Chapter 19 – Strategic Performance Measurement: Investment Centers

19–42 Return on Investment (ROI); Strategy Map; Review of Chapter 18;

Correlation Analysis (60 minutes)

The objective of this problem is to have the student think of performance

evaluation in terms of the strategy map, as defined in Chapter 2 (and

illustrated in Exhibit 2.6). Moreover, the problem helps to show, using the

concept of the strategy map, that financial measures such as ROI are

linked to other measures in the balanced scorecard.

In addition to the ROI for each of the 15 units, the information provided

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–47

19–42 (continued-1)

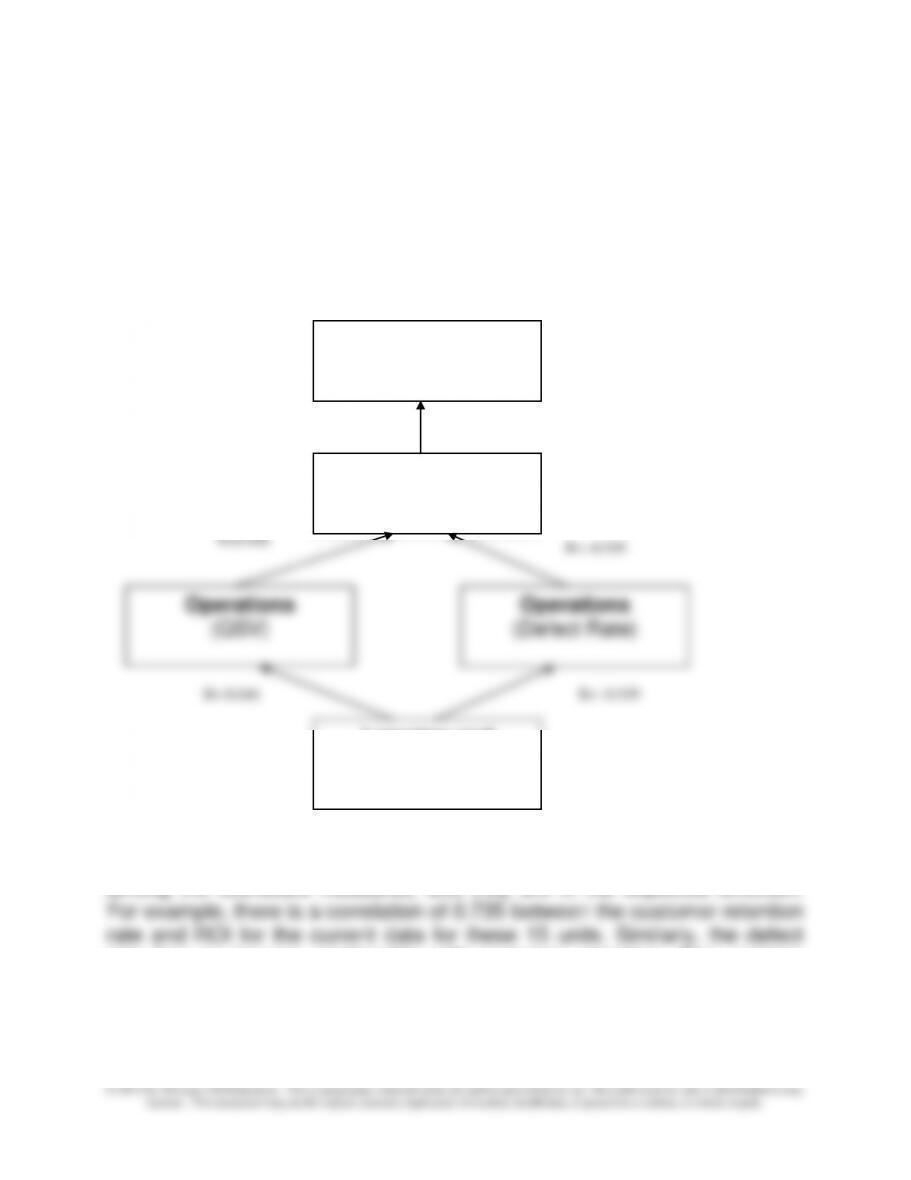

The strategy map (see text Exhibit 2.6) can be used to link these

scorecard measures in the following way. The correlation values (R) are

shown next to the related link in the strategy map. Note that there are two

measures and therefore two links in the operations perspective.

R= -0.539

R= 0.646

These correlations suggest that there is an important degree of correlation

among the scorecard measures, and they are in the expected direction.

rate has an inverse relationship with customer retention. Also, training

hours seems to have the desired effect of improving QSV and reducing the

defect rate.

Customer

(Retention rate)

Financial

(ROI)

Learning and

Growth

(Training Hours)

R = 0.735

R= -0.509

R=0.488

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–42 (Continued-2)

The next step could be to ask why the effect of training on the defect rate is

not stronger, or why the QSV score does not have a stronger effect on

customer retention. Are these in fact the key scorecard measures, or are

there other measures that might be more important in influencing customer

retention and ROI?

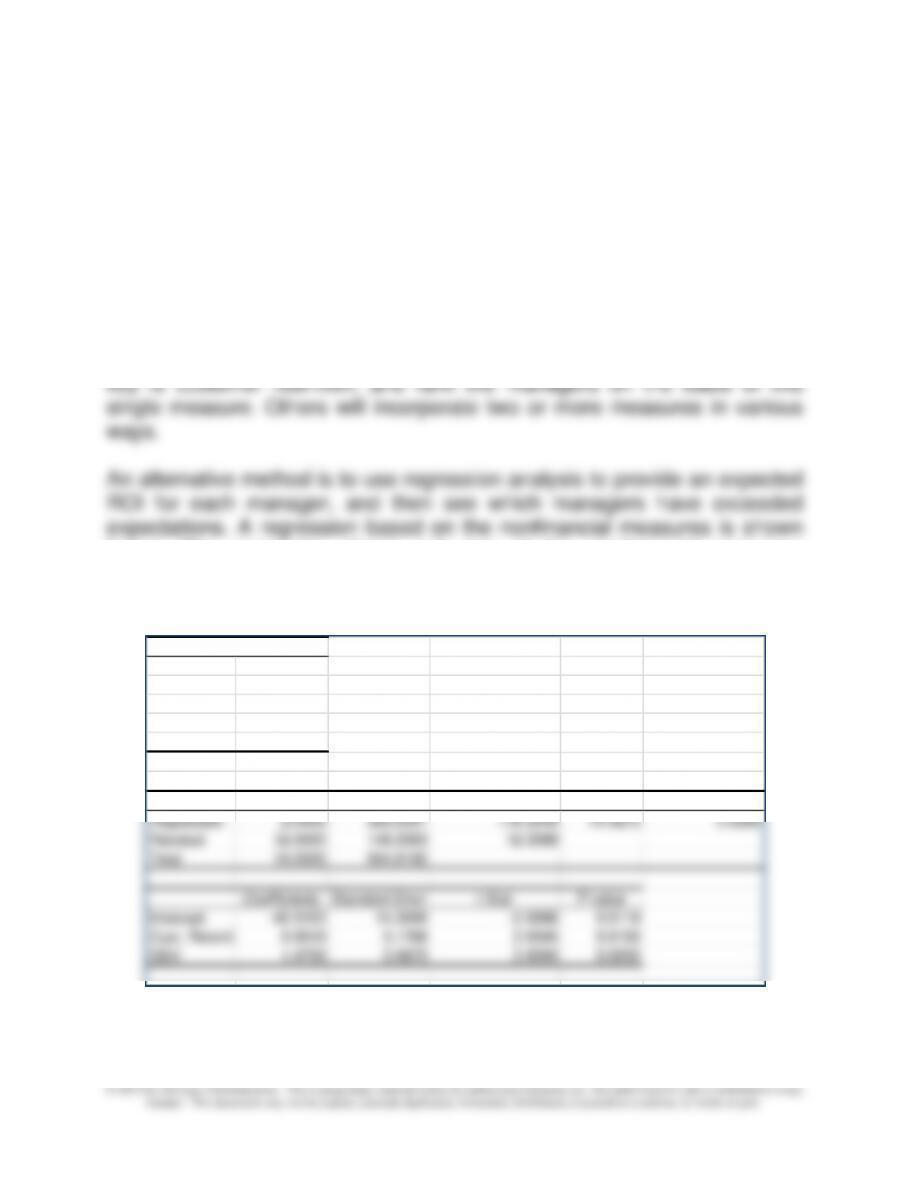

2. There are a number of ways to determine the best and worst managers/

units. Some students choose a single measure as the dominant scorecard

measure (such as ROI) and select on this basis. Others might say that the

below. The regression shows only two of the nonfinancial measures

(customer retention and QSV) because of the high multicollinearity among

the four measures.

Regression Statistics

Multiple R 0.8404

R Square 0.7063

Adjusted R S

0.6573

Standard Erro

3.5155

Observations 15

ANOVA

df SS MS F Significance F

Regression 2.0000 356.6097 178.3049 14.4273 0.0006

Residual 12.0000 148.3063 12.3589

Total 14.0000 504.9160

Coefficients Standard Error t Stat P-value

Intercept –42.5153 14.3689 –2.9588 0.0119

Cust. Retenti

0.5010 0.1768 2.8345 0.0150

QSV 1.4750 0.5673 2.6000 0.0232

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–42 (continued-3)

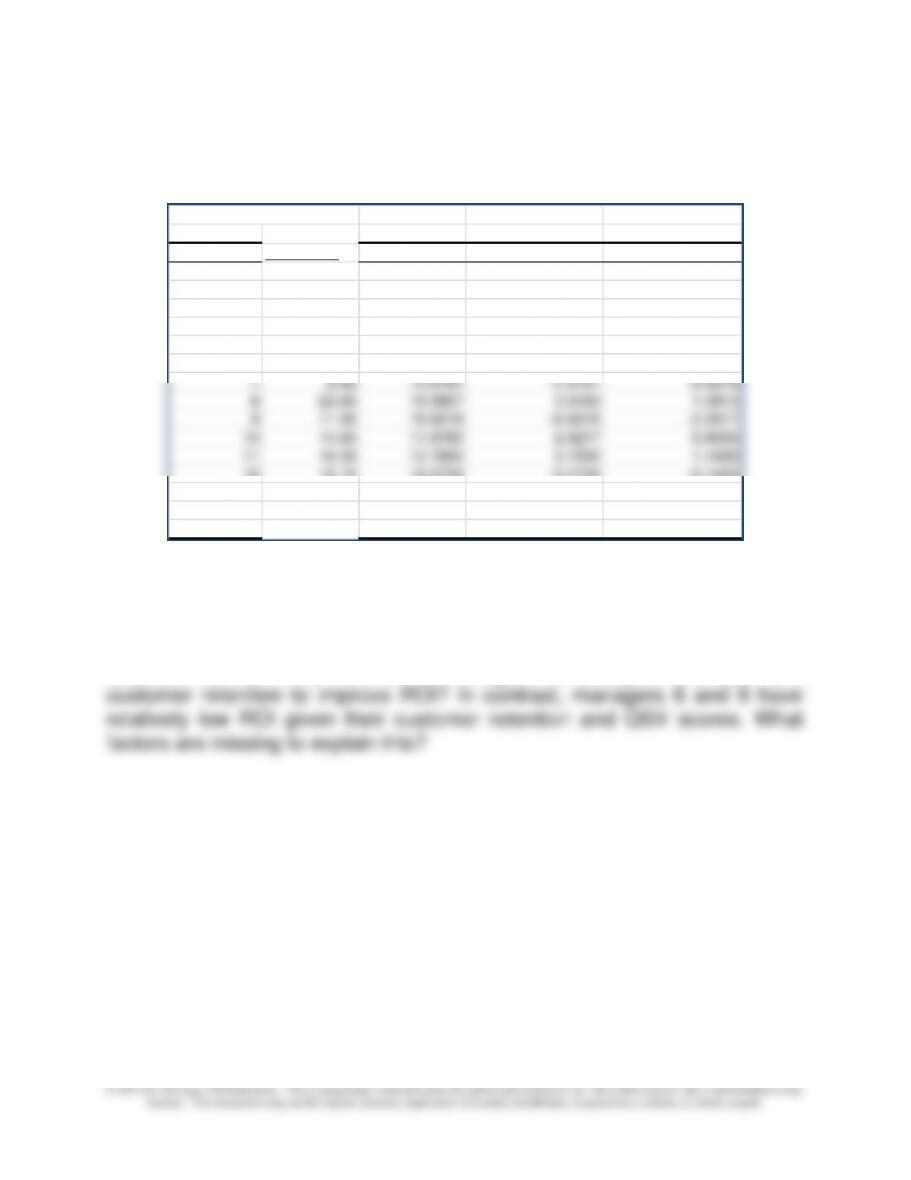

This regression has the following residual analysis:

Using this approach, and assuming that QSV and customer retention are

useful predictors of ROI, managers 1, 5, and 11 produced ROIs somewhat

higher than would have been expected given their QSV and customer

retention scores. What have these managers done beyond the QSV and

RESIDUAL OUTPUT

Manager Actual ROI Predicted ROI Residuals Standard Residuals

1 21.30 17.5617 3.7383 1.1486

2 15.40 18.4856 -3.0856 -0.9480

3 9.60 9.7738 -0.1738 -0.0534

4 12.40 13.0965 -0.6965 -0.2140

5 18.60 15.0786 3.5214 1.0819

6 4.50 8.8280 -4.3280 -1.3297

12 12.10 12.5734 -0.4734 -0.1455

13 6.20 3.5672 2.6328 0.8089

14 1.30 2.4649 -1.1649 -0.3579

15 9.70 10.6475 –0.9475 –0.2911

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–50

19–43 Return on Investment (ROI); Residual Income (RI) (45 minutes)

1. The calculation of the unit contribution margin for Reigis Steel Division,

assuming 1,484,000 units were produced and sold during the year

ended November 30, 2013 is presented below.

Reigis Steel Division

Operating Statement

For the Year Ended November 30, 2013

($000 omitted)

Sales Revenue

$35,000

Less Variable Costs

Cost of Goods Sold

$18,500

Selling Expenses ($2,700 × 40%)

1,080

19,580

Contribution Margin

$15,420

2. Calculations of selected performance measures for 2013 for Reigis Steel

Division are presented below

a. The pretax return on average investment in operating assets

employed is 12.2%, calculated as follows:

b. The calculation of residual income (RI) on the basis of average

operating assets employed is as follows:

RI = income from operations before taxes – minimum

required return on average assets

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–51

19–43 (continued)

3. The management of Reigis Steel would have been more likely to accept

the contemplated capital acquisition if residual income (RI) were used as

the performance measure because the investment would have

investment that would lower the overall ROI (12.2% for 2013), even

though the return is higher than the required minimum, as this would

lower bonus rewards.

4. Reigis must be able to control all items related to profits and investment

if it is to be evaluated fairly as an investment center using either ROI or

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–52

19-44 Calculating ROI and RI and Comparing Results (20-30 minutes)

1. a. ROI = Operating Income ÷ Average Assets

= $2,450,000 ÷ {[$15,000,000 + $15,000,000 ÷ 1.05] ÷ 2}

= $2,450,000 ÷ $14,642,857 = 16.73%

b. RI = Operating Income – (Investment × Min. rate of return)

2. In this case residual income (RI) provides the desired incentive for local

managers to make investments desired by top management. Delta

3. Like many organizations, Blackwood Industries should benefit from a

management control system which gives explicit attention to strategic

factors. The balanced scorecard (BSC) would be a useful approach to

accomplish this objective. The BSC considers not only financial

factors, but also non-financial factors such as progress with customer

relations, improvements in operations, and improvements in

capabilities of employees. The balanced scorecard would thus be a

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–53

19–45 Residual Income (RI), Performance Evaluation Time Horizon (45-60 Minutes)

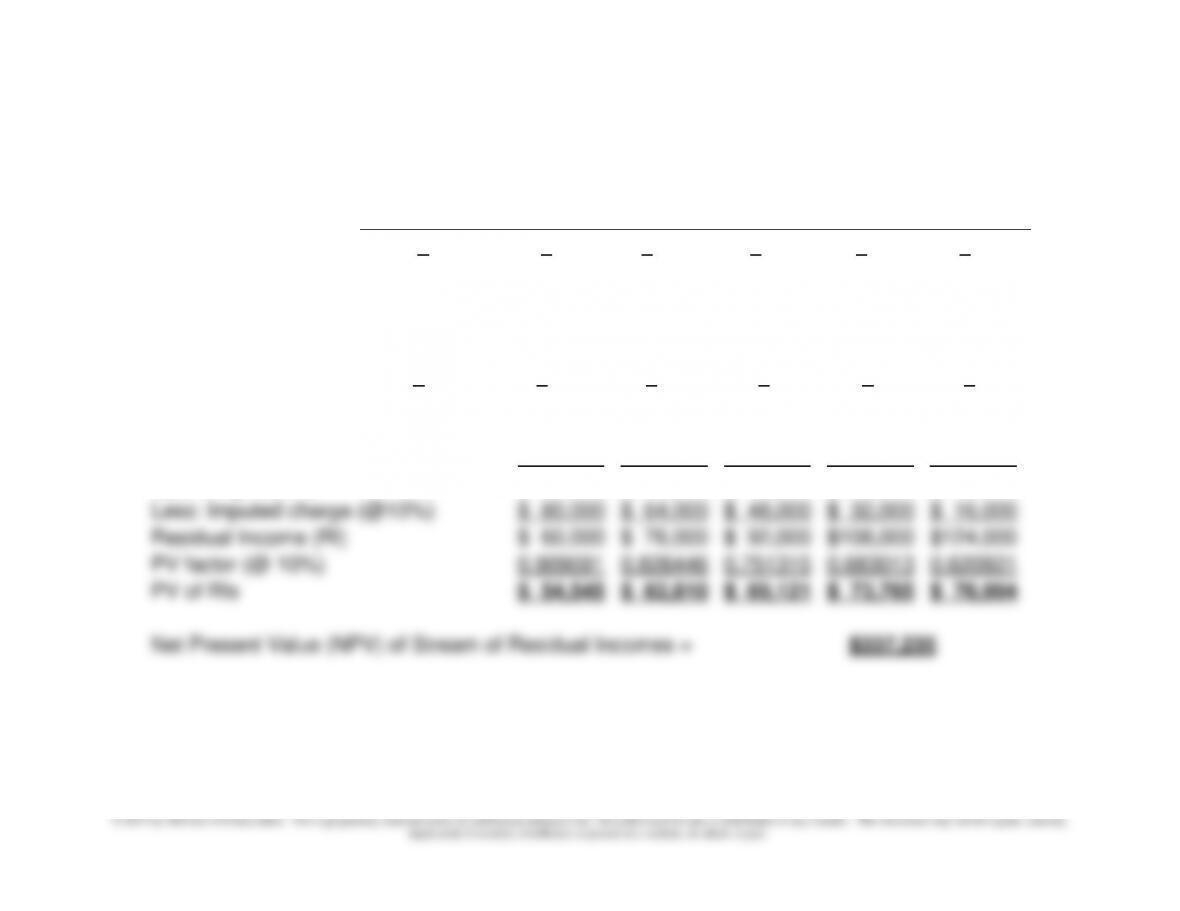

1. Estimated NPV of cash flows and estimated NPV of Residual Incomes (RI):

Time Period (Year)

0

1

2

3

4

5

Depreciation Expense =

$160,000

$160,000

$160,000

$160,000

$160,000

Beg.–of-Year NBV of asset =

$800,000

$640,000

$480,000

$320,000

$160,000

Time Period (Year)

0

1

2

3

4

5

Residual Incomes (RI):

Cash Inflow

$300,000

$300,000

$300,000

$300,000

$300,000

Less: Depreciation (SL)

$160,000

$160,000

$160,000

$160,000

$160,000

Operating Income

$140,000

$140,000

$140,000

$140,000

$140,000

Less: Imputed charge (@10%)

$ 80,000

$ 64,000

$ 48,000

$ 32,000

$ 16,000

Residual Income (RI)

$ 60,000

$ 76,000

$ 92,000

$108,000

$124,000

PV factor (@ 10%)

0.909091

0.826446

0.751315

0.683013

0.620921

PV of RIs

$ 54,545

$ 62,810

$ 69,121

$ 73,765

$ 76,994

Net Present Value (NPV) of Stream of Residual Incomes =

$337,235

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–54

19-45 (Continued)

Time Period (Year)

0

1

2

3

4

5

Cash Flow

($800,000)

$300,000

$300,000

$300,000

$300,000

$300,000

PV factor (@ 10%)

1.000000

0.909091

0.826446

0.751315

0.683013

0.620921

PV of cash flows

($800,000)

$272,727

$247,934

$225,394

$204,904

$186,276

Net Present Value (NPV) of Stream of Cash Flows =

$337,235

2. The basic issue illustrated in the calculations presented above in (1) pertains to the incentive effects

of financial performance metrics, such as ROI and Residual Income (RI). We know from Chapter 12

that long-term investment decisions are typically made on the basis of a discounted cash flow (DCF)

basis. On the other hand, it is more typical that subsequentfinancial analysis of investment projects is

conducted using accrual-based accounting data, e.g., ROI or Residual Income (RI). This divergence

achieve goal congruency. (In this regard, see also Problem 19-37.)

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–55

19–46 EVA® NOPAT and EVA® Capital; Operating Approach (45-60

Minutes)

Students should understand that EVA® is an approximation of an

entity’s true (i.e., “economic”) profits for a period. This measure of

profitability is defined as the difference between the entity’sNOPAT (net

operating profit after tax) and an imputed capital charge. NOPAT is

supposed to approximate the entity’s actual cash yield generated for

investors from recurring business activities during the period. The

amount of capital employed is supposed to represent the cash that

investors have put at risk in the firm, and upon which they expect an

appropriate return.To estimate both NOPAT and the amount of capital

for a period, the analyst begins with reported financial statement

amounts and then makes adjustments. These adjustments, in the

parlance ofEVA®, are collectively referred to as “equity equivalent

adjustments.”

The Operating Approach to NOPAT estimation starts by deducting

operating expenses—including depreciation—from sales. Next, equity-

equivalent (EE) reserve adjustments are made. Interest expense,

because it is a financing charge,is ignored, but other (operating) income

is added to get pretax economic profits, or Net OperatingProfit Before

1. EVA®NOPAT—Operating Approach (see next page):

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–56

19–46(Continued-1)

Net Sales

$2,000

Less: CGS

1,670

Gross Margin

$ 330

Less: S,G,& A Expenses

185

Less: Depreciation Expense

35

Less: Other (cash) operating expenses

50

$60

Adjustments:

Increase in LIFO reserve (1)

2

Imputed Interest—Non-capitalized leases (2)

4

Net Operating Profit

$66

Plus: Other Operating Income

12

NOPBT

$78

Less: Cash taxes paid on net operating profit:

Reported Tax Expense

$20

Less: Increase in Deferred Tax (3)

5

Plus: Tax Savings (foregone) on Interest (4)

10

25

NOPAT

$53

Interest Expense to Calculate Tax Savings (@40%):

Reported interest expense

$22

Imputed interest on non-cap. Leases

$4

Total interest (financing) expense

$26

Rationale for EE Adjustments made:

(1) LIFO Reserve: brings into earnings the current-period effect of

unrealized gain attributableto holding inventory during period of rising

leases because this is a financing, not operating, expense.

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–57

19–46 (Continued-2)

(3) Increase in Deferred Taxes: If the Deferred Tax liability increases

during a period, itimplies that cash taxes paid during the year <

shield (tax savings) from NOPAT income as well.

2. EVA® Capital—Operating Approach:

Reported Current Assets (CA)

$510

Plus: LIFO Reserve (1)

10

Adjusted CA

$520

Less: NIBCLS:

Accounts Payable

$150

Income Tax Payable

20

Other Current Liabilities

200

370

Net Working Capital

$150

Net Plant, Property, Equipment

$605

PV of Non-capitalized leases (2)

50

Adjusted PPE

655

Other Long-term Assets

120

EVA® Capital

$925

Rationale for Adjustments Made:

(1) LIFO Reserve: this adjustment converts the balance-sheet inventory

amount from a LIFO to a FIFO cost basis. In so doing, the resulting

amount better approximates the current replacement cost of

would consider an accounting “distortion.”)

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–58

19–46 (Continued-3)

3. EVA® estimate—Operating Approach:

EVA® NOPAT =

$53

Capital Charge:

EVA® Capital =

$925

WACC =

10.70%

$99

EVA® =

($46)

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–59

19-47 EVA® NOPAT and EVA® Capital; Financing Approach (45-60

Minutes)

1. Students should understand that EVA® is an approximation of an

entity’s true (i.e., “economic”) profits for a period. This measure of

profitability is defined as the difference between the entity’sNOPAT (net

operating profits after tax) and an imputed capital charge. NOPAT is

supposed to approximate the entity’s actual cash yield generated for

investors from recurring business activities during the period. The

amount of capital employed is supposed to represent the cash that

investors have put at risk in the firm, and upon which they expect an

appropriate return.To estimate both NOPAT and the amount of capital

for a period, the analyst begins with reportedfinancial-statement

amounts and then makes adjustments. These adjustments, in the

parlance ofEVA®, are collectively referred to as “equity equivalent

adjustments.”

The financing approach to estimating EVA® NOPAT begins with the

reported amount of income available to common shareholders. To this

amount, adjustments are made to eliminate financingeffects (distortions)

and accounting distortions (such as LIFO reserve adjustments and

adjustmentsregarding Deferred Income Taxes). The financing approach

to estimating EVA capital consists of adding together interest-bearing

debt + equity in the firm.

1. EVA® NOPAT—Financing Approach:

Income available to common

$30

Plus: Equity-Equivalent (EE) Adjustments:

Increase in Deferred Tax account (1)

$5

Increased in LIFO Reserve (2)

2

7

Adjusted Income to Common

$37

Financing Adjustments:

Reported Interest Expense

$22

Imputed Interest—Leases (3)

4

$26

Tax Savings (Foregone) on Interest (4)

10

Interest Expense after Income Tax Effects

16

EVA® NOPAT

$53

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–60

19–47 (Continued-1)

Rationale for above (EE) adjustments:

(1) Change in Deferred Tax account: this adjustment converts reported

tax expense to approximate the amount of cash tax expense

(2) Increase in LIFO reserve: this adjustment converts LIFO (i.e., “old”)

operating, activity, its net effect (after-tax) needs to be removed

from reported earnings.

2. EVA® Capital—Financing Approach:

Total debt + leases:

Short-term Interest-bearing debt (10%)

$100

Long-term Interest-bearing debt (8%)

150

PV of non-capitalized leases (1)

50

Other long-term liabilities

120

$420

Common equity

425

Equity-Equivalent (EE) Adjustments:

LIFO reserve (2)

$10

Deferred Income Tax (3)

70

80

EVA® Capital

$925

Rationale for above changes:

(1) PV of non-capitalized leases: this adjustment is needed to bring

consistency betweenthe treatment of capital and operating leases,