Chapter 11 – Decision Making with a Strategic Emphasis

11–26

• Channels – Pop’s, Inc. needs to research specific target markets and develop products to meet those

specific consumer’s needs. Pop’s, Inc. could do this by providing private labeled soda to specialty stores.

There are marketing research techniques designed to help develop product concepts that represent

“optimal” configurations of features, package design, size, flavors, or benefits (e.g., conjoint analysis) as

well as arriving at a consumer-based price rather than a cost based price (e.g., discrete choice modeling,

conjoint analysis). These would likely lead to very different assumptions and estimates of sales and costs.

These research techniques can be briefly mentioned as a way to get students to begin thinking and asking

questions about how adopting various types of differentiation strategies would affect sales estimates as

well as estimates of costs in the areas of (a) raw materials, (b) packing materials, (c) manufacturing, and

(d) distribution.

Pitfalls to a Differentiation Strategy

While a Differentiation Strategy would seem to be the best solution for this specific case, there are no

guarantees that this strategy will produce a meaningful competitive advantage. Michael Porter points out

that to build competitive advantage through differentiation a firm must seek sources of uniqueness that

are time consuming or burdensome for rivals to match. Other common pitfalls and mistakes pointed out

by Porter include (Porter 1985, pp. 160-161):

• “UNIQUENESS THAT IS NOT VALUABLE” – Uniqueness only leads to differentiation when the

buyer perceives that it either lowers the buyer’s cost or raises buyer performance.

• “TOO MUCH DIFFERENTIATION” – Over differentiating so that price is too high relative to

competitors or that product quality or service levels exceed buyer’s needs

• “TOO BIG A PRICE PREMIUM” – Trying to charge too high a price premium (the

larger the price differential the harder it is to keep buyers from switching to lower priced competitors.)

• “IGNORING THE NEED TO SIGNAL VALUE” – Failing to communicate discernable product

differences and relying only on intrinsic product attributes to achieve differentiation.

• NOT KNOWING THE COST OF DIFFERENTIATION – Not understanding or identifying what

buyers consider as value.

A low-cost provider will defeat a differentiation strategy when buyers are satisfied with a basic product

and are not willing to pay a higher price for “extra” attributes.

ADDITIONAL IN-CLASS DISCUSSION ITEMS

Target or Price-Led Costing verses Cost-Plus Mark-Up Approach

Based on the data provided in this case, Pop’s, Inc.’s approach to pricing has been primarily a cost-plus

mark-up approach. Under this approach a company develops a product, determines the cost, and adds a

mark-up to the product in order to determine the product’s selling price. While this method is obviously

simple and straightforward, the method fails to take into consideration what consumers will pay until the

end of the process. Peter Drucker points out that cost-based pricing can be an expensive approach:

“Most American and practically all European companies arrive at their prices by adding up costs

and putting a profit margin on top. And then, as soon as they have introduced the product, they

have to cut the price, redesign it at enormous expense, take losses and often drop a perfectly good

Chapter 11 – Decision Making with a Strategic Emphasis

11–27

product because it is priced incorrectly. Their argument? ”We have to recover our costs and make

a profit.”

This is true, but irrelevant. Customers do not see it as their job to ensure a profit for

manufacturers. The only sound way to price is to start out with what the market is willing to pay –

and thus, it must be assumed, what the competition will charge – and design to that price

specification.

Starting out with price and then whittling down costs is more work initially. But in the end it is

much less work than to start out wrong and then spend loss-making years bringing costs into

line.” (Drucker 1993)

Target or price-led costing is a much more efficient approach since knowledge of both the market and

customers are incorporated into the design of the product. While market research is costly, cost-based

pricing often requires much more costly fixing of pricing and product problems that never should have

occurred.

Discuss the decision to utilize contract-manufacturing versus in-house manufacturing. Ask students

to discuss the advantages and disadvantages of each decision.

Companies launching products for the first time often utilize contract manufacturing to limit the up-front

investment in capital. Advantages are obviously a lower throwaway on an unsuccessful launch and the

avoid these disadvantages most start-ups can negotiate a short-term contract to utilize contract

manufacturing during the launch a product and subsequently invest in an in-house production facility

once the product has proven itself.

Discuss the decision to enter a test-market. Ask students to discuss the advantages and

disadvantages and whether other alternative research methods exist.

A test market allows a company to launch its product in a real life setting and evaluate its success with a

much lower investment than taking a new brand directly to a national market. While the test market

provides a great tool for both fine-tuning a launch and gauging volume forecasts, there are some

alternative method is to allow customers to try the product and then answer questionnaires regarding the

product attributes and pricing.

Chapter 11 – Decision Making with a Strategic Emphasis

11–28

Discuss the promotional budget. Ask students to discuss how the proposed budget was

determined and the advantages and disadvantages of this type of “top–down” budgeting

(i.e., top management arbitrarily sets the budget).

One way to make this case discussion richer from a strategic vantage point would be to consider how an

“objective and task” method of budgeting could be employed. This approach begins by setting feasible

and measurable promotional objects. Examples are: (a) to increase the awareness level from 0% to 50%

for the new Pop’s soda among target consumers within the next six months, (b) to increase the level of

determine the overall budget necessary for promotional success.

Concluding the Case Discussion

At the conclusion of the case discussion, students should be told that the purpose of this case is to help

them recognize how they, as accountants, can add significant value to a firm’s strategic planning process.

There is ample evidence from the workplace and academia that aspiring accountants need training on how

to think beyond the numbers. They need to learn to think strategically. They add value first by asking the

Chapter 11 – Decision Making with a Strategic Emphasis

11–29

Chapter 11 – Decision Making with a Strategic Emphasis

11–30

Teaching Notes for Readings

Reading 11-1: “Relevance Added: Combining ABC with German Cost

Accounting”

This article describes ABC costing and German cost accounting (GPK) and provides a comparison of the

two methods. GPK is presented as a superior method for relevant cost analysis.

Discussion Questions:

1. What is GPK?

GPK is the acronym for German cost accounting, which is an enterprise system-based cost accounting

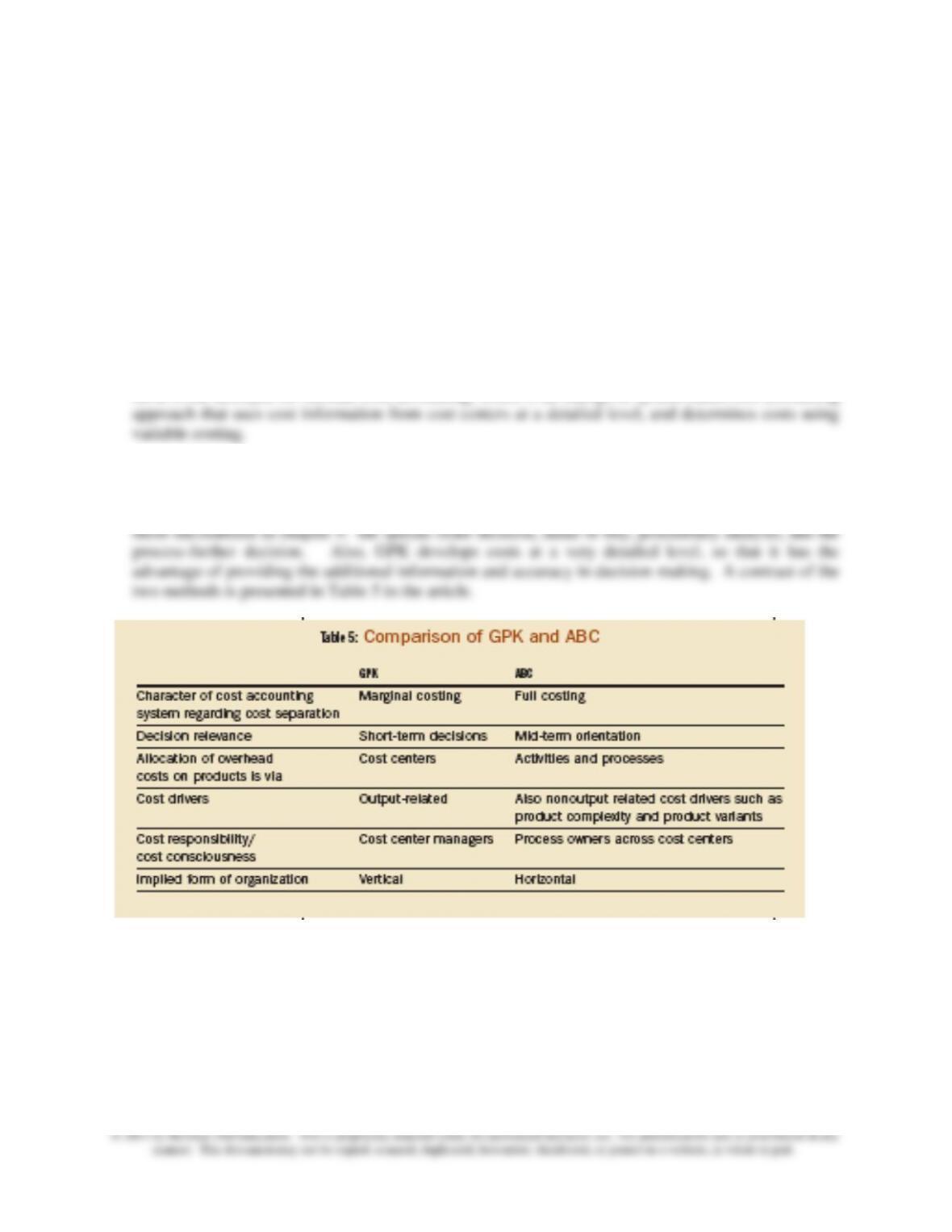

2. How does GPK compare to ABC costing?

Since it is based on variable costing, GPK it is considered useful for relevant cost decisions such as

Chapter 11 – Decision Making with a Strategic Emphasis

11–31

3. What are the key elements of GPK?

4. What are the two types of cost centers used in GPK? Explain the difference.

There are two types of cost centers, the primary cost centers and the final cost centers. Primary costs

Chapter 11 – Decision Making with a Strategic Emphasis

11–32

Reading 11-2: Analyzing Sustainability Impacts

To bypass traditional “triple-bottom-line” thinking, the authors offer a practical tool that can determine

the real costs and benefits of going green. This cost-benefit tool allows financial managers to consider

both the financial and social outcomes of potential decisions without the need for advanced knowledge of

sustainability models or methods. The process requires five basic steps. This article provides a practical

tool that can be used to determine the real costs and benefits of” going green.”

Discussion Questions

1. What is the principal link between this article and the material discussed in Chapter 11 of the

text? What motivation is offered by the authors to expand the basic decision model presented in

Chapter 11?

This paper argues for an expansion of the traditional decision-making model, that compares in some

sense costs and benefits associated with proposed investments and projects, to more fully include

environmental and social impacts of business.

2. In the opinion of the authors of this article, what are “sustainability outcomes” a function of?

The article defines “sustainability” outcomes as the sum of sustainability performance (i.e.,

Figure 1).

3. Provide an overview of the five-stage decision process recommended by the authors as a way to

incorporate sustainability outcomes into traditional decision-making models.

The authors suggest the following five-step decision process as a structured way to incorporate

sustainability outcomes in decision analysis:

1. Traditional (Cost-Benefit) Analysis

2. Identifying Sustainability Outcomes (see Table 1 for guidance in this regard)

Chapter 11 – Decision Making with a Strategic Emphasis

11–33

4. Provide an overview of the CityClean, Inc. example offered by the authors.

The hypothetical example provided by the authors involves a business, CityClean, Inc., that provides

various cleaning services to area businesses/local government and that is considering a move to more

environmentally friendly cleaning supplies. An expanded cost-benefit analysis of this decision (to

The basic or traditional cost-benefit analysis is expanded in Figure 3 in two major respects: (1) Figure

3 includes a “Sustainability Performance” box in addition to an “Operating Performance” box; and (2)

Figure 3 includes a “Stakeholder Reaction” box. In the latter case, the management accountant

working with management places an estimated monetary value on each of the “stakeholder reactions”

Chapter 11 – Decision Making with a Strategic Emphasis

11–34

Reading 11-3: A New Hue of Green for the Management Accountant

With energy prices at historically high levels, there’s ample incentive for companies to consider investing

in energy-saving technology that’s both cost efficient and environmentally friendly. Management

accountants can help the cause by preparing cost-benefit analyses of alternative investment possibilities

that contribute to the further “greening” of the United States. This creates a win-win situation for all.

Discussion Questions

1. Provide an overview of the context for the decision problem explored in this article.

This article focuses on the decision of Jiminy Peak Mountain Resort, located in the Bershire

Mountains of western Massachusetts. Jiminy Peak about draws about 250,000 visitors annually, while

summer pulls in roughly another 100,000 for mountain biking and other activities. As might be

invested in a wind-turbine project, an analysis of which is the primary subject of the article.

2. What were the major financial costs and benefits associated with the investment in the wind

turbine by Jiminy Peak Mountain Resort?

▪ Excess energy generated by the wind turbine—obviously, this cannot be “stored,” but it could be

automatically diverted to the power grid and sold to the regional electric utility company (~

$160,000/year)

depreciation; the value of this was increased present value of the tax savings attributable to the

depreciation deductions)

▪ Incremental out-of-pocket costs (maintenance and insurance): $75,000/year (estimated)

3. What were some of the major non-financial (i.e., qualitative or strategic) factors associated with

the investment by Jiminy Peak Mountain Resort?

▪ Reduction of emissions from power generation activity (e.g., burning of fossil fuels): CO2, SOX, and

NOX.

▪ Increased customer goodwill/enhanced customer reputation/positive effect on “brand”

Chapter 11 – Decision Making with a Strategic Emphasis

11–35

4. According to the authors, what are the primary roles that the management accountant can play

in terms of investment decisions similar to the one described in this article?

As indicated in Chapter 11, the management accountant’s primary role is to help generate the set of

relevant information related to proposed spending and investments on the part of management. These

benefits include financial (costs and revenue) effects, other (nonfinancial) quantitative effects, and

In addition, the management accountant can help design an effective feedback/control system

regarding such investments. This system might consist of two primary components:

1. Post-Investment Audit (see Chapter 12): the general idea here is to provide a check on the

2. Periodic Budgetary Reports (see Table 2 in the article). Note that the reporting framework

reflected in Table 2 includes a combination of financial, nonfinancial, environmental, and