Chapter 10 – Strategy and the Master Budget

10–89

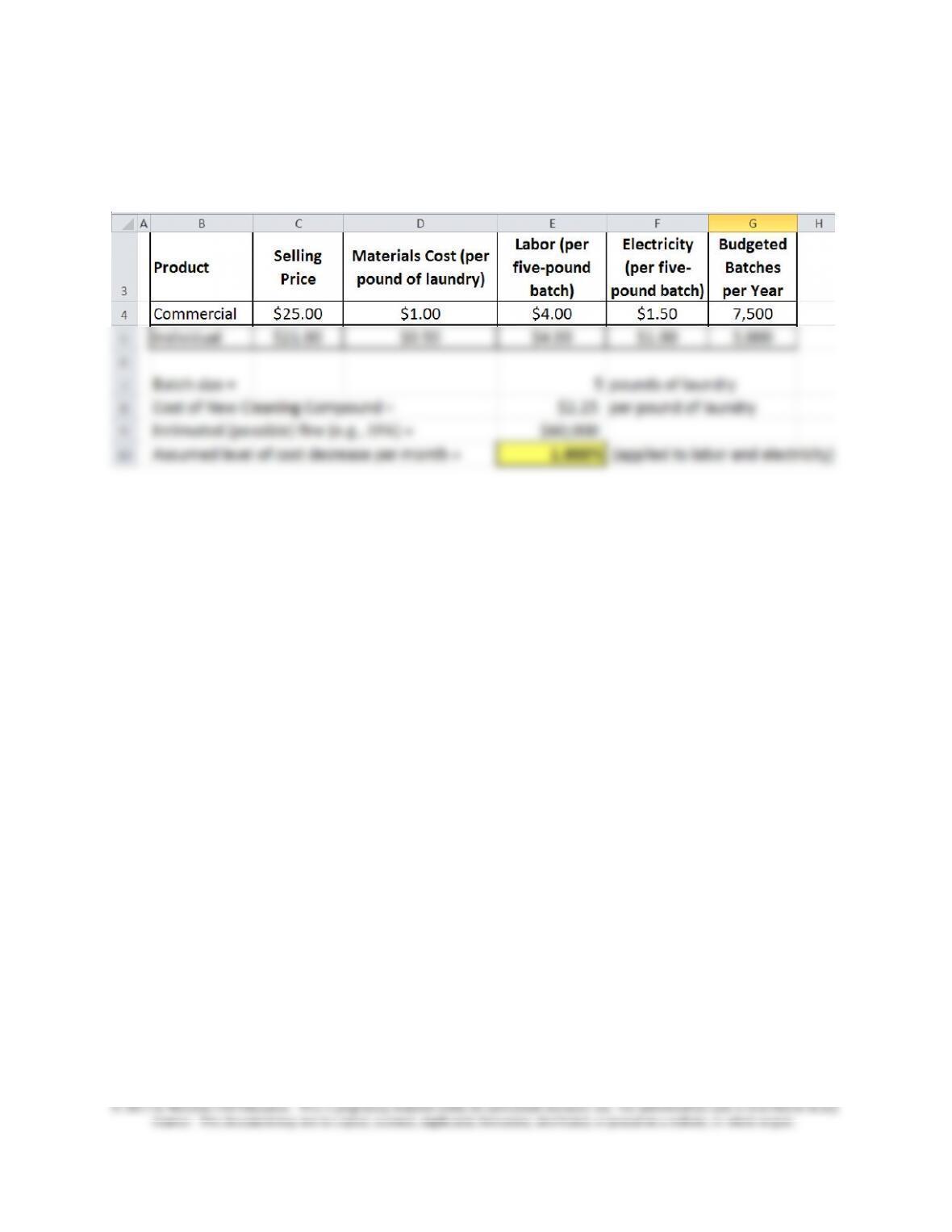

Cell references: $73,125 = cell G32 (=G23); $4,687.50 = cell G42 (=SUM(G37:G41));

$56,250.00 = cell G43.

Revised Level of Monthly Processing Costs (other than materials):

Month Labor Electricity

1 $3,465.00 $1,175.63

2 $3,430.35 $1,163.87

3 $3,396.05 $1,152.23

4 $3,362.09 $1,140.71

5 $3,328.47 $1,129.30

6 $3,295.18 $1,118.01

7 $3,262.23 $1,106.83

8 $3,229.61 $1,095.76

9 $3,197.31 $1,084.80

10 $3,165.34 $1,073.95

11 $3,133.68 $1,063.21

12 $3,102.35 $1,052.58

Total–Yr. 1 $39,367.64 $13,356.88 $52,724.52

\ Year 1 Kaizen-based cost savings (processing costs other than material) $3,525.48

Net Increase in Year-One Processing Costs (materials + labor + electricity) = $69,599.52

Difference between fine and net increase in year-one processing costs $9,599.52

Thus, strictly speaking, it is better to incur the fine rather than change to the new cleaning

compound, even after implementing Kaizen budgeting.

Chapter 10 – Strategy and the Master Budget

10–90

For requirement 3 (below), assume the following input data:

10-58 (Continued-2)

Requirement 3

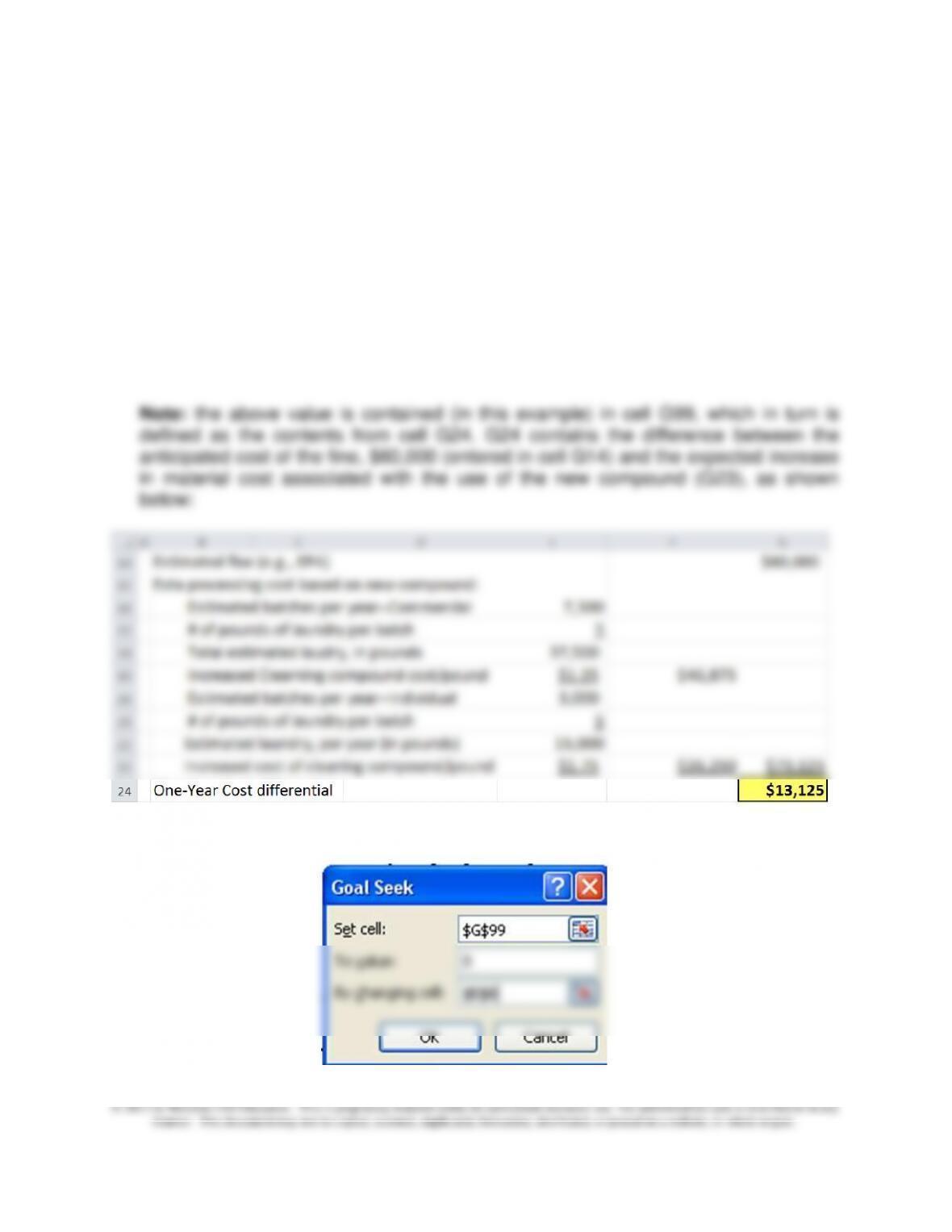

a. Determine the Monthly Cost-Reduction Rate that would Equate the net increase in year-one total

processing costs (materials + labor + electricity) with the anticipated fine

Step One: Define the Breakeven Cost Equation

Difference between the fine and net increase in year-one processing costs $9,599.52

Step Two: Run Goal Seek

Note: cell E10 contains the assumed monthly rate of cost decrease; cell G73

contains arithmetic difference between the cost of the fine and the net increase in

processing costs—other than materials cost, and after implementing Kaizen

budgeting. The value “0” in the above formulation essentially solves for the

Chapter 10 – Strategy and the Master Budget

10–92

10-58 (Continued-3)

b. The cost per pound for the new compound that would equate the anticipated fine with

the net year-one costs, assuming no Kaizen budgeting plan (i.e., no reduction per

month in processing costs):

Step One: Set Up the Cost Equation

Cost differential: anticipated fine and net one-year processing costs, with no Kaizen

budgeting plan = $13,125

Step Two: Run Goal Seek

Chapter 10 – Strategy and the Master Budget

10–93

10-58 (Continued-4)

Cell E8 contains the cost of the new compound, per pound of laundry; cell G99

contains the cost difference: the anticipated fine versus the increased processing

cost attributable to the use of the new compound.

Step Three: Results

new (higher-priced) compound. Of course, other considerations may affect the

ultimate decision.

4. Operational Changes Needed to Ensure Kaizen Cost Savings

The reduction in labor time might be realized by improving the efficiency of

operations, including a decrease in machine downtime. It is probably the case that

line employees (i.e., operating personnel) would have suggestions for ways to

improve operational efficiency (e.g., changes that would reduce idle time as well as

collaborative work with individuals/companies across the value chain. David Duncan

is more likely to achieve his cost-reduction goals by working with his suppliers. As

Chapter 10 – Strategy and the Master Budget

10–94

indicated above, if the cost of the new compound can be decreased by only $0.25

per pound of laundry processed, David would be indifferent (solely on an expected

cost basis) between incurring the fine ($60,000) and the increased processing cost

associated with the use of the new compound ($60,000 as well).

10-58 (Continued-5)

5. Other (qualitative) Considerations that Might Affect the Ultimate Decision:

• What impact, perhaps negative, will the Kaizen budgeting approach have on

employee morale?

• Will the quest to achieve aggressive levels of cost reduction have a negative

effect on service quality?

• Will the use of the new, environmentally friendly cleaning compound have a

beneficial effect on the image of the business and therefore on sales?

• Duncan’s business essentially consists of two service lines/segments:

commercial and individual. Is there a differential effect on marketing activity for

these two groups? (That is, do these groups differ in their response to either

positive or negative media coverage?)

• Would it make more sense for Duncan to invest in new technology, which might

bring the company into full compliance with current emission requirements?

Chapter 10 – Strategy and the Master Budget

10–95

10-59 Ethics in Budgeting/Budgetary Slack (30-40 minutes)

1. a. The reasons that Marge Atkins and Pete Granger use budgetary slack include

the following:

▪ These employees are hedging against the unexpected (i.e., they use slack to

deal with or reduce uncertainty and risk).

higher salaries, promotions, and bonuses.

▪ By “padding the budget,” the manager is more likely to get what he/she

actually needs in terms of resources for the upcoming period.

b. The use of budgetary slack can adversely affect Atkins and Granger by:

▪ limiting the usefulness of the budget to motivate their employees to top

performance

making, as the budgets will show lower contribution margins (lower sales,

higher expenses). Decisions regarding the profitability of product lines,

staffing levels, incentives, etc. could have an adverse effect on Atkins’s and

Granger’s departments.

2. The use of budgetary slack, particularly if it has a detrimental effect on the company,

may be unethical. In assessing the situation, the IMA’s Statement of Ethical

Professional Practice can be consulted (www.imanet.org). This statement notes that

“a commitment to ethical professional practice” includes: overarching principles

(expressions of core values) and a set of standards intended to guide actual conduct

and practice.

10–96

10-59 (Continued)

The IMA’s overarching PRINCIPLES include: Honesty, Fairness, Objectivity, and

Responsibility. The list of STANDARDS includes the following: Competence,

Confidentiality, Integrity, and Credibility. The following Standards could be

referenced in conjunction with the use of budgetary slack, as described above:

▪ Competence: Provide decision support information and recommendations that

understanding of the reports, analyses, or recommendations.

Though not asked for in the original CMA exam problem, you might want to discuss

with students how, in practice, they would deal with ethical dilemmas. In its

Resolution of Ethical Conflict statement the IMA provides the following guidance:

1. Discuss the issue with your immediate supervisor except when it appears that

the supervisor is involved. In that case, present the issue to the next level. If

you cannot achieve a satisfactory resolution, submit the issue to the next

management level. If your immediate superior is the chief executive officer or

equivalent, the acceptable reviewing authority may be a group such as the

3. Consult your own attorney as to legal obligations and rights concerning the

ethical conflict.

Chapter 10 – Strategy and the Master Budget

10–97

10–60 Criticisms of Traditional Budgeting/Incentive Issues (45 Minutes)

Many critics of conventional budgeting procedures cite dysfunctional consequences of

using fixed-performance budgets in managerial compensation contracts. These

individuals believe, among other problems, that such contracts motivate managers and

employees to “game the performance indicator,” that is, to take actions that improve the

performance indicator but are not value-adding to the organization. The following are

selected examples of “gaming behavior”:

• managing earnings by pushing expenses into the future (e.g., by delaying

purchases, delay making new hires, delaying an important product-development

initiative, or delaying needed expenditures)

• “channel stuffing” (or “trade loading”)—that is, shipping excessive amounts of

products to distributors to meet near-term sales goals, recognizing that many

such products are likely to be returned; such items are sometimes referred to as

“sale–or–return” products

• announcing price hikes for the next fiscal year, in an attempt to motivate

increases in end-of-current-year sales

• shifting funds between accounts to avoid budget overruns (costly, non-value-

added managerial activity)

Other dysfunctional consequences of traditional fixed-performance reward systems

include the following:

• negotiating low targets and high rewards (i.e., pushing for targets that are

inwardly comfortable yet appear outwardly difficult to achieve)

• spending whatever is in your budget (“use it or lose it”)

• intentionally asking for more resources than you need, anticipating that

Chapter 10 – Strategy and the Master Budget

10–98

reductions to your request will be made during the upcoming budget negotiation

process

10–60 (Continued)

In addition to gaming behavior, some critics suggest that excessive reliance on budget–

based incentive contracts leads to unethical and even fraudulent behavior. This

conclusion is based on the view that in an attempt to meet budgeted performance

requirements (which are tied to compensation), managers resort to questionable, if not

illegal, behaviors. Enron and WorldCom serve as good examples.

Critics of conventional budgeting practices, including those in the Beyond Budgeting

budgeting systems. Because of the use of time equations, and therefore greater

specification of resource requirements, the use of time-driven activity-based budgeting

(TDABB) may be particularly useful.

Chapter 10 – Strategy and the Master Budget

10–99

Check Figures: Chapter 10

10–24 Production Budget, 2nd Quarter = 75,600 units; Materials Purchases Budget, 2nd

Quarter = 223,080 lbs.

10–25 1. November, $242,111; December, $187,082; 2. November, $171,500;

December, $124,250

10–34 1. 1,000 units; 2. Alternative 1 = 4,000 units, Alternative 2 = 3,000 units; 3.

Alternative 1 = $400,000, Alternative 2 = $300,000

10–35 2. $1,050,000

10–36 2. Total Cash Available: I = $381, IV = $533, Year = $1,696; Total

Disbursements: I = $427, II = $426, III = $437, Year = $1,711; Borrowing from

Endowment Fund: I = $54, II = $0, IV = $0; Year = $166; 3. $23,000

10–37 No check figure

Chapter 10 – Strategy and the Master Budget

10-100

10–43 1. For February: 95 (from December), 90 (from January); For March: 100 (from

10–49 1 = $1,800,000 (C12); 2 = 11,900 (C12); 3 = $342,900 (budgeted purchases,

RM1); 4 = $1,078,500 (budgeted direct labor cost); 5 = $293,472 (budgeted

variable overhead), $245,579 (budgeted fixed overhead); 6 = $2,057,200 (CGS),

$48,596 (Ending Inventory); 7 = $645,000 (budgeted selling & administrative

expenses); 8 = $646,680 (after-tax income)

10-101

10–55 1. January: total premiums earned from active policy holders = $9,975,000;

February: number of active policyholders, beginning of month = 99,500; total

premiums earned from active policy holders = $9,925,125; December: number of

active policyholders = 94,635; estimated no. of policyholders, beginning of new

10–59 No check figure

10–60 No check figure