Chapter 10 – Strategy and the Master Budget

10-1

Chapter 10

Strategy and the Master Budget

Teaching Notes for Cases

10-1: Emerson Electric Company

Background

• Emerson is an $8 billion company.

• Its successful strategy is efficient, quality, and low cost production. R&D does not get a great deal

of attention from top management.

Planning Process

• Top management sets sales growth and return on total capital targets for the divisions.

• Each fiscal year, from November to July, the CEO and several corporate officers meet with the

management of each division at a one or two day division planning conference:

▪ Prior to its division planning conference, the division president submits four standard exhibits

to top management:

1. Value measurement chart

2. Sales gap chart

3. Sales gap line chart

4. 5-back-by-5-forward P&L

• The division president and appropriate division staff then meet with top management to present a

detailed forecast for the coming year based on the result from the division planning conference and

conduct a financial review of the current year’s actual performance versus forecast:

▪ Contingency plans for several lower levels of activity also developed to protect profitability

at lower sales levels.

▪ However, changes to the division’s forecast are not likely unless significant changes occurred

in the environment or in the underlying assumptions. Changes in the forecast must be

approved by top management.

• In August, the information generated for and during the division planning conferences and fiscal

reviews is consolidated and reviewed at corporate headquarters by top management.

• In September, top management presents the corporate and division forecasts for the next year and

the strategic plan for the next five years to a conference attended by top management and top

officers of each division.

Reporting

• Each month each division president submits to Office of the Chief Executive the President’s

Operating Reporting (POR).

• Corporate top management meets quarterly with each division president and the division’s chief

Chapter 10 – Strategy and the Master Budget

10-2

financial officer to review the most recent POR and monitor overall division performance.

Compensation—Base salary and “extra” salary:

• An extra salary amount is established at the beginning of the year.

• The executive of a division earns the extra salary if the division hits targeted performance.

▪ The targeted performance consists of primarily measurable objectives such as sales,

profits, and return on capital.

▪ The multiplier ranges from 0.35 to 2.0.

▪ Other factors considered include inventory turnover, international sales, new product

introductions, and an accounts receivable factor.

• Stock options and a five-year performance share plan also available to top executives.

Question 1: Evaluate Chief Executive Officer Knight’s strategy for the Emerson Electric Company.

In view of the strategy, evaluate the planning and control system described in the case. What are its

strong and weak points?

• Planning at Emerson is top-down with CEO Knight actively involved from the start of the

process.

• The first four exhibits capture the essence of the planning system.

▪ The value measurement chart contains comparisons in five-year increments for

investments, operating profit, return on invested capital, sales, operating capital turnover,

capital charge, and economic profit.

▪ In addition to NOPAT, Emerson uses a measure of “economic profit”.

▪ The chart reflects the sales and return on total capital targets set by top management.

• The division sales targets that are set by top management are optimistic. The purpose of the sales

gap chart and the line chart is to identify the sources of five year sales growth and to highlight the

sales shortfall. Exhibit 2 illustrates a 15% target growth rate for sales which results in shortfalls

for each year. Of course, division presidents must provide action plans for closing the gap.

• The comparative profit and loss statements for eleven years in Exhibit 4 seem like overkill. One

advantage is that they show trend. Included at the bottom is the return on total capital.

• The strength of the Emerson process is that it gets commitment from the division presidents.

Certainly, they participate in the planning process to a great degree. There is no reliance on

planning staff. Division presidents are given full responsibility and accompanying authority.

• The linkage between the plan and the detailed forecast (the one-year operating budget) is

extremely tight. Top management must approve any changes from the approved plans. In

addition, divisions are expected to prepare contingency plans at lower level of sales. Top

management may request that a division switch to contingency plans if forecasted performance

falters.

• The key document to the control process is the president’s operating report (POR). This represents

an unusual approach to monitoring performance. There are only six items of data on this report:

Chapter 10 – Strategy and the Master Budget

10-3

intercompany sales, sales, gross profit, SG&A expenses, operating profit, and earnings before

interest and taxes. Monthly reporting during a quarter can lead to a change in the forecast data for

that quarter. The CEO and senior managers review performance.

• Divisions are expected to meet the annual forecast performance.

Advantages include heavy involvement of division presidents in the planning process and the cost-

reduction programs:

• There seems to be a lot of discussion and interaction between division managers and top

• Both the short-range and long-range compensation systems reinforce the planning and control

system.

Disadvantages include:

• The possibility of overly optimistic top-down directives on sales and return on investment targets.

• There is no explicit data on market share or other non-financial measures of performance.

• The cost of capital may not be adjusted for risk when applied to different divisions.

Question 2: What role should the eight business segment managers have in Emerson’s planning and

control system?

When questioned on the role of the new business segment managers, a top Emerson official remarked that

it was a good observation. Evidently the planning system does not explicitly involve the business segment

managers. What might their role be? Emerson consists of forty divisions organized into eight business

segments. This is an average of five divisions per business segment. The case says the reasons for this

Chapter 10 – Strategy and the Master Budget

10-4

Case 10-2: Letsgo Travel Trailers

The Letsgo Travel Trailers case is designed to prompt student discussion of the interactions between

various functional areas of the company, for example, the impact of the sales projection and desired

inventory levels on production. The case also allows the instructor to discuss both short-term and long-

term strategy. In the short term, Letsgo’s major problems occur because of an uneven sales and

production schedule, which may lead to product-quality problems. The use of alternative approaches to

production planning and cash management is also introduced in the case.

Letsgo manufactures travel trailers used primarily by young families and retirees interested in a light,

low-cost trailer that can easily be pulled by a mid-sized family car. The travel trailer industry is expected

to experience high growth rates (in the case, at least through 2020) due primarily to the aging “baby–

boomer” population. Yet the environment is changing, and many factors will affect Letsgo Travel

Trailer’s projected sales growth rate. Changes in the aluminum industry and increasing demand for light–

weight construction materials will affect Letsgo’s ability to access a critical raw material. Demographic

trends and changes in the demand for and production of aluminum will have a profound effect on the

future success or failure of Letsgo.

Budgeting, approached as a team effort, can be a powerful coordinating tool. Effective cooperation

among functional areas (i.e., sales, production, purchasing, and finance) would allow Letsgo to negotiate

lucrative prime vendor contracts and implement JIT. Unfortunately, Letsgo currently approaches

budgeting as a mathematical exercise to be performed by accounting, based on narrowly viewed sales

projections. Furthermore, Newman, the company president, does the sales projections with little or no

mention of outside resources or input from Letsgo’s functional managers and line employees.

In the longer term, Letsgo will inevitably face increased outside competition as the desirability of

marketing to the growing population of baby-boomer retirees increases. The case allows discussion of

sales projections and the need to identify both the underlying demographic factors that may affect future

sales and the more finite market forces, such as barriers to entry and lower-cost manufacturing threats.

Suggested approaches to the case questions follow. The instructor need not take the suggested

approach explicitly for all questions, however, since the case allows numerous opportunities for the

instructor to guide the class discussion into more or less depth on many of the case questions. Please refer

to the case addendum in which we provide a recent article from The Wall Street Journal. This article can

be used to update some of the information contained in the case.

Suggested Approaches to Case Questions

Question 1: Discuss the validity and reasonableness of Letsgo’s sales projections

The source of Letsgo’s sales projections is not revealed in the case. The projections may be too

optimistic. Actual sales increased 8.1% from 1992 to 1993, 7.5% from 1993 to 1994, 11.4% from 1994 to

1995, 10.2% from 1995 to 1996, and 18.8% from 1996 to 1997. The projected increase of 20% from 1997

Letsgo’s sales are heavily seasonal, with more than 40% of the sales taking place in just three months

(February, March, and April). It may appear odd to students that people are buying travel trailers in

February and March, until students become aware that the company sells its trailers to retail outlets, such

as L.L. Bean, which begins preparing for the summer season early in the spring.

Does Letsgo plan to concentrate exclusively on the retiree market? The company president appears to

consider the future to be retirees. It is unclear, however, that the company has adequately utilized market

research. Do market data support Newman’s beliefs? Further, the company’s strategy needs to be

Chapter 10 – Strategy and the Master Budget

clarified. Budgeting provides the communications tool to implement strategy. The production budget and

market.

Question 2: Prepare production, purchasing, and cash budgets for Letsgo for the fist six months of

1998. Discuss the advantages and disadvantages of the budgets you prepared. Who in the company

does the budget help and whom, potentially, does it hurt? Does the budget help or hurt the sales

department? What about production and finance? How are the various functional areas affected,

and why?

Note to Instructor: An Excel spreadsheet solution file is embedded below. You can open the spreadsheet

object that follows by doing the following:

1. Right click anywhere in the worksheet area.

2. Select “worksheet object” and then select “Open.” To return to the Word document,

select “File” and then “Close and return to…” while you are in the spreadsheet mode. The

screen should then return you to the Word document

3. You can also use this method to copy a portion or all of the embedded spreadsheet into

an Excel spreadsheet for your own use.

Production Budget: The production schedule appears to be dictated by sales and marketing. The

generous inventory levels are created by the policy of having on hand at the end of each month finished

good (completed trailers) equal to 300 trailers plus 20% of the next month’s projected sales in units. The

“cost” of this policy is in warehousing. Finance is affected by the need to direct significant dollars to

Case 10-2: Letsgo Travel Trailers

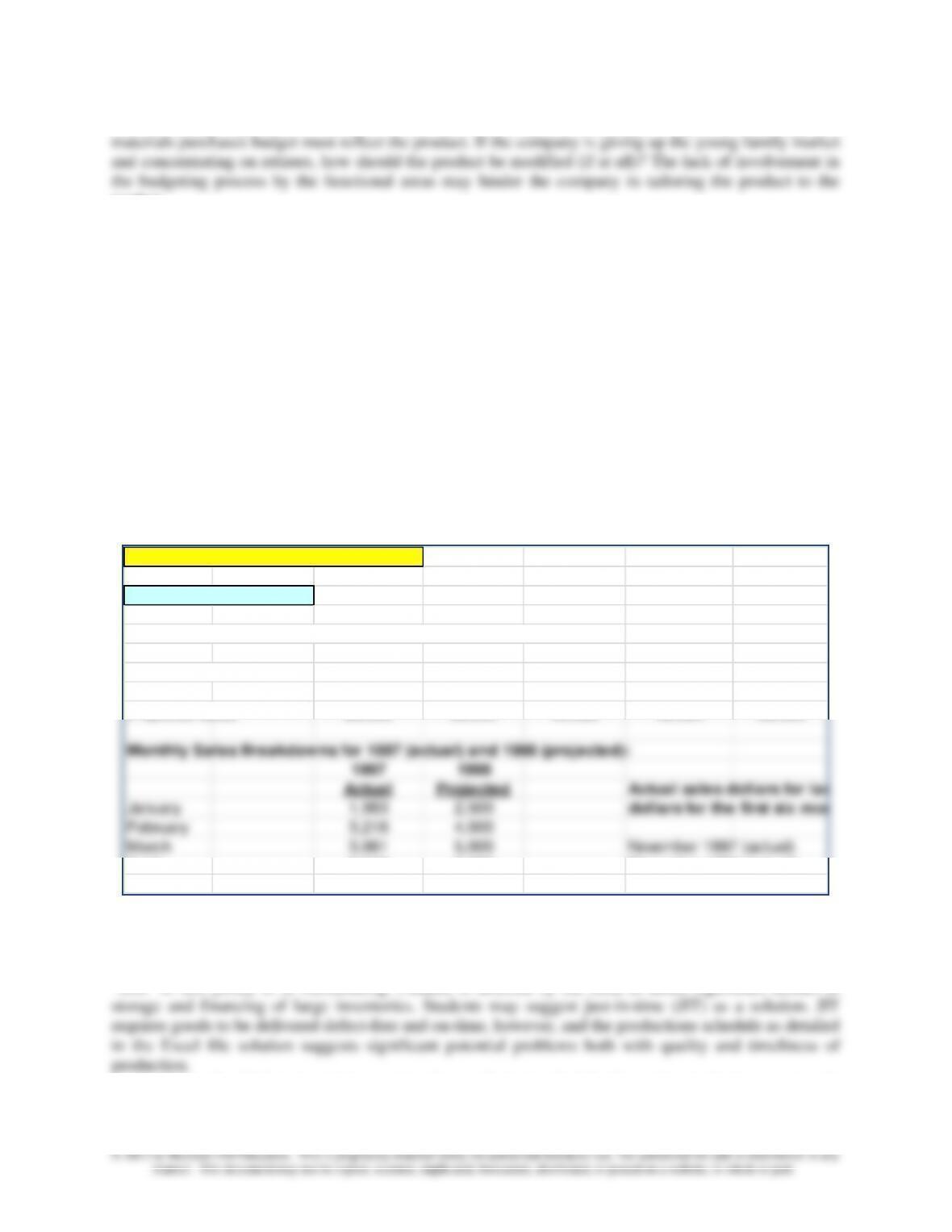

Data Input Area

Exhibit 1: Actual and Projected Sales in Number of Trailers

1992 1993 1994 1995 1996

Actual sales 13,765 14,880 15,991 17,809 19,634

1998 1999 2000 2001 2002

Projected sales 28,000 33,600 40,320 48,384 58,060

Monthly Sales Breakdowns for 1997 (actual) and 1998 (projected):

1997 1998

Actual Projected Actual sales dollars for las

January 1,983 2,500 dollars for the first six mon

February 3,218 4,000

March 3,981 5,000 November 1997 (actual)

April 3,240 3,000 December 1997 (actual)

May 1,755 2,000 January 1998 (budgeted)

Chapter 10 – Strategy and the Master Budget

10-6

meet production highs, manufacturing will almost certainly be forced to hire part-time workers or work

extensive overtime, both of which heighten the potential for quality problems and production delays.

would indicate a figure of only 800 (i.e., 300 + [2,500 January sales × 0.20]).

The case notes that the company does not keep track of work–in-process (WIP) inventories. This

appears to be a potentially serious flaw in managerial control. Lack of control over WIP violates

management’s fiduciary responsibility to protect and control shareholder assets. Accounting for inventory

is not, however, the only way to control WIP. Letsgo may be tracking production directly by monitoring

throughput time or output rate.

Is a six-month budget adequate for planning and control? Most companies plan at least 12 months

ahead, a fact that can prompt a discussion regarding “continuous budgeting.” The availability of sales

forecasts five years in the future may also prompt discussion of three– to five-year planning budgets and

the role of budgets in achieving longer-term strategic targets.

Materials Purchases Budget: The uneven production schedule is reflected in the uneven sheet

aluminum purchasing schedule. Preparation of the material purchases budget allows students to begin

recognizing the broader need for cross-functional coordination. Purchasing as well as production and

finance are affected by the product’s seasonality.

adhere to strict payment schedules to maintain favorable relations with prime suppliers.

Cash Budgets: Letsgo will be unable to repay the anticipated $800,000 loan in 90 days (January 1—

March 31). Further, the company will need to borrow an additional $1,411,000 to finance operations

through May 31st.

Letsgo appears to plan an increase in the selling price of its trailer in May 1998, from $1,000 per

trailer to $1,100 per trailer. Students should question the lack of clarity as to selling price. Of potentially

greater importance, however, is the timing and competitiveness of such an increase. By increasing the

selling price of the trailer in April just prior to the slowest selling time of the year (June, July, and

reinforcing Letsgo’s apparent lack of a formalized strategy.

The budgeted expenses for equipment rental, equipment purchases, depreciation, and selling/

administrative costs raise questions. Why, for example, do equipment rentals vary only in the month of

April? Students expect either of two scenarios. Either the equipment rental should vary with production (a

very reasonable but difficult production scenario from a practical aspect), or the amount should remain

flat over the entire six-month period. In fact, what is happening is the replacement of rented with owned

equipment. Newman plans to replace all rented equipment with owned equipment over the next three

years. This replacement of rented with owned equipment is also responsible for the increase in

depreciation expense in April. The company’s policy is to initiate depreciation expense on new equipment

following the quarter in which the equipment was purchased. Students should recognize depreciation as a

Chapter 10 – Strategy and the Master Budget

10-7

non-cash expense.

The replacement of rented with owned equipment, which apparently is being financed either through

operations or with short-term financing, can initiate a discussion of the role of different financing

vehicles. Long-term debt or issuance of capital would, in most instances, be a preferable financing

balance to be maintained, while not necessarily typical, may prompt discussion of the Board’s role and

the responsibilities assumed by its members.

Question 3: Andy Baxter, newly hired by Letsgo from a competitor, suggests preparing the

production budget assuming stable production. Prepare a second and third set of production,

material purchases, and cash budgets with production held constant at 3,000 trailers per month for

the second set of budgets and 3,500 trailers per month for the third set of budgets, using the

following approach for the production budget (the purchasing and cash budget formats remain as

presented above in question (2).

Discuss the advantages and disadvantages of the second and third sets of production, material

purchases, and cash budgets you’ve prepared. Who in the company do these budgets help and

whom, potentially, do they hurt? Do these budgets help or hurt the sales department? What about

production and finance? How are the various functional areas affected, and why?

Production Budget: (NOTE: the solution generated for Question 3 differs from the published

solution by the author of the case, in two respects: (1) treatment of cash outflows for wages (labor)

expense, and (2) treatment of cash outflows for materials purchases (both aluminum and non-aluminum

materials. To generate a solution for Question 3 we made some assumptions, which are clearly identified

in the case itself. These assumptions, however, were not included in the original case.) Alternative

assumptions are possible. This portion of the case, therefore, illustrates the need for assumptions and

sensitivity analysis when evaluating operating policies, such as a production plan (specifically, the plan

for smooth production.

A level production schedule will allow the production department to maintain better quality by hiring

and training a corps of workers. Use of part-time workers and overtime will be minimized. The 3,000

substantial advantages to be gained through JIT, prime vendor, and cash control.

With production level at 3,500 trailers per month, purchasing can attract prime vendors due to the

level demand in aluminum (105,000 square yards per month). However, as reflected in the cash budget,

Letsgo will need to borrow additional funds as compared to the situation illustrated in Question 2. A

number of explicit assumptions were made regarding materials and labor costs and payments in order to

generate a cash budget for Question 3. Students might think of ways to decrease the borrowing needs

associated with a planned production level of 3,500 units per month.

Students should be prompted to see the production problems as a company-wide problem with

dependence on a single seasonal product. The longer-term solution lies either with product diversification

or controlled productions and sales (i.e., limiting the number of trailers available).

Chapter 10 – Strategy and the Master Budget

10-8

The preparation of three separate yet connected sets of production, purchasing, and cash budgets

acquaints the student with the power of budgeting as a planning tool.

Question 4: What should Letsgo use to measure performance for each of the managers in the case?

What bonus system would you suggest that incorporates these measures and also encourages the

managers to work as a team?

Letsgo suffers from a customer-driven sales pattern. Examination of Exhibit 1 in the case reveals

significant swings in sales from month to month. In 1997, for example, sales dropped from a high of

3,981 in March to a low of 793 in July, with the greatest drop (1,485 trailers) occurring between April and

May. This type of demand schedule creates significant problems for production, leading to quality

in turn, negatively affect purchasing, preventing Vicky Draper from implementing JIT. Prime vendors are

reluctant to deal with firms that vary material requirements dramatically, since such fluctuations also

affect their production scheduling.

Letsgo’s difficult, customer-driven production schedule has a negative impact on suppliers, workers,

managers, and customers. Uneven labor demand leads to excessive overtime and inefficient use of

workers, which leads to quality problems. Uneven material demand can also influence quality, as Draper

attempts to fill material order while lowering cost in an effort to earn her bonus.

Recommendations

Letsgo should develop performance measurements with strong quality considerations. While the current

bonus scheme appears to cater to customers, by prompting sales to meet all customer demand, the actual

impact on customers is negative due to quality problems.

Letsgo can best serve customer needs, particularly those of seniors, who value quality, by

implementing performance measures that reward quality. Furthermore, the performance of all managers

should be evaluated in a team atmosphere. For example, an effective bonus scheme would reward the

vice-president of sales and marketing for gains in quality created by a shift to the flat production schedule

suggestion in Question 3. In similar fashion, the production manager should be rewarded, in part, for the

cost savings of JIT, prime vendor contract that can, practically, be obtained only when the production

schedule is consistent.

Chapter 10 – Strategy and the Master Budget

10-9

Case 10-2: Addendum

The instructor might find the following Wall Street Journal article a useful update to the case as originally

written.

Roadside Distraction: The Trouble with RVs

As Sales Soar, Retirees Face Leaks, Breakdowns, Recalls; the Limits of the Lemon Laws

By JENNIFER SARANOW; May 31, 2006; Page D1

Mary Lou and Herb Humphries sold their home in Massachusetts last July to travel the country full time

in a new, nearly $500,000 motor home. But so far, they haven’t gone much farther than the dealership lot.

Since they bought the luxury Beaver Patriot Thunder, made by Monaco Coach Corp., they have faced

problem after problem, including burned-out fuses, mold, misaligned doors, and a broken alternator that

caused a breakdown on the highway last fall. Since buying the motor home last August, the Humphries,

who live in the coach, have split most of their time between the dealership and the manufacturer’s service

facility, both in Florida.

“We’ve lost nine months out of our retirement life because of this motor home,” says Ms. Humphries, who

says the coach has required about 400 repairs (many of those repeats), covered under warranty. “Our

dream has literally turned into a nightmare.”

Sales of recreational vehicles have jumped in recent years, boosted by the large number of baby boomers

reaching retirement age and wanting to take to the road. (Late last month, the movie “RV,” starring Robin

Williams, opened No. 1 at the box office.) According to the Recreation Vehicle Industry Association,

384,400 RVs were shipped to dealers last year, up about 4% from a year earlier and a 27-year high. Motor

homes, which can sell for as much as $400,000 or more, make up about a fifth of the RV market and

towable trailers, which generally cost anywhere from $5,000 to $100,000, about 80%.

But as summer travel season starts, complaints about recreational vehicles are mounting. Some of the

downsides: So-called lemon laws, which guarantee consumers replacement motor vehicles or refunds

after a certain number of problems or days in the shop, vary by state and often don’t apply to RVs.

Consequently, RV owners, stuck awaiting repairs, often have little legal recourse. Gas prices also remain

high.

The RV Consumer Group, a nonprofit group that rates recreational vehicles for safety and handling, says

it gets about 100 complaints a month related to structural deficiencies with RVs, up from about 50

complaints a month a decade ago. The Council of Better Business Bureaus Inc. received 844 complaints

about RV dealers in 2005, repair issues being among the most common, up from the 488 complaints it

received in 2000.

Nationwide law firm Krohn & Moss, which specializes in lemon laws, has received nearly 1,500 inquiries

about problem RVs since it started an online free case review database two years ago, and it has started a

special division devoted to RV lemon cases. The magazine of Escapees Inc., an RV-owner club based in

Livingston, Texas, included its first article on the topic of lemon RVs in its May/June issue.

Chapter 10 – Strategy and the Master Budget

10–10

RVs often have more problems than other vehicles because they are made in much smaller quantities than

cars and without the same sophisticated manufacturing methods. Unlike cars, motor homes are made by

multiple manufacturers. Auto makers typically build the engine and transmission. RV manufacturers then

assemble living quarters, often by hand, increasing the chance for human error. More RVs on the road

also means a greater chance of problems.

According to the National Highway Traffic Safety Administration, there were more than 100 recalls

involving RVs last year, up from 83 in 2000, for defects varying from faulty microwave ovens to

improperly installed furnace exhaust vents. A 2005 survey commissioned by the RV industry found that

64% of motor-home owners brought their RVs in for services beyond a routine visit, most often citing

problems with the interior, appliances or electrical components. A quarter of owners were dissatisfied

with how problems were corrected.

In response, legislators in Michigan, Pennsylvania and Montana have introduced bills that create RV

lemon laws or expand existing lemon laws to include RVs. According to the law firm Kimmel &

Silverman, lemon laws in 17 states and Washington, D.C, don’t cover RVs at all and those in 20 states

cover only their motor-vehicle components. Motor homes are covered in the lemon laws of 13 states —

but often only those under a certain weight.

Manufacturers argue that buyers today unfairly expect RVs to meet the same quality standards as cars

when they should be comparing the coaches to homes. RVs tend to have more problems than cars

“because of the nature of it,” says Richard Coon, president of the Reston, Va.-based Recreation Vehicle

Industry Association, which represents the RV makers and component suppliers. “Put your whole house

on a truck bed and drive it down the street and things start happening,” he says.

While the RV industry has lobbied against including RVs in lemon laws, manufacturers and dealers say

they are working to improve quality and service.

In regard to the Humphries’s problems, a spokesman for Monaco Coach says the company doesn’t

comment on specific cases. But Monaco has instituted an inspection system for each vehicle that comes

off the assembly line. Coachmen Industries Inc. has opened a center in California to service vehicles on

the West Coast so that customers there don’t have to rely on dealers for warranty repair work. Companies

such as Winnebago Industries Inc. and Thor Industries Inc. are focusing on “lean manufacturing”

processes that cut down on how often parts are handled during production, reducing the chance of

damaging them. Thor Industries says many of its brands have put in place electronic warranty processes

to speed up the repair-approval process.

In states where RVs aren’t well covered by lemon laws, consumers who end up with problem motor

homes often have few choices other than to sell the RVs at a loss or postpone trips and make repairs. The

good news is owners often aren’t responsible for paying for repairs during the first few years of

ownership. RVs are generally covered under one- or two-year base warranties and additional ones for

various parts.

Earlier this year, the Recreation Vehicle Dealer Association started a new pilot certification program for

dealer service managers to make them more effective at getting the units serviced correctly the first time.

The association, which has had certification for technicians since the early ’90s in a joint program with the

Recreation Vehicle Industry Association, has also released a guide for parts personnel to help them

increase their expertise.

Chapter 10 – Strategy and the Master Budget

10–11

In Florida, where the lemon law covers only the motor-vehicle components of motor homes, RV makers

are funding a new mediation program operated by an independent third party, in which RV owners and

manufacturers try to reach a settlement before going through the lemon-law arbitration process. During

mediation, owners can bring up issues that go beyond the lemon law, such as problems with leaks in the

living quarters. As of last July, they also can bring them up in arbitration if manufacturers agree (so far,

none have). The Recreation Vehicle Industry Association says it would like the Florida program to be a

model for other states.

Groups such as the Family Motor Coach Association and publications such as Trailer Life Magazine have

intermediary and ombudsman programs that will help RV owners solve problems they may be having

with dealers or manufacturers.

Attorneys say they can defend RV owners using other laws, such as a federal law that provides protection

to buyers of consumer products under warranty, but say they turn away many RV owners because such

cases are harder to win, expensive and can take years. RVs also don’t have many of the protections homes

do, such as state laws requiring owners to disclose problems and pre-purchase inspections.

Chapter 10 – Strategy and the Master Budget

10–12

Sales of motor homes have started to slow in recent months, partly because of high fuel prices. Motor–

home retail sales fell about 21% to 7,328 units in the first two months of this year, compared with the

same period a year ago, as RV buyers delay purchases or opt for towable trailer models.

To attract buyers, manufacturers and dealers are rolling out a host of discounts. This summer Thor

Industries says several of its brands will be offering gas cards to attract buyers. Terry’s RV Center in

Frankfort, Ill., rolled out a loyalty program for customers that allows them to redeem points earned on

service and parts for perks like free RV washes. Lazydays, an RV dealer in Seffner, Fla., where the

Humphries bought their coach, just launched a membership club for owners called Club Lazydays that

provides benefits like breakfast and lunch when customers are on the premises for repairs and 30%

discounts off area attractions.

Chapter 10 – Strategy and the Master Budget

10–13

Case 10-3: Building Processes for a Solid Financial Foundation—The Case of

Community Health Initiatives

(Source: Sandra Richtermeyer, Strategic Finance, August 2007, pp. 52-57. Note: this case was the case

used as the 2008 IMA Student Case Competition. The Student Case Competition is sponsored annually by

the IMA to provide an opportunity for students to interpret, analyze, evaluate, synthesize, and

communicate a solution to a management accounting problem.)

Overall Case Objectives

1. Primary objective: developing accounting processes to provide decision makers with information useful

for decision support, planning and control.

2. Secondary objective: create a professional development plan for an early career management accountant.

General Context of Case

This case gives students an opportunity to develop and plan accounting processes for an early career accounting

professional (Stephanie) who is making a career transition from auditor (external role) to management

accountant (internal role) in the setting of a nonprofit organization. The case also presents a scenario where

students can learn more about the benefits of the Institute of Management Accountants (IMA) by integrating

Certified Management Accounting (CMA) certification and professional development into the recommendations for

the case.

CASE REQUIREMENTS

Develop a plan for Stephanie to follow over the next three months as she develops accounting processes

that will provide the CHI leadership (executive director and board of directors) with the right type of

information designed to be useful for decision support, planning, and control. In preparing your answer,

you may want to consider some of the specific questions/issues from the case:

▪ How can CHI adopt an effective budget process?

▪ How can CHI demonstrate that their organizational strategy links to their financial information?

▪ How can benchmarking be useful for CHI?

▪ How can Stephanie manage her work relationship with the board of directors and executive

director and evaluate her progress during her first three months on the job?

▪ How can Stephanie develop herself professionally to be prepared for her new challenges at work

Chapter 10 – Strategy and the Master Budget

10–14

High-Level Snapshot of Possible Approaches to Case

Summary of possible recommendations related to primary objective: developing accounting

processes to provide decision makers with information useful for decision support, planning and

control. (See subsequent discussion for more detail and suggestions for each of the points listed

below.)

➢ Develop more formal budget procedures and guidelines.

➢ Determine the “as is” and the “to be” in terms of financial reporting

➢ Develop procedures to monitor metrics and key measures of performance.

➢ Develop benchmarking procedures and educate decision makers on items that may be considered

by charity monitoring organizations.

Summary of possible recommendations related to secondary objective: create a professional

development plan for an early career management accountant. (See discussion below for more detail and

suggestions for each of the points listed below.)

➢ Management accountant (Stephanie) needs to obtain more education on the types of financial

information frequently requested by boards.

➢ Management accountant (Stephanie) develops a plan for her own continued education and

professional development. Possible solutions include CMA certification, CPE courses, IMA

chapter programs, networking with finance directors from similar nonprofits.

Develop more formal budget procedures and guidelines–possible steps:

• Assess the current budgeting style – frequent changes, lack of adherence, limited usability as a

planning and control tool.

• Describe the types of notes/disclosure about assumptions that may accompany the budget

• Require adopted budget procedures to be in place before the beginning of the fiscal year (the case

time frame is four months into the year).

• The budget reporting practices (Table 2) do not provide a format that is useful to compare

specific program budgets. For example, the expenses are not allocated to the programs.

Determine the “as is” and the “to be” in terms of financial reporting

Students should become familiar with the basic nonprofit financial statements prepared under GAAP

(released by the auditor) because that is the best assessment of the “as is” reports. The focus of GAAP–

based audited financial statements for a nonprofit centers on reporting assets, liabilities and net assets

with an emphasis on revenues, expenditures and excess/surplus. A possible solution may compare

components of audited financial statements to reports that are more oriented to specific decisions (such as

program decisions) or that are more “user friendly.” The “to be” statements may incorporate balanced

scorecard, benchmarking reports, reports that illustrate program results, etc.

Chapter 10 – Strategy and the Master Budget

10–15

Develop procedures to monitor metrics and key measures of performance.

• Consider the use of a balanced scorecard (BSC). Develop a sample scorecard linked to the

strategy of the organization.

• Develop a plan to implement the scorecard that includes board training, review and technology

enablement.

• Link the scorecard to incentives for board, employees, program managers, etc.

• Each program could have its own scorecard or there could be an overall organizational scorecard.

Examples of sample metrics for some programs are presented below (best list of metrics for

scorecard is provided in Table 3 of case):

Program: Relief-Travel and Housing Grant Program (sample metrics)

• Number of constituents served in program – metric = flat number or growth rating

• Volunteer management – # new volunteers in program or volunteer retention ratio

• Volunteer satisfaction ratings – use results of volunteer satisfaction survey

• Volunteer assessment ratings – use results of volunteer assessment form

Program: Moving from Dependency to Independency (sample metrics)

• Volunteer satisfaction survey results

• Constituent success ratings

• Level of in–kind services received

Establish Methods of Monitoring Risk Factors

Start by assessing the risk factors listed in Table 4 of case. Students may introduce solutions linked to the

COSO Enterprise Risk Management (ERM) framework. List examples of each type of risk and discuss

with the board. Once the board agrees upon risk factors, determine the best way to monitor the risk and

report back to the board.

External Risk Factors (see Table 4)

Natural environment–protection of assets (including information) from natural disasters, etc. May

include assessment of program sites where constituents and volunteers are present.

Political–new laws and regulations that could affect the nonprofit’s ability to obtain funding or maintain

exempt status. This risk factor is particularly important to consider if the organization relies on

governmental grants.

Social–changing demographics, social mores, family structures and work/life priorities that can affect

programs and contribution revenues.

Technological–ability to use emerging technology to deliver value to constituents of nonprofit. Data

security related to information maintained on employees, constituents, volunteers, donors, etc.