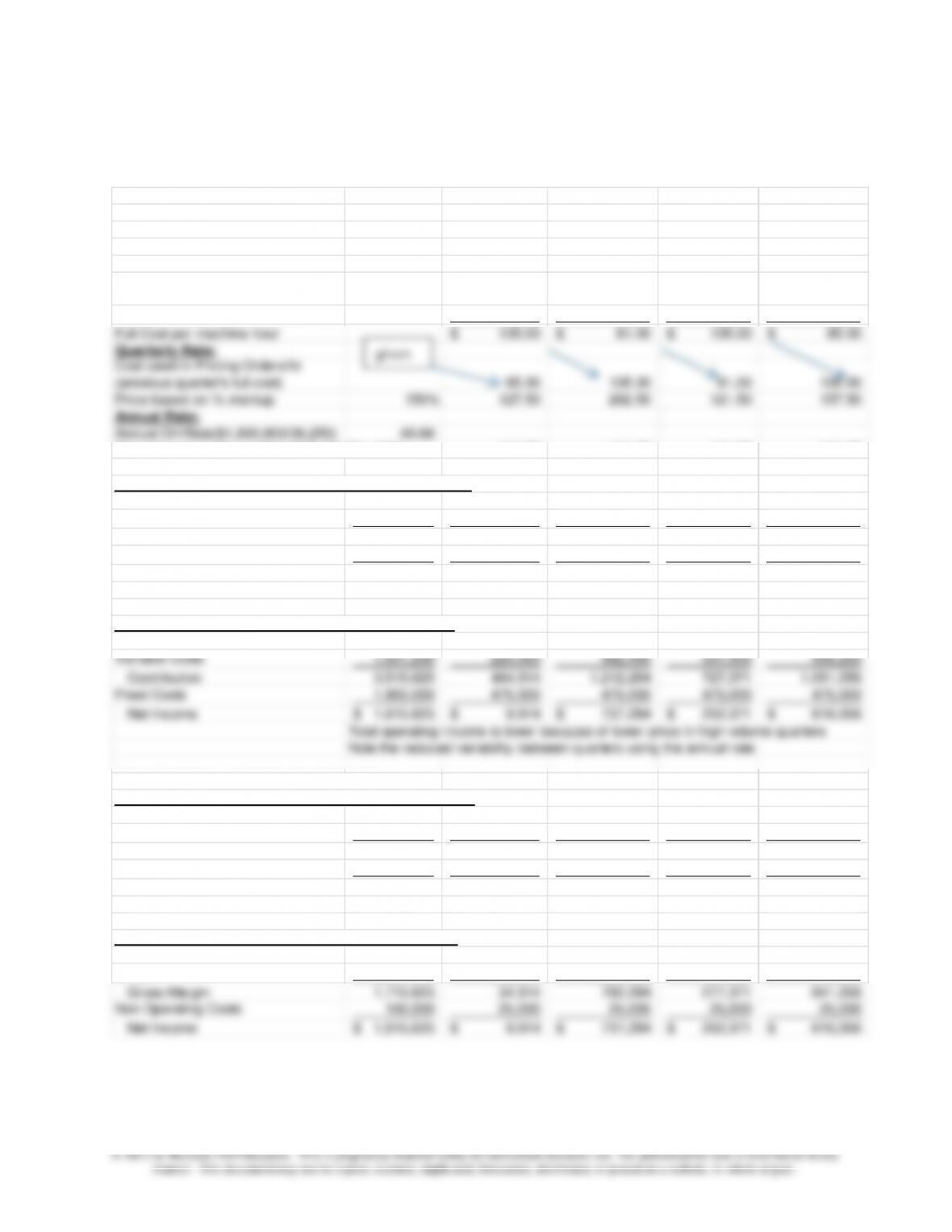

4-43 Quarterly and Annual Overhead Application

1,2,3

Mansfields Machine Shop

Annual First Quarter Second Quarter Third Quarter Fourth Quarter

Number of machine hours/quarter 36,250 5,000 12,500 7,500 11,250

Fixed Administrative Costs/qtr 100,000$ 25,000$ 25,000$ 25,000$ 25,000$

Overhead per quarter 1,800,000 450,000 450,000 450,000 450,000

Overhead per machine hour, for

each quarter

90.00 36.00 60.00 40.00

Variable cost per machine hour 45.00 45.00 45.00 45.00

Full Cost per machine hour 135.00$ 81.00$ 105.00$ 85.00$

Quarterly Rate:

Cost used in Pricing Orders/hr

(previous quarter’s full cost)

85.00 135.00 81.00 105.00

Price based on % markup 150% 127.50 202.50 121.50 157.50

Annual Rate:

Annual OH Rate($1,800,000/36,250) 49.66

Price Based on Annual Rate($45+49.66)x 150% 141.98 141.98 141.98 141.98

Using Quarterly Rate: Contribution Income Statement

Revenue 5,851,875$ 637,500$ 2,531,250$ 911,250$ 1,771,875$

Variable Costs 1,631,250 225,000 562,500 337,500 506,250

Revenue 5,146,875$ 709,914$ 1,774,784$ 1,064,871$ 1,597,306$

Variable Costs 1,631,250 225,000 562,500 337,500 506,250

Contribution 3,515,625 484,914 1,212,284 727,371 1,091,056

Fixed Costs 1,900,000 475,000 475,000 475,000 475,000

Net Income 1,615,625$ 9,914$ 737,284$ 252,371$ 616,056$

Total operating income is lower because of lower price in high–volume quarters

Note the reduced variability between quarters using the annual rate

CONVENTIONAL INCOME STATEMENTS

Using Quarterly Rate: Conventional Income Statement

Revenue 5,851,875$ 637,500$ 2,531,250$ 911,250$ 1,771,875$

COGS 3,431,250 675,000 1,012,500 787,500 956,250

Revenue 5,146,875$ 709,914$ 1,774,784$ 1,064,871$ 1,597,306$

COGS 3,431,250 675,000 1,012,500 787,500 956,250

Gross Margin 1,715,625 34,914 762,284 277,371 641,056

Non Operating Costs 100,000 25,000 25,000 25,000 25,000

Net Income 1,615,625$ 9,914$ 737,284$ 252,371$ 616,056$

given

Chapter 4 – Job Costing

4-25

Problem 4-43 (continued –1)

4. The analyses in parts 1-3 show:

a) An annual pricing rate under the annual approach would be $141.98,

based on the actual results of the prior quarter.

b) The result of the quarterly policy as implemented is to have overhead

rates and pricing rates relatively high in the high volume quarters, the

quarters in which per-hour overhead rates are the lowest. This arises

because the high and low quarters alternate, and the rates are

calculated for one quarter to apply to the next. It appears that

George and Steve may be unaware of the fact that volume

the conventional full cost income statement. The higher variability of

revenues and profits could cause strategic problems, such as

creating problems in cash flow management, as cash flows fluctuate

significantly from season to season.

Total annual profit is greater under the quarterly rate approach

($2,320,625 relative to $1,615,625 for the annual rates) because the

quarterly approach has higher rates in the high volume quarters.

Total costs are the same in both approaches but revenues are higher

for the quarterly approach. The fact that Mansfield is charging

somewhat higher rates during the high volume months is probably

Chapter 4 – Job Costing

4-26

4-43 (continued -2)

variability in profits among quarters. Of course, it also appears that

going to the annual rate could also reduce profits. The demand

figures used in the analysis are the actual figures for the prior year,

so using an annual rate would have produced lower profits in the prior

year if demand were the same.

d) If the use of annual rates would significantly increase demand, then

George and Steve should consider the change, as it would increase

profits and reduce variability in pricing and profits across quarters.

However, there is a significant difference in annual profit figures for

approximately 27 machines x 150 hours x 3 months = 12,150

machine hours. Right now the busiest quarter has 12,500

machine hours of demand, indicating that these machines are

already used beyond planned capacity levels in this quarter, and

thus, any increase in capacity means a need for more machines,

an investment that should be carefully considered.

e) Given the seasonality of the business, George and Steve may want

to consider monthly profit reports, irrespective of the overhead rate

and pricing method chosen.

f) A good additional question for class discussion would be the

following: What would be the effect of the choice of a quarterly or

annual rate on the quarterly income statements if Mansfield were to

close the overhead account quarterly and close the underapplied or

overapplied overhead to cost of goods sold? The solution shown for

Chapter 4 – Job Costing

4-27

4-44 Overhead Application (30 min)

Note: the information in part (a) is not needed for the solution.

1. Total manufacturing cost: Job X = $83,600; Job Y = $75,800

2. Underapplied overhead: $3,100; increase Cost of Goods Sold

See calculations below:

Problem Information

Direct

Materials

Direct

Labor Machine Hours

Job X 22,000$ 1,100

Material A 8,000$

Material B 3,000

Job Y 15,000$ 800

Material A 16,000$

Material B 8,000

Factory Overhead Application Rate $46 per machine hr

Solution

1. Total Manufacturing Costs for each job

11,000$ 24,000$

Total Direct Labor Cost

22,000 15,000

Applied Overhead

Machine Hours 1,100 800

x Application rate $46 $46

=Total Applied Overhead Cost 50,600 36,800

Total Manufacturing Costs 83,600$ 75,800$

2. Calculate Factory Overhead Under or Overapplied

Actual Factory OH:

Utilities 3,000

Depreciation 18,000

Insurance 2,500

Total Actual Factory OH $90,500

Applied Overhead 87,400 =(1100+800) x $46

$3,100 UNDERAPPLIED

Adjust Difference to COGS 3,100 Incease Cost of Goods Sold by this Amount

Chapter 4 – Job Costing

4-28

4-45 Application of Overhead (20 min)

1. Total manufacturing cost: Job S = $358,437.50; Job T=

Chapter 4 – Job Costing

4-29

Problem Information

Direct Materials Direct Labor Labor Hours

Job S 55,500$ 6,175

Material A 28,500$

Material B 12,000

Job T 45,000$ 4,275

Material A 71,250$

Material B 35,000

Factory Overhead Application Rate $42.50 per labor hour

Solution

1. Total Manufacturing Costs for each job

Total Direct Materials Cost Job S Job T Total

40,500.00$ 106,250.00$

Total Direct Labor Cost

55,500.00$ 45,000.00$

Applied Overhead

Labor Hours 6,175 4,275 10,450

x Application rate $42.50 $42.50

Total Manufacturing Costs $358,437.50 $332,937.50 $691,375

2. Calculate Factory Overhead Under or Overapplied

Actual Factory OH:

Indirect Materials 211,000$

Indirect Labor 133,000

Utilities 14,250

Depreciation 45,000

Insurance 18,000

Total Actual Factory OH 421,250$

Adjust Difference to COGS (22,875)$ Decrease Cost of Goods Sold by this Amount

Chapter 4 – Job Costing

4-30

4-46 Cost Flows, Application of Overhead (50-60 min)

1. Predetermined Overhead Rate

= $1,235,475 / 86,700 = $14.25 per direct labor-hour

2. a. Materials Inventory 125,000

Accounts Payable 125,000

Materials Inventory (indirect materials) 1,098

$25 x 3,500 = $87,500

$36 x 30.5 = $1,098

d. Work-in-Process Inventory 141,900

Factory Overhead 46,000

Cash 187,900