Chapter 10 – Strategy and the Master Budget

10–31 Purchase Discounts (25 minutes)

The financial cost of not taking advantage of the early-payment discount for

purchases made on credit can be approximated by the following formula (we use

the term “approximate” here to denote the fact that the estimate below does not

assume compounding of interest and as such provides a conservative estimate):

1. In the case of 2/10, n/30, the approximate economic cost of not taking

advantage of the early-payment discount is:

= [0.02 ÷ (1 − 0.02)] × [365 ÷ 20] = 0.020408 × 18.25 = 37.25%

Basically, if you choose not to take the early-payment discount, you are giving

up a 2% discount (on the net amount) in return for an extra 20 days in which

of the net bill (the bill without financing cost).

2. In the case of 1/10, n/30, the opportunity cost of not taking advantage of the

early-payment cash discount is:

3. Given the significant opportunity cost of not taking advantage of early-

payment cash discounts, good accounting practice would be to record

Chapter 10 – Strategy and the Master Budget

10–17

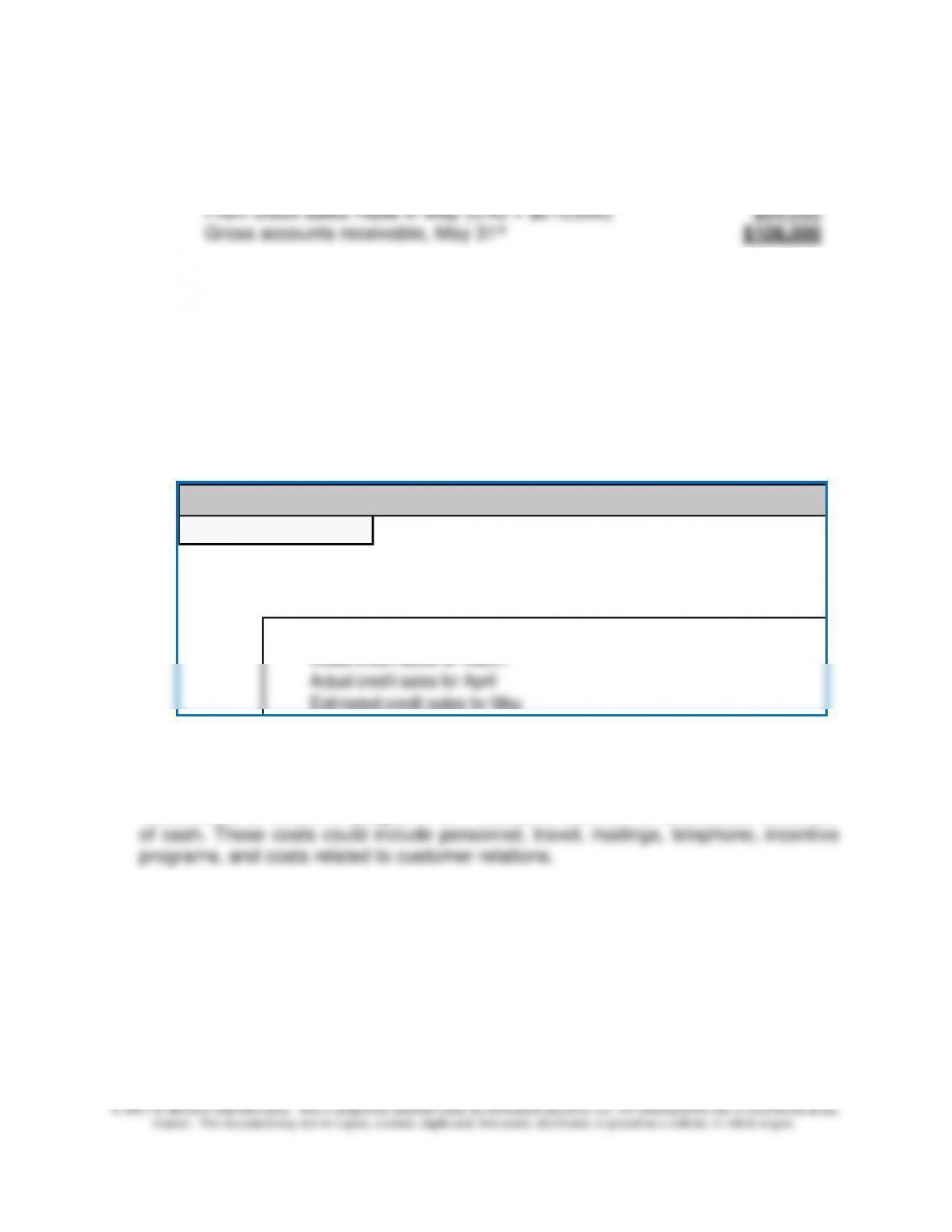

10-32 Accounts Receivable Collections and Sensitivity Analysis (50 minutes)

Original Assumptions/Data:

Actual credit sales for March $130,000

Actual credit sales for April $160,000

Estimated credit sales for May $210,000

Estimated collections in month of sale 25%

Estimated collections in first month following month of sale 60%

1. Estimated cash receipts from collections in May:

Collection from sales in March (0.10 × $130,000) $13,000

Collection from sales in April (0.60 × $160,000) $96,000

2. Gross accounts receivable, May 31st:

From credit sales made in April (0.15 × $160,000) $24,000

3. Net accounts receivable, May 31st:

Gross accounts receivable, May 31st $181,500

Less: Allowance for uncollectible accounts:

4. Revised data/assumptions:

Actual credit sales for March $130,000

Actual credit sales for April $160,000

Estimated credit sales for May $210,000

Estimated collections in month of sale 60%

a. Estimated cash receipts from collections in May:

Collection from sales in March (0.10 × $130,000) $13,000

Chapter 10 – Strategy and the Master Budget

10–18

10–32 (Continued)

b. Gross accounts receivable, May 31st:

From credit sales made in April (0.15 × $160,000) $24,000

Note to Instructor: An Excel spreadsheet solution file is embedded in this document.

You can open the spreadsheet “object” that follows by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return

to…” while you are in the spreadsheet mode. The screen should then

return you to the Word document.

5. The principal benefit is the accelerated receipt of cash, which the company can

potentially employ to pay down debt, reduce borrowing, invest, etc. Principal costs

would relate to whatever programs are needed to secure the accelerated collection

Actual credit sales for March

Estimated credit sales for May

Exercise 10-32: Accounts Receivable Collections and Sensitivity Ana

Background

Papst Company is preparing its cash budget for the month of May. The follow

concerning its accounts receivable:

Chapter 10 – Strategy and the Master Budget

10–19

10–33 “What–If” Analysis (20-25 Minutes)

1. The term “what if” analysis is one example of the more general term “sensitivity

analysis” and is used to explore the effects (e.g., on a decision or a budget for an

upcoming period) of different marketing, production, or selling strategies (e.g., the

case, if an underlying assumption (viz., rate of bad debts expense) changes.

2. What-if Analysis

January

February

March

Credit Sales

$100,000

$120,000

$110,000

Estimated Bad Debts Expense

January

February

March

Assumed rate of B/D

expense:

1%

$1,000

$1,200

$1,100

3%

$3,000

$3,600

$3,300

5%

$5,000

$6,000

$5,500

8%

$8,000

$9,600

$8,800

3. Managers today work in a world of uncertainty. One way to cope with uncertainty

in the master budgeting process is to model the underlying relationships

associated with the various budgets that are prepared and then to perform

10–20

10-34 Profit Planning and Sensitivity Analysis (40-45 minutes)

1. Sales volume in units:

Let “X” = required sales volume. Thus, when total cost at each alternative cost

structure is the same, we have:

$85.00X + $40,000 = $80.00X + $45,000

X =

1,000 units

2. Sales level needed:

Pre-tax profit = (cm/unit * X) − FC = 5% (sp/unit * X)

0 = [(cm/unit * X) − 5% (sp/unit * X)] − FC

X = FC ÷ [(cm/unit) − 5% (sp/unit)]

Alternative 1

Alternative 2

Selling price/unit =

$100.00

$100.00

Variable cost/unit =

$85.00

$80.00

Contribution margin/unit =

$15.00

$20.00

Operating profit target (%) =

5%

5%

Required Sales Volume =

4,000

3,000

Check:

Sales Revenue

$400,000

$300,000

Variable Costs

$340,000

$240,000

CM

$60,000

$60,000

Fixed Costs

$40,000

$45,000

Operating Profit

$20,000

$15,000

Operating Profit ÷ Sales Revenue

5.00%

5.00%

3. Sales volume in dollars needed under each alternative to achieve a profit

goal of 5% on sales.

FC = (cm ratio * X) − 5.00%X

X = FC ÷ [(cm ratio − 5.00%)*X]

Targeted pre-tax profit (% of sales) =

5.00%

5.00%

Let X = sales dollars, then:

Pre–tax profit = [(cm ratio)*X] − FC = 5.00%X

Chapter 10 – Strategy and the Master Budget

10–21

10–34 (Continued)

Alternative 1

Alternative 2

Selling price/unit =

$100.00

$100.00

Contribution margin/unit =

$15.00

$20.00

Contribution margin ratio =

15.00%

20.00%

Operating profit target (%) =

5%

5%

Required Sales Volume =

$400,000

$300,000

Check:

Sales Revenue

$400,000

$300,000

Variable Costs

$340,000

$240,000

CM

$60,000

$60,000

Fixed Costs

$40,000

$45,000

Operating Profit

$20,000

$15,000

Operating Profit ÷ Sales Revenue

5.00%

5.00%

Chapter 10 – Strategy and the Master Budget

10–22

10–35 Scenario Analysis (45-50 minutes)

1. “What-If Analysis,” within the context of budgeting, refers to the process of varying

one or more budget inputs for the purpose of examining the resulting effect on a

variable of interest (e.g., budgeted sales, operating income, or operating cash flows).

Scenario analysis can be viewed as the result of simultaneously changing two or

more inputs and examining the resulting effect on a variable of interest.

The basic version of Excel can perform three kinds of “what–if” analyses: scenarios,

data tables, and Goal Seek. Scenarios and data tables take sets of input values and

determine possible results. A data table works only with one or two variables, but it

can accept many different values for those variables. A scenario can have multiple

variables, but it can accommodate only up to 32 values. Goal Seek works differently

from scenarios and data tables in that it takes a result and determines possible input

values that produce that result. In addition to these three methods, an Excel add-in,

Solver, can be used to perform “what–if” analyses. The Solver add-in is similar to

Goal Seek, but it can accommodate more variables.

See the following tutorials for additional information about performing “what–if”

analyses using Excel 2010:

1. Introduction to What-If Analysis:

http://office.microsoft.com/en-us/excel-help/introduction–to-what-if–analysis-HA010342628.aspx

2. Using Excel to Perform Scenario Analysis:

http://office.microsoft.com/en-us/excel-help/switch-between-various-sets-of-values-by-using-scenarios-

HP010072669.aspx

3. Using Excel to Create Data Tables:

http://office.microsoft.com/en-us/excel-help/calculate-multiple-results-by-using-a-data-table-

HP010342214.aspx

4. Using the Goal Seek Routine in Excel:

http://office.microsoft.com/en-us/excel-help/use-goal-seek-to-find-the-result-you-want-by-adjusting-an–

input-value-HP010342990.aspx

5. Using Solver to Perform What-If Analysis:

http://office.microsoft.com/en-us/excel-help/define-and-solve-a-problem-by-using-solver-

HP010342416.aspx

http://office.microsoft.com/en-us/excel-help/video-use-the-solver-add-in-VA101840549.aspx

Chapter 10 – Strategy and the Master Budget

10–23

10–35 (Continued)

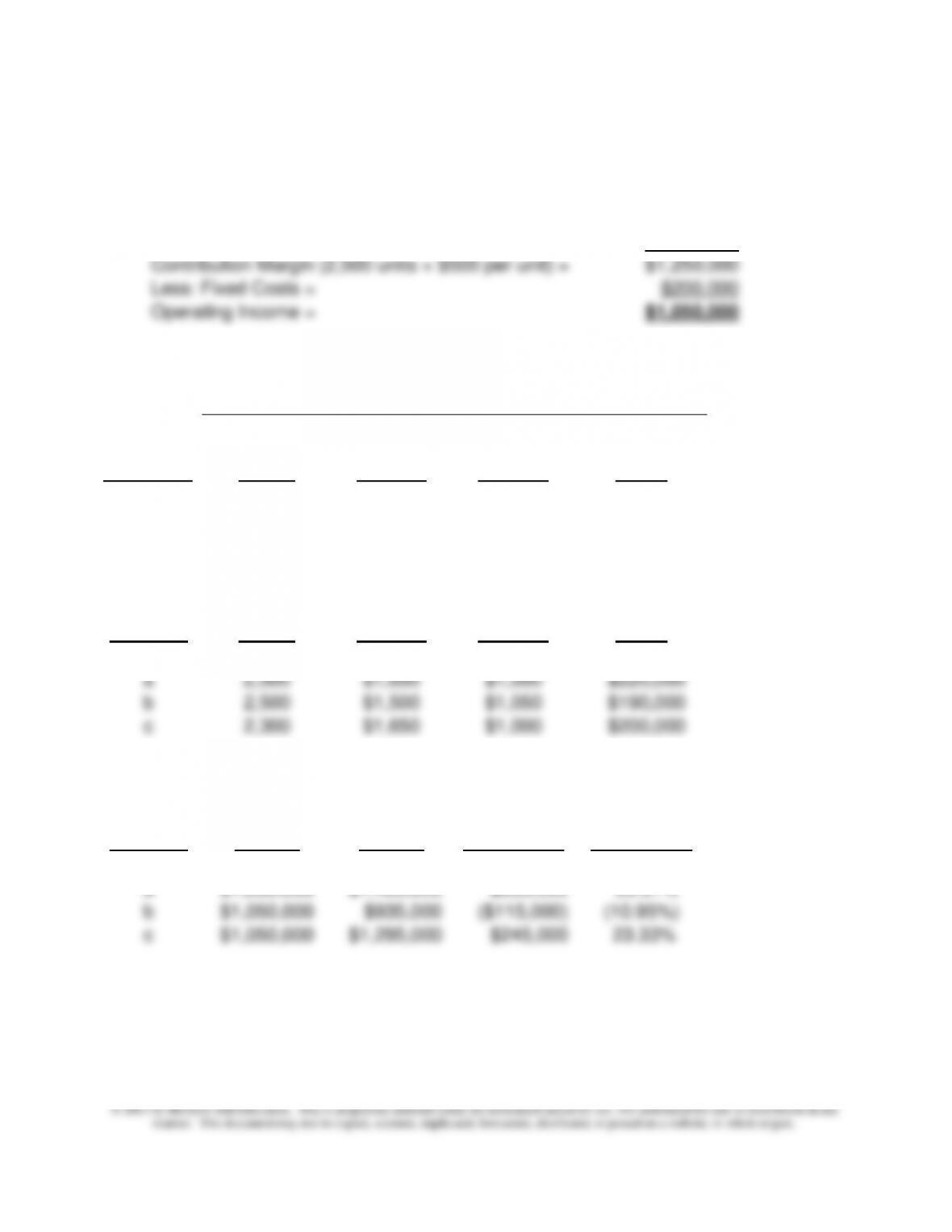

2. Budgeted Operating Income—Current Year:

Sales Revenue (2,500 units × $1,500 per unit) =

$3,750,000

Less: Variable Costs (2,500 units × $1,000 per unit)

$2,500,000

Contribution Margin (2,500 units × $500 per unit) =

$1,250,000

Less: Fixed Costs =

$200,000

Operating Income =

$1,050,000

3. Scenario Analysis:

Percentage Change from Baseline

Sales

Volume

Selling

Price

Variable

Cost

Total Fixed

Scenarios

(units)

per Unit

per Unit

Costs

a

0.00%

10.00%

0.00%

10.00%

b

0.00%

0.00%

5.00%

(5.00%)

c

(8.00%)

10.00%

0.00%

0.00%

Sales

Volume

Selling

Price

Variable

Cost

Total Fixed

Scenario

(units)

per Unit

per Unit

Costs

Baseline

2,500

$1,500

$1,000

$200,000

a

2,500

$1,650

$1,000

$220,000

b

2,500

$1,500

$1,050

$190,000

c

2,300

$1,650

$1,000

$200,000

$ Difference

% Change

Baseline

Operating

Budgeted

Operating

From

Baseline

from

Baseline

Scenario

Income

Income

Op. Income

Op. Income

Baseline

$1,050,000

$1,050,000

$0

0.00%

a

$1,050,000

$1,405,000

$355,000

33.81%

b

$1,050,000

$935,000

($115,000)

(10.95%)

c

$1,050,000

$1,295,000

$245,000

23.33%

Chapter 10 – Strategy and the Master Budget

10–24

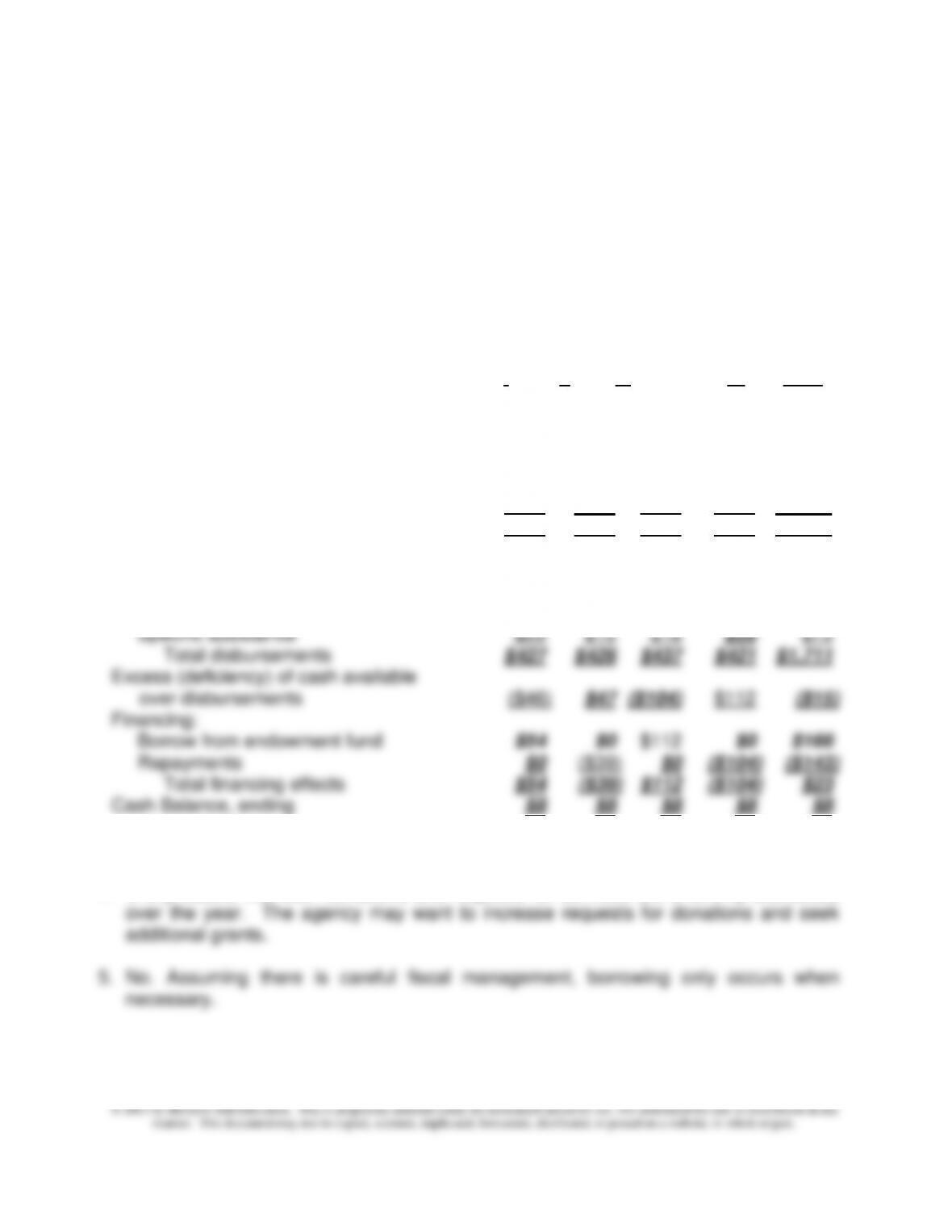

10-36 Cash Budgeting: Not-for-Profit Context (30-45 minutes)

1. “Endowment fund:” a gift (contribution) whose principal must be maintained but whose

income may be expended. (You might use the example of an “endowed professorship”

as an example.)

2.

Cash Budget for Tri-County Social Service Agency

2013

(in thousands)

Quarters

I II III IV Year

Cash Balance, beginning $11 $8 $8 $8 $11

Receipts:

Grants $80 $70 $75 $75 $300

Contracts (evenly during year) $20 $20 $20 $20 $80

Mental Health Income (+5 in Qtrs II, III) $20 $25 $30 $30 $105

Charitable donations $250 $350 $200 $400 $1,200

Total Cash Available $381 $473 $333 $533 $1,696

Less: Disbursements:

Salaries and Benefits $335 $342 $342 $346 $1,365

Office expenses $70 $65 $71 $50 $256

Equipment purchases & maintenance $2 $4 $6 $5 $17

3. $23,000.

4. It is probable that both donations and requests for services are unevenly distributed

Chapter 10 – Strategy and the Master Budget

10–25

10-37 Budgeting: Not–for–Profit Sector (20–30 minutes)

1. Stewardship is defined by Merriam-Webster Online Dictionary as “the conducting,

supervising, or managing of something; especially: the careful and responsible

management of something entrusted to one’s care.”

The Socially Responsible Investment Guidelines cited states: “Although it is a

moral and legal fiduciary responsibility of the trustees to ensure an adequate return

on investment for the support of the work of the church, their stewardship

embraces broader moral concerns.” Also, the principles of stewardship lists two

fundamental and interdependent principles: “The Conference should exercise

responsible financial stewardship over its economic resources.” and “The

Conference should exercise ethical and social stewardship in its investment

policy.”

The latter states: “Socially responsible investment involves investment strategies

based on Catholic moral principles. These strategies are based on the moral

traditional Catholic moral teaching, and employing traditional principles on

cooperation and toleration, as well as the duty to avoid scandal, the Conference

can reflect moral and social teaching in investments.”

2. “These two major principles work together to encourage the Conference to identify

investment opportunities that meet both our financial needs and our social criteria.

3. No. (Reasons should vary.)

Chapter 10 – Strategy and the Master Budget

10–26

10–38 Service Firm Budget (60-75 minutes)

1.

Total hours for the budgeted activities:

Hourly

Budgeted Charge

Revenue Rate Required

(Given) (Given) Hours

Business returns $1,000,000 $250 4,000

Complex individual returns $1,200,000 $100 12,000

Simple individual returns $1,640,000 $50 32,800

Professional staff requirements for the budgeted revenue:

Senior

Total Hours Partner Manager

Consultant _Consultant_

Required Each Total Each Total Each

Total Each Total

Business returns 4,000 0.30 1,200 0.20 800 0.50 2,000 0.00

Complex individual returns 12,000 0.05 600 0.15 1,800 0.40 4,800 0.40

Simple individual returns 32,800 0.00 0 0.00 0 0.20 6,560 0.80

Total Hours 48,800 1,800 2,600 13,360

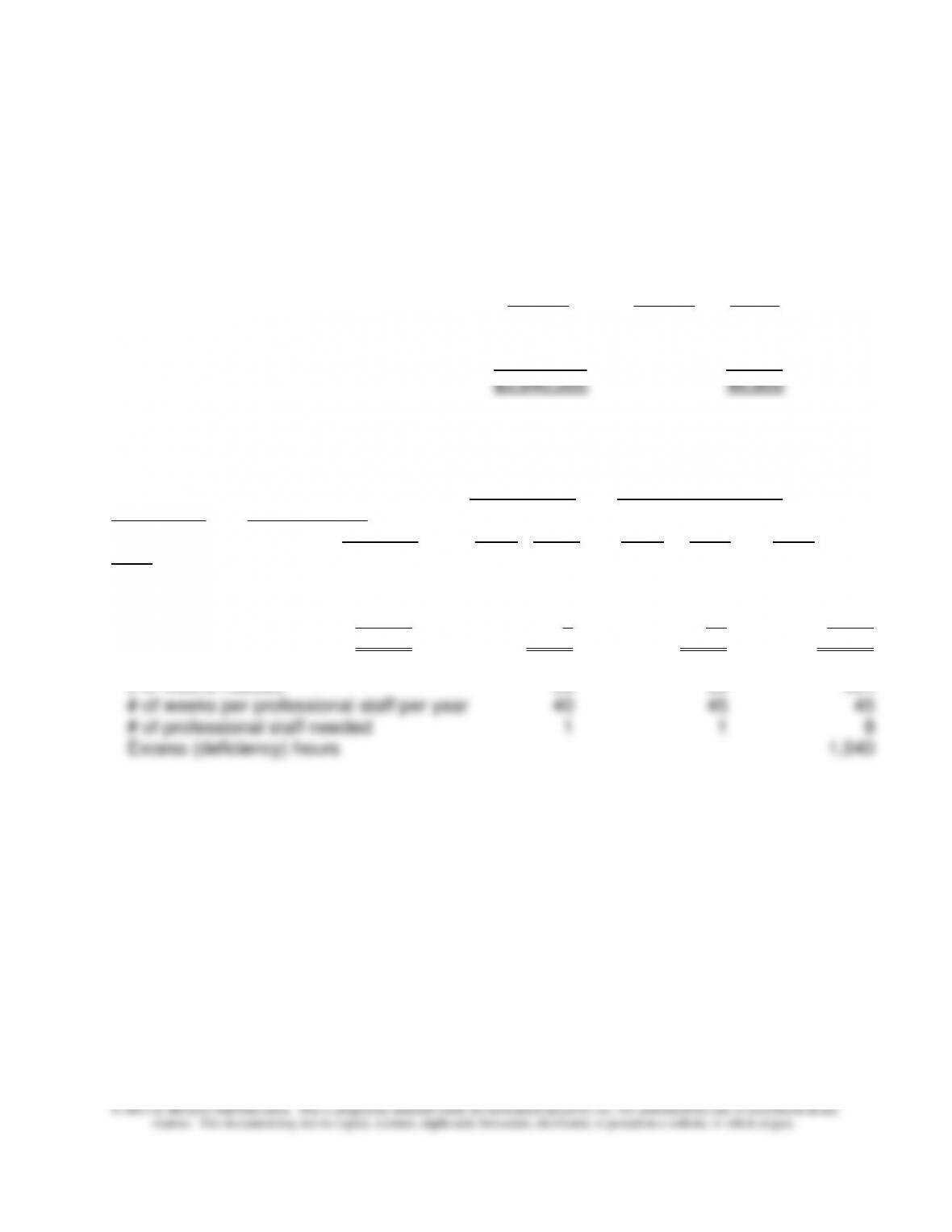

Hours per week 50 45 40

# of weeks needed 36 58 334

Note: Because Consultants can be hired on a part-time basis, we round the calculation

DOWN for this class of labor. The other three labor classes are given (i.e., do not have

to be planned for based on data in the problem).

Since, according to the present staffing plan and anticipated workload needs,

there is an excess of senior consultant hours, the budgeted cost for overtime

hours worked by senior consultants would be $0.

10–27

10–38 (Continued)

2. Number of full-time consultants needed for the year:

No. of consultant-weeks needed for the yr = 776 (from solution to

requirement #1, above)

No. of weeks/full-time consultant/yr = 48 (from solution to

requirement #1, above)

No. of full-time consultants needed = 16 (776 ÷ 48, rounded

down)

3. The manager’s total compensation, assuming that the revenues from preparing tax

returns remains the same:

Consultant’s pay:

Earning per year =

$60,000

Hrs. worked/year =

1,920

Hourly pay rate =

$31.25

No. of PT hours, consultants =

320

Annual Salaries:

Per partner = $250,000

Per manager = $90,000

Chapter 10 – Strategy and the Master Budget

10–28

10–38 (Continued-2)

AccuTax, Inc.

Budgeted Operating Income

For the Year ended August 31, 2013

Revenue $3,840,000

Payroll expenses:

Partner $250,000

Manager 90,000

Senior consultants—base pay 720,000

Senior consultants—pay for overtime hours 0

Consultants:

Full-time $960,000

Total compensation for the manager:

Salary (given) $90,000

1. Right click anywhere in the worksheet area below.

2. Select “Worksheet Object,” then “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode.

Refer to AccuTax, Inc. in the chapter. One of the partners is plann

remaining partner, plans to add a manager at an annual salary of $

45 hours per week for 45 weeks per year. She plans to change th

Exercise 10-38: Budgeting for a Service Firm

Background

Chapter 10 – Strategy and the Master Budget

10–29

10-39 Budgetary Slack and Zero-Based Budgeting (ZBB) (30 minutes)

1. Budgetary slack is a planned difference between budgeted revenue and expected

revenue, and/or budgeted expenditures and expected expenditures. Budgetary

slack describes the tendency of managers to under-estimate revenues and over-

estimate expenditures during the budgetary process in order to build in

2. a. From the point of view of the business unit manager, budgetary slack provides:

▪ performance that will “look better” in the eyes of their superiors

However, the use of budgetary slack limits the objective evaluation of a

business unit and, therefore, limits the objective evaluation of the performance

of the unit manager. It also becomes more difficult for the business unit

manager to evaluate the performance of subordinates and to use the budget as

a control mechanism over subordinate performance.

b. From the perspective of corporate management, the use of budgetary slack

increases the probability that budgets will be achieved. This increased

probability facilitates the overall corporate budgeting process. Corporate

operating activities.

3. a. Zero-based budgeting (ZBB) is a budgeting technique that evaluates all

proposed operating and administrative expenditures as though they were being

initiated for the first time. Each manager must evaluate the proposed

10–30

10-39 (Continued)

b. Atlantis Laboratories could benefit from ZBB as each of the business unit

managers would be required to identify and justify all proposed expenditures for

the benefits of ZBB outweigh the associated costs.