10–44

Reading 10-3: “How Challenging Should Profit Budget Targets Be?

This article argues for using “highly achievable” budget targets, and explains six key advantages for

doing so, including the favorable effect on a manager’s commitment and confidence. The article also

explains some of the risks of using highly achievable budget targets. The concept of risk is illustrated

with probability distributions, with a relatively low-risk environment having a probability distribution

with lower variance.

Discussion Questions:

1. Explain each of the six advantages of highly achievable budget targets mentioned in the article.

Can you think of any in addition?

The article gives the following six advantages:

a. managers: commitment to achieve the budgeted target is increased

Potential additional advantages include:

g. the harmful decision making effects of risk aversion are reduced (as explained in Chapters 3

and 18); risk aversion in connection with incentive reward systems can cause managers to

performance

2. What are the risks of highly achievable budget targets mentioned in the article? Can you think

of any in addition?

a. managers may not be challenged to perform at their maximum potential, if there are not

10–45

Reading 10-4: A Closer Look at Rolling Budgets

Traditional budgets cover a fixed period of time, e.g., a one-year time frame. For this reason, these budgets

are sometimes referred to as “static” in nature. By contrast, some commentators suggest that some of the

negative consequences of this choice can be overcome with the use of rolling (continuous) budgets. This

article deals with issues related to the successful implementation of rolling budgets.

Discussion Questions:

1. What is the primary management-related issue addressed in this article?

As noted at the start of the article, more and more companies are using continuous or rolling budgets as an

integral part of the organization’s overall planning process. Such budgets maintain a constant (e.g., one–

year) planning horizon: as each period (e.g., month) elapses, a new month is added to the budget. The

training, reexamination of incentive and bonus systems, and so forth.

2. What is the primary point of the “practical example” (“Static Budget versus Flexible Budgets”)

offered by the authors?

The example deals with the general issue of incentive effects, which constitute one primary consideration

in the design of an effective management accounting and control system. The case at hand involved a

salesperson whose initial sales goal was rather easily achievable. As such, this individual typically met

authors is that this issue is fundamentally a management (or control system design) issue, not a software

or technology issue.

10–46

Reading 10-5: Budgeting: Perspectives from the Real World

This article survey evidence from senior accounting and finance managers regarding the budgeting

process at for-profit companies, including the usefulness and perceived value of the process, user

satisfaction with this process, and the impediments and challenges to budgeting. Respondents included

815 members of the Institute of Management Accountants (IMA). The study is a follow-up to a recent

study on budgeting published (2007) by Libby and Lindsay.

Discussion Questions:

1. What are the general accounting-related questions addressed by the authors of this paper?

The survey research project of these authors was designed to collect perceptions of accountants regarding

the budgeting process. Specifically, they were interested in obtaining information regarding the

mechanics of budget-preparation process (i.e., how they were prepared and how they were used for both

employed today.

2. What were the primary survey findings regarding the budgeting process used currently in the

U.S.?

The majority of survey respondents indicated that a negotiated process (a combination of “top down” and

“bottom up”) characterized the budget-preparation process at their respective organizations. Further, 85%

of respondents stated that this process was the same throughout the entire company. These results are

roughly consistent across the two groups of respondents, corporate and segment.

In terms of planning, 69.5% of respondents indicated that the primary planning tool continues to be the

(primarily customer satisfaction and market share). Moreover, 78% of respondents reported that

managerial compensation plans, including incentive compensation formulas, incorporate achievement of

specified budget objectives for financial performance measures, while 62.7% reported the same for

nonfinancial measures.

3. What did the authors find regarding the perceived value of the budgeting process (from the

standpoint of survey respondents)?

The survey administered by the researchers asked respondents for their opinions regarding the usefulness

of budgeting systems in relation to specific business objectives: strategic planning, resource/operational

10–47

planning, operational control, communication, coordination/teamwork across subunits, coordination/

teamwork across functional areas, motivation, and incentive rewards determination.

As noted in Table 1, Panel A of the article, the majority of respondents believe that the budget is either

“useful” or “very useful” as it relates to the list of business objectives. In a traditional management

accounting setting, the budget was considered to be important for planning and control purposes only.

The fact that these preparers indicated that it is also useful for other functions such as strategic planning,

at all useful”: coordination across subunits (21.4%) and functional areas (19.1%), motivation (14.1%),

and incentive rewards determination (11.8%).

The perceived usefulness of the budgeting process does not vary much based on whether respondents are

at the corporate or segment level.

4. What were the primary findings of this study as regards the level of satisfaction with the

budgeting process?

Respondents to the study (who were all accounting/finance personnel) also were asked to denote their

level of satisfaction with their organization’s budgeting system as it relates to a specified list of

management objectives. Satisfaction ratings for the full respondent sample are presented in Table 2,

Table 2, Panel B, shows that segment-level respondents are relatively more satisfied with the budgeting

process than are corporate-level respondents, with one exception: Corporate respondents are more

satisfied with the budget as it relates to resource and operational planning. The difference for this

attribute, however, does not appear to be substantial.

In response to the question “Increasingly, the accounting/ finance function is being challenged to provide

value-added services to management. How would you rate your budgetary process in terms of adding

value to your organization?” Forty percent of respondents feel that the budgeting process meets this

overall goal. At the same time, approximately 23% of respondents to the authors’ survey believe that the

budgeting process adds relatively little value to the organization. This result is being driven more by the

segment accountants—29% of them held this view.

The researchers also posed this question to respondents: “What impediments/challenges exist that affect

the ability of an organization’s budgetary process to add value to the firm?” Responses lend support to

10–48

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

5. As indicated in Chapter 10 of the text, there are potential negative behavioral consequences

associated with the budgeting process. What did respondents in this study say as regards this

issue?

Respondents to the survey believe that budgets do not:

❒ Block employee initiatives,

Compared to corporate-level respondents, more segment-level managers either agreed or strongly agreed

that the budget:

❒ Blocks employee initiatives,

❒ Pressures managers to make decisions with a short-term focus,

Figure 2 in the article presents perceived positive behavioral effects of budgeting. There was general

agreement among respondents that budgets can be used to support continuous improvement, to provide

managers with information they need to respond to change, to motivate information and knowledge

sharing across subunits, and to encourage appropriate risk taking.

10–49

6. What future research is suggested on the basis of this study?

The authors offer the following suggestions for extending their research project:

a) Survey operational managers (i.e., “users”) to determine the extent to which their views are consistent

with the views of finance/accounting personnel.

b) Examine the statistical relationship between budgeting practices and financial performance variables

(e.g., stock price or stock returns). Such a study could provide evidence as to the market’s perception of

improvement.

e) Finally, as noted in this article (and Chapter 10 of the text) there are some firms that have moved away

from the budgeting process as it is commonly construed. A study to determine conditions under which

such a move is tenable would contribute greatly to the profession’s knowledge of the budgeting process.

10–50

Reading 10-6: Turning Budgeting Pain into Budgeting Gain

The author of this article is a career CFO and presents in the article survey evidence regarding the

budgeting process. The survey was conducted jointly by Centgage and the Institute of Management &

Administration (IOMA).

Discussion Questions:

1. On page 47 of the article, the author notes that “the budgeting process at most companies is

broken.” What evidence does the author offer in support of this statement?

The author relies principally on survey results obtained from a sample of CFOs. In general, the referenced

survey indicated lack of confidence in budget forecasts as a significant obstacle for budgeting systems;

(3) Tools—that is, inadequate technology, particularly general-purposes software tools such as Excel.

(The instructor can contrast this with dedicated software packages.)

2. What potentially positive roles does the author envision for properly constructed budgets?

Basically, the list of benefits proposed by the author of the article parallels the discussion in the text. That

is, the benefits of budgeting typically fall into one of the following two general categories: planning and

control. The following list of specific benefits is presented in the article:

a) cash-flow-management tool (particularly for smaller companies) (i.e., planning)

f) crystal ball—“what–if” scenarios, etc. (i.e., planning)

3. What recommendations does the author offer for improving the budgeting process?

The author of this article offers a seven-step process for improving budgeting. Note: this would appear to be a rather

general process (set of steps) that could be applied to other organizational changes. Of particular importance are

behavioral considerations associated with successful changes/process improvements.

1) Critically evaluate the existing budgeting process

7) Follow through

10–51

Reading 10-7: Planning for Uncertainty—Rolling Forecasts

Corporate financial planning expert Steve Player highlights how CPA financial executives can use nimble

rolling forecasts to replace annual budgets.

Discussion Questions

1. According to the article, what are some of the most severe criticisms of conventional budgeting

practices, such as those associated with the master budgeting process illustrated in Chapter 10 of

the text?

• If compensation/incentive pay is linked to budgetary performance, it provides incentives for

managers to “low–ball” budgeted performance (i.e., to negotiate the lowest possible target). The

author maintains that this practice, at a minimum, provides disincentives for organizational growth.

costs too much, and is out of date often before it is printed.”

2. What is the essence of “rolling forecasts” and according to proponents of using rolling forecasts

how do they improve upon traditional budgeting practice?

Traditional budgets are based on a fixed time period (e.g., one year), which means that as the year

progresses, the planning horizon decreases. Some assert that this very process leads to a perspective and

actions on the part of employees/managers that are not consistent with the long-term interests of the

organization.

Rolling forecasts provide a fixed planning horizon (e.g., five quarters or six quarters): as one time

component (e.g., a quarter) elapses, a new quarter is added to the planning document. In this sense, the

scenarios/combinations. According to this matrix, “if it’s highly critical and highly volatile, you look at

it (i.e., regenerate a forecast) very frequently…if (an item) is low on both, you can drop back to an

infrequent update only as necessary.” A summary of how this planning matrix was implemented by

Southwest Airlines is given in Exhibit 2 of the article.

3. According to the article, what are some common mistakes associated with forecasting systems?

For those familiar with the Beyond Budgeting Roundtable, these alleged errors are well-known. In the

space below, we repeat the major errors, as listed in the present article:

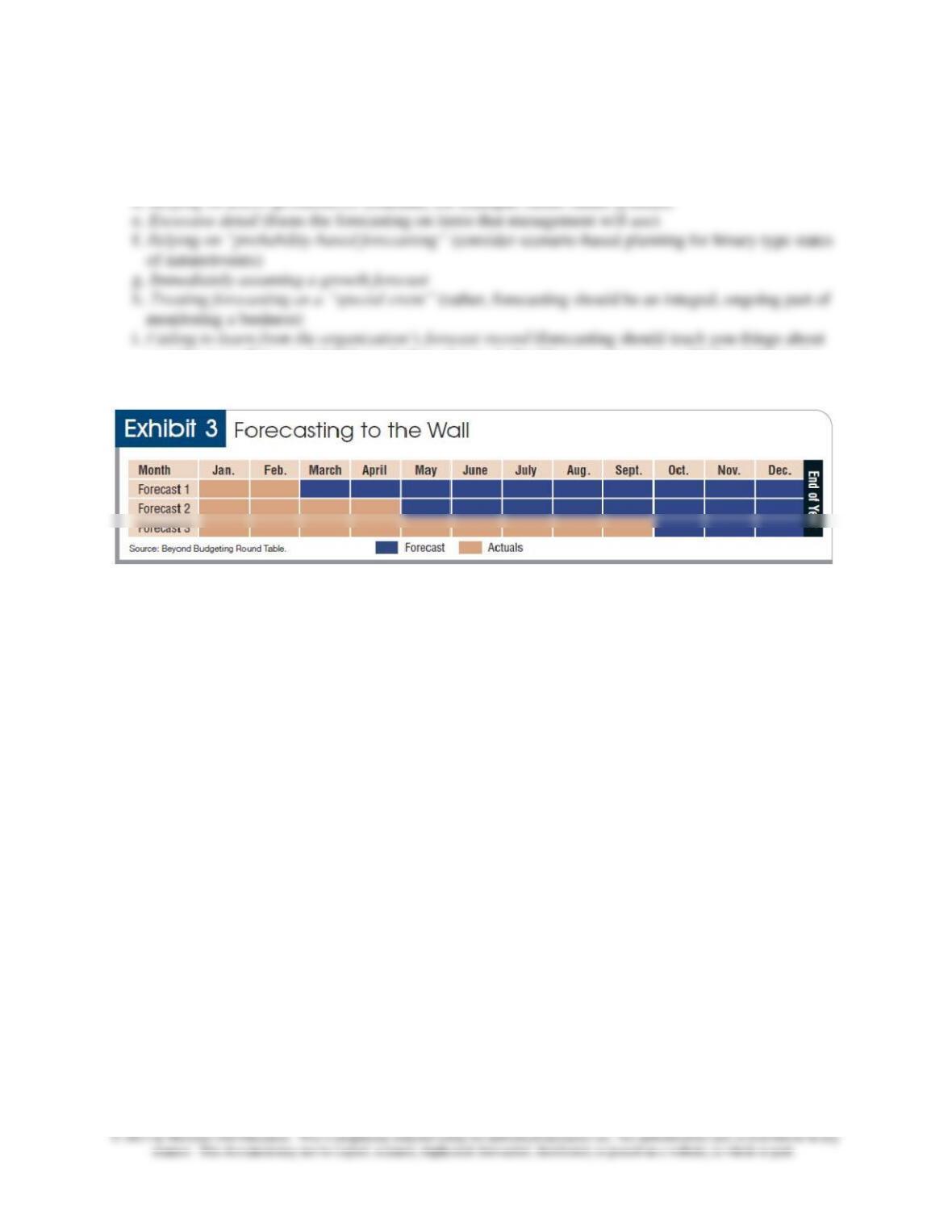

a. Forecasting to the wall (diminishing planning horizon, as the year unfolds), as in Exhibit 3 (see

below)

10–52

b. Confusing forecasts with targets (with a consequent negative effect on innovation, risk

management, etc.)

c. Demanding forecast accuracy (with reduced incentive to grow or achieve bench-marked

performance)

d. Relying on Excel spreadsheets (consider, for example, cloud-based systems)

your business that you didn’t know before; that is, it should represent a value-added activity to the

organization, on a cost-benefit basis)

10–53

Reading 10-8: Scenario Planning—Navigating Through Today’s Uncertain

World

Scenario planning is a way of understanding forces such as demographics, globalization, technological

change and environmental sustainability that will shape the future, and harnessing them to plan for risk.

This article, based on an AICPA-sponsored Management Accounting Guideline, introduces the types of

scenarios you should consider and provides tips for getting started with scenario planning.

Discussion Questions

1. How does this article relate to the topic of budgeting (as presented, for example, in Chapter 10 of

the text)?

By going through the master budgeting process, it should be obvious to students that the end product

of the master budgeting process—a set of pro-forma financial statements—are a function of many

assumptions made by those constructing the budgets. Complicating the budget-preparation process is

uncertainties associated with volatile markets.

2. What is meant by the term “scenario planning”?

According to the article, “scenario planning” is a tool that can be used to help deal with the

uncertainties associated with volatile markets and unpredictable events. In essence, “planning” is

3. Provide an overview of the basic approach to scenario planning (as illustrated, for example, in

Exhibit 1 of the article).

As noted in the article, scenario planning essentially consists of answering three questions: What could

happen? What would be the impact on our strategies, plans, and budgets? And, how should our

organization respond?

One process that could be used to develop scenario plans is illustrated in Exhibit 1 of the article. The

10–54

As noted in the article, there are four broad types of scenarios that the planning team for the

organization should be considering: (1) Social, (2) Economic, (3) Political, and (4) Technological.

The above processes can be illustrated via a discussion of the ElectriclQ, a software company that

different scenarios developed by the company, across two dimensions (public opinion vs. public

policy) are presented in Exhibit 4. Finally, the link between scenario development (Exhibit 4) and

strategy is illustrated in Exhibit 5.

4. Provide a description of the managerial value of the type of information presented in Exhibit 5 of

the article.

Rephrased, the purpose of this question is to get students to think about how scenario planning can be

markets and conditions.

10–55

Reading 10-9: Budgeting for International Operations: Impact on and

Integration with Strategic Planning

Multinational companies contend with an array of external factors, internal considerations, and other

forces that influence budget policies, composition, and control and—on a more general level—their

strategic planning. Budgeting in a global business environment calls for an enhanced level of coordination

and communication because of the variety of powerful components that impact organizational

performance. This article examines how international issues influence the budgeting process of

multinational companies headquartered in the United States that control foreign affiliates and describes

how the output of the budgeting effort impacts and integrates strategic planning.

Discussion Questions

1. According to this article, what are the three major external factors that affect, that is, complicate

the process of preparing, budgets for multinational companies?

As indicated in the introductory paragraph to the article (p. 1), the following three major (external)

factors affect the development of budgets for multinational companies are:

The authors state (p. 1) that changes in currency exchange rates have the most direct effect on the

budgeting process for multinational companies.

2. The authors of this article present 19 examples of specific planning issues faced by multinational

companies. Provide an overview/short summary of one (1) example from each of the following

three (3) categories in terms of budgetary complexities:

a. Foreign Currency Exchange Rates (i.e., Translation Exposure, Transaction Exposure,

Economic Exposure, Interest Rates, or Inflation)

b. Effects on Specific Budgets (i.e., sales budgets, expense budgets, capital expenditures budgets,

or cash budgeting)

c. Other (Miscellaneous) Considerations (i.e., Transfer Pricing, Inventory Policy Decisions,

Timing Issues, Budget Control)

Details are provided in the article. One possible strategy is to ask students to work in teams and to

assign to student teams specific examples, which the teams would then present in class to the rest of the

presented by the presenting team.